Loungers (LGRS) is an operator of café/ bar/ restaurants across England and Wales under two distinct but complementary brands, Lounge and Cosy Club. It is the only growing all-day operator of scale in the UK, with a strong reputation for value for money and sites that offer something for everyone regardless of age, demographic, or gender.

The Company operates successfully in a diverse range of different sites and locations across England and Wales. As of 2019, LGRS operated 167 sites across its two brands. Its two founders own ~14% of the company.

The LGRS thesis is a bet on the underlying unit economics of the company’s mature sites. The company spends ~1.30% of revenues in maintenance CAPEX while spending a whopping 13.5% on growth CAPEX to build more sites.

Once mature stores reach a higher percentage of total stores, the company will realize substantial free cash flow for its shareholders. Every mature site the company has is profitable. Also, LGRS’ esoteric interior decoration means that the site Improves with age, leading to a lower-than-average maintenance CAPEX.

LGRS sees a path towards 500+ sites between Lounge and Cosy Club. That means the company’s penetrated a mere 30% of its addressable market. Even if they open an additional 400 Lounge sites, they’d still be less than half the other UK hospitality operators’ size.

New site initial CAPEX ranges from GBP 600K for Lounges and GBP 1M for Cosy Clubs. The company has averaged a 34% cash return on invested capital each over three years (2016-2018). If the company completed its full roll-out target of 500 sites, it would generate GBP 500M in run-rate revenues while spitting off GBP 146M in free cash flow.

Investors can buy LGRS for ~4.4x our estimate of steady-state free cash flow or a 27% FCF yield at the current market price.

Let’s get after it.

What Makes The Loungers Experience Unique?

Loungers have two site brands: Lounge and Cosy Club. Each site poses unique characteristics that make it unlike anything else on the market. Let’s start with the Lounges.

The Lounge: A Unique Place To Socialize With Friends

A Lounge is a neighborhood cafe/bar that’s a part coffee shop, part pub, and part dine-in experience. 72% of customers don’t categorize Lounge as a pure-play “restaurant” or “bar” rather a unique experience culminating multiple environments. ~75% of the company’s new builds are Lounge sites. LGRS had 136 Lounge sites by the end of 2020.

The best way to think about a Lounge is like a home-away-from-home. Each Lounge site has the local interior decor that makes it feel like a home. The homey feel makes sense as most Lounge sites live in secondary suburban high streets and small towns (as low as 10,000 people).

Lounge sites are unique to the community. Each location has a different name without any heavy “Loungers” branding. Stores are encouraged to decorate the interior to match the theme of the local town/city they occupy. Given the level of store customization, every store looks a little different.

Differentiation makes sense in a community-based environment where 8 out of 10 Lounge customers live locally. This local feel translates into repeat weekly visits. 25% of customers visit at least once a week, and 67% of customers visit each month.

Customers visit the Lounge not so much to eat but to socialize with friends and family. 60% of customers visit a site to socialize with friends. 51% visit to “grab coffee with family/friends.” Most hangouts occur on the weekend and tend to skew towards more female gatherings.

American readers (myself included) can think of Lounge like a Cracker Barrel (CBRL). CBRL has vintage, homey-feeling interior decor, with each store unique to its location.

For example, a Cracker Barrel in Virginia will sport local collegiate apparel in its shops (from Virginia Tech, UVA, etc.). However, the same CBRL store in Pennsylvania will offer Penn State clothing. There are more similarities between the two concepts, which we’ll cover later.

Cosy Club: Closer To A ‘Fancy’ Restaurant

Where Lounges are informal social gathering hubs that serve food/drink, Cosy Clubs are the more formal option. Cosy Clubs command a more traditional sit-down restaurant with sites located in city centers/large market towns.

Where Lounges are informal social gathering hubs that serve food/drink, Cosy Clubs are the more formal option. Cosy Clubs command a more traditional sit-down restaurant with sites located in city centers/large market towns.

Think of Cosy Clubs as old-school high-end restaurants. The company houses its Clubs inside theatrical buildings that catch the eye. LGRS generates higher sales and EBITDA (on average) in its Clubs versus Lounge sites.

As a more traditional restaurant, 70% of its customers visit to enjoy evening drinks. 65% of customers go for lunch, and 63% visit for daytime drinks (I see you, Britain). Cosy Clubs generate most of its visitors on weekends (63% Fri-Sun vs. 37% Mon-Thurs).

