Through bitter experience, I have learned that a mistake in position correlation is the root of some of the most serious problems in trading. If you have eight highly correlated positions, then you are really trading one position that is eight times as large. ~ Bruce Kovner

Good morning!

In this week’s Dirty Dozen [CHART PACK] we look at the latest credit, fiscal, and monetary data points from around the world. We then talk about the widening US deficit and what that could mean for the US dollar. We end with some sentiment and positioning, take a look at buybacks, as well as a stock that’s set to benefit from the strong US housing market. Plus more…

Let’s dive in.

***click charts to enlarge***

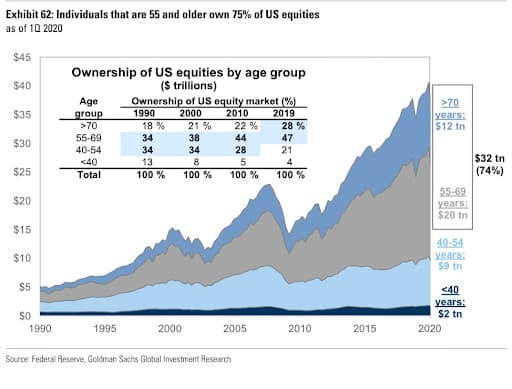

1. @Callum_Thomas shared this chart from GS on the twitters last week, showing equity ownership in the US broken down by age group. What’s interesting is that those in the 55-year and over group have seen their share of equity ownership climb from 52% in 1990 to 75% today. This is another one of those pernicious effects of the long-term debt cycle which has led to the current wealth and income divide we see today.

2. China was the country that saved the global economy from slipping into a much more painful and prolonged economic depression in the 2010s following the GFC, thanks to their China-sized fiscal stimulus. While China has once again turned on the liquidity spigots in response to COVID, their ability to drive credit growth has become diminished. You can only build so many ghost towns, high-speed rail lines, and bridges to nowhere before you start to see a negative impulse from investment.

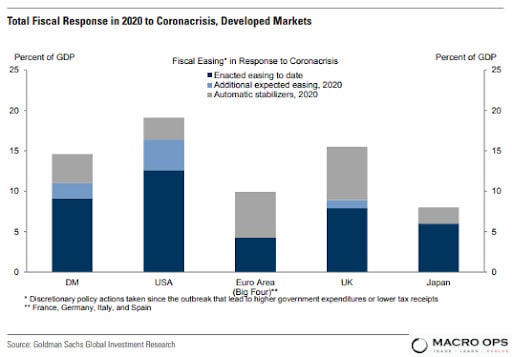

3. Luckily for markets though, the rest of the world has aggressively stepped up to the fiscal plate. Here’s GS’s latest summation of the total fiscal response year-to-date. The numbers are mind-boggling…

4. The fiscal response along with a weakening dollar has helped put a bottom under EM markets.

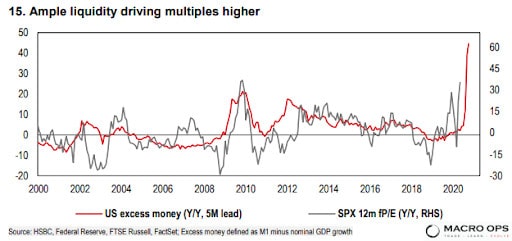

5. And this chart from HSBC shows that US excess money Y/Y has a high leading correlation (5-months) to multiple expansion in the SPX.

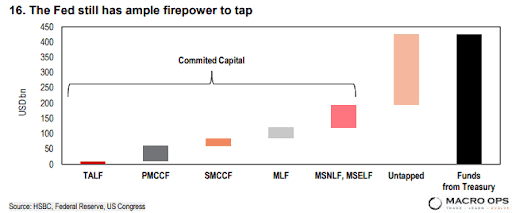

6. The question for markets looking forward is will the liquidity hose continue to spray at full bore? While the fiscal side is looking more precarious in the US with debates over extending the additional UI benefits, HSBC points out that the Fed still has plenty of room to maneuver, noting:

“So far the Fed has only tapped c45% of the total funds from the US Treasury, according to our credit strategists. In other words, the Fed still has ample firepower to combat any deterioration in financial conditions and risk-off waves in markets.”

