Over a third and growing quickly. That’s the share of the market that’s now comprised of blind sheep passive indexers.

That much passive money is nothing to sneeze at. Call me old-fashioned, but I was originally led to believe that the function and role of markets in a capitalist society was to direct capital to its most productive end — you know, Smith’s “Invisible Hands” and the productivity/profit link and all that jazz.

So what happens when instead of being deployed by thinking profit-driven investors… a growing portion of a nation’s savings are invested with the same diligence generally utilized by a co-worker choosing donuts for his office mates: “Umm…yeah, I’ll take two dozen of whatever you got?”

That’s the question research firm Sanford C. Bernstein asked in a recent piece comparing the current passive investing craze to a lesser form of Marxism — it being appropriately titled “The Silent Road to Serfdom: Why Passive Investing is Worse Than Marxism.”

The report notes the different types of capital allocation models societies can choose, saying (bolding is mine):

Active investment decisions form a crucial part of the capital allocation process in an economy and as such there is a clear and distinct social worth in their aggregate action. A possible alternative is a Marxist economy where the capital allocation is planned, such a system is perfectly viable but just less effective. However, a supposedly capitalist economy with no active investment — where passive management is the only capital allocation process — is, in our opinion, worse than either of these alternatives, hence our assertion in the title of this note.

The commonality between both active market management and the Marxist approach is that in both cases there are a set of agents trying – at least in principle – to optimise the flows of capital in the real economy.

Walter Bagehot, former editor of The Economist from 1861-1877, and all-around wise dude, once wrote:

One thing is certain, that at particular times a great deal of stupid people have a great deal of stupid money… At intervals, the money of these people — the blind capital, as we call it, of a country, is particularly large and cravin; it seeks for someone to devour it, and there is a ‘plethora’; it finds someone, and there is speculation; it is devoured, and there is ‘panic’.

