Before we dive into the piece, a quick note: We’re opening up our Macro Ops Collective enrollment until the end of the year.

The Collective is our premier service, offering discussions on high-level theory and performance, differentiated research, real-time trade alerts, portfolio tracking, and a global community of serious traders and investors dedicated to mastery.

We’re having a decent year (~+50%), catching a few big themes, finding a few stocks nobody had heard of, and not doing anything stupid.

If you’re interested in our Trifecta Lens Framework and trading philosophy or want to eliminate the guesswork of position sizing, risk management, and market noise, check us out.

Click below and sign up.

Last week, I talked with a Collective member about hot/cold streaks and whether to “press the gas” when you’re up versus dialing back and protecting existing profits.

Here’s the comment.

Member: I’m convinced that individual P&Ls are often hurt by people clinging to monthly, quarterly, and yearly returns. One of my takeaways from Annie Duke is that the best poker players and risk managers would never think like that. Don’t get more aggressive when doing well (or vice versa) … Don’t be a slave to having to produce numbers at a specific point in time.

The member said this because I mentioned that I want to hit 60% returns by year-end (higher would be nice, too 🙂).

He then referenced a personal poker analogy (emphasis added):

“The same phenomenon [in markets] can happen to me at poker. If I go to a poker room and win early it’s often a down night.”

I found that fascinating because I’m the exact opposite.

Sticking with poker … if I win early, I relax and often play better due to my early success.

Psychologically, a few early wins allow me to risk “the house’s” chips and play more aggressively than I would if I risked my stack (i.e., principal).

I may bluff, ride more hands to the river card, or change my tactics completely. Why? Because I’m not risking “my” capital.

What struck me was the dichotomy between how people view “being up” and “being down” in markets, the poker table, or other competitive endeavors.

Take sports, for example.

Some athletes perform better with a lead, while others perform better when losing. Why is that?

There are two types of athletes:

- “Feed Me” Winners: These athletes play more relaxed and aggressive when leading because they have a cushion. They feel confident like they can beat anybody … “Feed me the rock, I can’t miss.”

- “Back To Basics” Losers: These athletes perform better when losing because they hyper-focus on fundamentals or the basics of their craft. How do you eat an elephant? One bite at a time … one good shift, one good crossing pass, one good mid-range jumper, etc.

Of course, the world’s best performers seamlessly transition between states depending on the game’s score.

Let’s use tennis as an example since it’s my favorite (as best) sport.

I play as the “Feed Me” Winner when I’m winning. Maybe I take that down-the-line backhand winner. Maybe I try two first serves because I have a comfortable lead. I play more aggressively because I’ve earned the right by being in the lead.

But if I’m losing, I strip my game down to its most basic job: getting the ball over the net. Instead of that down-the-line backhand, I’ll hit a heavy topspin ball deep into the center of the court.

The idea is that I must earn the right to play aggressively. I earn that by having a lead and playing with the house’s money.

This applies to trading and investing. I earn the right to trade more aggressively by being up on the year, booking substantial profits on closed trades, and having existing positions at breakeven or profit levels.

George Soros said it best (emphasis mine):

“Risking your profit is much easier than risking your principal. The reason we have such a good record is we never lose our principal.“

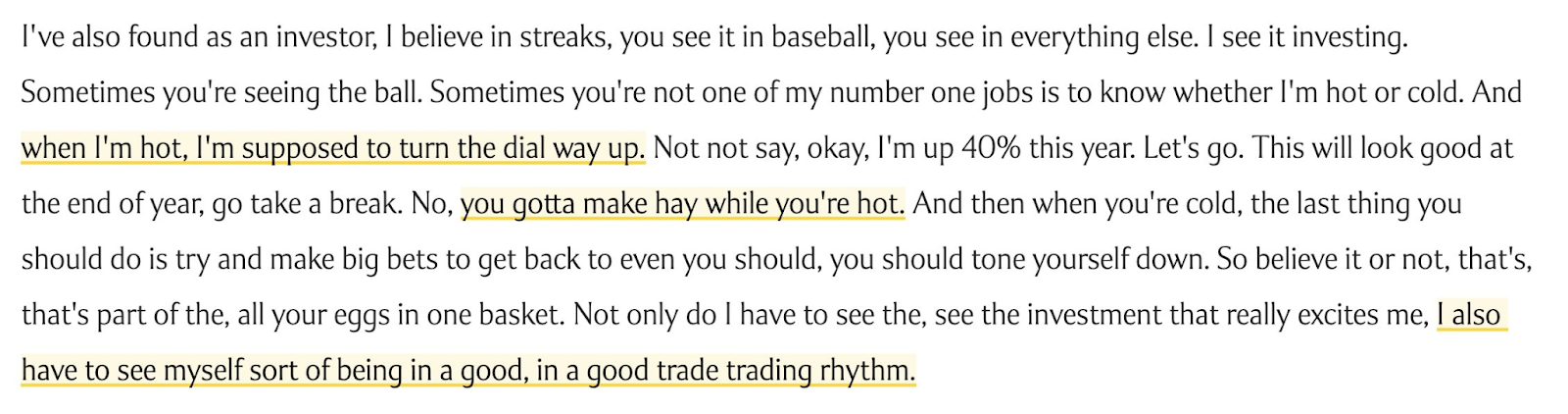

Stanley Druckenmiller echoes this idea, saying, “You gotta make hay while you’re hot.”

