I have resigned from the professional undertaking of coin-flipping. I am not here to tell you where gold’s gonna be. I have no idea. That’s my existentialism. I am a student of uncertainty. I have no idea where the stock market is going to be. So when I am creating trades in my portfolio for my clients, I am agnostic. I just want to enhance the probability that I make money come what may. ~ Hugh Hendry

In this week’s Dirty Dozen [CHART PACK] we look at the latest Global Fund Manager Survey data, walk through the growth versus value debate, look at falling capex in the oil and gas space, before discussing the dollar, the fall of empires, and recent COVID-19 growth numbers, plus more…

Let’s dive in.

***click charts to enlarge***

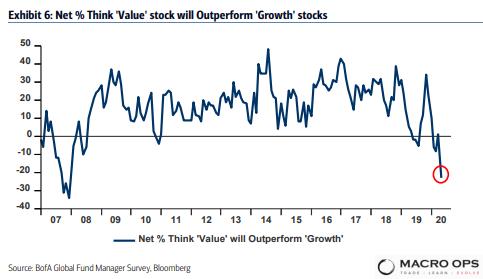

- BofA’s latest Global Fund Manager Survey (FMS) came out last week. Here are the highlights from the report. Summary: lots of bearishness and the pain trade is up in credit and equities.

- I like this chart. It shows that the lowest net % of respondents since 08’ think value with outperform growth. Now, I’m never one to fight a trend or step in front of a momentum train. But… we gotta be nearing the point where this theme becomes so disconnected from any possible future outcome that the mean reversion of reality will begin to kick in. I mean, there’s a lot priced in here.

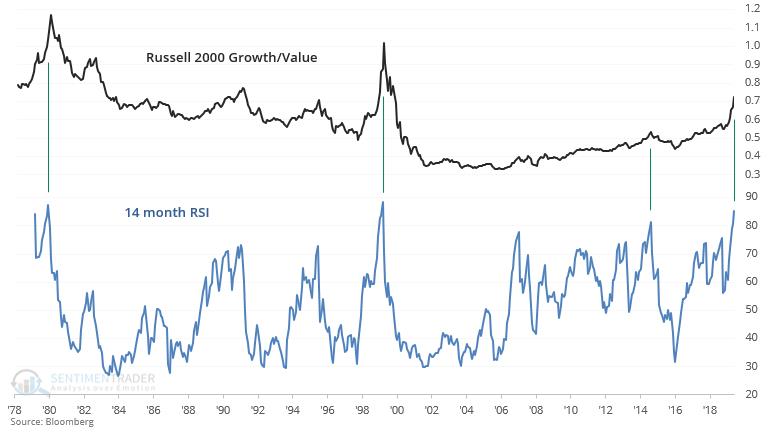

- In a similar vein, SentimenTrader shows how extended this trend has become. “Russell Growth/Value ratio’s 14 month RSI right now is among the *HIGHEST* readings ever.

This only happened:

Feb 1980: stocks crashed next month in March 1980

Dec 1999: near end of dot-com bubble

July 2015: stocks crashed next month in Aug 2015”

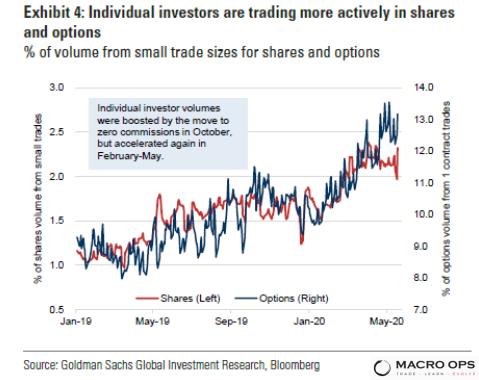

- The trend is certainly being helped along by COVID-19, stimulus checks, and a new generation of speculators coming into the market for the first time. Goldman Sachs recently pointed out that “Trades consisting of just one contract now account for 13% of total volume.” And Bloomberg noted last week in a report that “In some popular stocks, like CMG and GOOGL, small options trades account for nearly ⅓ of total volume.”