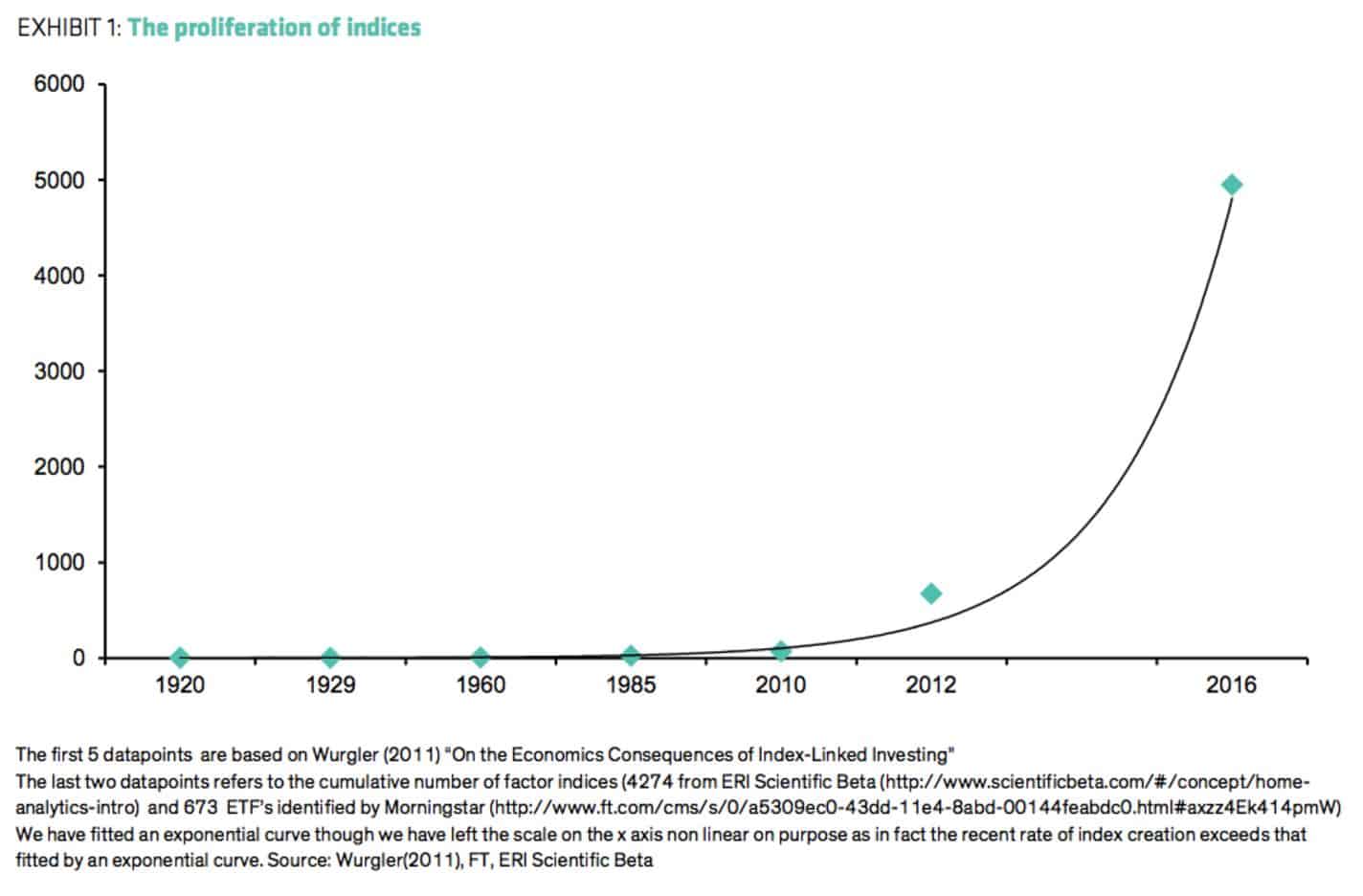

With that in mind, let’s now turn our attention to the following chart, again via Bernstein.

It shows the growth in indexes… which looks like one side of a classic parabola.

It shows the growth in indexes… which looks like one side of a classic parabola.

Here’s Bernstein on the absurdity (bolding is mine):

The proliferation of indices has been greater since then as smart beta indices increasingly offer exposures that cover part of what was known as active before. We now have the bizarre situation that there are more indices than there are large cap stocks, this is not at all helpful for investors.

Is this trend in allocation not the very embodiment of what Bagehot was talking about? The “blind capital, as we call it, of a country, is particularly large and cravin; it seeks for someone to devour it, and there is a ‘plethora’.” When he said these words it was in reference to the infamous “South Sea” bubble of the 18th century. And ironically, the backdrop and cause of which are very similar to today’s nonsense.

The blind speculation in shares of the South Sea Company was spurred by a complicated debt monetization scheme in which Britain’s national debt was packaged and exchanged for worthless “fiat” shares of a profitless “trading” company; thus driving down interest rates, borrowing costs, and creating a self-fulfilling credit-fueled feedback loop.

Sound familiar? It should, the South Sea bubble was one of the first instances of quantitative easing (QE) in a modern economy; with South Sea acting as a central bank.

Which brings us back to the future of passive indexers. The cause of this fad, and it is a fad, will also be its undoing.

Blindly throwing money at the wall is a thing, because of how central banks have distorted markets and suppressed volatility — they’ve given the illusion of having extinguished risks; so investors have had little incentive to know what they’re really investing in.

