A few months ago, I shared a longer-form essay on Bowl America’s CEO Annual Shareholder Letters. Those letters (twenty-four in total), told the story of owner-operator Leslie Goldberg. Goldberg won’t win any 100-bagger awards, nor will his name appear on any Forbes 500 list. Yet the man excelled at his job. He stewarded a company, grew its earnings, and never had a losing year in 24 years of operations.

I received greater feedback than I could’ve imagined after posting the essay. After encouragement to write another similar piece, I had a goal. Find another Leslie Goldberg.

In reality finding such an operator proved challenging.

As always, I wanted to find an outsider, a CEO you hadn’t heard of. Sure I could write about Constellation’s CEO, or Richard Branson, or Jack Welch. But what value does my “n”th article bring to an already saturated topic? Like my investing style, I went off-the-beaten-path.

After a couple months of searching, I found the Reed family and Mestek, Inc. (MCCK:OTC).

Mestek (MCCK) manufactures and sells heating, ventilating, air conditioning products; and metal forming equipment in the United States and internationally. The company is a collection of family-owned businesses rolled together into one, public company. Think of Brent Beshore’s Permanent Equity, but for HVAC equipment and the sort. MCCK feels like a private equity company. You’ll see it in their shareholder letters.

Over the course of this essay, we’ll look back at 11 years of shareholder letters, starting in 2007. We begin with Mestek’s founder and CEO, John Reed. Reed penned the 2007 – 2009 letters. Then, in 2009, his son’s name, Stewart Reed, appeared on the letters. John Reed passed away in 2013. Stewart stepped up as CEO that same year, and the rest is history.

These letters, like most great corporate governances, sound like broken records. That’s a good thing. I found a few common threads woven in through each of them:

-

- Dedication to the company’s people, culture and acquired businesses

- Tireless effort to play the multi-iteration game as best they could

- Disdain for dividends

- Creating a sense of long-term ownership, buying and building forever

These themes worked. Since Reed took the helm as CEO, MCCK’s grew from $13/share to over $27/share. That’s a 118% return in seven years. Not bad.

We’re in the midst of one of the scariest bear markets in financial history. It’s moments like these where investors need reassurance. They need to readjust their True North. With countless stocks down 20, 30 or 50% from their highs, Stewart Reed’s letters act as the standard metric in which all company corporate governance should be judged.

All bolded quotes from the letters are my emphasis.

Letters from 2007 – 2009

2007: Focusing On Right Metrics, Sarbanes Oxley & Balance Sheet

“While it is always encouraging to do better rather than worse, your management is not particularly proud of the year’s financial results. We should be earning a considerably higher return on total capital employed and we will not really be satisfied until we do.”

-

- Reed doesn’t measure success by earnings per share or the percentage dividend yield. Rather it’s the return the company generates from its excess cash invested. That’s arguably the best way to measure a company’s success, yet we see so little of this mentioned throughout most CEO shareholder letters.

“Operating as a private company has definitely increased our overall efficiency and freed up some significant time for senior executives. Our G and A expenses for 2007 are budgeted at about $1,000,000 less than the 2006 actual expense, despite allowing for appropriate salary increases, mostly because of the avoidance of Sarbanes-Oxley and the costs of SEC regulations.”

-

- Many companies go dark for the above reasons. There’s a negative stigma around dark companies, and perhaps some of it makes sense. There’s a number of crooked businesses lurking in these corners.

- For many micro-cap companies, going dark unlocks capital that management can plow into the business to generate excess returns. Think about MCCK’s case. They were spending around $1M to list on the exchange and comply with Sarbanes-Oxley.

- It raises the question, though. If it’s so expensive for micro-cap companies to list, why do they? Why don’t they all go dark? It’s an interesting question and one which I wish I had a better answer. Here’s my (elementary) take. The opportunity cost of increased liquidity outweighs the expense of complying and maintaining regulations. But I’m in the market for a better explanation!

“During the next two years, we will be giving particular attention to our balance sheet as well as to our earnings and cash flow. While our financial position is fully adequate to our current needs, we have developed a specific program to improve it by the sale of unneeded facilities, inventory reduction and maximizing cash flow.”

-

- I like when CEOs offer quantifiable goals for the year(s) ahead. Reed informed shareholders of his plans, and in turn shareholders can track the performance of the CEO. CEOs that present lucid or opaque plans fall victim to never delivering outsized performance.

2008: Goal Setting & Pitfalls of GAAP Accounting

“Our Dundalk, MD manufacturing plant was closed and the building sold. The Waldron, MI facility was closed and operations combined with the American Warming plant at Bradner, OH. The leased factory at Pacoima, CA was closed at the lease termination date of September 30 and its products moved to our factory at Carson, CA. All of these moves should result in improved profitability for 2008 as overhead expenses have been reduced without loss of volume.”

