It’s my favorite time of the year … Hedge Fund Annual Letters! We’ll spend the next few weeks reviewing our favorite value managers’ letters. We talk about broad market concepts, specific investment ideas and what companies they love most.

Before we dive in, make sure to listen to our latest podcast episodes:

-

- Episode 6: Joe Boskovich & Brian Laks, Old West Capital

- Episode 7: Andrew Wittman, PhD

Here’s the letters we’re covering this week:

-

- Woodlock House Capital Letter

- Vlata Fund

- East72 Capital

- RV Capital

Let’s get to it!

—

January 15, 2020

Y’all Are Record Long: Shoutout to Alex at Macro Ops for this week’s stat of the week. According to SentimenTrader, “y’all bought to open 21.6 million speculative call options. That’s the most *ever*. Your previous record was 19.7 million during the week of Jan 26, 2018. Your total bullish / bearish volume was the most since March 2000. So…wow.”

Greedy when others are fearful and fearful when others are greedy. Well, we know which way the “others” lean. How will we react?

___________________________________________________________________________

Investor Spotlight: Letters Galore!

GIFs by tenor

GIFs by tenor

We’re covering four investor letters this week. We’ll highlight the main theme of each letter as well as individual stocks mentioned.

Woodlock House Capital: +12.43% 2019

Chris Mayer ended the year up 12.43%. In his words, “If I could lock in a 12.43% return every year for the next 30 years, I’d take it.” We agree, Chris!

