French elections are over.

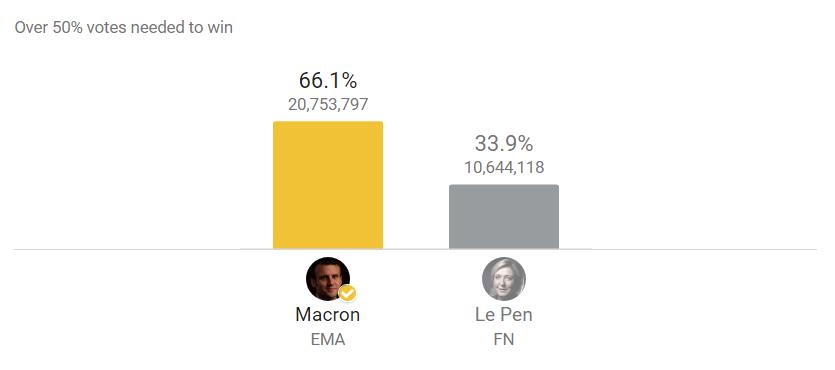

The Populist hydra has been slain (for now) and the world has taken a step back from a repeat of pre-WW2 political turmoil. Center globalist Macron bulldozed the “French Trump”, winning 66.1% of the vote.

Macron did very well among the rich and educated white collar demographic. Le Pen on the other hand attracted the blue collar, less “sophisticated” rural working class.

In essence, the vote was a battle between the “haves” and “have nots”. If you’re doing well in life, you don’t want Le Pen rocking the boat. But if you’re out of work and struggling, then you want someone who can overturn the established regime.

This is the exact dynamic we saw with Trump. The “haves” wanted the stability of Hillary. The “have nots” wanted Trump to shake things up and make factory jobs great again. In America’s case, there were a lot more “have nots” than what people thought — hence the Trump upset.

So what happened in France? Why wasn’t Le Pen able to do the same?

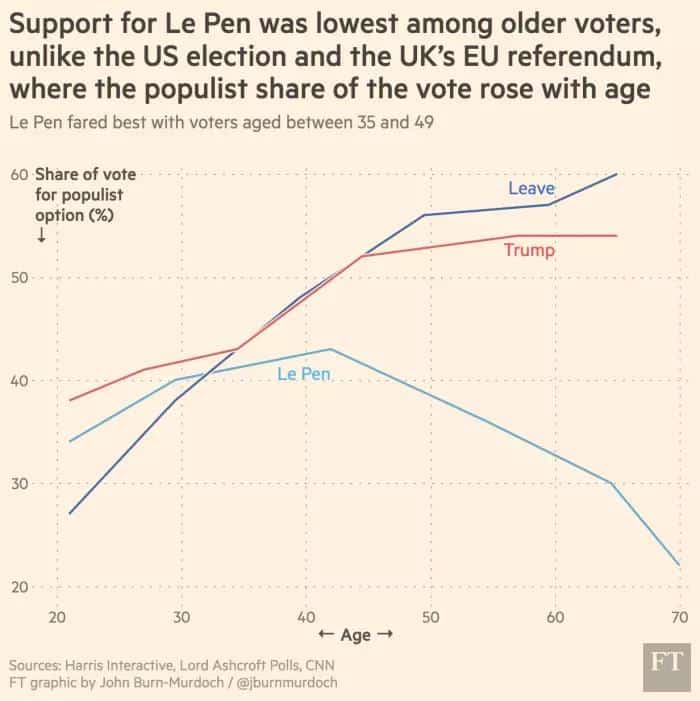

It’s because she didn’t persuade the old folk.

Both the Brexit and Trump events were heavily supported by older demographics. The older you were, the more likely you were to vote for the populist option.

But this wasn’t the case in French elections.

Le Pen supporters actually topped out around 40 years of age and then rapidly tailed off. Only passionate young people, still jockeying for position in the work force, wanted to upset the apple cart. The old folks didn’t want to live out their golden years in the midst of an EU breakup, with a currency change to boot.

Despite the bad beat, Le Pen actually took it pretty well. She was caught dancing away at a nightclub on the night of her defeat in classic French “C’est la vie” fashion.