-

- At the end of 2007 Reed had one goal in mind: strengthen the balance sheet and improve cash flow / earnings. He accomplished his goal in one year. This is why it’s important to review management’s decisions over time. How successful were they in doing what they said they would? Are they all talk and no action? If so, that should play into your valuation work on the company’s future.

- We often forget that you should discount not only future cash flows of the business but management’s promises.

“An accounting charge resulting from our investment in CareCentric, a software and service provider, penalized our GAAP reported earnings by $6,735,000, made worse by the fact that we received no tax benefit on this paper “loss,” the details of which are contained in the notes following the consolidated statements of operations … CareCentric, with its substantial customer base and respected product, has, in my opinion, real value which should eventually be realized, however, GAAP accounting, being rule-based rather than principle-based and applying the equity method rule, counts 45.53% of CareCentric’s own losses as though they were Mestek’s. Hence, the $6 million plus charge.”

-

- Reed emphasizes a common pitfall of GAAP accounting: rule-based. GAAP accounting is rule-based, not principle-based. In other words, the point of GAAP is to systematize everything. Make all accounts and statements fit into a neat, little box. In most cases, this works — and GAAP accounting provides a wonderful way to measure an enterprise’s operations. Yet when it comes to these types of issues, GAAP accounting can turn a lousy year into a disastrous one on paper.

2009: How To Survive a Recession, Mestek’s Guide

“During 2009, Mestek gained a deeper understanding of the ancient Chinese proverb, “May you live in interesting times”. The proverbial black swan, so well explained by author Nassim Taleb, appeared on our doorstep. Like many other American manufacturers, the absence of alternatives cleared our minds. Mestek needed to cut expenses, and cut them rapidly, to react to a rapidly shrinking order book.”

-

- It fascinated me to see Reed quote Nassim Taleb (one of my favorite authors). I also liked how Reed laid out a simple strategy for dealing with the black swan that was the GFC. His plan was simple: cut expenses and cut them rapidly.

- Like a trader wanting to protect his capital by cutting losers, business owners find refuge in trimming the fat. Reducing the unneeded, before shifting attention to top-line growth.

- In the throes of a recession, survival was the only goal. Reed (if I had to guess) didn’t care about growing revenues, earnings or cash flow. All he cared about was What helped him survive? A strong balance sheet and drastic employee cuts.

“Mestek has been proud of a long record of minimal layoffs and restructurings, providing opportunity and stability for its employees. That record came to an abrupt end in 2009. Mestek will endeavor to restore its former reputation as a business offering stability and interesting careers to our capable current and future employees. Unlike some businesses in today’s fast-paced world, Mestek has always believed in career employees in all areas of the company, and has offered a high degree of stability to loyal, capable, and dedicated people.”

-

- I love this quote from Reed. Company culture, loyalty, and stability matter. If you want to build something great — something that will last — you need some semblance of stability and loyalty within the trenches.

- People often compare business to war. In some ways, this is a complete over-exaggeration but in other ways its the perfect analogy. Loyalty to a business and stability within the organization. Those things percolate through military ranks. You also find them in the best-run businesses. How do these qualities manifest in the day-to-day operations of a company? Here are some examples:

- Employees stay late when they don’t have to

- Everyone loves what they do

- Company incentivizes long-term ownership

- Employees take pride in their work and where they work

“The balance sheet remains strong; the revolving bank indebtedness declined to $8.9 million from $24.6 million. The reduction would have been $8.2 million greater, reducing bank debt to almost zero, had we not acquired CareCentric minority interests and refinanced its outstanding revolving bank line of credit. Long term debt remains low, approximately $6 million, versus equity of $120 million”

-

- A theme we see throughout the first three letters is an emphasis on having a strong balance sheet. A strong balance sheet carries its weight in gold during black-swan environments like 2008-9.

“Your company continues to look for genuinely synergistic acquisition opportunities available at an equitable price. We realize that a majority of acquisitions prove to be a mistake for the acquirer; therefore we set a high standard for ourselves. Management egos, or growth for growth’s sake, will never be an acceptable element in any acquisition. Two plus two must have reasonable prospects of equaling five within a year or two from the acquisition date. Your management has a big stake in the future of Mestek, clearly evidenced by a large ownership position. We regard Mestek’s financial resources the same way we regard our own, a willingness to assume risks up to a point, but only when we are reasonably convinced that the risk/reward equation is favorable. And we would never “bet the store”; we are builders, not gamblers.”

-

- This is by far my favorite quote of any letter to this point. Reed offers a perfect blueprint for how owners should think about acquisitions. Let’s break each part down.

Mestek’s Acquisition Philosophy:

-

- An equitable price

Don’t overpay for an acquisition. I know, it’s not news to you. But in low-interest-rate environments, it’s tempting to stretch the definition of “equitable price”.

Another way to think about paying an equitable price is to inverse the question. How can you overpay for a business? There are a few ways:

-

- Paint too rosy of a future for the acquisition.

- Assume nothing will go wrong during the course of transition/business operations

- Not buying with a margin of safety

- Paying too high of a multiple for the business

All these things distort the reality of the situation and help you justify any purchase price. Want to buy a business for 14x EBITDA but are worried about your return? Don’t worry! Simply increase your projected earnings growth rate and lower your borrowing costs. Problem solved.

-

- High hurdle rate for potential deals

I love this piece. A high hurdle rate does two things for an investor or business owner. First, it reduces the number of transactions. Whether it’s stocks or entire businesses, both involve transaction costs.

Again, you don’t want to buy okay businesses. All else equal, it takes the same time, research and transaction costs to buy a great business. So why not wait until you find a great business?

-

- Never do a deal to stroke management’s ego or for the sake of growth

Business owners — like investors — get an itch to make a deal or buy a company. Inactivity is viewed as a negative in most cases. After all, if you’re an investor or business owner, isn’t your job to make deals? Well, yes. But your first priority is to not screw things up. Don’t do anything stupid.

I love Munger’s thoughts on this premise: “We try our very best to not do anything stupid. You’d be surprised how far you can go by trying not to do anything stupid.”

-

- 2+2 must equal 5 in 1-2 years

Another crutch employed on sub-par deals is time. If you stretch an investment out far enough, it’ll generate a great return. Pay 16x owner earnings for a business? That’s fine. 16 years from now you’ll have your money back and keep the business for free. After all, this is a long term investment.

It’s easy to fall victim to that type of thinking. And it’s not our fault. We’re taught by the greatest investor in the world (that guy from Omaha) to buy and hold for the long term. If you buy a good business at a decent price and just hold on, you’ll do just fine.

The problem with that is most businesses (and their shareholders) don’t have that kind of time. Great acquisitions add value almost immediately. If you’re hoping to break-even in year five or six, move on to the next deal.

-

- Never bet the farm

This rule ties into rule #3, specifically regarding ego. Our ego doesn’t help us make investment decisions. In fact, it’s our worst enemy. Overconfidence can cost your business (or your investment account) the ultimate price. Permanent loss of capital. Most investors have some form of risk management. A tried-and-true capital preservation strategy. Great traders risk no more than 1% of their capital on a trade.

But why do they do that? After all, these traders and investors are at the top of their game. They’re the best. Why not bet the farm if you’re that good? The reason is simple but profound: It doesn’t matter how great you are at investing, trading or buying businesses. You can always be wrong on your next try.

That’s why risk management is key. That’s why you don’t bet the farm. You never know when your next error will occur. But you know one thing, it will happen at some point. Create a strategy to protect yourself from your worst enemy — you.

Letters from 2010 – 2012

2010: Making Decisions Without All The Facts

“William Burroughs observed that paranoia is sometimes a condition brought on by having all the facts.”

-

- In business, investing and life you won’t have all the facts. Yet you must make decisions. Do you buy shares of a company even though you don’t know all the facts? Do you propose to your significant other, knowing you might not know their true feelings?

- Here’s the freeing part: you’ll never have all the facts. This realization frees up the investor to make decisions without 100% knowledge of the company. Why? Because nobody else has perfect information either (barring anything illegal). It’s an even playing field.

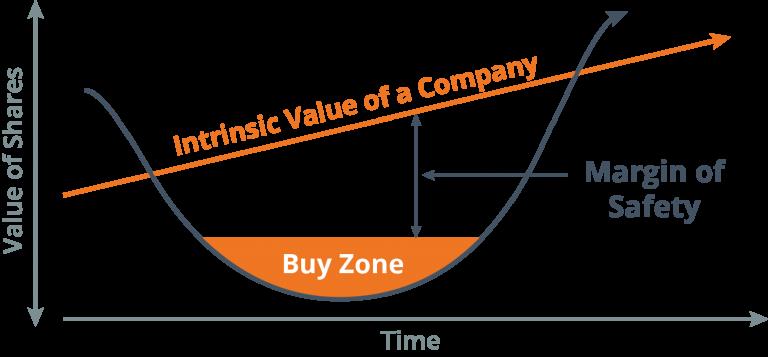

“Despite the bullish stock market, it is difficult to be optimistic about the American economy, and the construction and machinery industries in particular. All of the inflation-adjusted growth in the U.S. economy during the past decade has been the result of increased government spending and home equity withdrawals. The real growth is evidenced by debt and not equity in the consumer and government sectors of our economy.”

