I recently finished reading Joshua Ramo’s book The Age of the Unthinkable. Imagine if Per Bak’s Complexity, Martin Gurri’s The Revolt of the Public, and David Epstein’s Range got together and produced a love child. The Age of the Unthinkable would be its weird spawn.

Ramos dives into the tech-enabled asymmetric power wielded by small terror groups, the ineptitude of old institutions in this new revolutionary environment, the interconnected sandpile in which we all play and interact, as well as some methods for living in and analyzing this system for signs of criticality.

There’s lessons pulled from Israeli spy chiefs, Hezbollah middle managers, silicon valley VCs, South African AIDs doctors, and Cubist art critics… All in all, it makes for a fun and quick read.

It has a number of interesting takeaways, but I want to talk about just two as they’re relevant to a few things going on in markets today.

These are the ideas of mashup and new math.

Mashup is a term born out of DJ’ing apparently. A DJ, for those of you not familiar, is a name given to a child of wealthy parents who didn’t want to go to college or get a job because it’s just not his bag…

Anyways, these DJs take existing music then cut, slice, and dice things together to create something new. And voila, you have a mashup. Something not entirely original but not entirely not, either.

Really, mashups are about the combinatory creation of existing ideas. Ideas often pulled from foreign fields and disparate disciplines.

The example given in the book is of Shigeru Miyamoto and how he created the Nintendo Wii. A gaming console with dated processors and auto airbag accelerometers, that went on to outsell the much more advanced — and conventional — rival consoles, Xbox and Playstation.

New Math, is a term originated by Earl Gray, an American environmental scientist and tea enthusiast (I assume). It refers to when “zero plus zero equals something”. When, for example, “chemicals that separately have no effect on the body but when mixed together create a toxic, cancerous result.”

New math is like chasing down a packet of Pop Rocks with some RC Cola. Both, by themselves, harmless consumables from the 90s. But, if mixed together in one’s lower intestines… instant death — or so my childhood myth goes.

Another example would be ESG trends and climate fighting government policies. Both totally innocuous, well-intentioned ideals.

But….

When mixed together in an increasingly Hungry World where the interconnections are so deep and varied, that when a butterfly farts in Boca Raton a property Giant defaults in Shenzhen — meaning, unintended consequences are unavoidable and often iatrogenic.

Take what’s going on in commodities.

Demand for dirty coal peaked nearly a decade ago, yet thermal coal prices are near all-time highs.

Rising coal has helped drive LNG prices to new records. This, in turn, has boosted European gas, which has resulted in a wild spike in electricity pricing.

As a result, aluminum has mooned as the HODLers would say, and the list of linkages goes on and on…

How and why is all this happening?

Well, let’s work backward and see… China produces the majority of the world’s aluminum (60%+). Aluminum smelting is a terribly energy-intensive business. China gets most of its electricity from coal.

But…

Chinese coal production has had a difficult time keeping up with demand. This is partially due to climate-related regulatory reforms and years of under-investment on the supply side. And hydropower, another significant source of Chinese power, has faltered this year following major droughts in certain parts of the country.

As a result, China has had to turn to the international market for coal where many of the large producers are facing similar problems.

Increased Chinese demand for seaborne coal, means higher coal prices around the world. Higher coal prices ripple into higher LNG costs, which means rising electricity rates for China and the world. And since China produces most of the world’s Aluminum, we get soaring aluminum prices. A butterfly farts and…

This is new math at work. Legacy institutions don’t understand this, which is why they keep trying silly things like imposing rigidity on the grid, in the form of renewables at the cost of dependables that live at the whims of our increasingly sporadic weather.

As a result, we end up consuming more dirty fuels at higher costs, because the capital hasn’t been invested to produce the needed supply — or put into clean, reliable nuclear but that’s a whole other thing.

Legacy institutions favor signaling over substance and so unintended consequences will continue to be on the menu.

These old centers of power still operate in a linear hierarchical world. They don’t yet know we live in a giant mesh, with no center. Only nodes of transient influence with ever-changing edges, connecting the whole mess.

In this world, variance reigns supreme. The border controls the center. Not by intention, since the border is the furthest thing from being homogenous. It does so because it derives its power from the new rules. It’s intrinsically geared towards mashup creation and new math effects. While the center’s power is built on a collapsing facade of pretense and elitist pageantry.

The fracturing of the public along niche interests has unleashed swarms of networks against every sacred precinct of authority. Failure has been criticized, mocked, magnified. The result is paralysis by distrust. The Border, it is already clear, can neutralize but not replace the Center. Networks can protest and overthrow, but never govern. Bureaucratic inertia confronts digital nihilism. The sum is zero. ~ The Revolt of the Public (emphasis me)

This is the connected and increasingly strange world we live in.

It’s one where rising internet usage mixes with decades-old cryptographic ideas that are fueled by evolving central bank policies which then gets Vitamixed together by the meme factory of social media… And the end result is something that no one… not a single person… crazy, sane, or otherwise, could have guessed… And that is this mind-numbingly dumb yet also perfectly symbolic of the times jpeg of Bored Apes. A jpeg which sold recently for just shy of $3mn…

I’m not quite sure what to make of it all. But I do know it’s of increasing importance. The game has new rules, rules that are changing on the fly. We’re now gassing along at breakneck speeds, with the Center blowing smoke into oblivion and the Border burning cash on the Apes… What does it mean? Nobody knows, it’s some mashed-up new math sort of weird jazz…

Anywho, let’s talk markets.

First off, I don’t believe this is the start of a significantly larger sell-off (famous last words, I know).

Evergrande is not Lehman. Most of its debt is local. Xi is trying to smoke out speculation in the real estate market. He’s making an example out of Evergrande but the CCP won’t risk letting things tip into criticality.

Evergrande has been a known-known for months. This is all an example of back-fitting a narrative to price action more than anything else.

The reality is more boring and looks something like this.

- The market is coming out of its weakest seasonality of the year

- FOMC meeting this week = paring back of risk

- Months without a 5%+ selloff in the SPX = a lot of weak hands built up

- Record aggregate fund flows into stocks creates instability of its own

This all reads more like a healthy shakedown. A positioning cleanse that should coil the spring for one more leg up.

We haven’t put in the typical conditions for a longer-term top yet. We haven’t gone parabolic. SQN isn’t elevated. Our TL Score is still neutral. Trend Fragility is high, but not extreme, etc…

We’ll probably see a bit more pain. Most likely a retest of today’s lows, if not lower heading into the FOMC.

A number of markets hit their lower bands today (chart below). That’s usually good enough for at least a small bounce. We’ll have to see how breadth looks over the next few days.

This is an opinion, weakly held of course. I’ll change my mind if breadth deteriorates further. If the Russell breaks below its key support. If buyers fail to come in when we’d expect them to and the tape stays heavy, etc…

This is basic but it often pays in markets to stick to KISS (Keep It Simple, Stupid).

We’re going to wait until we see signs of selling exhaustion/capitulation or a strong reversal in the internals before we add risk. But here are a few names we’re looking to either add to or enter.

The Australian uranium producer, Paladin Energy (PDN).

We own this one and are looking to build on the position. A further pullback into or below the green zone followed by a reversal would be a good spot to do so. On a side note, with all the red in markets yesterday, did you see the one thing that was green? Sprott’s Uranium Trust…

Japan’s Nikkei has one of the best-looking charts in global markets right now. I’ve been covering the strong internals and fundamentals for the last few weeks, so I won’t waste more ink on that here. With that said, we’d like to get a position on if price comes down a bit further.

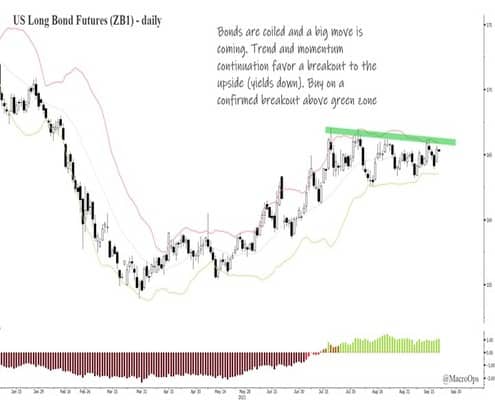

Our yield indicator still points lower, meaning bonds up.

Bonds are coiled tight on a daily and weekly basis. Bandwidth is in the sub 5th percentile for both notes and bonds and are close to triggering a major compression signal. Compression signals are directionally agnostic and just mean that odds are increasing we’ll see a big move soon.

We’d be buyers on a confirmed breakout. And buyers in size on a confirmed breakout that’s driven by increasing risk-off in markets.

We remain long-term US dollar bears for the reasons I outlined here in Soros’ Currency Arrows.

Short to intermediate term, the US dollar is in neutral range mode. USDJPY is still coiled and we’ll take another swing short on breakout follow-through. We also might get long EURUSD for a swing long soon (we’ll send out an alert if/when we do).

We’ll be out with much more in the next few days as I expect this to continue to be an eventful week.

Thanks for reading.

Until then, stay nimble and keep your head on a swivel.