Lojas Quero-Quero (LJQQ3, “Quero-Quero”, or “Quero”) is the largest specialty home improvement retailer in Brazil with more than 400 stores in Rio Grande do Sul, Santa Catarina and Paraná. The Company offers its customers a complete solution in construction materials, complemented by home appliances and furniture.

Quero has barely tapped its addressable market and has a roadmap to doubling its current store count. Should it get there, it would generate over R$ 3.5B in revenue and nearly R$ 500M in EBITDA.

While its competitors battle over larger-city prominence, LJQQ3 is quietly dominating the small-to-medium cities throughout Brazil. The company has stores in ~315 cities. Only a third of their potential 915 cities addressable market.

While its competitors battle over larger-city prominence, LJQQ3 is quietly dominating the small-to-medium cities throughout Brazil. The company has stores in ~315 cities. Only a third of their potential 915 cities addressable market.

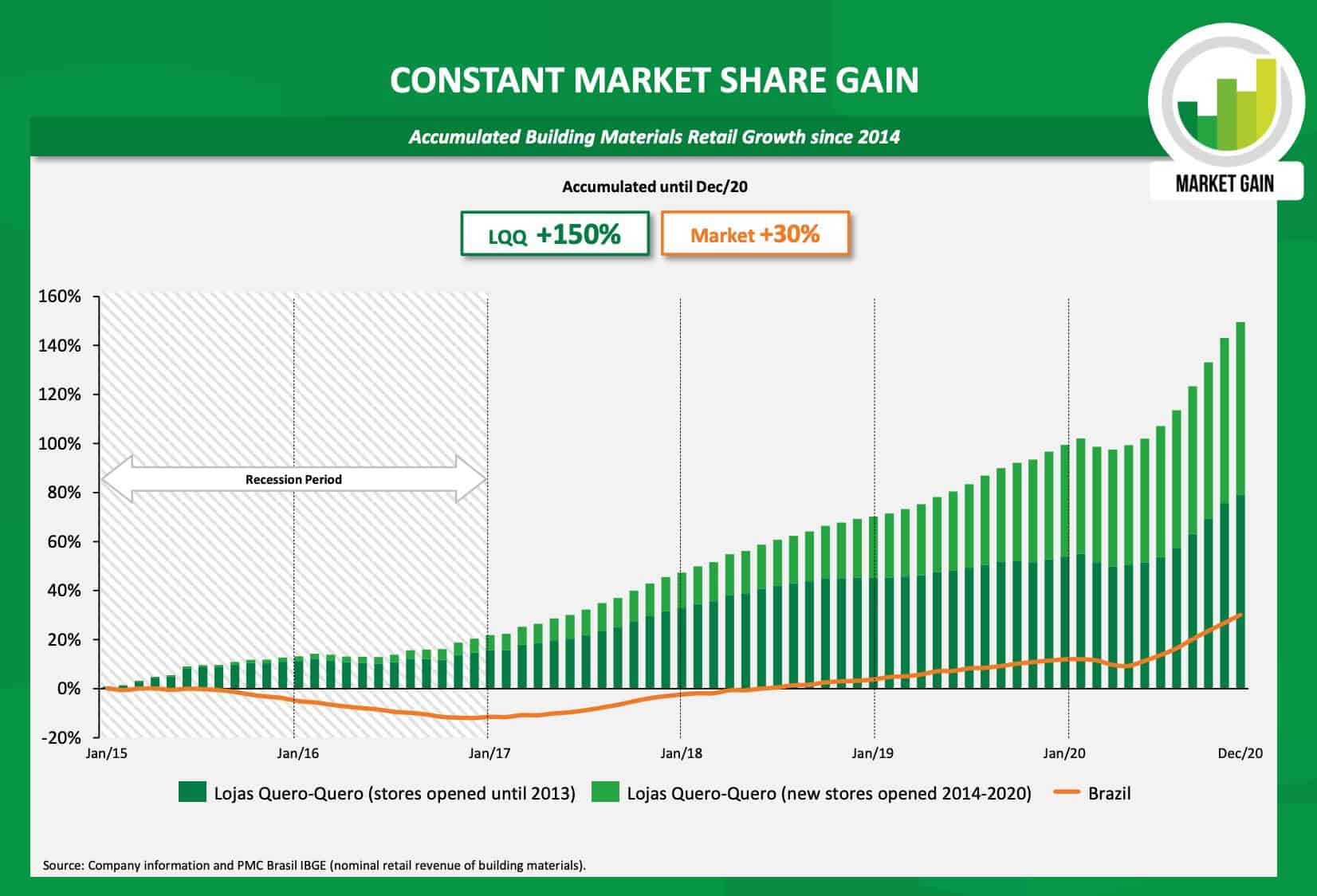

LJQQ3 is aggressively taking market share, growing 150% since 2015, while the rest of the industry has grown only 30%.