-

- Amazing how relevant that quote is to our current market situation (March 2020). I like to imagine the intrinsic value vs. market price chart shown below (source: Miller Value):

2011: The True Power of Balance Sheets

“As makers of capital equipment, we have noticed that our customers and their customers, who are the owners of large businesses, are now quite interested in the financials of their suppliers. This has been a comparative advantage. As our financials show, Mestek has built dependable, long-lasting quality products over the years and will continue to do so for many years to come.”

-

- Balance sheets always Sometimes they go in-and-out of focus. At the end of the day, defense wins championships. Solid balance sheets beat weak balance sheets.

- Normally we think of strong balance sheets as a prerequisite for making an investment. But it goes beyond that. A strong balance sheet signals to your suppliers, customers, and shareholders that you’ll weather the storm. That you’ll right the ship. A strong balance sheet is more than an investment criterion — it’s a badge of honor during market downturns. If that’s the case, investors or business owners should focus on a strong balance sheet at all time

2012: People Matter, Dividends Don’t

“Mestek’s balance sheet remains very strong, $120M of shareholders’ equity offset by $12M of debt, a ten to one ratio. The company paid a $3.00 per share common stock dividend during December of 2012 to reward our patient investors, and to partially escape the long and grasping arm of government.”

– Infrequent (or special) dividends are a sign of an in-tune management company. These are more shareholder-friendly for two reasons:

-

- Creates more capital allocation opportunities than a regular dividend

- Shows that management is in tune with the intrinsic value and return capabilities of their business

Many companies choose to pay dividends because they can’t generate higher returns in their business. But if a company pays special dividends, they’re free to bounce between reinvesting in their business. They can deploy capital to shareholders when opportunities dry up.

“Let’s return to well-defined priorities. First and foremost, it’s all about people, especially leadership, but still people in every job throughout Mestek. Today’s leaders, tomorrow’s leaders, engineers, software developers, sales executives, plant managers, industrial engineers, technical support professionals, I could continue the list. Competent people with a desire to win, a desire to exceed customer expectations, a desire to lead others to a better and more interesting future are the key to our present and future endeavor.”

-

- I love this quote. Every business should have something like this as part of their ethos. Again, it’s the specifics that matter. It’s not enough to have competent people working at your company. You can always hire someone competent. But you can’t always hire someone with passion, drive and a desire to win.

Reed continues …

“Each exceptional person within Mestek should have the opportunity for quality mentoring and training, a chance to broaden his or her skills. Your management regards this as a top priority, not an afterthought.”

-

- Turnover is expensive. I discussed this idea of turnover expense with Dr. Andrew Wittman on the Value Hive podcast. You can check it out here.

- From a business owner’s perspective, there are two choices when it comes to investing in employees. First, you couldn’t. That’s an option. But you risk stagnating both your employees and your business. You also risk a higher turnover. The other option is to invest in your employees. Granted, they still might leave — you can’t stop them if they’re hell-bent on going somewhere else. But what you can do is create an environment where they don’t want to leave.

- Think of GOOG, FB and most top-tech companies. They invest heavily in their employees, making sure they have everything they need at work, as well as extracurricular growth opportunities/incentives.

“Some of this [R&D] spending is already bearing fruit, some we believe will bear future fruit, some we hope and pray will pay off, and some will likely be wasted. Whatever the results prove to be, we will celebrate our successes and learn from our failures. R&D, and much of business in general, remain all about risk versus reward, an ancient and deep-rooted underpinning of capitalism. We will continue to try to make ‘odds on’ bets with your money.”

-

- There are a couple of things I like from this quote. First, notice how Reed phrases “your money”. It sounds drab, but it’s powerful. Reed’s spending shareholders’ hard-earned cash on R&D investments. When phrased in that matter, it creates both a sense of responsibility within management, and it makes shareholders feel like actual owners. Fantastic wording.

- Second, Reed is honest about Mestek’s R&D process. He notes that some ideas will work well, others will break-even and (hopefully) a few will go to zero. It’s the same philosophy shared by the world’s best investors and traders. Some investments will go to zero, others will break-even. But a select few will provide all the returns. It’s the Pareto principle in its purest form.

Reed finishes the letter with a nod to his patient shareholder base …

“Although Mestek is a family company built-in that American tradition, your management is keenly aware of its fiduciary responsibilities as it spends and invests your stake in the business. You have entrusted this management with a part of your financial wealth, and we pledge to never lose sight of this fact. You deserve an above-average return; your management will strive to realize this reasonable objective.”

What a quote — who wouldn’t park their money with a guy like that?

Letters from 2013 – 2015

2013: Capital Allocation, Keeping Employees & Growth Strategies

“Your management believes that business consists of three major disciplines: people, strategy, and operations, and that people are the most important of the three. Years ago your company planned to move a product line. The planning was meticulous and the physical move proceeded smoothly. We were ready to begin production on schedule. But, a large consequential but, the people and the culture were wrong for the task; and the results were unhappy customers and financial losses, an important lesson learned. People are the deciding factor.”