I love this part … “When I’m hot, I’m supposed to turn the dial up.”

In other words, if you know you’re in the zone, go for the jugular.

Let’s go back to the tennis example. There are days when I feel like I can hit every shot. And there are days when I forget how to grip my racquet.

I should play as aggressively as possible – so long as I’ve earned that through being up in the match – when I feel like I can hit every shot.

But we can dive even deeper than that.

There are days when I can’t miss my backhand, but my forehand gives me trouble. So what do I do? I stay aggressive on my backhand and hit big targets on my forehand.

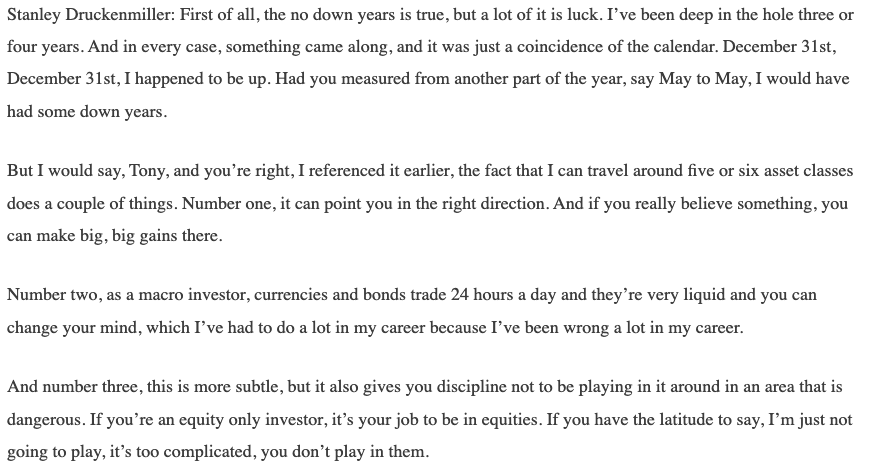

This is the game-within-the-game. It’s how Druckenmiller never had a down year (see below).

Druck only played the markets where he had a “Feed Me” Winning psychology. It kept him from having a down year.

There are times when futures carry the MO portfolio; other times, one or two equity positions generate most of the portfolio’s returns. It’s all about what market we “feel hot” in.

What does this mean for the MO portfolio, and how do we view the last few weeks of the trading year?

We’re being as aggressive as possible with our current book … buying more of what’s working and cutting what’s not.

We’re using our closed and open profits (i.e., stops beyond the breakeven point) to increase risk without risking our principal. In other words, we’re trying to make hay while we’re hot. We’re risking the house’s money to do it, all while protecting our principal.

Alright, onto Valeura Energy!

Valeura Energy (VLE.TO): A Trifecta Lens Energy Trade

Valeura Energy (VLE.TO) is a $500M market cap Canadian oil producer with four producing assets in Thailand.

Here’s why we bought it.

The company has $156M in cash and no debt, and it recently reorganized its operations to unlock $400M in tax losses. At the historic 50% tax rate, the tax losses represent ~$200M in incremental cash flow.

Insiders own ~19% of the company, and VLE recently announced an NCIB to repurchase 7.4M shares (6.5% of the total).

The stock has increased by 137% over the past year, outperforming its peers in relative outperformance. Value investors don’t like buying stocks that have gone up a lot, so the outsized returns are part of the bull case. There’s still more meat on the bone.

Management knows what they’re doing. They took VLE from a $30M cash box to a $500M market cap company with four producing assets and hundreds of millions in annual FCF while increasing reserves/production and reducing ARO liabilities.

Over the past year, the company increased reserve replacement by 200% while reducing ARO by 30%.

How cheap is VLE? Here’s our napkin math.

At $70/bbl and 26.4K/bopd, VLE would generate $640M in revenue. The company pays ~$10/bbl in royalties, $24/bbl in opex, ~$4/bbl in SG&A, and another $12.50/bbl in sustaining capex.

That gives us $175M in pre-tax profits.

Remember, we have $400M in tax losses. This means next year’s pre-tax profits could equal net profits … and the year after.

VLE could generate half its current EV in net cash flow this year while still having $200M in tax losses to carry forward in 2026 … which would be worth more than the entire EV by year-end 2025 (assuming we’re directionally correct on oil price and business model).

This doesn’t include any acquisitions VLE might make next year to increase production and cash flow. We’re getting that for free.

Catalysts:

- Acquisition announcement (probably an onshore Turkish asset)

- Increased buyback allotment on the NCIB

- Special dividend

- Higher oil prices

I highly recommend watching the latest VLE CEO interview (here). Here’s what CEO Dr. Sean Guest said about buybacks (emphasis mine):

“The best way to return capital to shareholders is through buybacks. When we buy those shares, we’ll cancel them. And we want to tell people that our shares are a very good investment at the current price. They represent a good investment.”

And they’re still investing in growth.

“We have so much cash flow that we can do all these things … acquisition, buybacks, production increases. Our cash flow allows us to do all of these things simultaneously.”

VLE is a Trifeca Lens trade.

It has outperformed nearly every E&P on a 1-YR and 3-YR time frame.

The stock is still very cheap. Thanks to $200M in tax losses, it will earn half its EV in net profits this year.

Oil prices and sentiment look like they’re bottoming and could significantly boost revenue and cash flows.

Your Value Operator,

Brandon