The joy of winning and the pain of losing are right up there with the pain of winning and the joy of losing. Also to consider are the joy and pain of not participating. The relative strengths of these feelings tend to increase with the distance of the trader from his commitment to being a trader. ~ Ed Seykota

In this week’s Dirty Dozen [CHART PACK] we look at supply overhangs and market retracement odds before diving into the virus’ second-order economic impact, then we tally up all the many fiscal and monetary actions taken to date, discuss the poor health of our state finances, and end with a deep cyclical value play. Plus more…

Let’s dive in.

***click charts to enlarge***

- The market ran into a supply overhang at the end of last week. A supply overhang is a price point where many players had previously accumulated shares before prices moved against them, making them underwater on their positions. It’s their breakeven point or close to where they can dump their holdings at only a small loss and breathe a sigh of relief.

Odds now favor 1-2 weeks minimum of sideways to down action from here.

- The NAAIM Exposure Index shows that managers have brought their risk level nearly back up to pre-sell off levels. Nothing like price to change sentiment…

- Deutsche Bank put out a report over the weekend talking about some of the second-order economic impacts of the virus; one of them being tourism and what the lack of travel means for GDP. They noted that “According to the UNTWO, a couple of years ago, tourism was directly the source of 9% of all jobs globally — and for every job in tourism another 1.5 jobs are created.”

- Nomura has created a number of “lockdown trackers” to show how much of the global economy is in shutdown. Here’s the tracker showing how much of the global populace “should” be on lockdown in accordance with government mandates.

![]()

- And this one uses alternative data to show what people are “actually” doing.

![]()

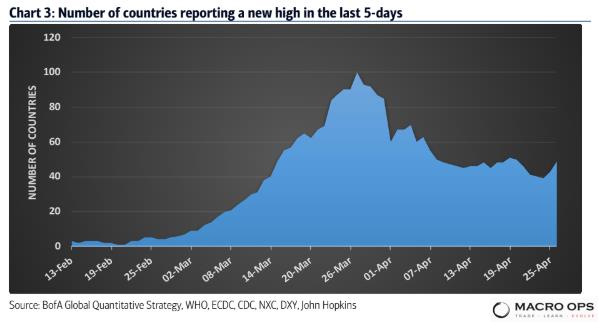

- BofA reported that “The number of countries (> 50 cases) reporting a new high in daily cases in the preceding five days is down from 102 (March 27th) to 49 (April 26th). A risk to monitor is a second wave of new cases as measures to slow the spread of the virus are eased”.

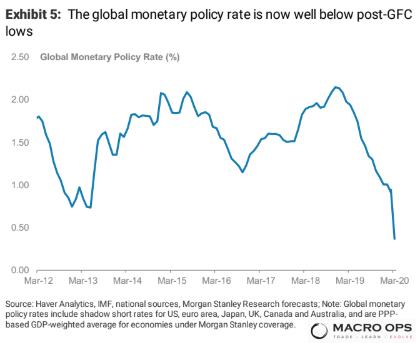

- Morgan Stanley detailed the aggressive monetary and fiscal policy to date, writing (with emphasis from me) “Since mid-January, all of the central banks we cover have eased monetary policy. The global weighted average policy rate has declined to below post-GFC lows — rates have fallen by 64bps since December 2019 and 177bps since December 2018. G4 central banks have announced aggressive quantitative easing programs. We estimate that G4 central banks will make asset purchases of ~ US$13 trillion in this easing cycle. The Fed alone will make cumulative asset purchases of ~US$7.8 trillion.”

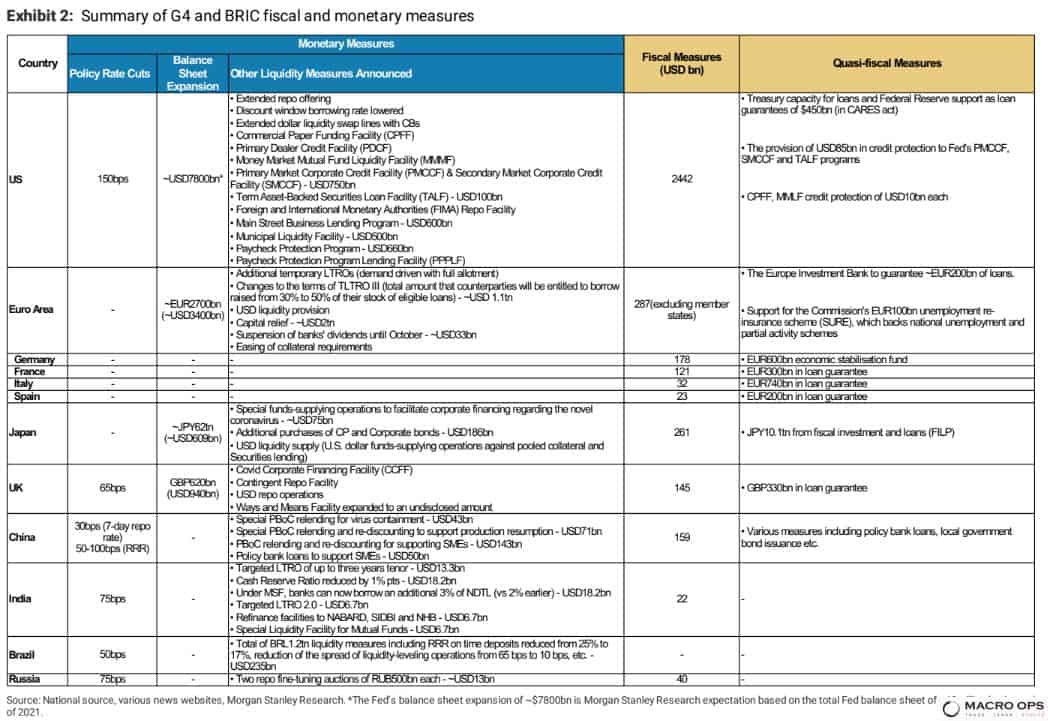

- Here’s a running tally from them of all the global monetary and fiscal measures announced to date (click chart to enlarge).

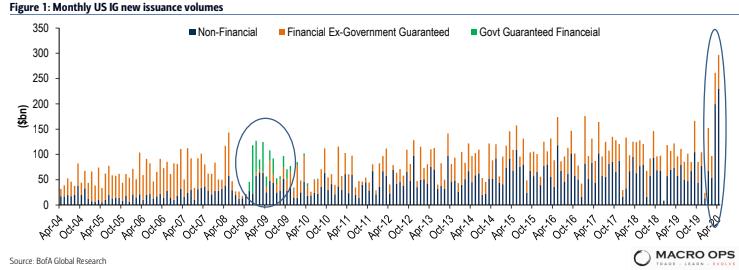

- Thank Zeus the money spigots are on or else we would have seen massive credit cascades. This chart shows a lot of companies are raising a lot of money as IG new issuance crushes the former records.

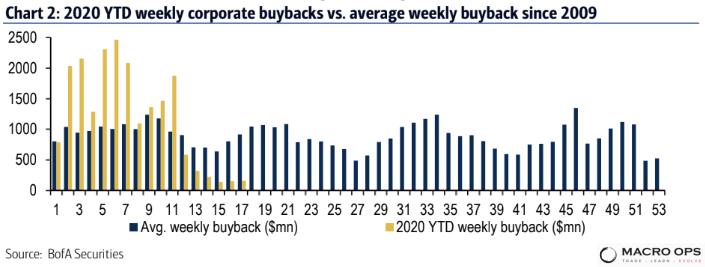

- While at the same time companies are slashing buybacks and dividends. Buybacks have been an important source of equity demand this cycle and so this trend matters a lot going forward. While many people rightly point out that there’s not a one-for-one relationship between buybacks and the market’s performance, it’s the long-term impact to the supply/demand equation for the market where this shows up.

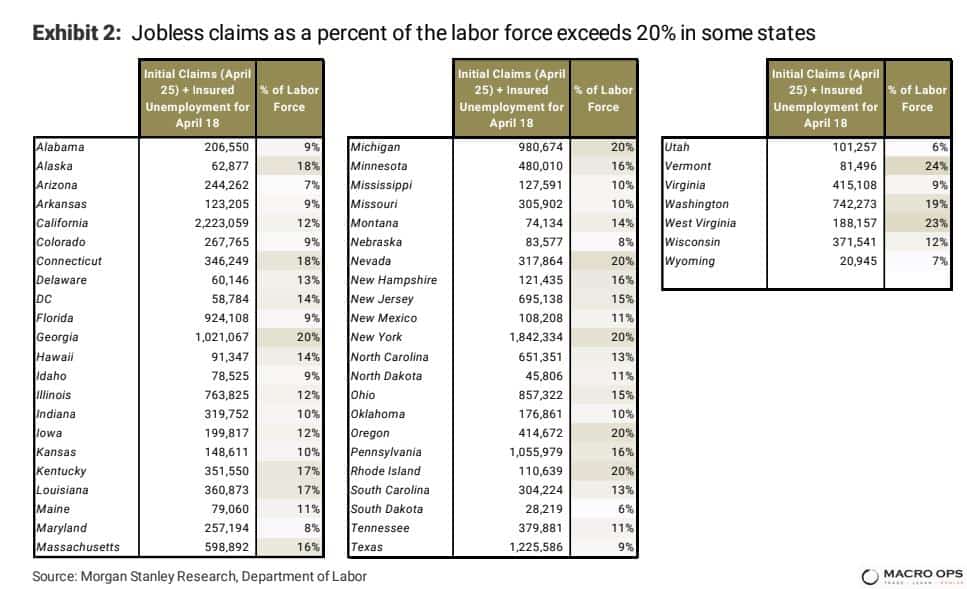

- Morgan Stanley pointed out the troubling state of many State finances due to lockdown measures. They wrote, “Joblessness is reducing taxable income, declining retail activity impedes sales tax, weak stock markets stunt capital gains tax revenue, and the decline in the price of oil hurts severance (natural resources extraction) tax revenue.”