-

- Once again we see an emphasis on people. This is a hallmark of a great leader and great corporate governance. It’s also a lesson on having great products and processes in place, but with the wrong people, the value of such luxuries reduces to zero. Yet as we mentioned in the previous letter, your people are only an asset if you can keep them around. Reed reveals how Mestek retains its talent …

“When an opportunity arises to hire an exceptional person in our industries, we often do so whether we “need to” or not, regardless of whether we have a specific job opening at that time … In this way, Mestek is a throwback to an earlier era, a time when an employee expected to spend his or her entire career with one company. We all have the responsibility to learn, grow, and improve our skills each year throughout our careers; that said, we are proud to be a throwback company for employees who do so.”

-

- Imagine being an employee and reading your company’s annual shareholder letter. How good would it make you feel? To know that management cares that much about its people and culture? Pretty damn good if you ask me.

“We strive to grow organically with new products, higher market share, and new untapped markets; and we are always eager to provide a good home for other businesses in our industries. Mestek has acquired a substantial number of companies during our sixty-eight year history. mostly private family-owned enterprises. Our track record of preserving local employment, and respecting the people and culture of these businesses is apparent, a source of great satisfaction for us.“

-

- If you replaced “Mestek” with Brent Beshore’s “Permanent Equity“, could you tell the difference? Mestek takes a long-term, permanent equity approach to acquiring family-owned businesses within their niches. Here’s the key point: they do whatever they can to not screw things up when they buy.

- In other words, they keep the local management in place, keep the employees — let the business operate the way it wants. Who’s to say you’re going to go in and make changes that are positive for the business?

I love how Reed ends this paragraph, it’s something I wish every CEO of a public company would utter:

“Unlike private equity firms, we buy, build, and hold, forever. We become part of their culture and they become part of our culture. Traditions matter.”

Love it. You can’t value sentences like that through a screener or a DCF model.

“Mestek believes in a relaxed management style. We strive to win, but not at any cost. Having fun along the way, for all of us, is also a part of our culture. We try to succeed by making work a liberating and creative experience, an activity worth doing on its own merits, not simply for a paycheck. We ask people to do the job and then allow them to do it their way within reasonable limits, no one size fits all attitude.”

-

- There are a few things we can pull from this. First is the idea of a “relaxed management style.” I like how Reed mentions the company strives to win, but won’t cut corners or engage in shady business to get there. Reed wants employees to love working at Mestek. Plain and simple.

- Also, note how Reed sounds like many Silicon Valley software companies. In a way, I can see why Mestek wins in their business. People take pride in their work in an otherwise reluctant business. Mestek’s business isn’t the type of enterprise that would turn people’s heads at a bar. Maybe that’s a good thing.

“My primary role is capital allocation, compensation, asking the right questions, and helping the people who do the heavy lifting. Who could ask for a more interesting and enjoyable job?”

-

- Wondering what the job of a CEO is? Look no further than Reed’s quote. Once you trim the fat, you realize the job of a CEO is simple (don’t read “easy”). Capital allocation, compensation (which ties into capital allocation), asking the right questions and helping the people on the front lines.

2014: Interest Rates, Financial Engineering and The Ideal Shareholder

“Consider M&A activity in a near-zero interest rate environment where almost every cash acquisition immediately adds to earnings, an environment that has persisted for more than six years. Consider the immediate earnings boost provided by share repurchases paid for with non-earning cash, or with ultra-low-cost debt. Perhaps rational for executives with stock options, especially the CEO, but not necessarily reasonable for long term shareholders. In more than a few instances, the moral hazard could be an apt conclusion to draw.”

-

- Said in 2014, Reed’s words ring true today. We’ve seen massive buyback programs while market valuations remain elevated. In fact, much of the market’s return is due to these buybacks. But what’s important to note isn’t necessarily the size of the buybacks, but the financing of such purchases.

-

“Coronavirus may threaten companies’ buyback plans…Companies authorized ~$122 billion in future buybacks through February, marking nearly 50% drop from same period a year ago and representing slowest pace in three years” https://t.co/YZKU3WHEix pic.twitter.com/maoAoR4Qv0

— Trevor Noren (@trevornoren) March 11, 2020

“Your management does not believe in financial engineering or excessive leverage; we believe in building Mestek on a sound foundation. Owning manufacturing businesses entails competitive, operational, and legal risks; the probability of rewards must outweigh these risks in the decisions we make. In short, what we do must be both rational and reasonable. We are keen observers of the financial revelries of Wall Street; yet we will continue to watch from the sidelines. We wish the partygoers well, but prefer to stay sober. We prefer marathons to sprints.”

