I have a friend who has amassed a fortune in excess of $100 million. He taught me two basic lessons. First, if you never bet your lifestyle, from a trading standpoint, nothing bad will ever happen to you. Second, if you know what the worst possible outcome is, it gives you tremendous freedom. The truth is that, while you can’t quantify reward, you can quantify risk . ~ Larry Hite

Good morning!

In this week’s Dirty Dozen [CHART PACK] we cover wide-scale insider-buying in energy and financials, talk about the troubling dearth of CAPEX intentions in the IT space, discuss the ugly earnings trends, make the case for fiscal, throw some rocks at the FANG trend, and end with a long pitch for a fintech advertising company. Plus more …

Let’s dive in.

***click charts to enlarge***

- Jesse Stine published a market note this past where he shared some great charts like the one below as well as his take on the market, which I find myself in much agreement with. Here’s a link to the report and an excerpt:

“As we see trillionaires AAPL, AMZN, MSFT, and stuff like TSLA single-handedly dragging the indexes higher day after day after day after day, the vast majority of the market hasn’t gone anywhere in 3 months. My point here is that there’s very little “froth” in 95% of the U.S. market and/or global markets. Thus, it’s difficult to argue for a “crash” on the horizon for a majority of stocks. I’d love to see money rotate out of the trillionaires into the rest of the market. We rarely see such orderly rotation out of the big boys, but you never know.”

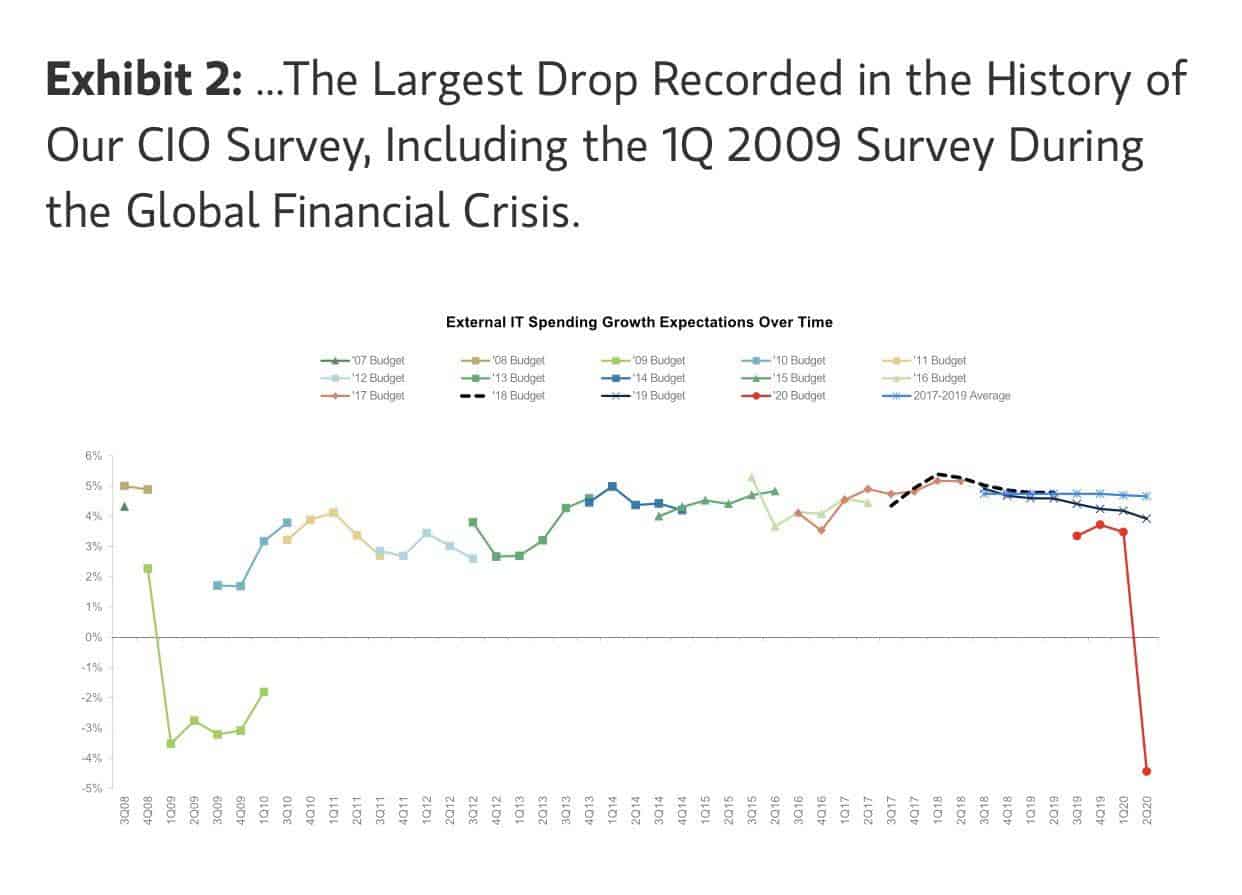

- @GavinSBaker shared this chart from the recent MS CIO Survey showing that IT Spend Intentions are down -4.4% YoY, marking the first decline in a decade and the largest decline + negative revision on record… This matters because one person’s (or company’s) spending (CAPEX) is another’s profits. If companies don’t become more optimistic about the future and ramp their CAPEX back up, well, then… let’s just say the market rodeo that started in February is only just beginning.

- The earnings picture is more precarious once you take into account the fact that the trend was down and out before COVID even hit. This market is being propped up purely by TINA (fat relative risk premiums) and fiscal injections. Nothing wrong with that. I mean, I trade the trend and am definitely no financial justice warrior… But, at some point this becomes unsustainable.

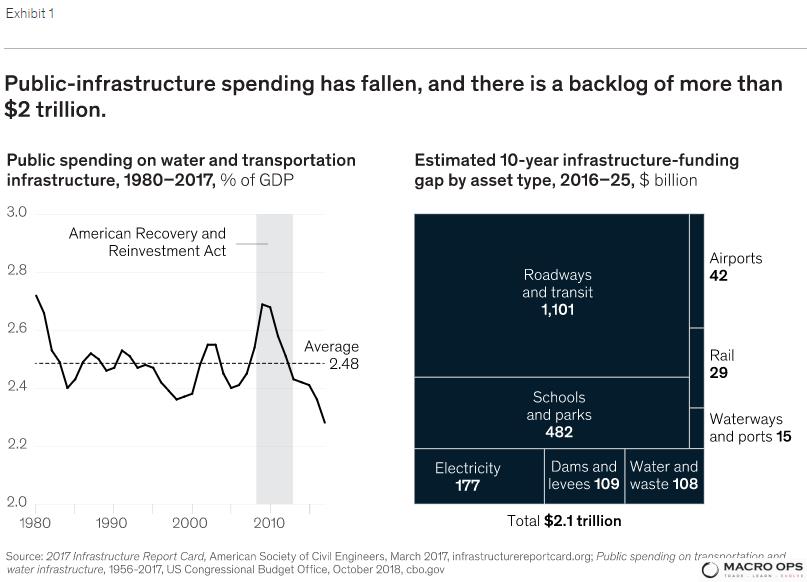

- What this economy needs and needs soon considering COVID cases are spiking again and another round of lockdowns now seems all but inevitable in large parts of the country, is a new New Deal. We need to get fiscal. Like, really fiscal. And invest in our declining capital stock. You know, build some roads and bridges. And better yet, some small modular nuclear power plants! And luckily for us, according to this report from McKinsey, there’s a lot of low hanging high return fruit available for us to choose from.

- Of course, who really cares about fiscal, CAPEX, and future earnings when you can just pile your money into the narrowing leadership of the very top-heavy Nasdaq.

- I prefer to ride freight trains, not step in front of them. That’s why I’m not looking to short this buy climax we’re seeing in the FANG stocks — not until the tape says so, at least! But, I do enjoy pointing out the signs of increasing fragility within the trend. And on that note, here’s one more. Short interest in FANG stocks just fell to a record low, below 1% of float (chart via BofA).