Like its sister brand, Cosy Clubs offer all-day hospitality and dining, with Clubs providing the same menu from 9 AM to 10 PM.

The company had 29 Cosy Clubs nationwide at the end of 2020.

Value For Money: The Benefit of Always Low Prices

LGRS has a simple yet powerful motto: “Serving Everyone for Every Occasion, Everywhere.”

Part of that motto is to provide high-quality food at low costs to its customers. LGRS makes this easy by charging the same price for the same type of food at each of their 167 locations. It doesn’t matter if it’s in a sleepy town of 10K or a bustling city hub of 100K. Of course, they could charge more at the latter location, but they choose to reward their customers with lower prices everywhere. The company prides itself on “substantial, good quality meals for less than 10 euros.”

For example, LGRS charges 7.75 euros for Avocado Brunch, 6.75 euros for Tripe Stack Pancakes, and 8.50 euros for a Halloumi Burger.

The company stays “in line” with other neighboring coffee-only shops when pricing its cup of joe.

Homogenized menus and prices do more than please customers in the form of lower prices.

These mandates allow LGRS to roll-out stores at a faster pace. The company knows what it will charge for everything on the menu before it finds a new location. A consistent menu also gives LGRS leverage with its food suppliers by commanding lower ingredients prices.

On the customer side, there are two significant benefits to identical menus and prices. First, customers know what they’re getting regardless of which Lounge or Cosy Club they visit. This familiarity is one reason why McDonald’s became so popular. A burger in DesMoines, IA, tastes the same as a burger in California.

Second, LGRS’ sites become go-to locations in times of economic hardship. With already low prices, LGRS doesn’t need to offer discounts to attract customers. Plus, they capture incremental consumers as customers trade down during recessions. Customers will always have enough money to spend 7.65 euros on a veggie breakfast to hang out with their friends at a cool, hip location.

One of the best examples of this dynamic is CBRL. Like LGRS, CBRL has roughly the same price points and menus throughout its locations. So whether I’m in NY or PA, I know what I’m getting when I walk into a CBRL establishment.

Lower prices also allow LGRS to enter smaller, secondary locations without competitors with higher cost structures.

LGRS Benefits From *Gulp* Socialization As A Service

I know. I threw up in my mouth as I typed that title. Yet the more I think about LGRS, the more I realize it’s about socialization. The bull thesis doesn’t hinge on the quality of the food (which is good). Nor does it hang on the price of the meals (which are cheap).

Instead, the thesis lives by customers’ desires to visit Lounges or Cosy Clubs to socialize with friends. Starbucks, for example, isn’t a place to get coffee. It’s a spot that offers free WiFi, a beautiful aroma, and a place to work. Oh, and they make a decent cup of coffee.

Matthew Dollinger of Fast Company wrote a great piece on this Starbucks idea. He went so far as to interview a Starbucks manager to get the inside scoop. This manager, Kelly, says that Starbucks’ goal is to become a customer’s ‘Third Place.’ Here’s what she means (emphasis mine):

“Starbucks goal is to become the Third Place in our daily lives. (i.e., Home, Work, and Starbucks) “We want to provide all the comforts of your home and office. You can sit in a nice chair, talk on your phone, look out the window, surf the web… oh, and drink coffee too,” said Kelly. (Notice she put “drink coffee” last???)”

LGRS wants the same result for its “home from home” Lounges.

A 7.75 euro Lounge Avocado Brunch isn’t a meal. It’s a ticket to socializing with friends at a hip spot. Said another way, the meal is simply a means (eating) to an end (socialization) like tickets are to watch a sporting event.

LGRS Boasts Strong Growth & Unit Economics

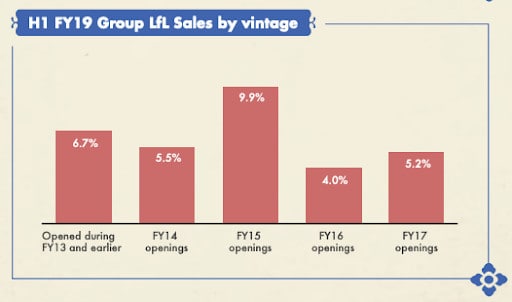

The site concepts work, and we can see their success in the financials. LGRS has grown sites at a 29% CAGR since 2014 (from 44 to 146 in 2019). During that time, the company increased sales and adjusted EBITDA at 38% and 39% CAGRs.