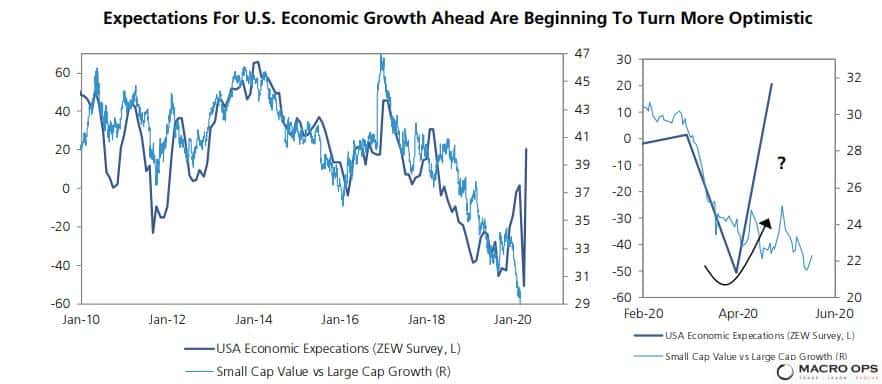

- UBS thinks this period of historic underperformance from value may be coming to an end.

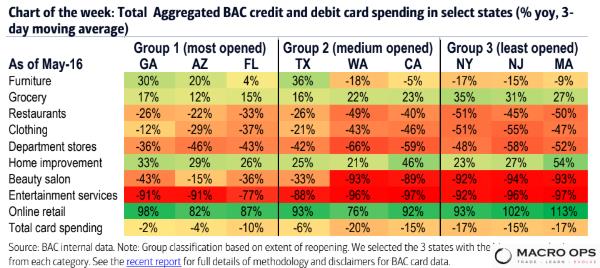

- Though this aggregated BAC credit and debit card spending by state data does show that the virus has caused a rift, essentially creating two separate economies. What macro hedge fund manager, Jim Leitner, calls the “dual economy of bits and things” in this recent Macro Hive podcast (link here).

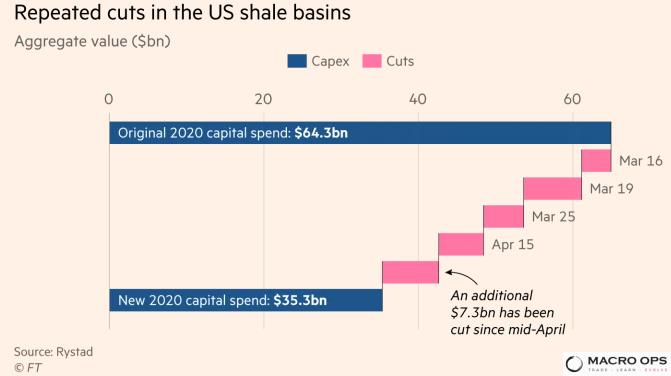

- The FT published an article over the weekend titled “Boom to bust in the US shale heartlands” that’s worth a quick read (link here). With current prices well below the lowest average breakeven rates of some of the best US basins, companies are having to dramatically reduce capex spend, which was already on the low side. They say the cure for low prices is lower prices. This is the capital cycle at work. Lots of future opportunities will be born out of this.

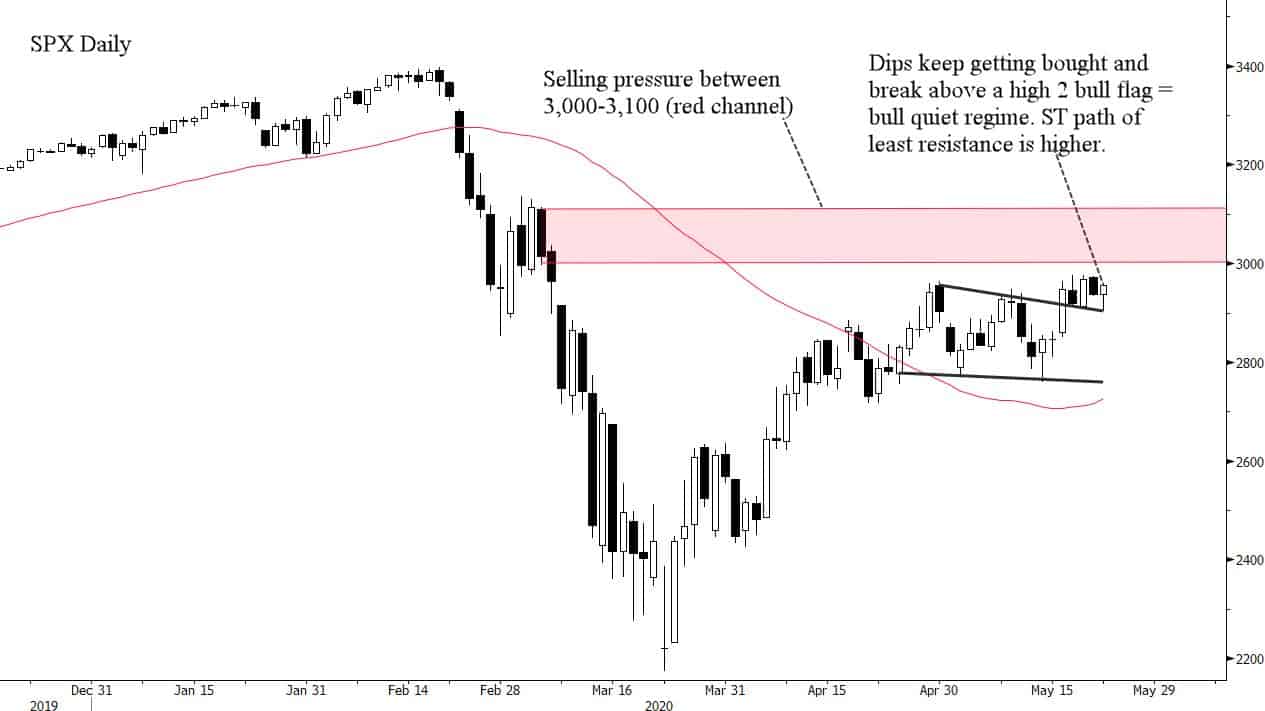

- While the SPX is set to run into some selling pressure in the 3,000-3,100 range, the short-term path of least resistance remains up. When every sell setup fails and every dip gets forcefully bought, it’s a sign that the market is in a bull quiet regime. I think it’ll likely turn in the next 1-2 weeks but we need to wait for the market to change its tone. Until then, higher we go…

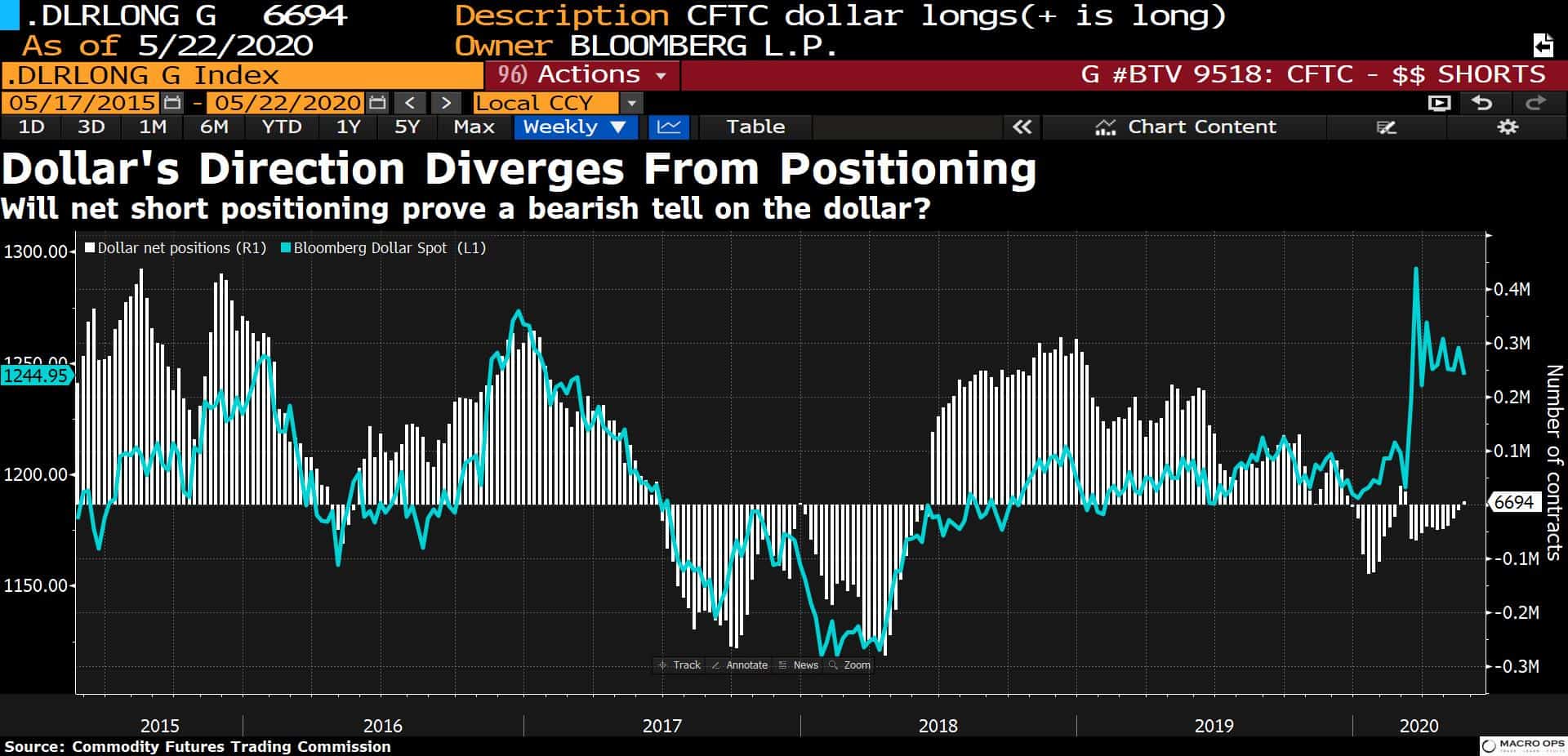

- I think the second half of this year is going to be fireworks in the DM FX market. There’s a lot of tight coiling going on — many springboards being geared up for launch. While I have my biases, I’m trying to stay agnostic on direction and will let the market dictate my trading. This chart from Bloomberg shows that positioning has not followed the move higher in DXY.

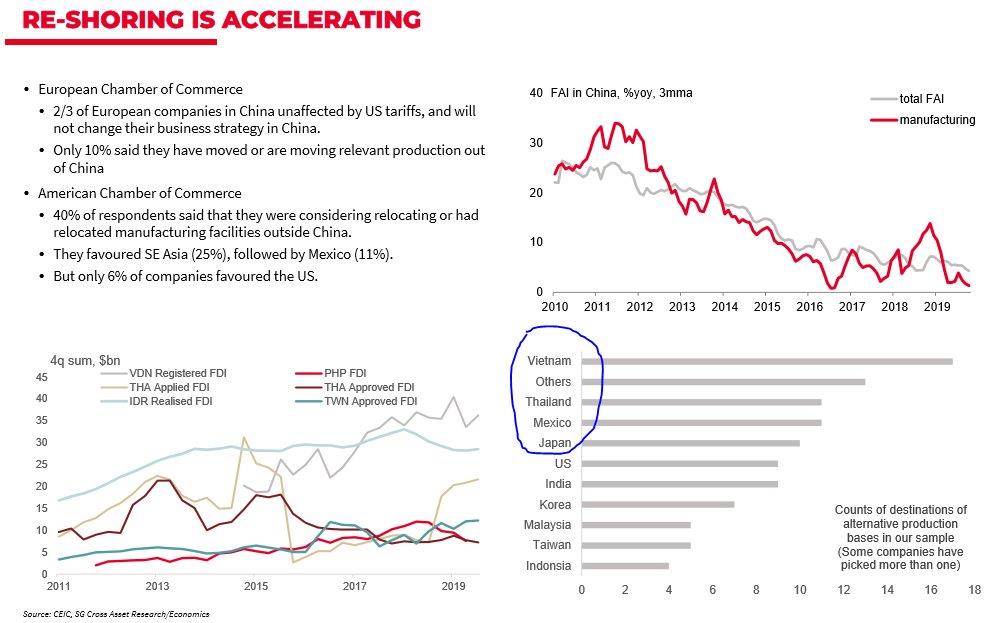

- My friend Kean Chan (@keanferdy) shared this great slide on the twitters recently showing how COVID-19 and souring US-China relations are accelerating the trend of deglobalization and reshoring. Mexico and Malaysia are two countries I’m a long-term bull on and this is one of the reasons why.

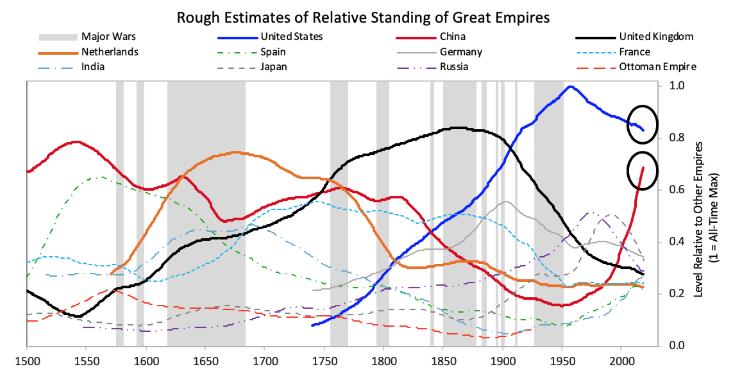

- Ray Dalio published his latest post in his “The Changing World Order” series (link here). It’s a good read and I appreciate how he attempts to quantify the various inputs that drive the rise and fall of empires. There’s some interesting stats in the post. But one area where I completely disagree with Dalio on — and I plan to write a post on this soon — is his blind bullishness on China. I’m of the very strong opinion that China will be a shell of its current self in 20-30 years’ time. Debt, history, and inherent regime fragility nearly ensure it.