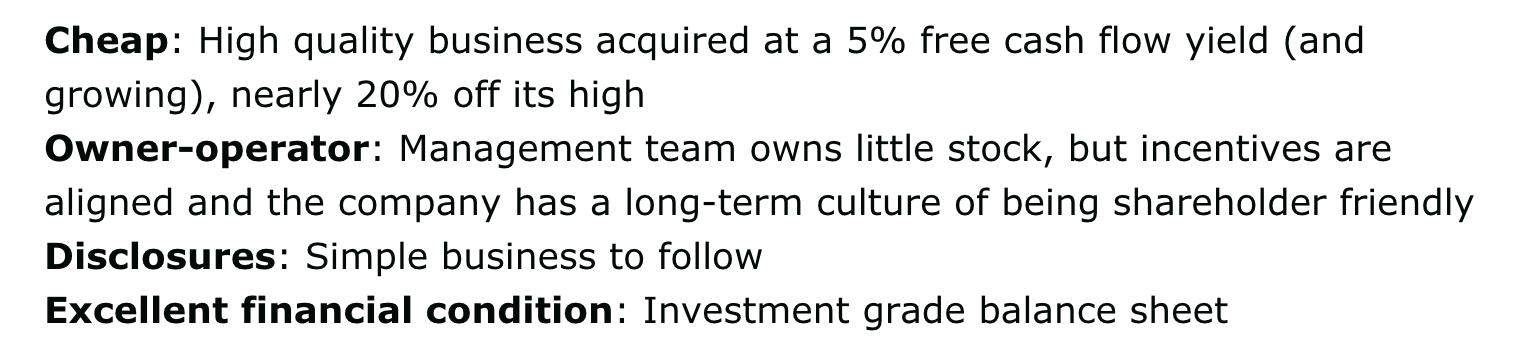

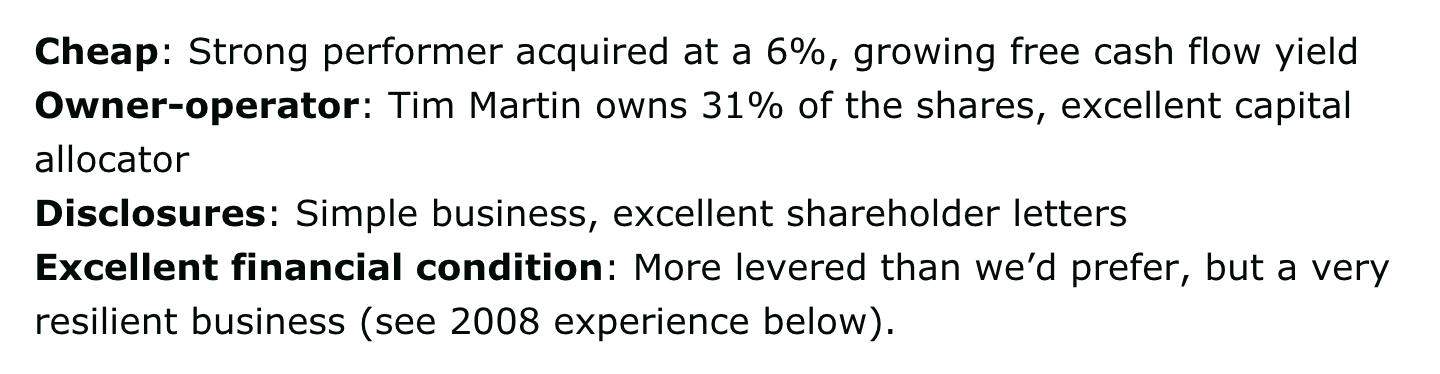

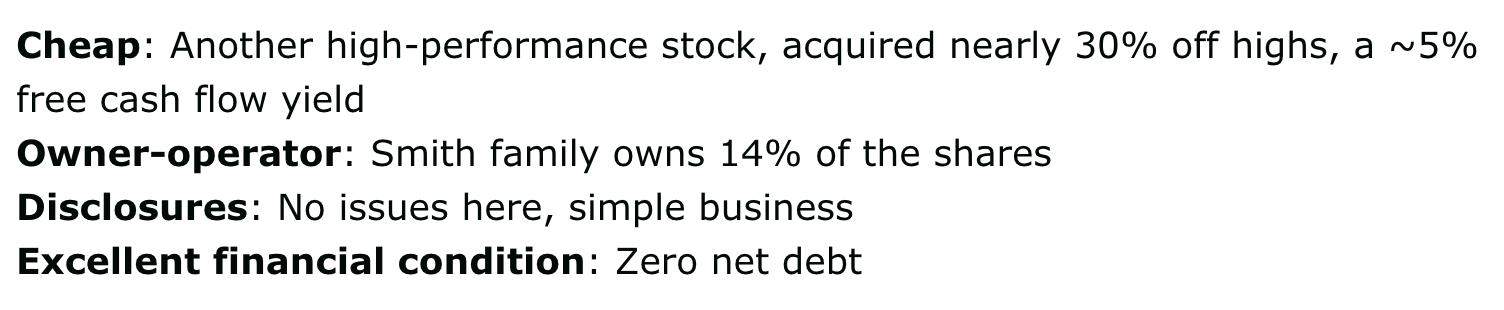

Woodlock House invests in high quality, low risk assets. To help him focus on such ideas, Chris uses the acronym CODE …

Cheap (Undervalued)

Owner-operator (skin in the game)

Disclosures (easy to follow)

Excellent financial condition

CODE is a great addition to anyone’s investment process. What’s not to love about each of those characteristics?

Portfolio Overview

Woodlock House owns fifteen stocks. The top five makes up around 42% of the Fund. Chris didn’t name all his stocks, but he mentioned eleven. Six old names and five new ideas.

The Old Names:

-

- Howard Hughes Corp. (HHC)

- Exor (EXO)

- Bollore (BOL)

- Fairfax Financial (FFH)

- Fairfax India (FIH-U)

- Air Lease (AL) — reduced position to 5.5%

As the above list infers, Chris spends a lot of time looking at international companies. In fact, a mere 35% of the Fund’s capital invests in US-listed names. Now onto the new names. Chris uses his CODE acronym for each new investment.

The New Names:

InterContinental Hotel Group (IHG.LSE)

JD Weatherspoon (JDW:LSE)

Next, Plc. (NXT:LSE)

Texas Pacific Land Trust (TPL)

AO. Smith (AOS)

Vlata Fund: +25.40% in 2019

Daniel Gladis returned 25.40% for the Vlata Fud in 2019. Since the Fund’s inception eleven years ago, Gladis’ returned 368.4%. That’s 33.50% annualized returns. Not bad!

Real-Time Intrinsic Value Estimation

Gladis spent the majority of the letter defending his choice to report estimated portfolio value along with NAV. In other words, Vlata Fund tells their LPs what the portfolio’s worth on an NAV (market) basis AND an intrinsic value (estimated) basis.

Here’s Daniel’s reasoning (emphasis mine):

“In the end, the following argument was what decided our internal debate: I consider the information on value to be very important and I also use it in portfolio management. How could I as a shareholder justify keeping that to myself and not provide it to the other shareholders? We did not find a satisfactory answer to that question, and therefore we began to publish data on the portfolio’s value.”

What’s interesting about this idea is its application to portfolio management. For instance, when the NAV is much lower than estimated intrinsic value, that might be a time to buy. Or, if NAV mirrors intrinsic value its a sign of a fair-priced portfolio.

Daniel offered two ways for investors to interpret the NAV-to-Intrinsic Value delta:

-

- The value development is a good indicator of future returns

- If you see that the difference between value and NAV becomes extreme, you can use it to plan your own investments.

This makes intuitive sense. But it goes against the mindset of so many investors. Investors tend to pile into a Fund after great returns. Yet they flee the scene after one bad year. But, if you have an idea of the Fund’s intrinsic value compared to its current “market price”, it changes things.

Portfolio Overview

Gladis doesn’t offer his portfolio in a direct way, but we can back into some holdings from his letter. Here’s a list of the holdings he reveals:

-

- Samsung (005930)

- Sberbank (SBER.RU)

- BMW (BMW)

East72 Capital: -6.15% Q4 2019

Andrew Brown and Marc Lerner returned -6.15% in Q4 2019. If you take away their short position in TSLA, the Fund returned a positive 6.15% for the quarter. The majority of the letter deals with the company’s long-standing investment in Exor (EXOR).

Deep Dive Into Exor NV

Brown and Lerner offer six reasons why they continue to hold EXOR (direct from letter):

-

- EXOR is now moving to extract added value from CNH, through an intended spin-off of its US$13billion “on-highway” bus and powertrain business …

- CNH has been placed on a path to far higher margins across the two businesses intended to double pro-forma earnings over four years; if achieved this would give scope for a significant $4-$8billion uplift in the value of Exor’s holding;

- EXOR continues to reduce its dependence on the value of the traditional ICE (internal combustion engine) auto business of Fiat via more capital extraction (two dividends paid in May 2019 and the further $1.78billion attributable dividend payable late in 2020 on merger with Peugeot)

- EXOR’s debt to gross asset value is down around 13% (gross) and 10% (net) – the lowest since the PartnerRe acquisition in 2016

- The equity market’s pricing of Exor shares seems to have ignored the significant uplift in the price of reinsurance company stocks in the past year.

- Exor is still cheap on the basis of the price of current portfolio investments without imputing any uplifts from the initiatives highlighted

New Investment: Yellow Brick Road Holdings (YBR.ASX)

East72’s newest investment is Yellow Brick Road Holdings (YBR). The company provides wealth management advice to retail and SME clients in Australia.

Here’s East72’s take on YBR’s history:

“Over the past two years, YBR’s inability to consistently produce a profit, partly brought about by unsustainable overheads designed to grow the group, allied to a decline in the home loan market, has seen the company’s share price decimated, falling by over 90% at one stage from the placement price in 2014. Moreover, previously supportive shareholder Macquarie Group divested its shares at prices between $0.09- $0.14 in mid 2018.”

Brown and Lerner think the future will look much different than the past. According to the duo, YBR can increase revenues and profits from four areas:

-

- Vow, a lower margin high volume mortgage aggregator

- YBR franchisees acting as brokers

- Resi MOrtgage Corporation

- Resi Wholesale Funding which manufactures mortgages

East72’s position in YBR is around 1/3rd of their estimated $0.22/share capital cost. Here’s the rest of their valuation pitch:

“In total this suggests YBR to be worth ~$0.20/share, prior to proving the existing structure can provide sustainable growth.”

