Alex here with this week’s Macro Musings.

As always, if you come across something cool during the week, shoot me an email at alex@macro-ops.com and I’ll share it with the group.

Recent Articles/Videos —

The Gerschenkron Growth Model – Alex explains how China’s reckless growth strategy will end just like the busted up economies of the Soviet Union and Japan.

Bullish 3D Printing — The 3D printing space is an undervalued goldmine right now.

Simple Trading — Comb through your investing process and take out the steps that aren’t adding to your bottom line.

Articles I’m reading —

I came across some good articles/papers this week. It wasn’t easy picking just a few to share, but here’s my three favorite must-reads of the week.

First, Michael Mauboussin put out a great paper on the benefits and limitations of certain valuation multiples with the exciting title, What Does an EV/EBITDA Multiple Mean?

He touches on many important points in the piece, as well as dispel some all-too popular misconceptions on just what various valuation multiples say about a business exactly. Read the paper in full, it’s worth your time. Here’s the link and an extract (emphasis by me).

In their pathbreaking paper on valuation, Miller and Modigliani provide a formula that is core to understanding value. They say: The value of the firm = steady-state value + future value creation. Over the last 60 years, roughly two-thirds of the value of the S&P 500 price was attributable to steady-state value and the other one-third to future value creation. Both pieces are important. Here’s an intuitive way to think about it. Say you owned 10 mature and profitable restaurants. Assuming the current profits persist for the foreseeable future, those restaurants are the foundation for the steady-state value. Now consider the possibility of opening new restaurants that are worth more than they cost to build. That is future value creation.

The important point is that future value creation is based on three elements: finding projects that generate a positive spread between the return on invested capital (ROIC) and the weighted average cost of capital (WACC), how much you can invest in those projects, and how long you can find those projects in a competitive world. Note that the latter elements, how much and how long, only create value if there is a positive spread between ROIC and WACC. If the spread is zero, the second term on the right side of the equation collapses to zero. Indeed, the second term can be negative if the investments fail to earn the cost of capital. This illuminates the critical lesson that you have to start with the spread between ROIC and WACC. Calculating ROIC and WACC correctly is a prerequisite to doing this analysis appropriately. Growth creates a lot of value only when the spread is positive and large, has no effect when the spread is zero, and destroys value when the spread is negative. Too many executives and investors focus on growth without recognizing the need for a positive spread in order to create value.

Second, Srinivas Thiruvadanthai, who is one of my favorite follows on twitter at @teasri, authored a paper titled Current Account Balances, Debt Buildup, and Instability. If you’re not familiar with his work or the framework he and his team at the Jerome Levy Forecasting Center use to analyze the world, I suggest visiting this site and reading the Profits Perspective and then go through some of their research papers.

Anyways, this is a great paper on the role current account imbalances play in macro leveraging and ultimately, financial instability. The paper includes many important concepts for understanding the broader structural problems facing emerging markets, today. Here’s the link and an excerpt.

Yet, as I argue in this paper, the mainstream view of current account imbalances ignores, among other things, their critical role in increasing financial fragility, both on the external and the domestic fronts. While, in theory, current account deficits could be financed substantially through equity investments, in practice, they tend to be disproportionately financed by debt. Thus, growing current account deficits lead to rising external debt. An even lesser known fact is that widening current account deficits lead to rising domestic leverage, especially in the private sector, with serious consequences for financial stability and future economic growth. The free-market resolutions of these imbalances do not happen smoothly via exchange rates but by severe economic contraction and prolonged economic weakness, with depressive effects on the rest of the world.

And finally, Daniel Want and team over at Prerequisite Capital shared some of their research this week. Daniel is a super smart guy and I’m a big fan of the way he approaches markets. Give this report a read where he shares his framework for analyzing currencies — there’s also a ton of great quotes in the piece. Here’s a section and the link.

When it comes to analysing the complex environment, or more specifically the ‘underlying conditions’ of the market in question – it is essential that we focus on generating competitive insight (a variant perception that is anchored in a high degree of reality).

Another principle (that bears repeating again) when studying and analysing the world, is that it helps to be able to glimpse reality through many different, unrelated ‘lenses’ (or perspectives). If you can look at reality through a multitude of independent but robust perspectives and you find yourself glimpsing the same underlying reality, then your conviction is able to grow around what you are seeing and your confidence to act grows. Hence, we tend to want to apply a multitude of unrelated tools and frameworks to our object of analysis.

Chart I’m looking at —

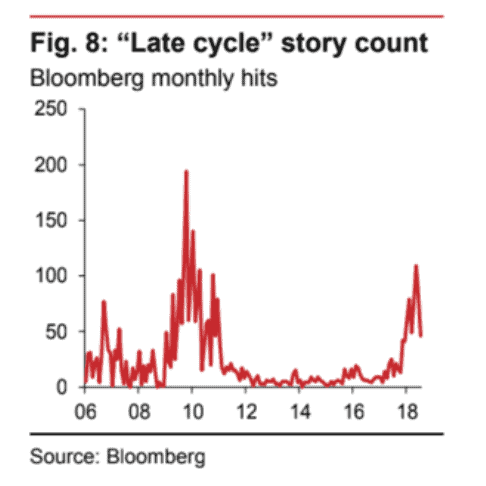

There seems to be general consensus that we’re “late in the cycle”. Dalio came out this week saying we’re in the 7th inning and we’ll see recession in 1-2 years and then Tepper appeared on CNBC saying we’re in the 8th… and the “Late cycle” story count via Bloomberg shows late cycle mentions spiking. Stating we’re “late cycle” just feels right, doesn’t it? It feels like the responsible and wise thing to say, which is why I guess everybody is saying it. But here’s the thing, markets just don’t work like that. I can’t remember any time in the history of markets where everybody agreed on something, it happened, and then we all made money.