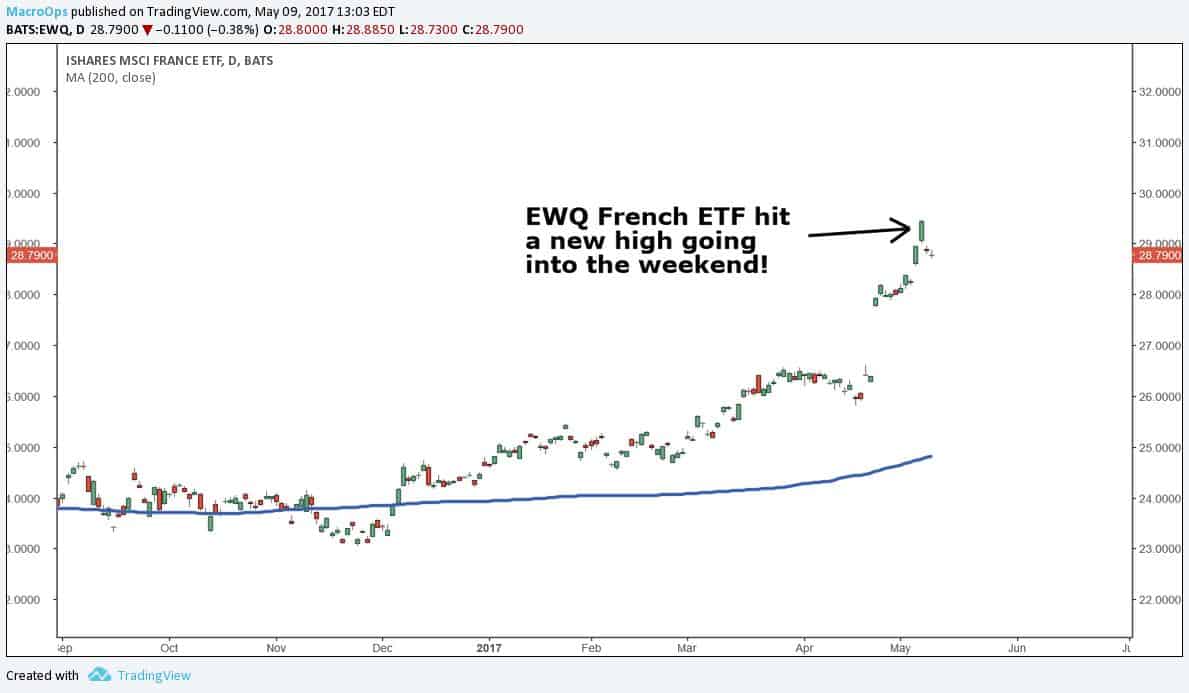

Anyone paying attention to the markets knew what was coming. On the Friday before elections, investors were so confident in Macron, that they pushed French equities to new highs for the year.

Our team still covered our downside risk with EURUSD option spreads just in case of a surprise. A fluke upset would have decimated the risk-on holdings we’ve been nurturing since earlier this year.

To make money on this theme you would’ve had to be long equities well before the 2nd round of elections. In early April the markets were still scared of a Le Pen win. You could see this through the expensive options and stagnant equities. The crowd wasn’t privy to the coming retrace in populist sentiment.

But the Macro Ops team was. We bet on a likely Le Pen loss well before the trade became consensus.

Since the beginning of April, we’ve been pounding the table about how the populism cycle had reached a short-term top.

Politics, like price action, doesn’t travel in a straight line. It moves in waves. Large impulse moves higher are followed by corrections to the long-term trend. Then, once doubters have been shaken out, the trend resumes again, with another impulse move higher.