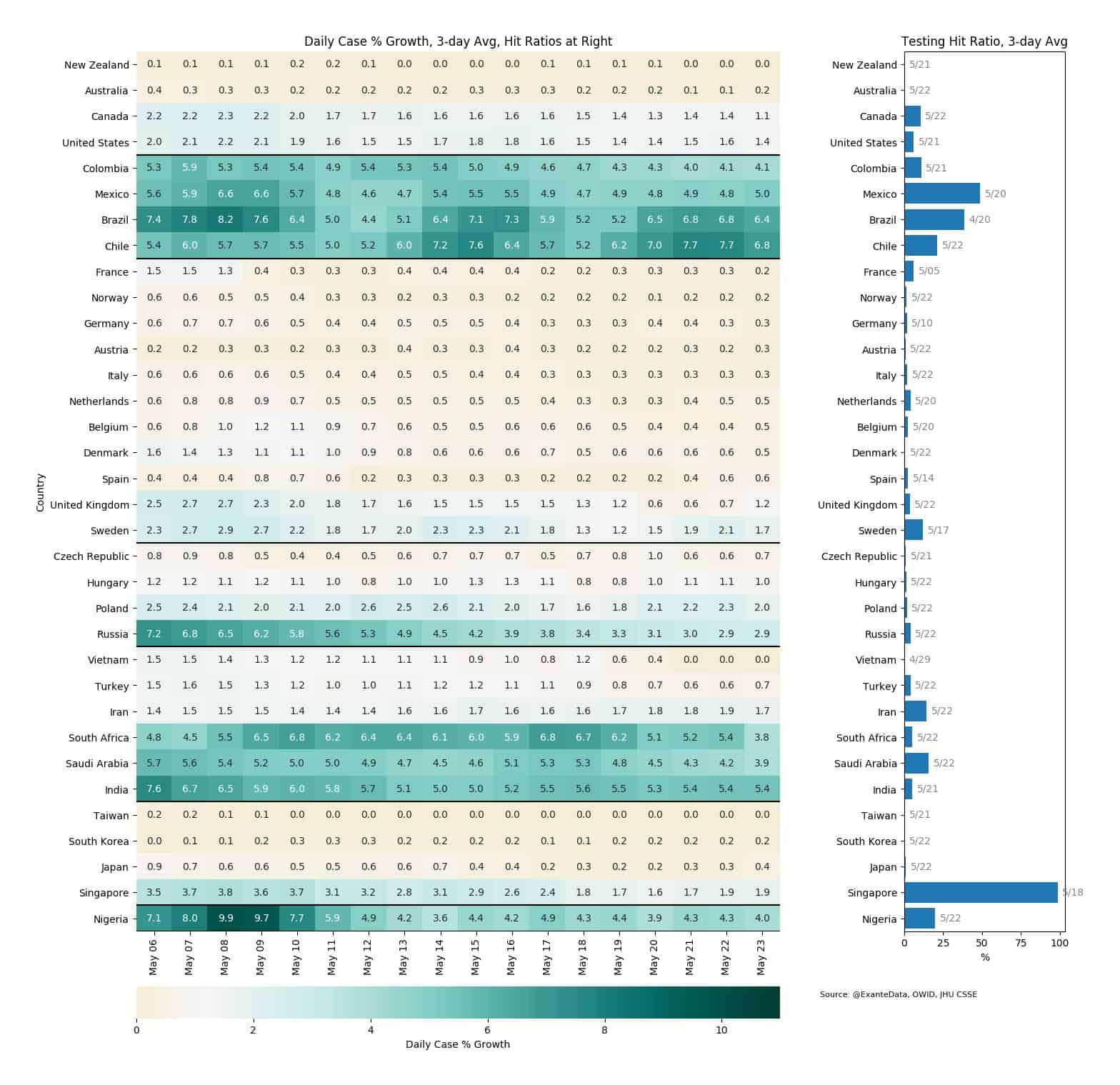

- This heatmap from Exante Data shows the trend of daily growth in confirmed COVID cases across countries. Chile, Brazil, and India have the highest 3-day growth trends of the bunch.

Stay safe out there and keep your head on a swivel.