RV Capital: +31.20% 2019

Robert Vinall returned 31.20% in 2019, beating the DAX by 5.70%. Since inception,. Vinall’s returned a whopping 649.6%, or 19.6% annualized. This compares to the DAX’s 7.6% annualized return during the same period. Not bad!

Robert’s letter is great. He discusses his dinner with Charlie Munger, a trip to South Africa and a new investment.

Diversification with Charlie Munger

One of the biggest takeaways for Rob from his dinner with Munger was on the topic of diversification. According to Rob, Charlie explained that one needs a mere two stocks to have proper diversification. Two stocks. Even a manager like Rob looks over-diversified with his ten stock portfolio.

Robert believes in his diversification methods, saying, “Despite Charlie’s admonitions, I have no regrets about holding around 10 stocks.”

Pessimism in South Africa

Earlier we discussed how investors are very optimistic about US markets. The reverse is true in South Africa. Everywhere Rob went he saw one thing: Pessimism. Rob mentions, “The people I met in SA were overwhelmingly pessimistic.”

This type of news should make our ears perk up as value investors. Greedy when others are fearful, right? Rob agrees (emphasis mine):

“If I put my investor hat on, the best time to invest in a country is when the mood seems darkest. Investors in Zimbabwe or Venezuela may beg to differ, but these countries strike me as exceptions that prove the rule. Cycles move in, well, cycles, not precipitously to the bottom. Germany, when I moved there in the late 90s, was the sick man of Europe. More recently, Greece was considered the basket case to end all basket cases. Cycles turn.”

I agree. Robert also discusses a new South African company that got his attention, Discovery (DSY).

Discovery (DSY): Health & Life Insurance

DSY is a health insurance platform aimed at improving the health of its members. Through incentives, the company works to lower insurance costs, increase life expectancy and reduce hospital visits.

According to Rob, the model works due to Shared Value. As the business thrives, so does its end customers.

DSY’s rolling out its platform, Vitality, to 14 insurers across 23 markets. Their goal is get 100 million people 20% more active. So far the model’s working. The company generated over R1.2B in 2018, paid a 1.78% dividend and sports attractive 14% pre-tax margins. Mr. Market’s offering DSY at 12x current earnings.

Rob doesn’t own DSY. He prefers tracking a company for years before making an investment.

Here’s what the charts look like …

RV’s Newest Investment: Wix.com (WIX)

Robert runs WIX through his list of investment questions:

-

- Does management set the right example?

- Is the moat widening?

- Is the price attractive?

According to Rob’s thesis, WIX checks off every box.

-

- Almost every senior executive at WIX has been with the company since the beginning.

- WIX sports five areas of competitive advantage (moat-widening):

- User stickiness

- Cost Advantages

- Data Advantages

- Brand

- Culture

- Robert estimates WIX will be worth $200/share by 2024 assuming steady-state FCF of $900M.

Here’s the chart …

___________________________________________________________________________

Resources of The Week: Table Stakes & Expectations Investing

GIFs by tenor

GIFs by tenor

Brent Beshore wrote a great piece on how to “unlock” a small business. Asking the right questions is vital to any investment decision. Brent categorizes the questions by topic (Operations, Finance and People). Here’s his list of Operations questions:

I’ll leave it to you to read the rest!

