Mister Spex (MRX) is Europe’s largest digitally native omnichannel retailer for eyewear products. The company sits at the inflection of three major structural tailwinds for eyewear.

Additionally, European eyewear sales sport one of any consumer product’s lowest online adoption rates (10%). Online adoption should rapidly increase as millennials and Gen Z enter their prime eyewear buying years in the coming decade.

Though a digitally native company, MRX invests heavily in building brick and mortar retail stores to better serve its customers. The strategy is working. The company captures 2x the market share in regions with physical stores while seeing a 22% increase in online orders.

MRX has experienced a 60% organic revenue growth CAGR since its founding in 2008 and is EBITDA profitable.

The company expects to generate mid-to-high 20% revenue growth while expanding EBITDA margins to the mid-double-digits.

Despite these attractive qualities, the stock is down 50%+ from its IPO price, thanks in most part to a minor downward revision in Q3 revenue and EBITDA guidance.

The share price decline creates an attractive value opportunity as the stock now trades for a fraction of what it could be worth in five years. And if MRX generates anything remotely close to its guided estimates, the stock likely has a 500%+ upside from here.

We begin this write-up with an overview of MRX’s addressable market and its various tailwinds for growth. Then, we address the existing competition and MRX’s position in the market.

Finally, we conclude with an overview of MRX’s customer value proposition, its brick-and-mortar strategy, and what the business might look like over the next five years.

Excited yet? Let’s dive in.

Structural Tailwinds for Eyewear

There are three layers to MRX’s potential TAM:

- German eyewear market: EUR 6B

- European eyewear market: EUR 32B

- Global eyewear market: EUR 105B

As of 2020, the company’s captured ~2.5% of its core German eyewear market. In other words, there is significant room for revenue expansion.

We can distill MRX’s TAM growth drivers into three levers:

- Growing myopia prevalence

- By 2050 there will be 4.8B people with myopia

- Digitally native cohorts entering prime eyewear buying years

- 20 to 44-year-olds are going to start needing glasses

- For example, 74% of 45 to 59-year-olds wear prescription glasses

- A growing trend in eyewear as fashion

- 69% of Millennials and 65% of Gen Z view glasses as part of fashion trends

MRX is at the inflection point between the above structural macro tailwinds and a rapid increase in online adoption rates in its industry.

MRX and The Existing Competition

We can think of MRX and its competition along an X, Y-axis focused on digitization and fashion. MRX sits at the top right on the graph with Warby Parker (WRBY). These are the most digitally native and most fashion-forward brands.

Then there are the less-digital, less-fashionable competitors like mom and pop shops. These are independent opticians and retail chains without a strong digital presence.

Specifically, MRX competes with the likes of:

- GrandVision

- Fielmann

- Online retailers

- Drug stores

- Mass and general retailers

- Independent Opticians

Existing competitors verified the disruptive nature of MRX’s digitally-first business model. The company notes in the IPO Prospectus (emphasis mine):

“In Germany, for example, the German Central Association of Opticians and Optometrists (Zentralverband der Augenoptiker und Optometristen – ZVA) published a position paper in July 2020 in an effort to sway public opinion stating that the trade with prescription glasses on the Internet could not guarantee a professional manufacture and individual fitting of prescription glasses.”

The best form of flattery, right?

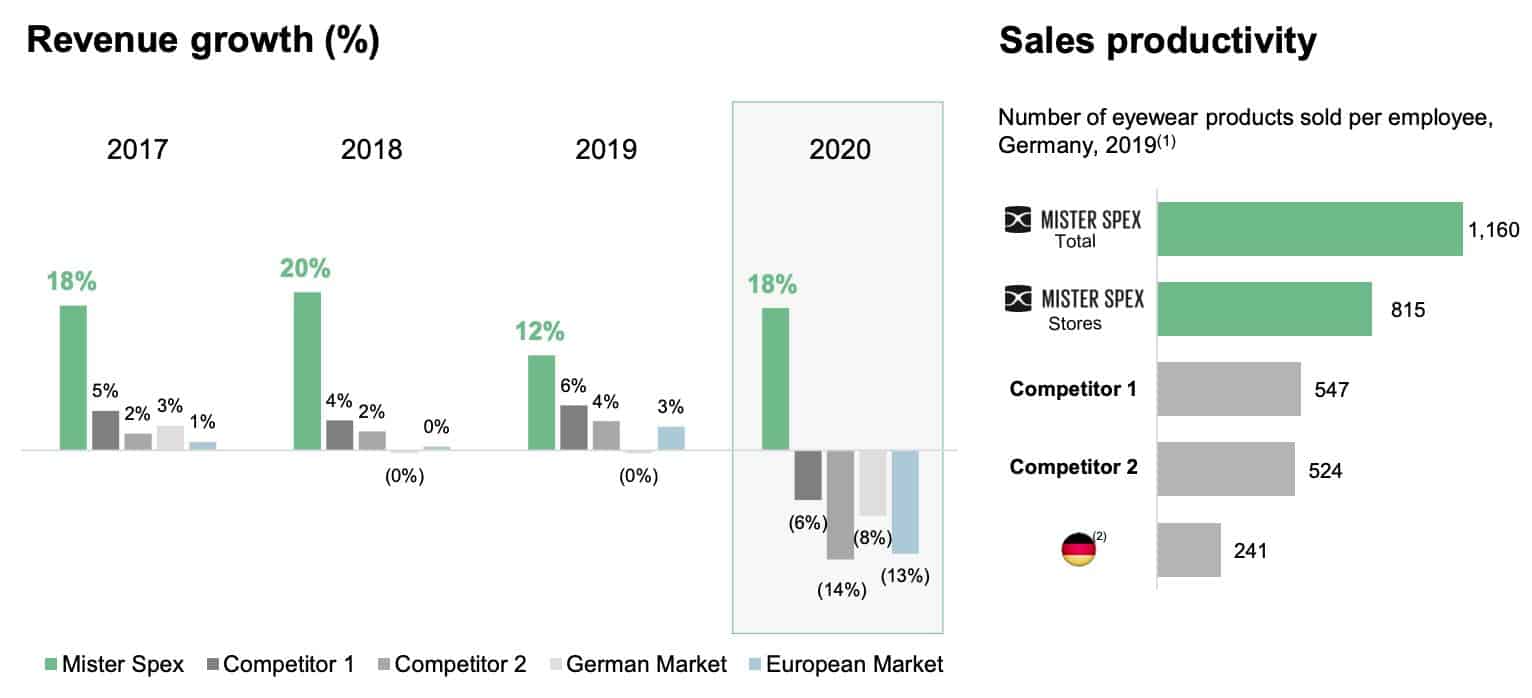

MRX has dominated its competition over the last four years. Check out the graphic below highlighting MRX’s torrid revenue growth rates versus its nearest competitors.

The company sells more than 2x the number of eyewear products per employee than the next closest competitor. These advantages — stronger average EBITDA margins and a more robust, digitally-first business model — are what separate MRX from the pack. MRX truly believes this and said as much in its IPO prospectus (emphasis mine):

“We believe that there is no competitor with a comparable offering: Our online-driven omnichannel approach combines the conveniences of online shopping and offline offerings, allowing us to respond flexibly to the different needs of our customers.”

One explanation for their industry-leading growth is the company’s largest assortment of eyewear products in Europe.