-

- Mestek’s stance on financial engineering and leverage cuts against the traditional roll-up strategy. The traditional framework involves loads of leverage with little (if any) acquirer skin in the game).

- It takes patience and a long-term mindset to sit idle while low-interest-rate environments encourage rampant and care-free deal-making. Preferring marathons to sprints looks foolish in the short-term. Especially when the gettin’s good.

“We must be prepared to pay equitable prices to founders, entrepreneurs, and business owners for their companies when they choose to retire, desire a less stressful position in their company, or simply want to financially diversify to spread their risks. We have a long and proven record of respecting successful corporate cultures, employee interests, and continuity when we have acquired businesses. We share best practices while respecting the individuality of the company. Our history of buying businesses includes honoring agreements, no haggling after due diligence. Also, mighty oak trees can grow from acorns; almost no quality business is too small to be of interest to Mestek if reasonable synergy is present.”

-

- Reed outlines three reasons owners might want to sell their business:

- Retirement

- Less stressful position with company

- Financially diversify their assets

- Reed outlines three reasons owners might want to sell their business:

As an acquirer, you want to buy from owners with these motives.

In essence, Mestek is a private equity HVAC platform business. They just happen to have shares on the OTC markets. Reed again reiterates what an acquisition looks like at Mestek. It’s a hands-off approach. Letting the business do what it does best, operate.

“Owning Mestek common stock is decidedly not for all investors. Your Directors and management take a very long term view of the business, fortunately, a view shared by the major stockholders. We are not alone; for example, Berkshire Hathaway shares an identical belief and does not pay a cash dividend to its common shareholders. Investors desiring predictable dividends are better served elsewhere.”

-

- Want to encourage a specific type of shareholder for your stock? Do what Reed did. Spell it out. Like Buffett, Reed explains the purpose of holding MCCK stock, and the type of investor that should hold MCCK stock. Dividend-hungry boomers are not welcome here!

- It seems like the best operators / CEOs have lines in the sand when it comes to shareholders. A common theme within that line-in-the-sand stance is dividend policy. The best operators hate dividends. Read The Outsiders if you don’t believe me.

Reed explains his disdain for dividends in the following paragraph …

“In addition, we believe that paying cash dividends would be shortsighted given the present U.S. tax regime. Dividends cause an immediate 30% federal and state income tax bite for most shareholders, rather than retaining one hundred cent dollars to compound in the business. Many Mestek shareholders would want to reinvest their dividends, then worth only seventy cents after tax. Not paying dividends (immediately double-taxed corporately and personally) is somewhat similar to a tax-deferred retirement account that compounds untaxed growth in value until it is ultimately utilized.”

-

- There’s nothing to add to that. I completely agree. I would much rather see management issue special, one-time dividends after a cash windfall (or something of the sort). If you can reinvest your earnings into the business at 10% or higher, what sense does it make to pay a 5-8% dividend? It doesn’t.

2015: Don’t Buy Businesses At 10x+ EBITDA, Recessions Create Opportunity

“When capital costs little or nothing, misallocation of capital is the certain result, not to mention the intense pressure put on insurance companies, banks, pension funds, 401(k) retirement accounts, retirees, and middle-class savers. Governments, ever eager to avoid structural reforms as demographics and globalization present new challenges, seek to relieve debt burdens by debasing the value of fiat money. In short, central banks are orchestrating a massive wealth transfer from savers to speculators and debtors, most notably the governments themselves which have piled up debt and made generous promises they are unable to keep.”

-

- Reed hits the nail on the head here. The first part of the quote is the most important. No-cost capital incentivizes speculation, loose valuations and exorbitant pension discount rates. It tempts business owners to buy crappy companies at high multiples. Because after all, when will we see money this cheap again?

“Double-digit EBITDA multiples, in some cases in the teens, often create excessive risks in cyclical industries while limiting potential rewards. Best-case scenarios conjured up by well-dressed investment bankers are fun to view, in some cases genuinely amusing, future earnings hockey stick and all, while keeping one’s powder dry is less fun but usually a better business decision.”

-

- When it comes to cyclical industries, mid-teens multiples create dangerous risk scenarios. There’s always the risk that you’re buying a cyclical business for double-digit EBITDA multiples at peak-earnings. What happens when the cycle turns, and your original purchase price of 12x EBITDA looks more like 18-20x normalized EBITDA? Ouch!

- If you’re interested in learning more about PE and where multiples are now, check out my Tweet thread on Bain & Company’s 2020 PE Report:

Bain Capital released their 2020 Private Equity Report yesterday.

I read it so you don’t have to.

