Alex here with your latest Friday Macro Musings…

Latest Articles/Podcasts/Videos —

A Monday Dozen — Alex’s latest macro chart storm! Complete with the 12 most interesting macro charts out there plus commentary.

Podcast: The Return of Vol Trader Darrin Johnson — Darrin, a volatility/option specialist and fellow MO Collective member has returned back to the podcast to talk about how to approach the market as an independent trader.

Articles I’m reading —

I’ve got a handful of great reads for you this week, from horse handicapping to earnings deep dives to the workings of Kepler’s mind. Let’s dive in.

Our friend Kean Chan @keanferdy shared this great piece from Albert Bridge Capital which includes a chapter from the book Bet with the Beset: Expert Strategies from America’s Leading Handicappers. We like to write a lot about horse betting and other forms of skilled gambling, such as poker because there are a number of vitally important mental models that can be carried over to the game of markets. Here’s an excerpt from the piece which shares one of these models (here’s the link).

The point of this exercise is to illustrate that even a horse with a very high likelihood of winning can be either a very good or a very bad bet, and the difference between the two is determined by only one thing: the odds. A horseplayer cannot remind himself of this simple truth too often, and it can be reduced to the following equation:

Value = Probability x Price

…If every horseplayer but you were a certifiable idiot, betting at random on names and colors, you would win every day. Conversely, if the only people betting into the pool were the small number of professionals who make a living this way, your chances for long-term victory would be slim.

Either way, what would make you a loser or a winner would not be a change in the number of winners you bet, but solely the odds that these horses would return. To put this another way: Your opportunity for profit at the racetrack consists entirely of mistakes that your competition makes in assessing each horse’s probability of winning. In that first happy scenario, where the escaped lunatics are betting at random, you would win because you would bet on high-probability horses at fat odds. Every horse in a seven-horse field would be 5-1 (after takeout) and you would just bet on those with a better than 20% chance of winning. Playing purely against the pros, every horse would be bet in accordance with his true chances, and takeout would reduce each return below an acceptable price. You would be taking the worst of it every time.

Expected value or EV is the name of the game. Know your odds and look to exploit other’s errors.

Kuppy put out a short but important read this past week on how index rebalancing creates opportunities. The gist of it is that indexes, like the Rusell small-cap, are the dumbest money out there. They are forced buyers and sellers, who buy more of what’s gone up and sell what’s gone down and do so on a fixed and completely telegraphed schedule. It’s not hard to see how this produces opportunity for those who are aware of the mechanics (again, exploit the errors of others).

Here’s the link and a cut from the piece.

The Russell indexes all re-balanced on Friday. Starting early in the second quarter, you had a pretty good idea of what they needed to sell. These stocks started collapsing as arbs pressed their shorts and longs stepped away. Who would buy before the index was finished selling? Look at some of the charts below—it’s just gruesome. I’m not saying that some of these businesses aren’t challenged, but they didn’t all get dramatically worse sometime in April. Index funds may have worked fine when the index owned a few percent of the company. Now the index fund is the largest shareholder and cannot enter or exit without wrecking the chart. It’s like the good old days of clean-up prints. Even worse, they tell you exactly how to make money off them. The pension fund I traded against may have been run by the coked-up son of the union boss, but he still knew enough to keep his mouth shut about the trades he was executing. Not the Russell, I’ve had the list for weeks. Are they asking you to front-run them?

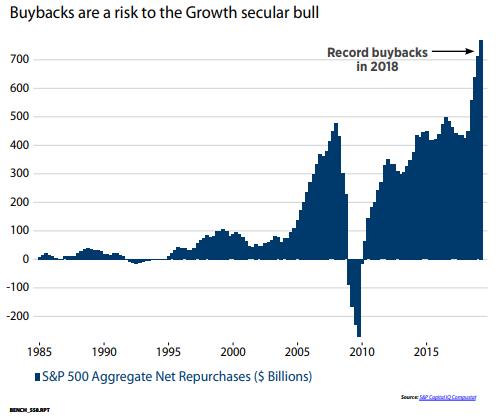

Give this recent Ned Davis Research piece titled “Will Value ever outperform again?” a read. There’s a ton of interesting tidbits in there on what macro drivers have created the current growth vs. value performance gap, what conditions are needed to flip this trend, and how this relative performance compares to past cycles. Here’s the link, two charts, and an excerpt.

Stock repurchases are another means of returning capital. By reducing the number of shares outstanding, the remaining shares own a bigger stake in the business. At $250 billion in 2018, Technology was by far the biggest share repurchaser in the S&P 500.

The combination of dividend yield and net repurchase yield is the net payout yield. Technology’s net payout yield is nearly 6%. As long as Technology companies are committed to returning capital to shareholders, they should be able to find an investor base. The risk to Tech, and in turn Growth, is if buybacks disappear.

The anonymous fintwitter @Jesse_Livermore teamed up with OSAM on another beast of a research paper. It’s titled “The Earnings Mirage: Why Corporate Profits are Overstated and What It Means for Investors”. I’m still digesting this one and plan on putting out some notes on it in the coming days. Here’s the link.