Historically, the company’s generated a ~26% ROIC while expanding stores at a 14.4% CAGR. This year, they plan to open 70 new stores throughout its existing 315 cities. It takes the company ~28 months to receive total payback from their initial build-out costs. In other words, investors reap the highest rewards ~3 years after the company builds a new store.

Our Variant Perception: The company plays an unfair game against its larger, more capitalized home improvement retail competitors. Here’s how. LJQQ3 designed its business model to work in small-to-medium-sized cities. Larger, big-box retailers can’t create good unit economics at such small demographics. In turn, large home improvement stores ignore the smaller markets, opting to play in their positive unit economics sandbox.

LJQQ3 is the only kid playing in their uniquely designed sandbox. They’ve created an unfair game that its larger competitors can’t entertain, and in doing so, exploited a vast addressable market with long runways for growth. For example, the company currently has a ~7% market share in its existing city base. LJQQ3 should expand stores at mid-double-digit rates with 20%+ ROICs as it penetrates existing cities and expands to 916+ potential cities. In doing so, the company will significantly increase market share and shareholder value over the next decade.

Creating The Unfair Game: Local Market Dominance

There are two ways home improvement retailers can build a business model. First, the big-box retailer model seeks large, highly-populated cities to plant mega stores. Think of Home Depot (HD) or Lowe’s (LOW) with massive parking lots and 100k+ SKUs. Unfortunately, such large stores only work in highly-populated cities due to higher initial build-out/maintenance costs.

There are two ways home improvement retailers can build a business model. First, the big-box retailer model seeks large, highly-populated cities to plant mega stores. Think of Home Depot (HD) or Lowe’s (LOW) with massive parking lots and 100k+ SKUs. Unfortunately, such large stores only work in highly-populated cities due to higher initial build-out/maintenance costs.

The second option home improvement stores have is to go small and operate in less densely populated cities. While there are distinct disadvantages to going small (fewer SKUs and less supplier negotiating power), there are unique advantages.

For example, smaller shops allow companies to foster relationships with local consumers, curate product mix based on a store’s specific region, and offer localized marketing communication. Over time, these advantages create lower customer churn and higher lifetime value (i.e., the higher the chances of becoming a “regular,” the lower the odds of shopping at other stores).

Quero-Quero chose to play the smaller game. Now, as Brazil’s largest home improvement retailer by store count, they’ve grown to enjoy economies of scale seen only by the largest big-box retailers.

The company went small for two reasons:

Small Cities Create Large TAMs

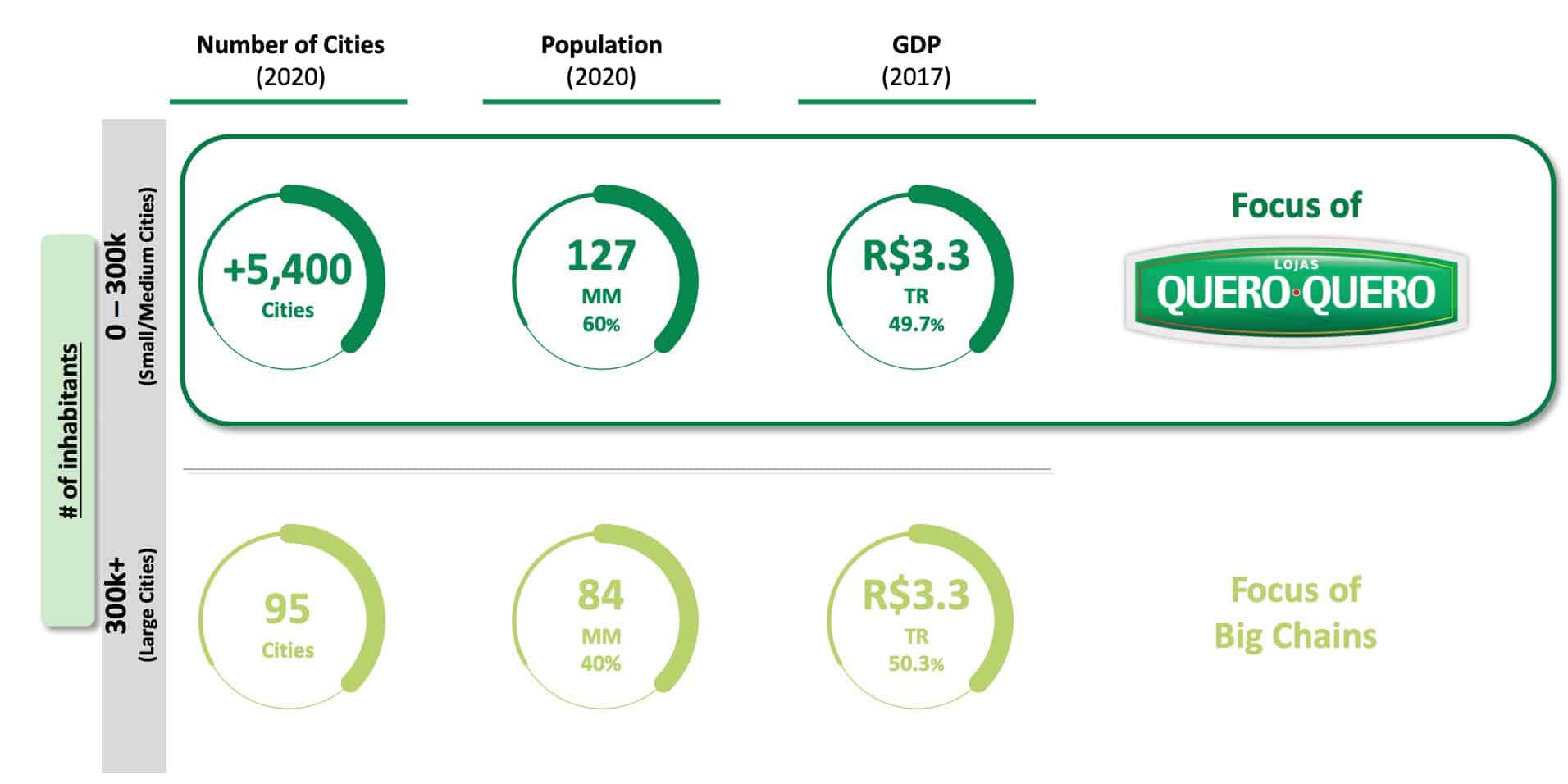

We can bifurcate Brazil into two groups by cities above/below 300K inhabitants. The 300k+ inhabitant group comprises 40% of the country’s population (84M), ~50% of Brazil’s GDP, and includes 95 of the country’s cities. Big retail chains focus on this group.

The >300K+ inhabitant group comprises 5,400+ cities, 127M people, and ~50% of Brazil’s GDP. Large box chains won’t open stores in these cities, leaving Quero Quero in a perfect position to take market share.

Untouched By Larger Home Improvement Retailers

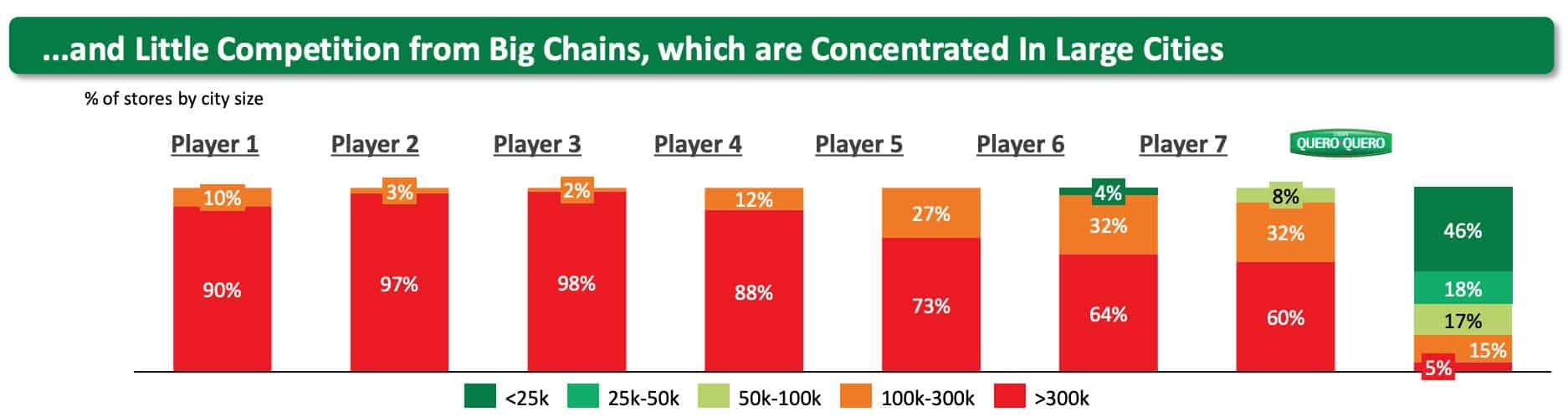

Big retail chains can’t touch smaller cities, leaving ~5,400+ locations up for grabs. These competitors only compete in large cities. For example, out of its seven home improvement competitors, only one retailer has stores in the towns with <25K inhabitants. Even then, those stores comprise ~4% of that competitor’s portfolio. In general, Quero-Quero’s competitors focus on 100-300K+ inhabitant locations (see below).

Quero-Quero: Flipping The Big Box Model On Its Head

Quero-Quero flips the traditional big-box retailer model on its head by intensely targeting cities with >300K inhabitants. For example, 95% of the company’s stores are in towns with >300K+ people. Moreover, nearly half (46%) of their stores operate in cities with >25K inhabitants.

It’s no surprise, then, that the company’s expanded its store count ~55% since 2017 (261 to 404). Without competition from larger retailers, Quero-Quero is left to compete against small mom-and-pop stores.

This is where the company can feel like a big-box retailer while maintaining the local flexibility of a small operation. Quero-Quero has 404 stores across the Southern region of Brazil with two large distribution centers (Santo Cristo & Corbelia).

Mom-and-pop shops can’t compete with Quero-Quero’s scale, which allows them to negotiate better pricing on goods while offering a wider assortment of products.

Plus, the company can offer its customers various financial products include credit cards and personal loans. 46% of the company’s stores operate in sub-25K populated cities. Quero’s credit financing options are one of the few ways these consumers gain access to credit in these areas.

Quero’s Growth Algorithm: New Store Expansion + Existing Store Maturation

The company has two main engines for future revenue growth and market share expansion:

- New store expansion

- Existing Store Maturation (increased same-store-sales)

Quero has 404 stores in 323 cities throughout the Southern Region of Brazil. That’s roughly 1.25 stores per city. The company has another 916 cities mapped for potential store expansion. If they add one store per mapped city, you will get ~1,320 stores throughout Brazil’s small-to-medium-sized cities.

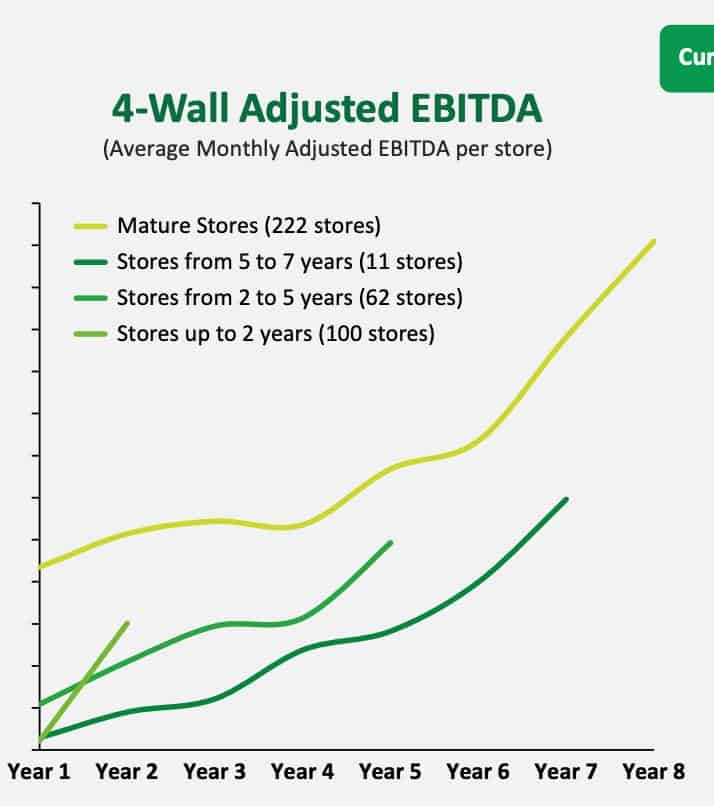

The second growth engine is exciting for long-term investors. Quero’s mature stores (i.e., 7+ years after opening) generate significantly higher EBITDA than any other operating period. In other words, each Quero store becomes more profitable the longer it operates. Currently, roughly half of Quero’s stores are “mature” stores.

To do this, the company remodels each store in three phases:

- Phase 1: Focus on Building Materials with wider inventory, more salesforce training, and dedicated logistics.

- Phase 2: Broader mix of Coating and Finishing, with project design service in selected stores.

- Phase 3: Increased focus on Paints, Coating, and Finishing, with specialized sales force, in-store customization services, and increased focus on the construction professional

Each phase increases the value proposition to the customer while increasing profitability through selling higher-margin products. Notably, Quero has barely tapped its Phase build-out across its 404 stores. For example, 9 stores are in Phase 3 mode (2.2%). In addition, 77% of the company’s stores remain in either Phase 1 or Traditional, Quero’s lowest-margin models.

Investors can think of the percentage of mature/non-mature stores as “Earnings Dry Powder” available to Quero over time.

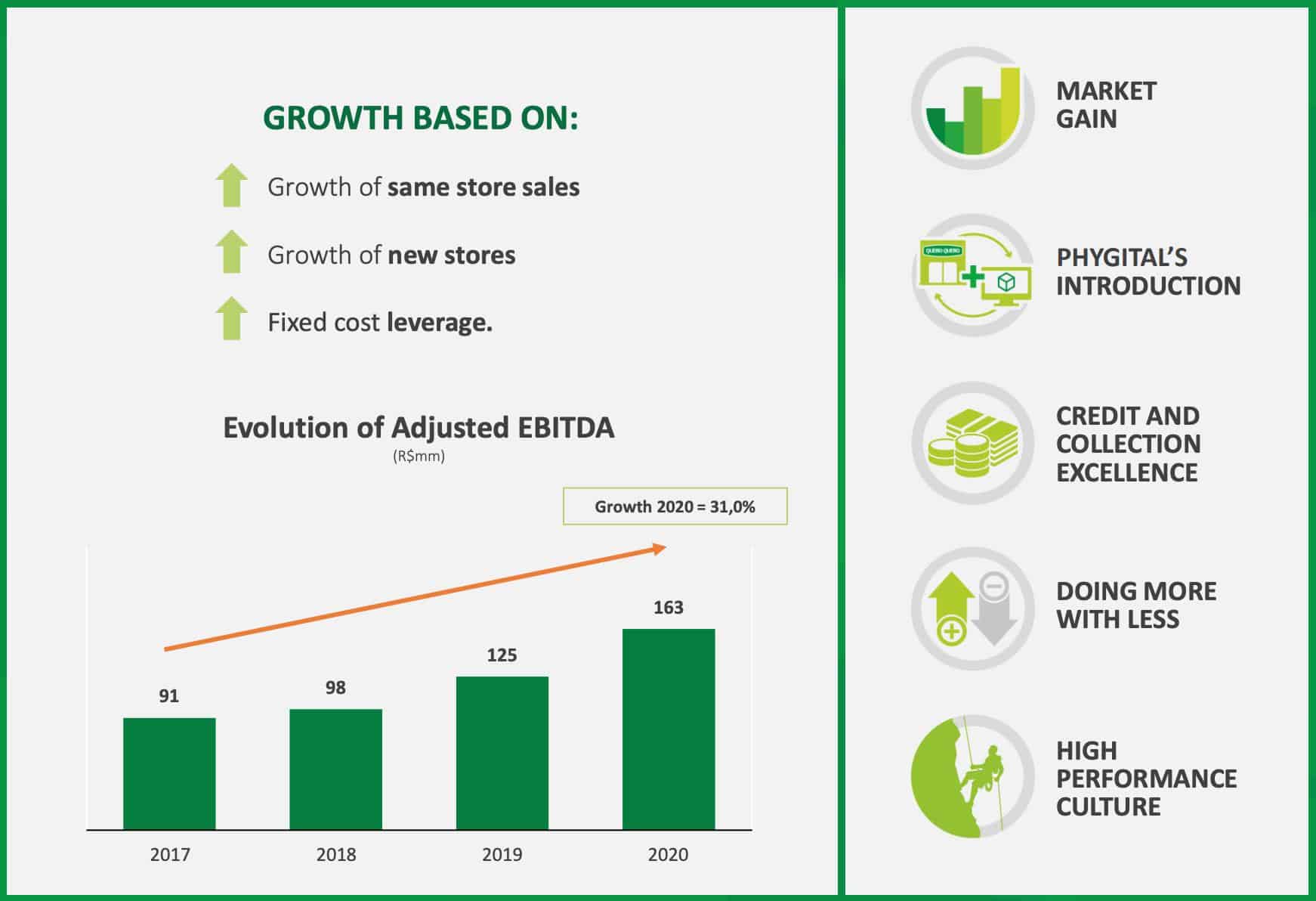

That’s not to say the company’s margin profile isn’t great now. Over the last five years, Quero’s expanded Gross Margin 500bps to 40% while nearly doubling operating margins (from 6% to 11.3%). Of course, we can’t estimate with any precision how high Quero’s margins can get on a run-rate basis, but today’s margins look like a floor.

Size of The Prize: What’s Quero-Quero Worth?

The company plans to open 70 new stores in 2021, increasing Quero’s total store count by 17%. Over the last three years, Quero’s grown store count by ~11% per year (2019 -2021). Next, we can estimate Quero’s average revenue and EBITDA per store using last year’s figures (the company generated R$ 1.62B in revenue and ~R$ 214M in EBITDA). That gets us R$ 4M in revenue and R$ 529K in EBITDA per store.

After 2021’s 70 store openings, let’s assume the company grows store count by ~14% per year for the next five years. That gets us to ~913 stores by 2026. Now, let’s assume the company generates roughly R$ 4M in revenue and R$ 529K in EBITDA per store over the next five years.

Though we know more mature stores generate higher revenues and greater profits, we’re not including that in our estimate. Under historical assumptions, Quero would end 2026 with ~R$ 3.65B in revenue and R$ 480M in EBITDA. Thus, investors are paying ~2x EV/2023E Sales and ~15x EV/2023E EBITDA at the current market price.

If we assume an investor would pay ~15x 2023E EBITDA, we get ~R$ 6.5B in shareholder value, or R$ 35/share. That’s ~52% upside from the current stock price.

If we assume an investor would pay ~15x 2023E EBITDA, we get ~R$ 6.5B in shareholder value, or R$ 35/share. That’s ~52% upside from the current stock price.

At that rate, Quero would command nearly 16% of its addressable market. Here’s the exciting part. Quero currently has ~1.25 stores per operating city. Our above assumption implies a 1:1 correlation between cities and stores served, or a quarter below historical city penetration rates.

Moreover, we’re not giving Quero the benefit of increased revenue and margin expansion as it remodels stores from Traditional to Phase 1, 2, and 3. Nor are we assigning any value to the company’s “Phygitial” omnichannel business offering, bringing big-box retail SKUs to the local level.

Risks: What Can Go Wrong?

There are a few critical risks with our bull thesis. First, big-box retailers could forgo short-to-medium term profits and attack Quero’s existing markets. This would damage Quero’s margin power and profitability as competitors with larger/more robust balance sheets slash prices to take share.

The second risk involves the company’s engagement in consumer credit products and customer financing. For example, 60% of the company’s revenues were paid via Quero’s own-brand credit card. An inability for consumers to make payments on time would result in higher delinquencies and a more significant proportion of product write-offs.

A third risk includes a consumer’s willingness to not choose in-person shopping. For example, suppose a customer wants to purchase home improvement goods online. In that case, they can just as quickly do so through a big-box retailer. In that case, Quero would lose its local competitive advantage as shoppers buy online.

Concluding Thoughts

Quero is an excellent business at a reasonable price. However, we’re looking for 25-30% IRR’s for new entrants, so we’d want lower prices before buying shares (somewhere between R$ 16-20/share).

The company plays an unfair game by going after the smaller markets throughout the Southern Region of Brazil. As a result, the company is competitively insulated from larger box retailers that can’t afford to open in smaller cities. In doing so, Quero also has an unmatched competitive advantage against its only remaining competitor in smaller markets, mom-and-pop shops.

Quero has two strong engines for future revenue growth and margin expansion in new store openings and the existing maturation of current stores. The hypothesis is simple. Over the next 5-10 years, Quero will have a much more extensive portfolio of stores. As these stores mature, they’ll generate even higher revenues and larger profit margins, creating an attractive investment.

The company positions itself as the clear leader in its category with long runways for growth and shareholder value creation by playing an unfair game.