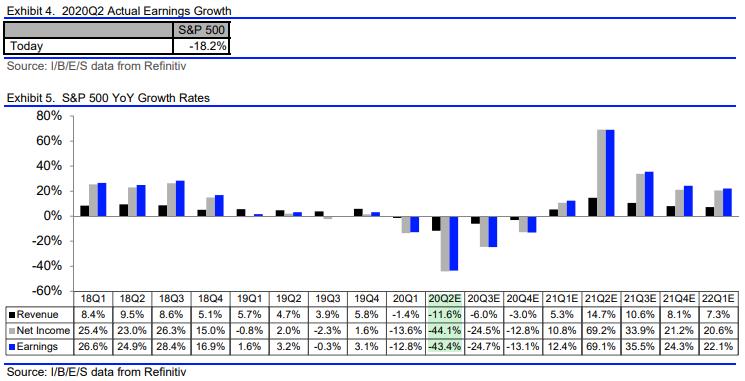

- Q2 earnings season is about to pick up and lucky for the market the consensus estimates are… how do you say… dour? 20Q2 earnings are expected to decrease 43.1% from 19Q2. The low bar is set, now let’s see if the market can clear it!

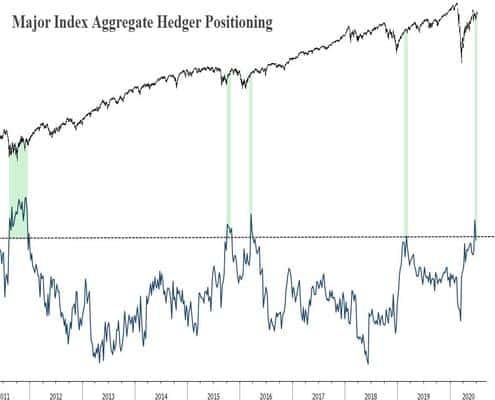

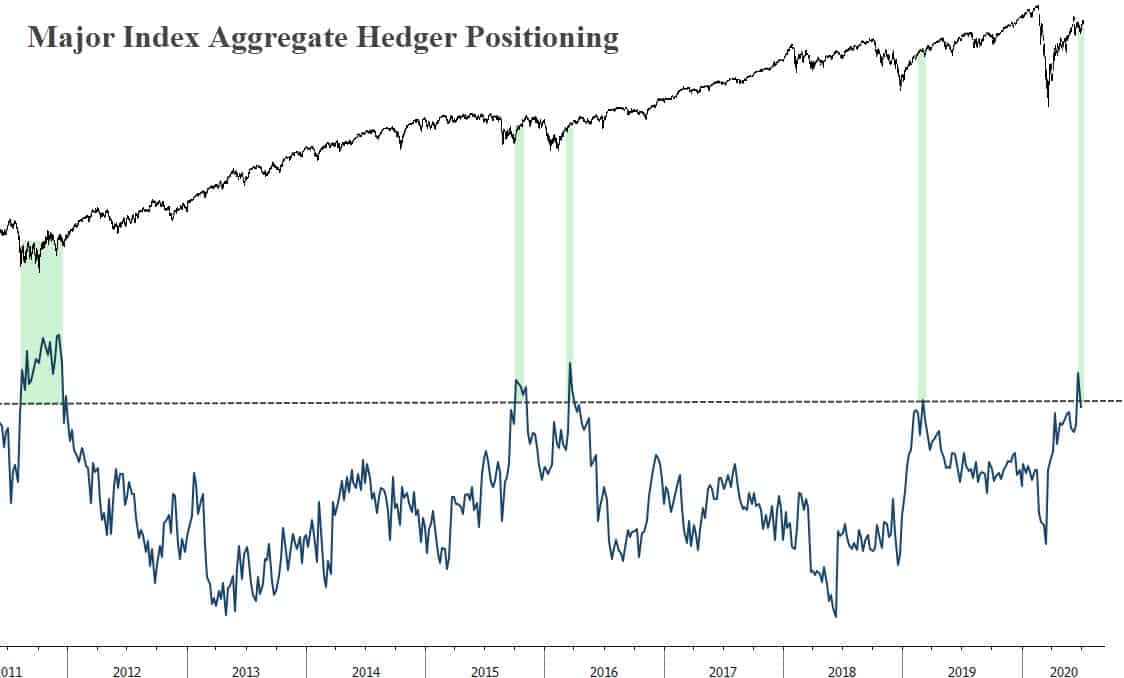

- It seems that analysts aren’t the only ones with pessimistic outlooks. Combined US Index Commercial positioning (the opposite of speculative positioning) is at 5yrs highs — levels that typically mark bottoms, not tops.

- Personally, I’m in the camp that the rise of the Robinhood trader’s impact on the market is overblown, except for in smaller less liquid areas of the market. With that said, they seem to definitely be skewing the options market and, I think, are largely behind the extreme Put/Call ratios these last few weeks. The following is from a NYT article via a tweet from @MacroCharts.

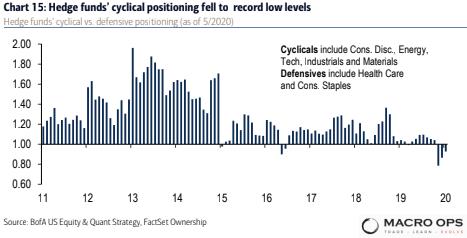

- I knew cyclicals were out of favor and all but I didn’t know it was this bad. Apparently, hedge fund positioning in cyclical stocks (think consumer discretionary, energy, industrials etc…) recently hit all-time record lows…

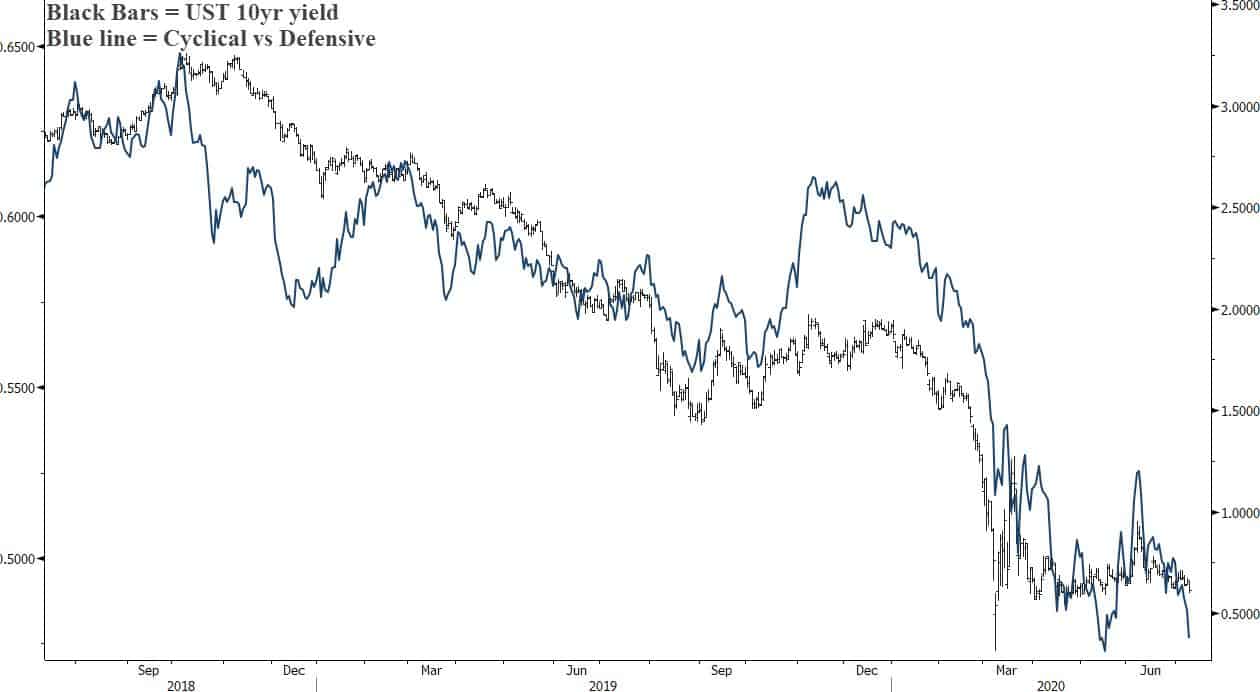

- But I get it… They’ve done nothing but go down or sideways as of late. Which reminds me, they’re suggesting that bonds might make a better investment. Bonds (below is bond yields) continue to give those long risk, a free hedge. Not sure how much longer this will last, but why not ride the trend until it bends?

- Cardlytics Inc (CDLX) is a well-run fast-growing company. Brandon, our resident value investor extraordinaire, pitched this one to fellow Collective members back in April. The stock has since risen 80% and still looks like a good buy (it’s breaking out of a month + long wedge as we speak). Operators can find the report hung up in our internal research page.

Stay safe out there and keep your head on a swivel.