A couple of my favorite quotes from legendary trader Bruce Kovner are:

What I am really looking for is a consensus the market is not confirming. I like to know that there are a lot of people who are going to be wrong.

As an alternative approach, one of the traders I know does very well in the stock index markets by trying to figure out how the stock market can hurt the most traders. It seems to work for him.

If you can figure out how the majority of the market is positioned and where the most consensus trades are, you can do very well by opportunistically fading the herd. This is playing the player and trading at the second level… a skill that’s vital to long term market survival.

Fading crowded trades is a great strategy, especially recently.

For example, our oil short went against near record long speculative positioning as noted in the COT report. Our long bonds trade went against speculative positioning as well and has been very profitable.

Since markets have lacked volatility and benchmark indices have gone vertical over the last few months, money managers have been desperately chasing and recklessly crowding into trades. This has resulted in a lot of one sided positioning that traders like us can continue to take advantage of.

Looking around global markets there’s one obvious trade that would make a lot of people wrong and hurt the most traders. That trade is the ole’ greenback.

Let’s look at the evidence.

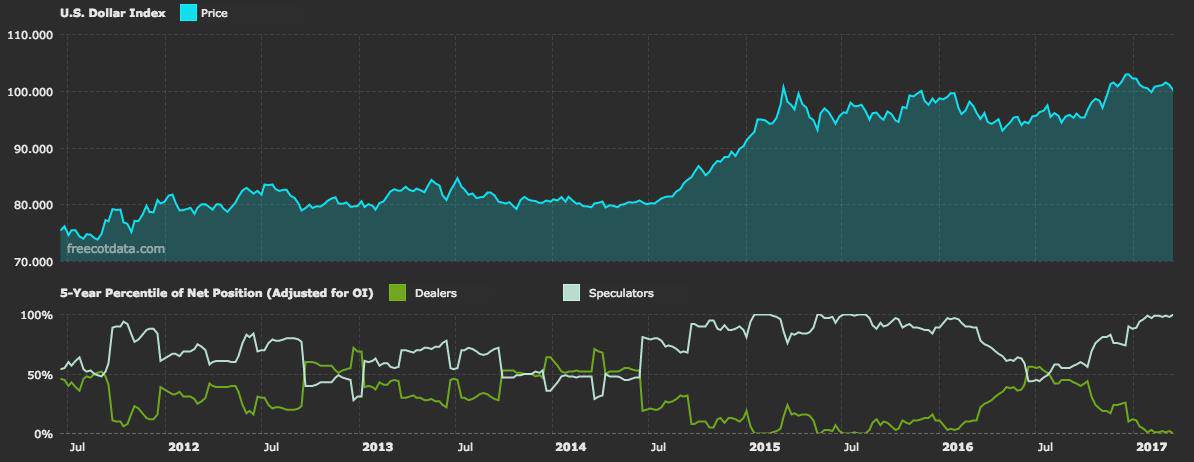

The chart below shows speculators are max long the dollar against broker dealers. This is an extreme reading. When you see COT positioning at this level of divergence, it’s almost always the dealers who win out. The market doesn’t pay a bunch of speculators so easily.

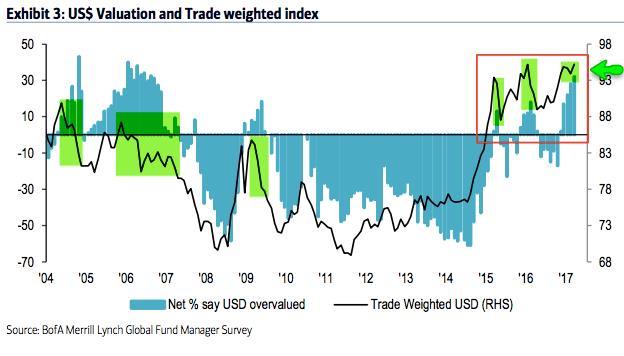

BofA’s monthly Global Fund Manager Survey was released this week. The chart below shows that a large net % of respondents are saying the dollar is overvalued. This survey has a pretty good track record of noting short-term reversal points in the dollar.

It’s been a long time since there was a large and violent forced selloff in the dollar. That means dollar longs have grown complacent and many of them are probably leveraged. When there’s been mostly one way moves in an asset for a few years, it creates a situation where positioning, leverage, and complacent beliefs are like piles of dried, kerosene-soaked kindling. They’re just waiting for a spark.