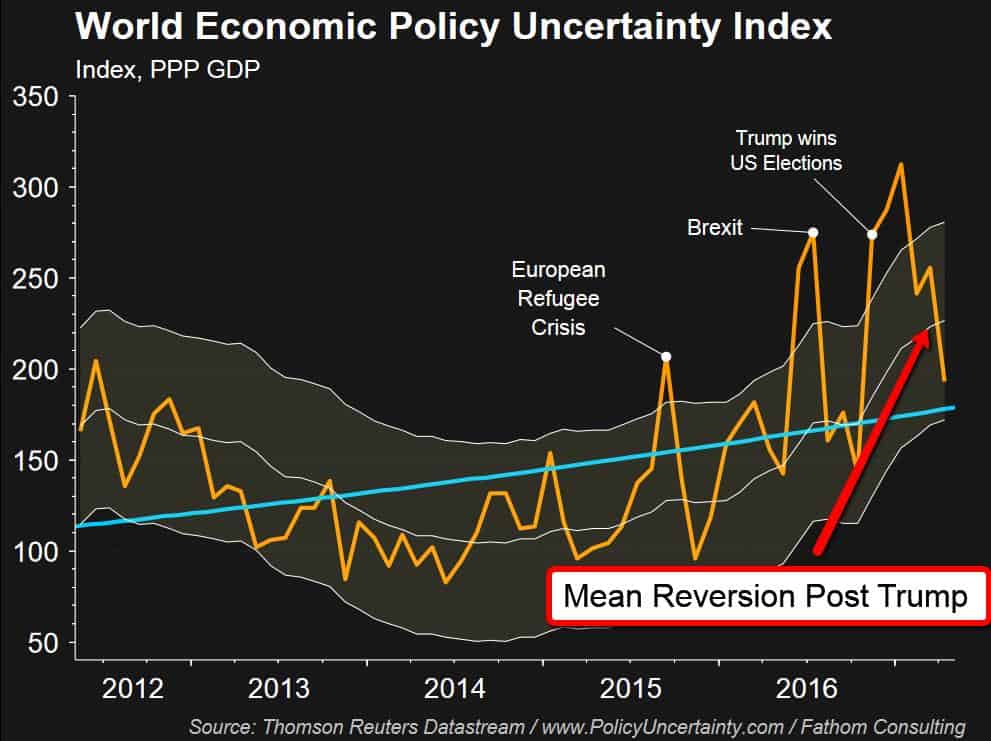

Our favorite chart of 2017, the World Economic Policy Uncertainty Index, made our analysis easy. It became clear that anti-establishment sentiment was overstretched post-Trump. We were due for some mean reversion.

This was a major reason why we called for a Le Pen defeat. Beggar-thy-neighbor politics had moved too far too fast.

And like clockwork, the index continued to revert back to its long-term trend line on the back of a Macron win.

Going forward we can finally take a breather from politics (thank god). German elections should be a non-event and Italy’s election isn’t until next year.

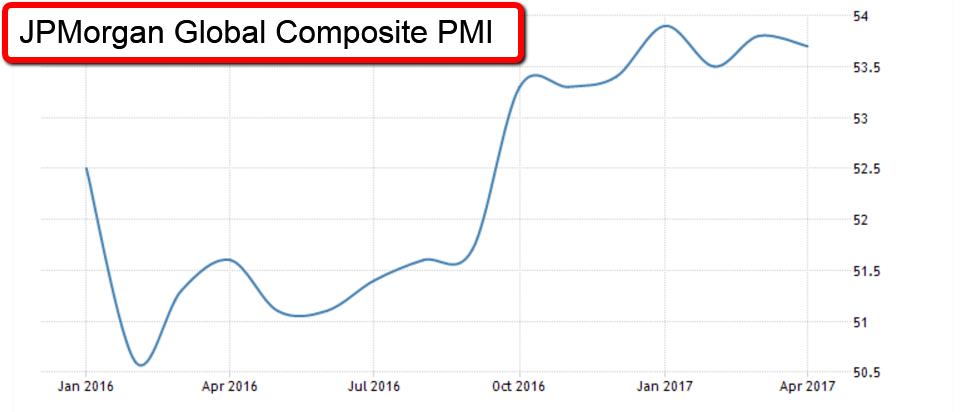

Now that political risk has subsided, there’s not much data pointing to a reversal in trend. It’s not just Europe that’s strong, econ data is picking up around the globe.

Since mid-2016, global PMI numbers have rapidly improved and continue to hold at expansionary levels.

And Citibank’s macro risk index is back near lows.

Notice the last time the chart was down to these levels — the end of 2009, the end of 2012, and now. All these periods were followed by major market rallies

The classic “risk-off” trades are all in the dumpster too. Gold looks weak. It’s stuck trading below its down-sloping 200-day MA.

And the rebound in bonds has proven to be short-lived as well.

For now, we’ll keep to the long side of markets while enjoying a respite from politics.

“It’s a bull market, you know.”