MRX Product Offering

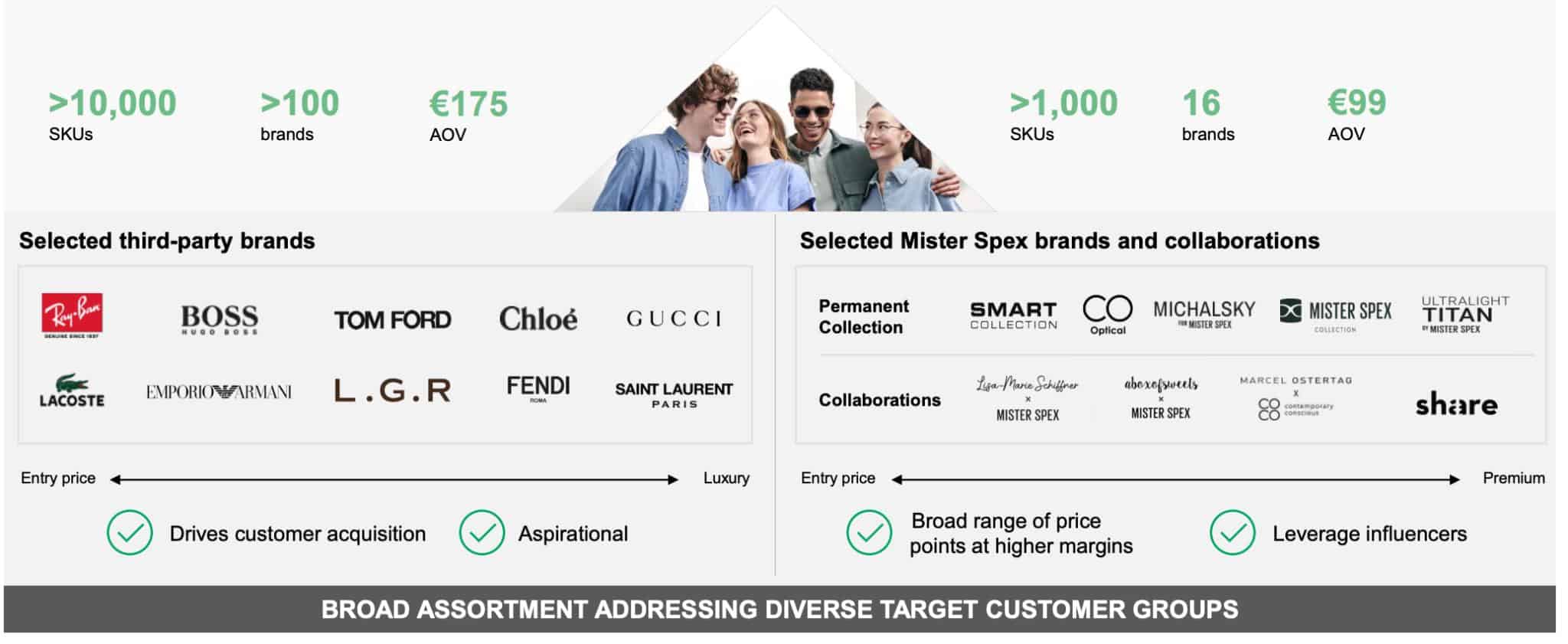

The company offers both own-brand and third-party eyewear products to create the largest assortment of eyewear in Europe.

- 3P Products: >10K SKUs, EUR 175 AOV

- Own-brand: >1K SKUs, EUR 99 AOV

MRX differs from its US peer, Warby Parker (WRBY), which sells only own-brand products.

Which is the better offering?

Most eyewear purchases are non-discretionary. When making non-discretionary purchases, consumers tend to care more about assortment than brands. In other words, since the customer must buy glasses, they’d rather see all available options.

MRX drives higher engagement and more customers through its channels by offering more SKUs. Selling third-party products also insulate MRX from competitors as they see the company not as a threat but as another distribution channel.

We see confirmation of this through EssilorLuxxotica’s 11% investment in the company (which they raised during the IPO from 8%).

The company wants to expand its share of prescription lens sales, which makes sense. Prescription lenses are one of the highest margin products in all eyewear. On average, prescription eyewear commands 70%+ gross margins and over 20% EBITDA margins.

MRX isn’t resting on its purely digital laurels, however. The company is aggressively building retail stores to capture more market share and convert more users to higher-paying customers. Let’s see how they’re doing it.

Benefits of Brick and Mortar Stores

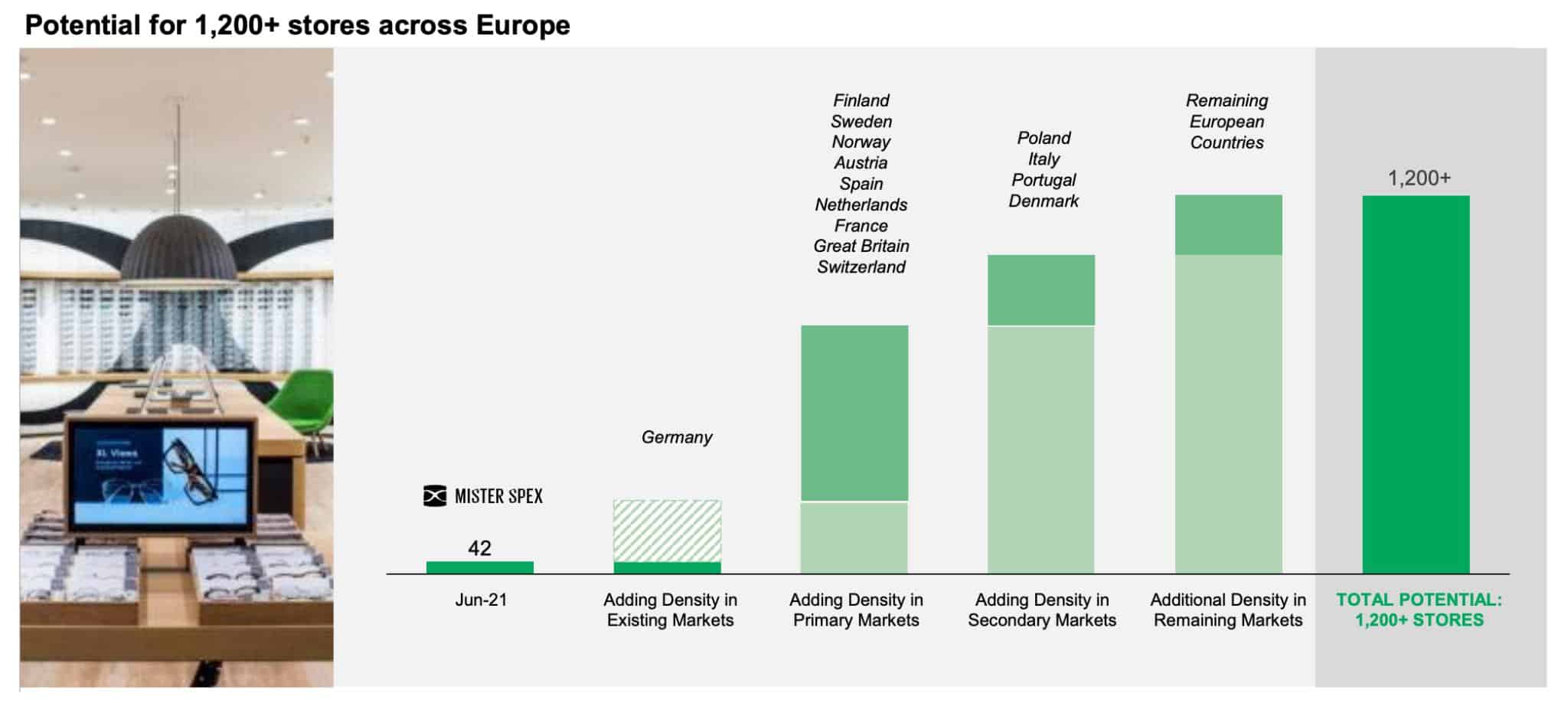

MRX has 48 brick and mortar locations throughout Germany with plans to reach 200 over 3-5 years. Looking beyond the company’s homeland, MRX sees another 1,000+ store locations throughout Europe.

Why build stores in the first place? There are a couple of reasons.

First, MRX increases its market share by ~2x in regions that have retail locations.

Second, regions with brick and mortar stores buy 22% more products online than non-store regions.

In other words, MRX generates a retail flywheel where each store attracts more customers, buying more products offline and online.

Brick and mortar stores also allow MRX to steal market share from smaller, independent opticians. Here’s how. Eye exams are a routine part of ordering new prescription lens (for example, this week I needed an eye exam to order new contacts).

MRX does offer a fully online eye exam for customers. But remember, most prescription lens consumers are older (44-59+) and don’t want to do eye exams online. The older customer cohort chooses the local optician retailer without a physical store.

What happens when MRX adds a retail location to that customer’s region? It adds another option for the customer:

- A) Visit the local independent optician and pay more with fewer options

- B) Visit Mister Spex and choose from 10,000+ SKUs while paying ~30% less than you would at the independent optician

The choice is clear. The customer chooses MRX.

Let’s discuss unit economics before moving to management. MRX’s Head of IR, Frank Bohme, outlined the unit economic breakdown:

- EUR 300K initial capex to build the store

- ~EUR 1M in revenue by the end of year one

- ~3-4 months to reach breakeven

- 20% ROICs by year 2-3

The company wants to aggressively build more stores, and they have enough cash to build ~636 stores before needing more capital.

Alright, onto management.