I don’t know, I’m not as smart as Dalio or Tepper, and the argument for it being late cycle is persuasive, I guess. But I still haven’t seen any of the uber bullishness, wide scale risk taking, and most importantly, leveraging, that typifies most “late cycle” periods. So to abuse the baseball analogizing further, maybe this game is going to extra innings?

Podcast I’m listening to —

This week I listened to a great Tim Ferriss podcast with one of my favorite non-fiction writers, Doris Kearns Goodwin.

She’s the author of the Lincoln biography, Team of Rivals, as well as one of my favorite books, The Bully Pulpit.

They cover a wide range of topics in the interview: from lessons on leadership, to amazing stories about the many Presidents she’s written on and spent time with (she worked and became close friends with LBJ). Anyways, Doris has lived a fascinating life and is a talented storyteller. I highly recommend giving it a listen. Here’s the link.

Book I’m reading —

This week I’ve been reading Out of Control by Kevin Kelly (founding executive editor of Wired magazine). This is a beast of a book, nearly 500 pages with small print. I’m about halfway through it now and really enjoying it.

I don’t even know how to describe the book. The back cover says the book “chronicles the dawn of a new era in which the machines and systems that drive our economy are so complex and autonomous as to be indistinguishable from living things.” Which seems to partly describe it, but doesn’t really do it justice.

Kelly goes deep into the subject of complexity and emergent evolution; discussing everything from the communication techniques of bee swarms to metaphysics and the systemic vulnerabilities of various forms of human government.

It’s an older book (published in 94’) but not outdated. If you enjoy learning about complex systems then pick this up, you won’t be disappointed. Here’s a section.

Coevolution is a variety of learning. Stewart Brand wrote in CoEvolution Quarterly: “Ecology is a whole system, alright, but coevolution is a whole system in time. The health of it is forward — systemic self-education which feeds on constant imperfection. Ecology maintains. Coevolution learns.

Colearning might be a better term for what coevolving creatures do. Coteaching also works, for the participants in coevolution are both learning and teaching each other at the same time. (We don’t have a word for learning and teaching at the same time, but our schooling would improve if we did.)

The give and take of a coevolutionary relationship — teaching and learning at once — reminded many scientists of game playing. A simple child’s game such as “Which hand is the penny in?” takes on the recursive logic of a chameleon on a mirror as the hider goes through this open-ended routine: “I just hid the penny in my right hand, and now the guesser will think it’s in my left, so I’ll move it into my right. But she also knows that I know she knows that, so I’ll keep it in my left.”

Since the guesser goes through a similar process, the players form a system of mutual second-guessing. The riddle “What hand is the penny in?” is related to the riddle, “What color is the chameleon on a mirror?” The bottomless complexity which grows out of such simple rules intrigued John von Neumann, the mathematician who developed programmable logic for a computer in the early 1940s, and along with Wiener and Bateson launched the field of cybernetics.

Von Neumann invented a mathematical theory of games. He defined a game as a conflict of interests resolved by the accumulative choices players make while trying to anticipate each other. He called his 1944 book (coauthored by economist Oskar Morgenstern) “Theory of Games and Economic Behavior” because he perceived that economies possessed a highly coevolutionary game-like character, which he hoped to illuminate with simple game dynamics. The price of eggs, say, is determined by mutual second-guessing between seller and buyer — how much will he accept, how much does he think I will offer, how much less than what I am willing to pay should I offer? The aspect von Neumann found amazing was that this infinite regress of mutual bluffing, codeception, imitation, reflection, and “game playing” would commonly settle down to a definite price, rather than spiral on forever. Even in a stock market made of thousands of mutual second-guessing agents, the group of conflicting interests would quickly settle on a price that was fairly stable.

Trade I’m considering —

My book is pretty full when it comes to long equity trades so I’m not really looking to add anything at the moment. And the following stock is much smaller and more illiquid than what we typically buy but I found the long thesis presented by Scott Miller so intriguing that I figured I’d share it with you guys and gals.

Anyways, the company is Chicken Soup for the Soul Entertainment Inc (CSSE). And yes, it’s that Chicken Soup for the soul… I could give you the skinny on the CSSE’s bull pitch but I don’t feel I’d do it justice so I’ll just give you the link to Scott’s latest letter and you can read it there (link here).

Quote I’m pondering —

There’s nothing wrong with pricing. But it’s not valuation. Valuation is about digging through a business, understanding the business, understanding its cash flows, growth, and risk, and then trying to attach a number to a business based on its value as a business. Most people don’t do that. It’s not their job. They price companies. So the biggest mistake in valuation is mistaking pricing for valuation. ~ Aswath Damodaran

That’s it for this week’s Macro Musings.

If you’re not already, be sure to follow us on Twitter: @MacroOps and on Stocktwits: @MacroOps. I post my mindless drivel there daily.