Finally, here’s KKR’s latest macro outlook (link here). Lots of great charts in there.

Charts I’m looking at—

Here are two charts that caught my eye this week.

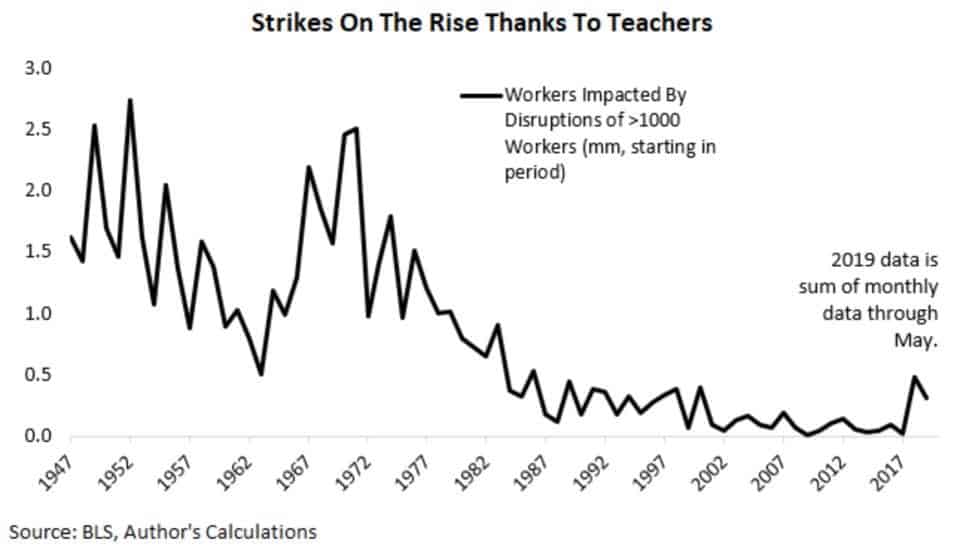

The first one is from that NDR piece and it shows the aggregate net repurchases of shares in the S&P 500, which hit a new record last year. And the second is from Business Insider and shows that after decades of dormancy, labor strikes are on the rise (here’s the link to the article).

Podcast I’m listening to —

I should just name this section “The latest Invest Like the Best Podcast I’m listening to” since the podcast is in here nearly every week. It’s not that I don’t listen to other podcasts, I do. It’s just that Patrick O’Shaughnessy is playing the podcast game at a whole other level. His last two episodes being prime examples.

His episode with @Jesse_Livermore (link here) last week was killer. I especially enjoyed his dissection and cost-benefit analysis of the three subcategories of the analytical process: intuitive, analytical, and statistical inference. It both scares me and motivates me that there are people as smart as him playing this game.

And then this week’s chat with VC Bill Gurley is just an absolute master class on tech business models, network effects, and a million other things. For those of you who don’t know of Gurley, he’s the Stan Druckenmiller of the VC space 🐐. Here’s the link.

Book I’m reading —

My book reading has slowed over the past two weeks. I’ve found myself reading more long-form blog posts and journal papers instead. I’m hoping to catch up on some new books that have recently arrived over the holiday weekend.

But, I have made some progress on Range by David Epstein; I’m roughly ⅔ of the way through and highly recommend picking up a copy. If you enjoyed Colvin’s Talent is Overrated (Range refutes much of its core thesis) and Newport’s Deep Work, then you’ll love Range. Epstein is a research machine as well as a lucid story-teller, the combination of which make for a fast and engaging read. You learn a lot about how we learn in this book.

Here’s an excerpt:

In an age when alchemy was still a common approach to natural phenomena, Kepler filled the universe with invisible forces acting all around us, and helped usher in the Scientific Revolution. His fastidious documentation of every meandering path his brain blazed is one of the great records of a mind undergoing creative transformation. It is a truism to say that Kepler thought outside the box.

But what he really did, whenever he was stuck, was to think entirely outside the domain. He left a brightly lit trail of his favorite tools for doing that, the ones that allowed him to cast outside eyes upon wisdom his peers simply accepted. “I especially love analogies,” he wrote, “my most faithful masters, acquainted with all the secrets of nature. . . . One should make great use of them.”

And if you’d like to read a bullet-pointed summary of the books main points then check out this site (link here), which has an awesome library of really detailed book notes.

Quote I’m pondering —

‘It is only half an hour’– ‘It is only an afternoon’– ‘It is only an evening,’ people say to me over and over again; but they don’t know that it is impossible to command one’s self sometimes to any stipulated and set disposal of five minutes — or that the mere consciousness of an engagement will sometime worry a whole day… Whoever is devoted to an art must be content to deliver himself wholly up to it, and to find his recompense in it. I am grieved if you suspect me of not wanting to see you, but I can’t help it; I must go in my way whether or no. ~ Charles Dickens, rejecting an invitation from a friend (h/t @paulg)

If you’re not already, be sure to follow me on Twitter: @MacroOps. I post my mindless drivel there daily.

Have a great weekend.