Management: A Founder-Led Business

Dirk Graber founded Mister Spex in 2007. He still runs the company today. Investors will likely highlight Graber’s lack of insider ownership as a negative. I thought so, too. But when I asked Frank about Graber’s lack of ownership, his answer changed my viewpoint entirely (emphasis mine, paraphrasing):

“[Graber] started the company and initially had majority ownership. However, over time, he gave more and more equity to his employees. He wanted to create a sense of entrepreneurship and ownership within the business. To [Graber], he was more focused on creating a successful, durable business, not becoming independently ultra-wealthy. He cares more about the long-term health and future of the business than any personal fortunes.“

I love that. When I asked about company culture, Frank reaffirmed the founder’s vision. Frank noted that employees love working at MRX.

“The company isn’t for those that want to coast,” Frank suggested, “If you want to do that, go to one of the larger incumbents.”

MRX plays to win the long term game.

The Path Ahead & Valuation

MRX trades at an unassuming EUR 386M market cap or EUR 238M Enterprise Value. The stock is down over 50% from its July 2021 IPO high of ~EUR 24/share (or ~EUR 800M market cap).

Why the major sell-off?

During Q3, the company revised its revenue and EBITDA guidance downward. MRX initially estimated 20% revenue growth and adjusted to 17-19%. Additionally, the company revised EBITDA guidance from EUR 6M+ to EUR 4-5M.

However, today’s prices are too low, given the company’s potential growth drivers. For example, MRX trades at ~1x NTM revenues and ~15x NTM EBITDA (assuming run-rate from Q3 2021 figures).

The company expects to grow revenues mid-20% over the next five years, landing us at ~EUR 487M by 2025.

By that time, MRX expects to generate substantially more revenue from its prescription eyewear segment, which should expand its gross and EBITDA margins.

Currently, the company anticipates a ~10% improvement in gross margin (to reach 59%) and a 6x improvement in EBITDA margins (to 12%).

It’s important to remember that the German eyewear market alone is worth over EUR 6B. Even if we assume the company generates 20%+ top-line growth over the next five years, it will only capture ~8% of that market share — notwithstanding the broader European market.

The most important questions to ask at this point are:

- What should we expect to see given our above assumptions?

- What should we not expect to see given our above assumptions?

We should expect to see the company take incremental market share from independent opticians, expand gross margins as they capture a more significant percentage of prescription lens sales, and generate higher EBITDA margins as they sell higher-margin products.

We should also expect to see more store openings. The company has EUR 190M in cash on the balance sheet. We should see that get put to use.

Now, what shouldn’t we see?

We shouldn’t see a decline in market share to independent opticians. We shouldn’t see a reduction in new customer growth rates since the company only has a 3% current market share.

Finally, we shouldn’t see lower AOVs as opening new stores generates higher average sales (and more frequent sales).

What’s the size of the prize if we’re right?

Let’s use Warby Parker as a comparable. Let’s assume MRX generates mid-20% revenue growth and reaches double-digit EBITDA margins by 2025. What would an investor pay for this business?

Currently, you can buy WRBY for 5x revenues for roughly the same top-line growth rates and EBITDA margin expansion. Let’s use a 5x sales multiple. That gives us a ~EUR 2.43B Enterprise Value. Add back the ~EUR 150M in net cash, and you get ~EUR 2.6B in shareholder value (or EUR 78/share).

That’s over 560% upside from the current stock price.

Concluding Thoughts

MRX is an easy-to-understand business operating in a high-margin, non-discretionary industry. The company has a leading customer value proposition, weak competitors, and a growing omni-channel presence that will likely go unmatched.

As millennials enter their prime eyewear buying years, which option will they choose?

Will they use a local, independent optician lacking the convenience of an omnichannel experience with a limited product assortment? Or will they use the company with a digital-first customer journey, the widest variety of glasses possible, all for prices ~30% cheaper on average than the competition?

The choice is clear. It’s just not reflected in the current market price.

If you enjoy differentiated research on excellent businesses trading off-the-beaten-path, then consider joining our Collective.

We’ve extended our enrollment window another week to ensure you get a seat at the table.

The Collective is the internet’s smartest group of traders, investors, and thinkers alike. Members include former hedge fund managers, venture capitalists, prop shop traders, and a couple of former Market Wizards …

We have one mission: to learn more each day, become consistently profitable, and have a hell of a good time along the way.

So, if you want to take the plunge and improve your trading, investing, and decision-making … join the Collective by clicking the button below.