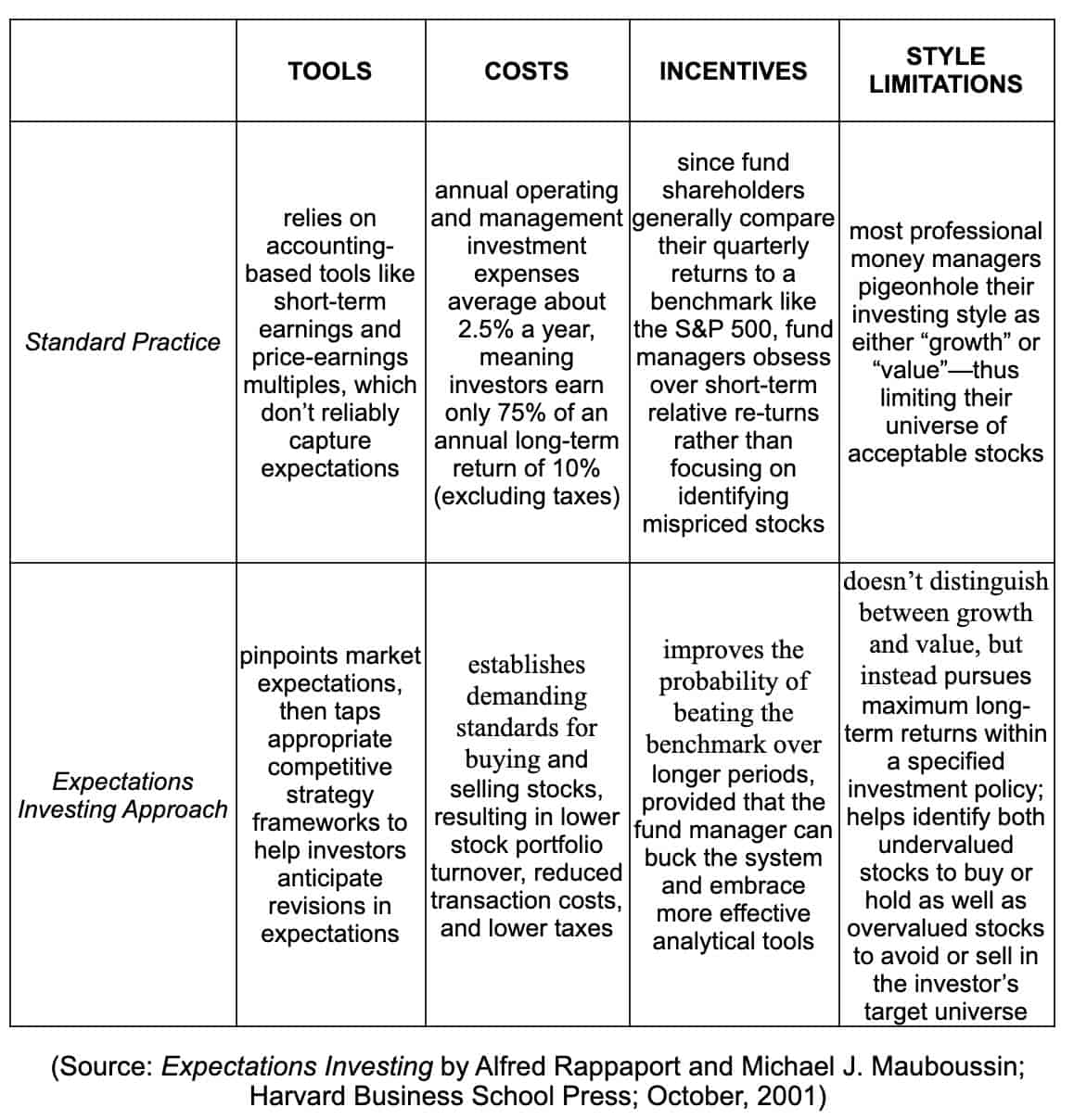

Expectations Investing Tutorial

I’m sure I’m late to the party, but Michael Mauboussin’s 11-part tutorial on Expectations Investing is fantastic. Best of all, it’s free. You can start the course here. As a teaser, here’s the difference between Expectations Investing compared to traditional investment thinking:

___________________________________________________________________________

Tweet of The Week: All The Accounting You Need

Deciding to purchase a stock, which is an interest in an actual real life business, without looking at a decade-long period (financial data, MD&As, etc) is like going to a firing range in the dark and trying to hit a target.

— The Rational Walk (@rationalwalk) January 13, 2020

That’s all I got for this week. Shoot me an email if you come across something interesting this week at brandon@macro-ops.com.

Tell Your Friends!

Do you love Value Hive?

Tell your friends about us! The greatest compliment we can receive is a referral (although we do accept Chipotle burrito bowls).

Click here to receive The Value Hive Directly To Your Inbox!