Like-for-like (LfL) sales also show approval of the concept. Check out the LfL sales growth breakdown by site opening year:

The company managed to grow sites at a 29% CAGR thanks to impressive unit economics. It costs ~GBP 675K to build a new Lounge and ~GBP 1M to create a new Cosy Club. So let’s say GBP 837K on average across brands.

Here’s the good news: LGRS generates an average Cash Return on Cash Invested (CROCI) of 34%. The company calculates CROCI by taking the last thirteen four-week periods and dividing it by each site’s cumulative CAPEX. At 34% CROCI the company generates ~GBP 284K in EBITDA by the end of the first year in a new location.

In other words, for every GBP 1 the company spends building a new site, they make GBP 0.34 in EBITDA.

At those rates of return, it makes sense for the company to plow every available dollar into opening new sites. Luckily that’s their plan. The company aims to open ~25 new sites annually until they hit their 400 new site target.

Like our Gym Group write-up, LGRS is a perfect example of a company’s cash-flow capabilities hidden by current reinvestment rates. Let’s flesh this idea out.

Current Reinvestment Rates Hide True Cash-Flow Yield

Our GYM thesis’s crux was that the company’s current reinvestment rates hid GYM’s true cash-earnings power. At first glance, investors see little free cash flow and an optically high EV/FCF multiple. In turn, the high multiple makes GYM (and LGRS) ‘unscreenable’ to most traditional value-based investors. Here’s how the accounting mechanics work.

LGRS bifurcates its CAPEX into “growth” and “maintenance” spending. Growth CAPEX compiles initial build-out costs for new sites. Maintenance CAPEX, on the other hand, represents the  annual cost to maintain every LGRS site. The company spent GBP 22.78M in total capital expenditures. Now, of that GBP 22.78M, LGRS spent GBP 17.37M in growth CAPEX (or 76% of total CAPEX) and GBP 1.97M in maintenance CAPEX (~8.6% of total CAPEX). Said another way, the company spends 10% of its revenues on growth CAPEX and ~1.16% on maintenance CAPEX.

annual cost to maintain every LGRS site. The company spent GBP 22.78M in total capital expenditures. Now, of that GBP 22.78M, LGRS spent GBP 17.37M in growth CAPEX (or 76% of total CAPEX) and GBP 1.97M in maintenance CAPEX (~8.6% of total CAPEX). Said another way, the company spends 10% of its revenues on growth CAPEX and ~1.16% on maintenance CAPEX.

Another added benefit to the LGRS site model is that they don’t have to spend a lot on maintenance CAPEX. The company’s Lounge sites have ‘homey’ interiors that don’t need constant upkeep.

LGRS will continue to spend heavily on growth as they expand site locations. Site expansion makes sense when you generate 34% CROIC. At some point, they’ll hit site saturation and reduce growth spending. Once that happens, investors will realize the tremendous cash-generating power of their mature sites.

Maintenance-only mode is (hopefully) a long way away, as we’ll discuss next.

LGRS Has A Long Runway To Open New Sites

LGRS enters 15YR leases with new site landlords. Such long-term contracts allow LGRS to negotiate favorable rent terms. For example, landlords usually offer rent-free periods during initial site builds. These rent-free periods create a negative working capital cycle and allow LGRS to operate at 100%+ cash conversion. Long-term contracts also give LGRS lower rent prices, which accounted for ~5% of revenues from 2016 – 2018.

The company’s goal is 20-25 new site builds per year. LGRS’ founders explain their roll-out strategy and infrastructure in their IPO documents (emphasis mine):

The company’s goal is 20-25 new site builds per year. LGRS’ founders explain their roll-out strategy and infrastructure in their IPO documents (emphasis mine):

“The Group’s operational infrastructure has been built to facilitate the rollout of 25 new sites per year, with a high ratio of operations staff to sites providing the capacity to support the rollout and ensure the intensity of site management. New staff are trained in nearby sites prior to opening and experienced staff are often brought in to help manage an opening. As a result of the gradual acceleration of the rollout, with a new site opening every two weeks on average over the last 12 months, openings have become part of the day-to-day operation of the Group. As the number of sites in the Group increases, the Group benefits from having an expanded base of experienced employees and a larger regional management infrastructure to support new site openings.”