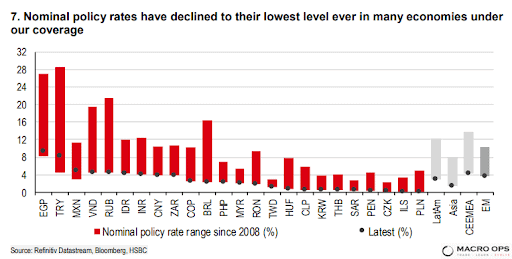

7. Nominal policy rates across the EM world have fallen to their lowest levels ever. What happens if this trend continues and the entire world effectively ends up at the zero-lower-bound?

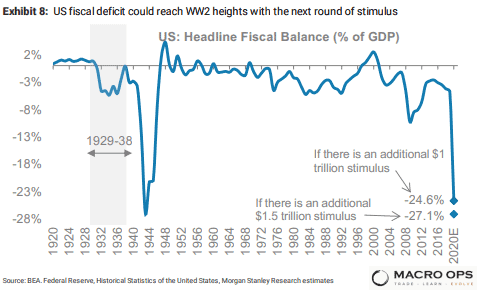

8. I know we live in a post-deficits-matter world with MMT and all… But, the US fiscal balance is set to reach the peak hit during WW2 with the next round of stimulus. At some point, the US’s financing needs will begin to surpass the structural demand for those safe assets. And we’ll see that imbalance correct itself either in higher interest rates or a lower dollar. My money is on the latter.

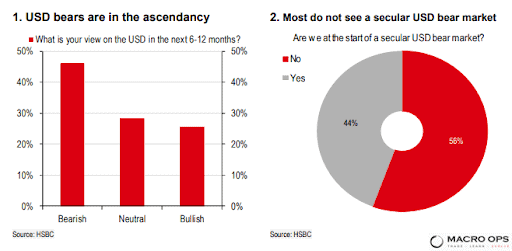

9. Speaking of the US dollar… HSBC’s latest survey shows that USD bears are in the ascendancy. On the surface, this would appear to be a check against the USD bear thesis. However, as the USD chart on the right shows. Most of the respondents believe the USD bear trend is nearer its end than its beginning.

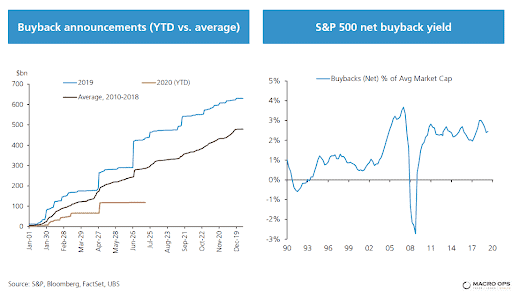

10. Buybacks are an integral part of my macro fundamental framework. A high net buyback yield (buybacks-net issuance) has kept this bull alive for much of the cycle. With announced buybacks off to a slow start for the year, it’s yet to be seen whether this fundamental driver can keep the party going.

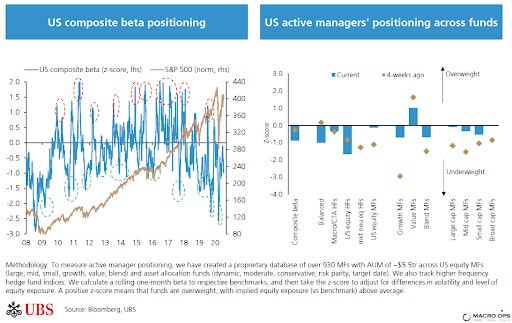

11. Those who still think this bullish rise in risk-assets makes “no-sense” have not been looking at the right data points. We have record-breaking levels of fiscal easing and stubborn bearish sentiment/positioning coming off record lows. That’s it. That’s the bull case.