Here’s the PDF: https://t.co/Y3h8wwLgrM

Here’s my TL;DR filled with my favorite charts, graphs and statistics …

cc: @BrentBeshore

— Brandon Beylo (@marketplunger1) March 3, 2020

“Recessions create multiple opportunities for companies with strong balance sheets including hiring great people, maintaining and enhancing R&D while competitors cut back, maintaining and enhancing sales and marketing initiatives to increase market share, better protecting dedicated employees from layoffs, and acquiring businesses and product lines at equitable prices. Mestek never welcomes recessions or other serious business challenges, but we don’t fear them either.”

-

- With a strong balance sheet, the fiscally responsible company is able to:

- Hire great people

- Maintain and enhance R&D

- Maintain and enhance sales & marketing

- Acquire businesses at equitable prices

- But before a business can do any of those things, it must have a solid financial foundation. High leverage, large interest payments and shrinking cash balances reduce a company’s ability to capture market share during recessions.

- With a strong balance sheet, the fiscally responsible company is able to:

“We try to always think like a big small business, rather than a small big business. We hate office politics and bureaucracy with a passion. We have a flat organizational structure. Whoever has the best idea wins, no matter if he or she is the most junior person in the meeting. We admit our mistakes early and often, trying to prevent our colleagues from making similar mistakes. We remember leaner times when money and credit were scarce. We don’t pretend to be big-time executives; most of us came up through the ranks intimately involved in the details of operations.”

-

- If you didn’t know where I pulled the quote from, you probably think it was Ray Dalio. I want to stress how important this framework is if you want to build a successful company. There’s no coincidence Mestek’s generated incredible returns due to their idea meritocracy framework.

- Mestek sounds like a great place to work. From the most junior position to senior executives. You have a voice, and your opinion matters. No egos, no loud-mouths. Rather a group of people dedicated to one common goal, maximizing the intrinsic value of their company.

Letters from 2016 – 2018

2016: Mistakes of Omission & Commission, Ownership and Taking RIsks

“I’ll never forgive myself for not buying a company we looked at several years ago. One of its two product lines was an ideal fit with Mestek; and the other product line was a straightforward business which we were capable of managing effectively. We were the preferred buyer in this non-auction opportunity. Why did we not rapidly close on this potential acquisition, you might ask?

Aside from general stupidity, a relatively small valuation difference and concern over a contingent liability clouded our thinking, assuming you allow me to use the word thinking so loosely. A painful lesson learned, the hard way as usual, Warren Buffet would not have made this mistake. Business is a fascinating blend of potential sins of both commission and omission. At Mestek, we don’t discriminate; we have substantial experience committing both types.”

-

- This quote ranks up there as one of my favorites in all the letters. Reed’s honesty and ruthless self-criticism is both refreshing and invigorating. As an employee or shareholder, I crave such candor from CEOs. Imagine if every CEO penned such thoughtful, sincere letters as Reed. One thing to note about this quote is why Reed passed on an unforgettable investment. His reason? A relatively small valuation difference and concern over a contingent liability. This quote reminds me of Buffett’s acquisition of See’s Candy.

“2016 was a disappointing year for Mestek. Revenues declined 4.7% excluding non-core divestitures completed in 2015; and earnings declined almost 11% to $2.14 per share. I could easily cite excuses for this result; but shareholders would be better served if instead I looked in the mirror.”

-

- I don’t have much to add to this quote except that I love the ownership and accountability. It’s striking how often CEOs are quick to blame exogenous factors for underperformance. Yet in the same breath douse themselves in praise when things go well due to factors they can’t control.

“Some failure is integral to well-run businesses. Blaming individuals for taking reasonable risks is counterproductive; learning from them is imperative. Mistakes are the best learning opportunities. What I ask of our executives is to not take large risks without talking to me; that way I can take the blame if things go wrong.”

-

- There are two things I love about this quote. First, Reed notes the importance of risk-taking in business (especially in R&D). If you want to stay a market leader, you need to innovate faster than your competition. Second, I love his stance on large risks. He isn’t against them. Rather, he wants his managers to let him know beforehand so that if things go wrong he can take the blame. How cool is that from a CEO?

2017: Innovation in Boring Businesses, Creating a Home For Family-Owned Businesses

“All things being relatively equal, the company with the best new products is likely to win. Great new products are the lifeblood of most manufacturing companies, including Mestek.”

-

- When we think of innovation and new products, we don’t jump to HVAC and boiler manufacturers. Yet these industries — like high-tech software companies — thrive on product innovation and differentiation. A great book on this topic is Hidden Champions. Many of the world’s best (and unknown) companies focus primarily on their R&D efforts. It keeps them one step ahead of their competition.

- There’s also positive flywheel effects with increased R&D spend. If you reach that critical mass (I.e., market leader), it allows you to spend more on R&D (in total dollar amount) than your competition. This reinforces your market dominance, allowing you to spend more than your competition … etcetera, etcetera.