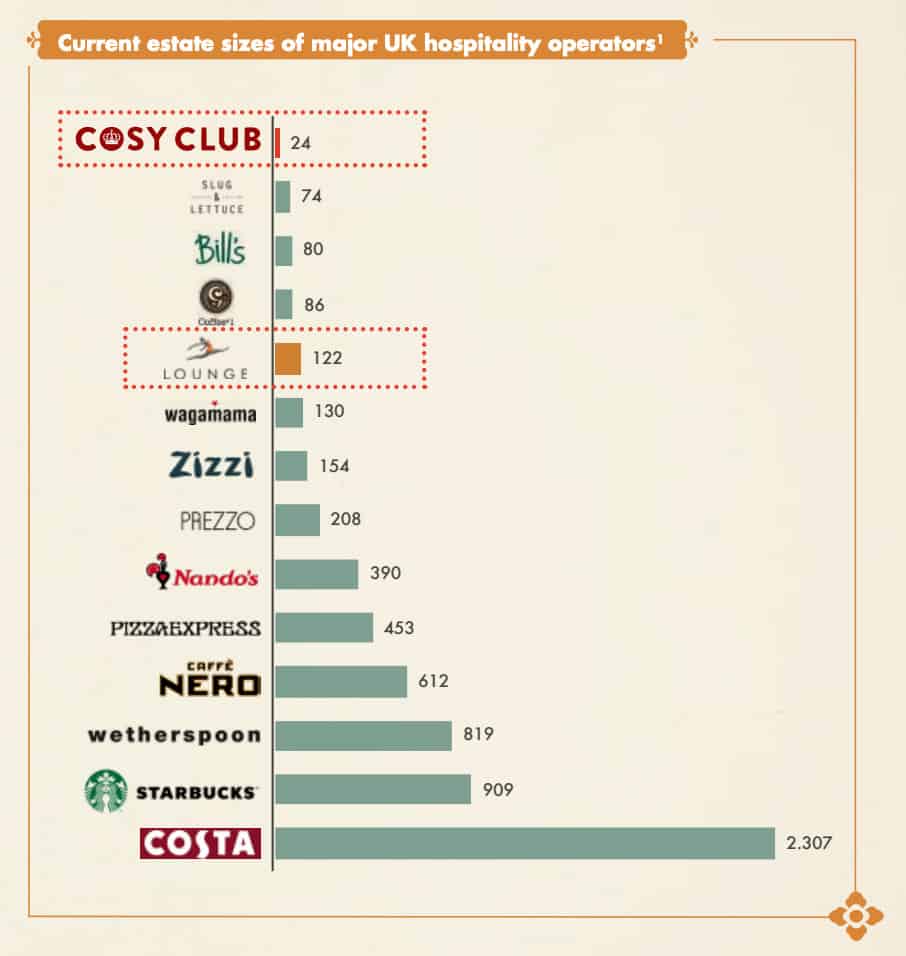

LGRS can expand to 500 total stores between their Lounge and Cosy Club brand. There’s a chance that 500 number is conservative given the success of the brands since its founding. One interesting note about the company’s roll-out strategy is that they can cluster multiple sites without cannibalizing sales.

Should LGRS hit their 500 store mark, it would place them with Nando’s (390) and Pizza Express (490), but halfway to Wetherspoon and Starbucks (SBUX).

At 167 stores, LGRS has lots of room to build new sites to hit its 500 goal.

Thinking About Growth, Revenue, and Valuation

The LGRS valuation model is simple with two main questions:

- How many stores can the company build over the next 5-10 years?

- How much revenue and cash flow can each store generate on a run-rate basis?