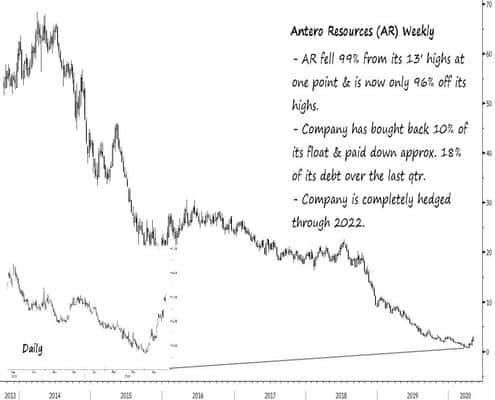

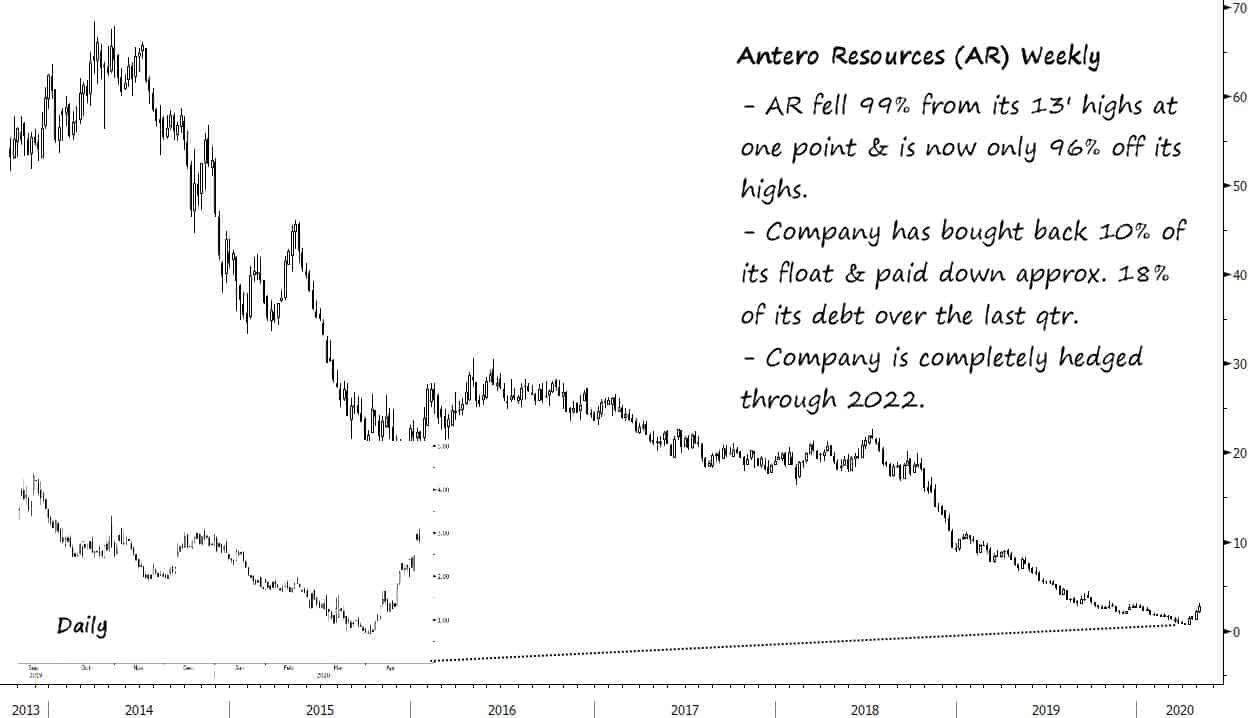

- There’s always a bull market somewhere as Jimmy Buffett would, I’m sure, say if he were an investor. Natural gas is a case in point. Look out past the near-term futures and the charts look good. Antero Resources (AR) is one of a number of good plays on this theme. Capped downside and LOTs of upside, which is what I like to find in a trade. I’m in the process of doing a deep dive into the space that I hope to share with fellow Collective members later this week.

Stay safe out there and keep your head on a swivel.