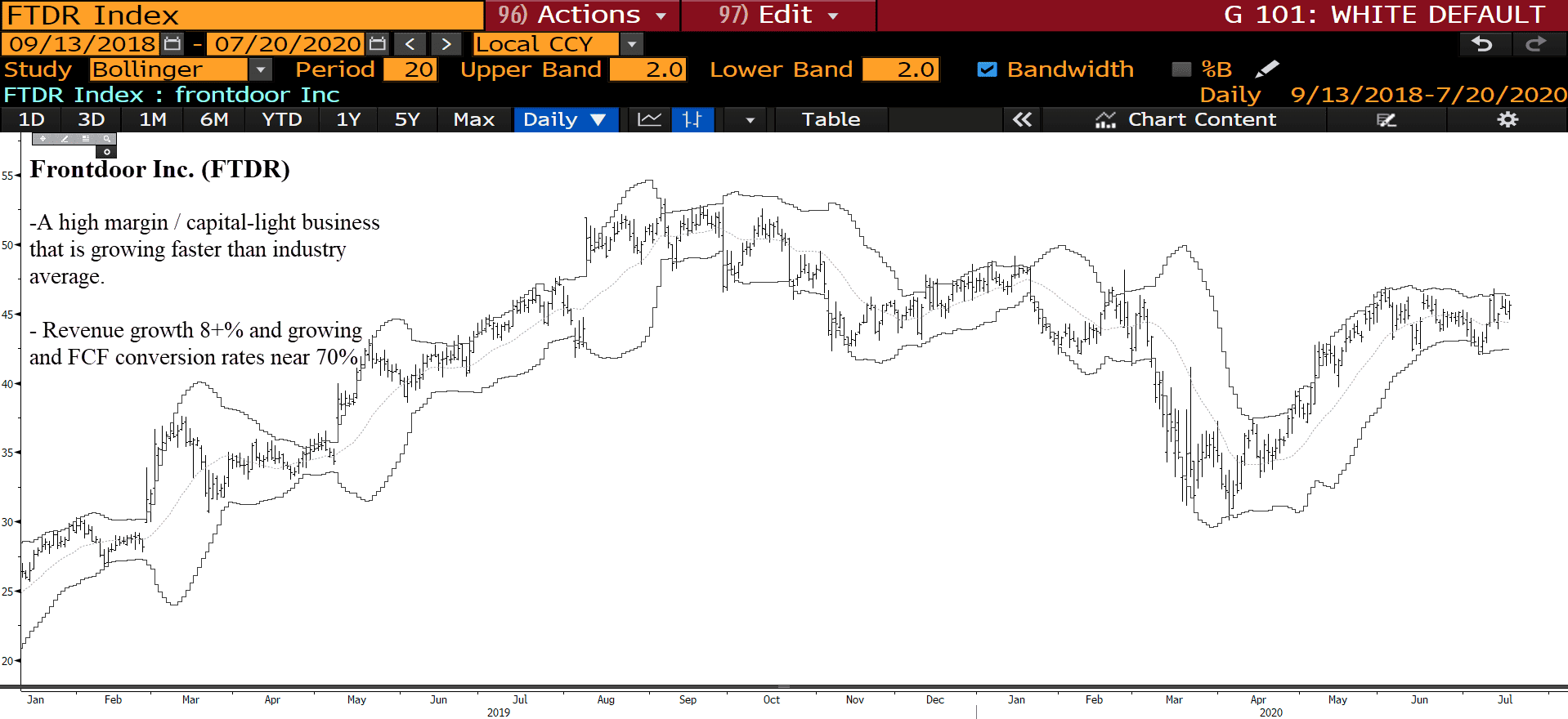

12. In Tim Duy’s latest “Fed Watch” note on the economy, he comments on the returning strength of the housing market (link here). A favorite play of ours to participate in this thematic is the home services plan company, Frontdoor Inc (FTDR). Brandon put out an update on this stock back in April when it was trading around $36 — Collective members can find the report hung up in our Research Library.

Stay safe out there and keep your head on a swivel.