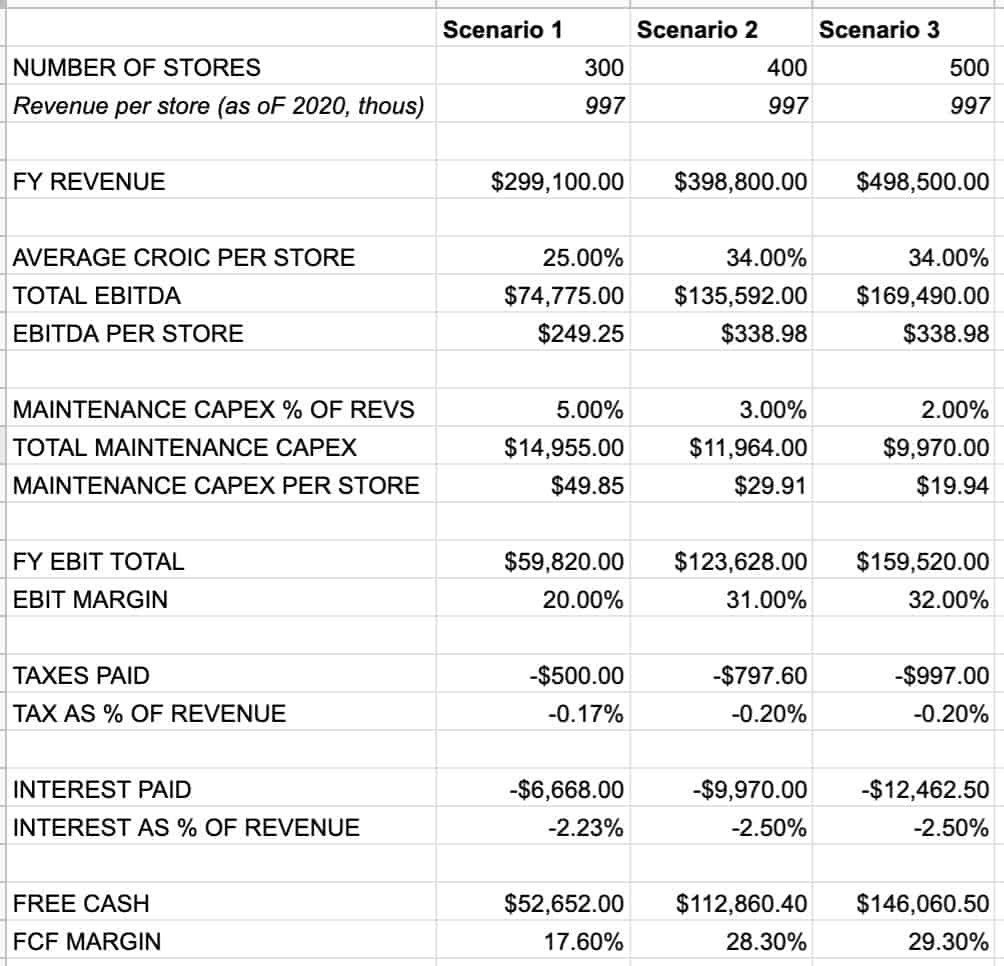

We can’t predict these two variables with any high degree of certainty, so we’ll work within a wide range of possible final store numbers. Let’s paint three scenarios:

- Scenario 1: 300 sites, 25% CROIC per store, and 5% of revenue on maintenance CAPEX

- Scenario 2: 400 sites, 34% CROIC per store, and 3% of revenue on maintenance CAPEX

- Scenario 3: 500 sites, 34% CROIC per store, and 1.5% of revenue on maintenance CAPEX

Here are the results of each scenario:

LGRS will generate gobs of cash if it continues its expansion policy at current CROIC rates. If the company hits its 500 site target, it will generate ~GBP 146M in steady-state free cash flow. LGRS currently trades at a GBP 380M Enterprise Value, making our 500 site estimate a ~38% FCF yield. Our three scenarios generate an average EV/EBITDA multiple of 3.38x (33% yield) and an average EV/FCF multiple of 4.40x (27.33% yield).

The company will use this cash to pay down debt, issue substantial dividends, and (hopefully) buy back stock when it’s cheap.

Concluding Thoughts

LGRS doesn’t have a “moat” in the traditional sense of the word. There are low barriers to entry and nearly zero customer switching costs. Yet customers love visiting each brand site. The company’s expanded stores at a 29% CAGR and generate 34% CROIC on each site.

In other words, they’re doing something right. Humans are social creatures. We crave face-to-face connection with others. It doesn’t matter how great the video-conferencing technology gets. When given a choice, we’d instead meet in person.

The company made an effort to build sites in smaller towns to create a central “watering hole” for residents. The watering hole provides low-cost/high-quality food, a great cup of coffee, and a comfortable, ‘homey’ atmosphere.

Over time, LGRS will expand sites and become the go-to indoor social spot to hang out and grab drinks with friends. Low prices allow the company to enter smaller markets without fierce competition. And during an economic downturn, customers will choose LGRS’s consistently low prices.

LGRS has a long runway to expand its branded locations through the UK. If they hit their 500 sites, the company will generate hundreds of millions in free cash flow. That will take time, of course. But at current market prices, the returns are well worth the wait.