Take away talk of the border adjusted tax and combine it with other global central banks like the BOE and ECB looking to end their easing cycles, and you have the potential for a ripe and violent reversal… or a dollar bonfire if you will.

USD price action is setting up in what looks like a textbook head and shoulders pattern. We could see a break below the neckline this week.

Now we don’t think this is a major reversal in the dollar here, it’s only short-term. But it’s still very playable.

There are a number of ways to get short the dollar since it directly and indirectly affects the pricing of many other assets (ie, emerging markets, oil, gold etc).

But in order to find the optimal dollar short trade, let’s again look at market positioning — using COT data and the BofA Fund Manager Survey — to see how other players are long dollars directly or synthetically.

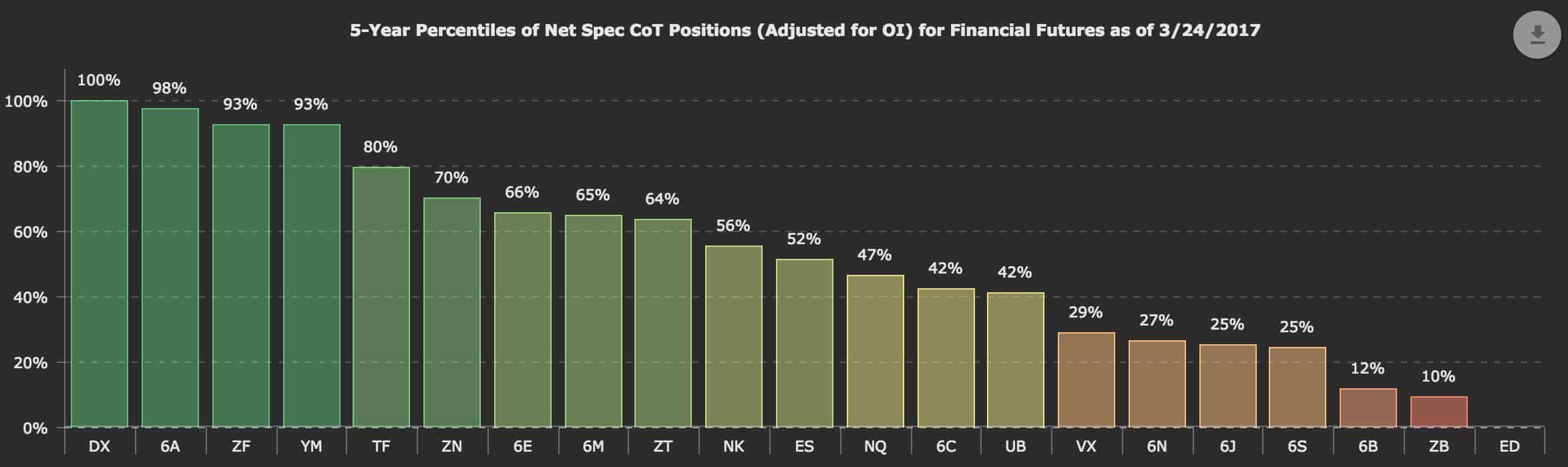

The chart below via www.freecotdata.com shows the 5-year percentiles for Net Speculator positioning. The instruments in red on the right are those that speculators are net short and vice versa for those in green on the left.

ZB, the bond futures contract we’re currently long, is essentially a synthetic dollar short position.

The 10-year yield and USD have moved in lockstep fashion over the last two years. This means that the potential for a dollar selloff looks good for our long bond positioning.

The next instrument — 6B — is the British Pound futures contract. Looking at the graph below from the Fund Manager Survey, you can see that respondents are historically net short the euro, pound, and bonds.

Like the dollar, both the euro and the pound have been forming inverse head and shoulders and are close to closing above their necklines.

We took a crack at going long the pound (FXB is the ETF alternative for the pound and FXE is the euro ETF alternative) a few months ago but closed our position for scratch as it failed to carry through. I’m willing to take another stab at it and perhaps the euro as well should we see price break those necklines.

If you’re interested in seeing exactly how we play these coming currency moves, take a trial of the Macro Ops Hub. Hub members get alerts to our exact entries, exits, and position sizes of both our model portfolios. Membership comes with a 60-day money-back guarantee. Check it out for 2 months, and if you don’t get your money’s worth, we’ll return it right away. Click here to learn more.