“An acquired business becomes part of the family, able to draw on the knowledge and resources of other family members while retaining almost complete autonomy to operate their business. The managers of acquired companies are given a mostly free hand while developing new skills and lifetime friends within the family. Successful managers are well-rewarded financially; yet maximizing profit is not our patron saint.“

-

- For each new deal Mestek widens their resources, deepens their knowledge base, and increases appeal to family-owned businesses. Even better, new managers are welcomed by other business leaders within their related industries. These serve as competitive advantages to the incoming firm. They have decades of experience to draw from within Mestek. All they have to do is ask. Yet at the same time, they’re given near 100% autonomy over their day-to-day operations. It’s a win-win-win.

2018: Builders, Multi-Iteration Games and Buffettology

“We almost never physically move the company; and in the rare case we do, we explain our intentions early in the discussions prior to any transaction. Post acquisition, local managers have access to capital, and to Mestek people resources including manufacturing services such as machinery, tooling, plant layout, compliance advice and assistance, in addition to legal and HR expertise, purchasing advantages, and sales and marketing potential synergies. Also, perhaps most important, and unlike many other potential acquirers, Mestek plans to own the business forever, offering peace of mind to career employees. We are business builders, not business buyers and sellers or fair-weather owners.”

-

- Reed sounds like a broken record, but that’s a good thing. As you’ve read through ten years of letters, you’ve pulled at one string: business builders. Each letter wove together the Mestek culture. The culture of buying businesses with no intentions on selling them. The culture of building, not making a quick buck on a flip.

- Reed created Mestek as a turn-key solution for family-owned HVAC, plumbing and related businesses. Access to precious capital (both physical and human), resources and a diverse base of other family-run businesses is quite the attraction.

“Mestek has pursued this strategy because the market niche is fragmented without dominant competitors, unlike several current Mestek market niches. A complicated and fragmented market segment usually signals a profitable growth opportunity for businesses with leading products and solutions.”

-

- Many boring, blue-collar industries are ripe for consolidation. What industry will spawn the next Mestek? Who knows. What I do know is that a strategy like Mestek can work. We see the profitable results of such a strategy through Reed’s letters.

“Unusually demanding customers who view long term partnerships as predominantly about price can be more of a problem than an opportunity. Mestek is focused on selling value added engineered equipment and services to long term customer partners, and making a reasonable profit, not profitless growth. The transaction price is important, but not the be all and end all.”

-

- This quote has myriad applications for investment fund managers. When I ask fund managers, “what is the most important thing when starting a fund?” I get an (almost) unified answer: choosing the right LPs. Who you do business with (I.e., your partners) has a tremendous impact.

- Business partnerships are more than fair prices. They’re about equitable transactions and creating win-wins for both parties. Reed demonstrates the strain that comes with choosing bad business partners. Not only that, choosing partners whose sole mission in the partnership is to extract the lowest price for a service they need.

- Business, like most things in life, is a multi-iteration game. If you know you’re going to see the person (or business) again in the future, you change how you act (or respond) in the present. Ideally, you want to create win-win scenarios. You want to play the “game” in a way that guarantees future iterations of the game. This is especially true if you’re playing in a non-sum zero environment (like business partnerships).

- Why is this so important? Let’s roll with the game analogy. If your goal is to win at all costs in one game, you’ll do whatever it takes. You’ll cheat, cut corners, all that nasty stuff. But what if the goal isn’t to win at that one game, but rather to play the highest number of equitable games as you can? Notice how that changes things. In that environment, you’re not playing to win at all costs. You’re playing for longevity. You’re trying to make the game fair and equitable so your opponent (or partner) wants to play again.

“As fellow shareholders, you are my partners, which always should be evidenced by deeds rather than simply words. As the majority shareholder, I have the ethical responsibility of putting your interests equal to mine, if not ahead of mine since the value of your investment depends on my ethics and judgement. Therefore, it is essential that you are offered opportunities for liquidity at an equitable price given the very low trading volume of Mestek common stock, and the fact that no regular dividends are paid. As a student of Warren Buffet, I have resisted the payment of divi dends since it is a taxable event which destroys a portion of our combined wealth and drains our capacity for acquisitions.“

-

- I find it fitting to end on this quote. Reed, as you’ve read through the years, is a student of Buffett. Value investing bleeds through the ink in his pen when writing each annual letter. Put simply, Reed wants to buy great businesses at equitable prices, then never sell. The strategy really is that simple. Implementing it on the other hand, a whirl-wind of difficulty.

Concluding Thoughts

Through each letter, Reed wove together a story, a vision for how one should run a company. Not everyone will agree with Reed’s choices, business ethics or management culture. And that’s okay. But what you can agree on is that it worked. Since taking the helm of CEO in 2013, Reed grew MCCK’s stock price from $13/share to over $27. He’s doing something right. I wish him the best of luck over the next seven years!

_______________________________________________