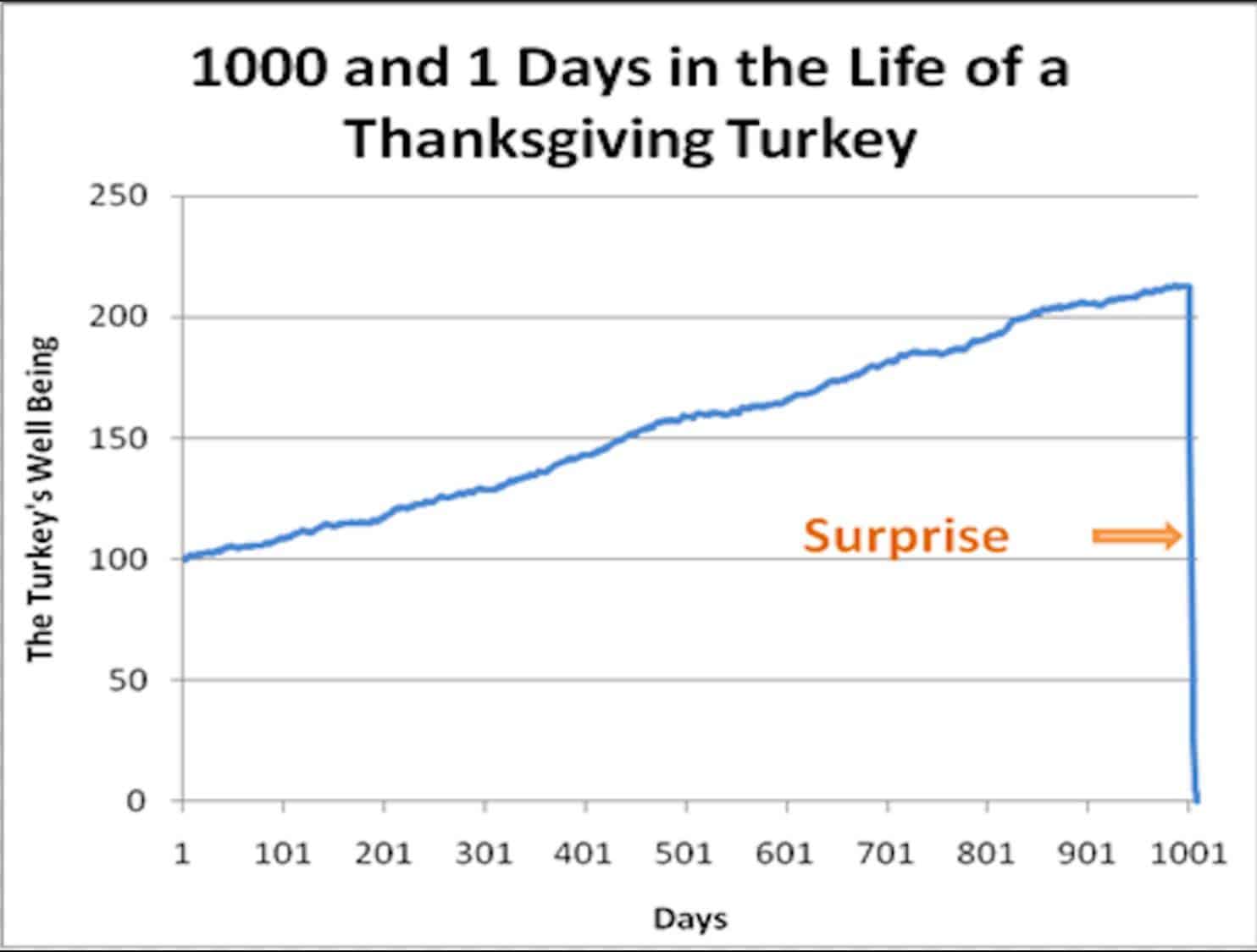

One can’t help but be reminded of Nassim Taleb’s “Turkey analogy” from The Black Swan.

It goes something like this.

Consider a turkey that is fed and cared for everyday by its owners. Every day of the turkey’s life he is fed, sheltered, and grows fatter and healthier.

This continuation of positive events reinforces the Turkey’s belief that he is cared for by his owners and will continue to be so.

This goes on and on, until of course the Wednesday before Thanksgiving rolls around. Then the turkey incurs a rude “revision of belief” and is snapped — quite literally — into what was just a day before, an unimaginable reality. And as Taleb notes, “Consider that [the turkey’s] feeling of safety reached its maximum when the risk was at the highest!”

The Bernstein note concludes by saying “A field of endeavor that performs no social function is ultimately unsustainable if it has a cost that is imposed on the rest of society. Any such activity will, in the ultimate analysis, simply be regulated out of existence.” So maybe these trends are irreversible and Adam Smith’s capitalist model of allocating savings is a thing of the past and we’re stumbling into a future without markets.

The likelier conclusion though — at least in this author’s opinion — is that like the South Sea bubble and blind capital “plethoras” before it, this party will end just as they always do. Right when risk seems to have been absolutely extinguished and investing passively becomes a no-brainer… the butcher will come and a once unbelievable reality will become painfully real.

It may be an awkward Thanksgiving. Make sure you’re not the turkey…