Bet Sizes

Leitner is a big fan of using the Kelly criterion to size his positions. The Kelly criterion calculates the max amount you can bet on your edge without going broke from a bad run.

- Knowing the Kelly bet size is important to prevent yourself from turning a positive EV bet into a negative one through the use of too much leverage.

- Always err on the side of caution. Be conservative instead of aggressive.

- You can go broke being over-aggressive.

- You can’t go broke being over-conservative.

- The max amount Leitner has ever bet is half the Kelly number. Since we’ll never know the true probabilities of a trade, it’s rare to bet more than half the Kelly bet.

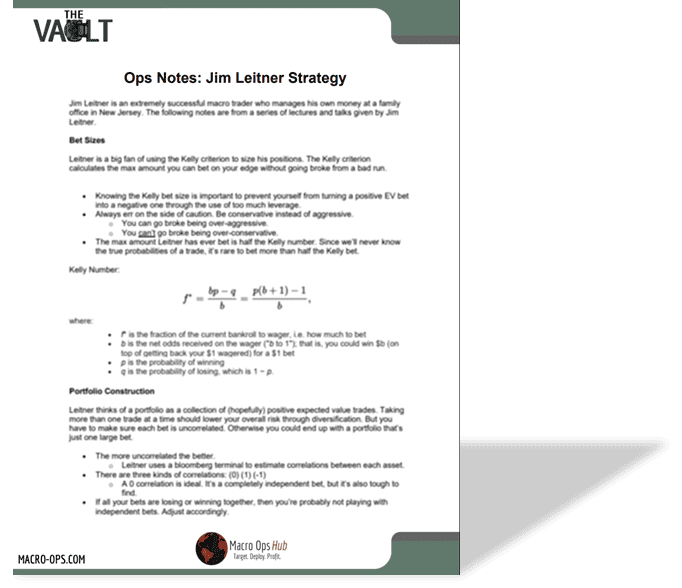

Kelly Number:

- The more uncorrelated the better.

- Leitner uses a bloomberg terminal to estimate correlations between each asset.

- There are three kinds of correlations: (0) (1) (-1)

- A 0 correlation is ideal. It’s a completely independent bet, but it’s also tough to find.

- If all your bets are losing or winning together, then you’re probably not playing with independent bets. Adjust accordingly.

Leitner likes to have at least 10 bets on his book. He takes half the optimal bet size from the Kelly criterion above and divides it by 10 to get portfolio position sizes.

Example:

The Kelly bet says to bet 30% of your money. You use half of that for safety, so now it’s down to 15%. Divide that 15% by 10 to get total portfolio level risk of 1.5% per trade.

For more on how Jim Leitner finds and manages his trades, along with his actual trade examples, enter your email below. You’ll receive our full notes on Jim Leitner’s investment strategy.: