Everyone knows WD-40 (WDFC), that blue and yellow can with the red cap. Odds are you have some in the garage right now. It’s one of those home cure-alls that you should always keep around, like duct tape or 550 cord. WD-40 fixes squeaky doors, tight locks, and smooths furniture joints. There are over 2,000 documented use cases for the stuff.

There’s nothing fancy about the product nor the company that makes it. Yet what is remarkable is the company’s ability to compound capital over multiple decades at above-average rates of return. Since its IPO in 1973, WDFC has generated a ~13% CAGR or a 9,474% cumulative return.

The company was founded in 1953 to help prevent corrosion on the Atlas Nuclear Missile. By 1990 (20 years after its IPO), the product became a household staple in 80% of American homes.

WD-40 is the perfect company to kickstart our Investment Case Study Series. There are a few reasons why.

First, WDFC sold one product for the majority of its early public life. Such product concentration seems unimaginable today, but it proved worthwhile. Today, WD-40 isn’t a product but a noun.

Second, WD-40 is an example of the power of selling boring products in a boring industry. Nobody will compete with you if you sell a boring-enough product. And if the incumbent brand is synonymous with the commodity itself, why bother competing?

Third, WD-40 is living proof that product distribution is a massive competitive advantage.

We’ve dissected our case study into four parts:

- Part 1: Early History & Finding Product-Market-Fit

- Part 2: The John Barry Era & IPO Years

- Part 3: The Garry Ridge Era

Finally, we’ll conclude each section with actionable models investors can use to find tomorrow’s long-term compounders.

If you don’t have time and want to let your “lazy” out of the cage, here’s our three most important lessons from WD-40’s history:

- Look for products/services that are 5-10x better than any alternative.

- If a stock’s earnings rise faster than its share price, the business may still represent a good value investment.

- Industry-leading product distribution is one of the most resilient yet least discussed competitive advantages.

Do you want to know how to turn $3,500 in sales to $400M? Keep reading!

Part 1: The Early Days of WD-40

The WD-40 story starts with Norm Lawson. Lawson worked for San Diego Gas & Electric before starting his own private aviation company, Airtech, in 1928. He ran his flying school until the start of WWII. In his final corporate act, Lawson founded the Rocket Chemical Company with some work colleagues.

In the 1950s, a Naval Commander approached Lawson with a proposition. The Journal of San Diego History explains the interaction, saying (emphasis mine):

“…A naval commander, who was a friend of the Lawson family, asked Norm if he could come up with something to help the US Navy prevent corrosion from ocean salts affecting the gears on the ships. They needed a lubricant—something stable, easy to store, transport, and apply.“

Charged with an idea, Lawson set up shop above his garage to work on the “simple” formula. Lawson tried 39 different mixtures for his corrosion lubricant, but they all failed. Then, on the 40th try, Lawson struck water-displaced gold. Now you know why they call it WD-40.

Charged with an idea, Lawson set up shop above his garage to work on the “simple” formula. Lawson tried 39 different mixtures for his corrosion lubricant, but they all failed. Then, on the 40th try, Lawson struck water-displaced gold. Now you know why they call it WD-40.

Lawson turned his formula over to Rocket Chemical for marketing and distribution rights, and the rest, as they say, is history.

Here’s the fascinating part: Consumers saw myriad uses for the rust-prevention lubricant from the very beginning. Take co-founder Cy Irving’s story with local tuna seiners.

After seeing its initial success, Cy Irving (co-founder of Rocket Chemical) took the product to San Diego’s tuna fishermen. Irving unveiled the rust-preventer at Union Oil Dock, a tuna seiner service station.

Tuna fishers, like the Naval Commander, wanted a way to prevent rust on their ships. Sam Crivello owned such a vessel called Sun Europa. Crivello, interested in the rust-prevention benefits, was one of the first people to use WD-40 outside its first application.

The product worked, and Crivello became an instant fan. So much so that he bought a 50% stake in Irving/Lawson’s Rocket Chemical Company.

You can read Crivello’s product success story below (emphasis mine):

“Cy and Sam took the motor and lowered it into the saltwater, left it for a while, and then brought it back up and sprayed it with WD-40 and it started right up. Julius Zolezzi’s father John was on the dock and told Julius the story. He said the product was amazing.“

Yet, it wasn’t until 1957-1958 that WD-40 flexed its commercial muscle.

How Packaging Can Expand TAM

Norman Larsen (not Lawson) ran Rocket Chemical Company from 1957 to 1958. While not a long stint at the helm, it proved valuable. You can argue that one Larsen decision paved the way for the current brand affinity the WD-40 company enjoys today.

The decision was simple. Larsen repackaged WD-40 into the familiar aerosol can.

By repackaging the product, Larsen expanded the total addressable market.

International Expansion & Aggressive Top-line Growth

Irving resumed the role of president in 1958. By this time, the former garage project was growing like a weed. The company added 5,000sqft to its manufacturing plant, acquired 30 distributors, and expanded nationally and internationally.

The Journal of San Diego History notes that by 1960, “Rocket Chemical had expanded into Latin America, Australia, and New Zealand. Irving reported that DeHavilland Aircraft would distribute their products in Australia and New Zealand while Diseños Industriales y Productores of Mexico City were serving as distributors throughout Mexico.”

Everyone wanted the yellow and blue can with a red lid. The state of Texas, for example, requested 36,000 gallons of WD-40 after Hurricane Carla. Even the US government wanted its hands on WD-40, ordering 233,000 cans and 300 55-gallon drums.

Irving and Lawson created a product everyone needed but previously never existed. More importantly, consumers kept finding new uses for the product, explaining how the company went from $3,500 in sales to $2.13M by 1969.

The Most Important Lesson: Invest in products/services that are 5-10x better than any alternative.

WD-40 was the best product because there was nothing like it on the market.

Part 2: The John Barry Era & IPO Years

John Barry became CEO of The Rocket Chemical Company in 1969. Barry increased sales by 4,172% from $2.13M to $91M (that’s a 198% revenue CAGR) during his twenty-one-year tenure. These revenue growth figures put Barry in a league of his own. So how did he do it?

We can deconstruct Barry’s strategy into three key pillars:

- Turn A Product Into A Noun

- Invest in Advertising

- Centralize Product Control

The world’s best companies still use Barry’s four key pillars to win customers.

Turning A Product Into A Noun

Barry’s first act as CEO was to change the company name from Rocket Chemical Company to WD-40. This makes intuitive sense, as Barry described, “We don’t make rockets.”

The name change marked a fundamental transformation in the company’s history. WD-40 became more than a manufacturing company. It became a noun in the minds of 8 out of 10 Americans.

Barry understood the power of the WD-40 brand better than anyone, and a 2009 New York Times article on Barry’s life provides an excellent example (emphasis mine):

“Mr. Barry acknowledged in interviews with Forbes magazine in 1980 and 1988 that other companies, including giants like 3M and DuPont, made products that closely resembled WD-40. ‘What they don’t have,’ he said, “is the name.‘”

The company’s name is synonymous with the product it makes, like “Google” for search engines or “Peloton” for in-home exercise bikes. Here’s why that’s so powerful.

WD-40 never patented its secret formula, fearing a competitor would copy the recipe. In other words, WD-40 needed that brand-noun connection to survive (and thrive) as a company.

A bold bet, but one we’ve seen before with the LEGO company. LEGOs critical plastic block patent expired in 1978, opening the floodgates to legions of lower-priced competitors. While other companies tried recreating the famous LEGO 2×4 brick, none succeeded in overthrowing LEGO’s toy-brand dominance.

This is why brands becoming nouns is so essential. Economic theory states that rational consumers would save money and buy the cheaper, knock-off LEGOs if given a choice. But that didn’t happen.

Instead, the word “LEGOs” became synonymous with “those little plastic toy bricks,” and the rest is history.

Invest in Advertising

WD-40 had a simple capital allocation policy when Barry assumed the role of CEO. Until that point, the company made one product, and there was no need to innovate. So, all earnings went to shareholders via dividends. WD-40’s 1975 Annual Report emphasized this strategy (emphasis mine):

“We have plenty of money. We don’t need the funds for growth so we decided we’d give it back to the people who own the company.”

Under Barry’s watch, WD-40 wasn’t a manufacturing company but a marketing company. This subtle mindset shift had significant consequences. As a marketing company, WD-40 wasn’t in the business of selling widgets but selling solutions to problems.

The company made three critical decisions during this time:

- Offered thousands of free samples

- Placed product in supermarkets

- Pushed for foreign sales channels

It was all a numbers game to Barry. The more places people saw the product, the better the chance they’d buy. He explained his reasoning in a San Diego Union interview (emphasis mine):

“It is a numbers game—the more shelves we’re on, the better the chance a buyer will pick us up—whether it’s in hardware or sporting goods.”

Centralize Product Control

Barry understood the power of controlling price and distribution. Like Costco, WD-40 set its terms on pricing and distribution. For example, at one point, Sears wanted to package WD-40 under its label. Barry said no.

Another time, one big chain retailer wanted discounted wholesale pricing for its WD-40 orders. Barry again said no. This is not normal for most brands.

The Most Important Lesson: Invest in products that allow its customers to provide the benefits of application diversification.

WDFC’s 1973 Annual Report highlighted that 90% of its revenue came from one product: WD-40. But Barry explains why such product concentration didn’t matter (emphasis mine):

“Your Company is built on a single product, WD-40, yet it is actually well diversified from a marketing point of view because of the broad range of WD-40’s proven applications.“

In other words, WD-40 customers kept finding new ways to use the product. This created a “new product” feel without the company needing to create a new product.

Let’s return to our LEGOs comparison to tie the bow on this section. LEGO made a plastic brick. Its customers (read: fanatics) created the sculptures, vehicles, spaceships, and working robots we know today.

There’s a tremendous (yet intangible) value associated with companies that create products that spark the consumer’s never-ending ingenuity.

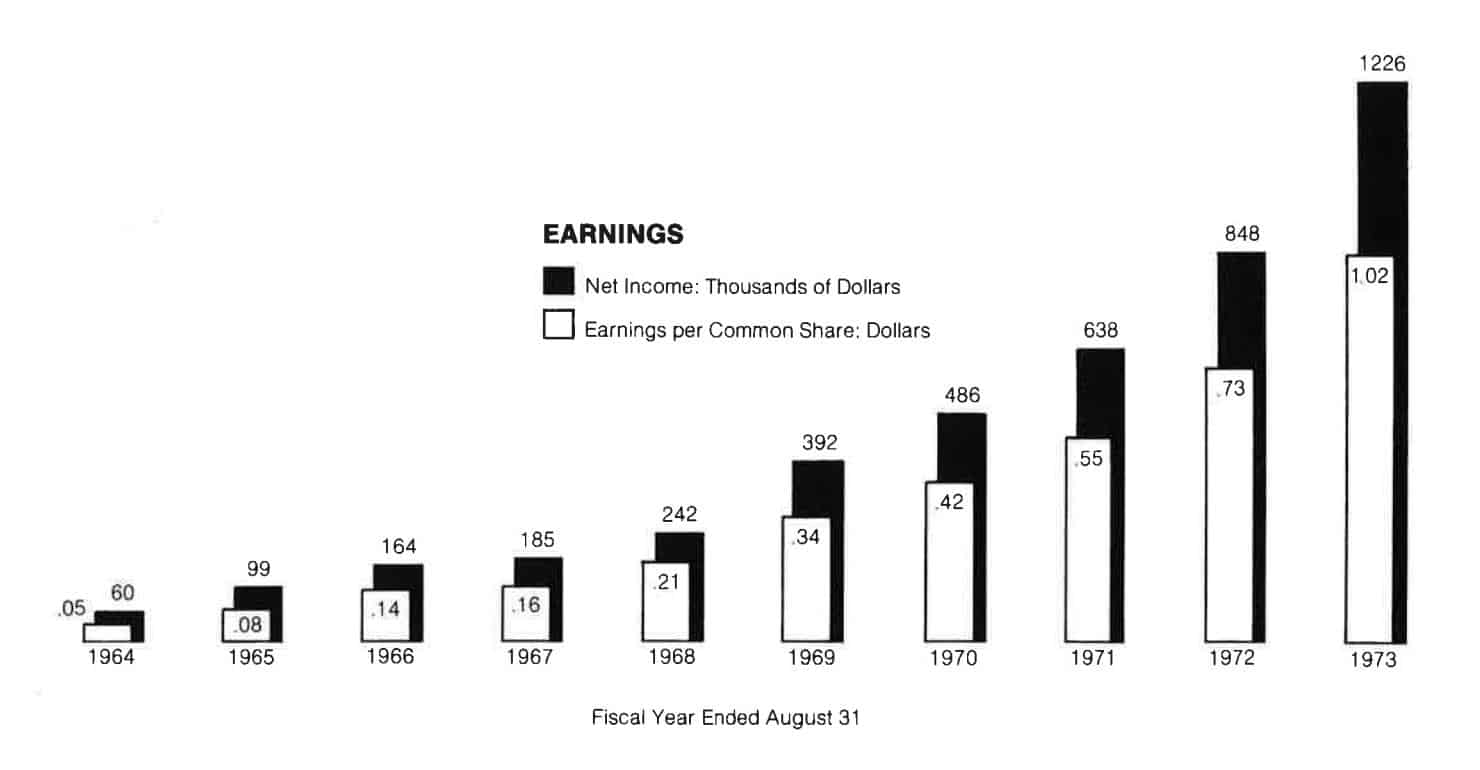

It’s this consumer-facing ingenuity that propelled WDFC from $450K in sales in 1964 to $7.3M by its IPO in 1973 while generating a 194% 10YR earnings CAGR. (see below from first 1973 Annual Report):

The IPO Years: Drawdowns, Growth & Everything In Between

WD-40 was a private company until 1973 when it IPO’d on the NYSE (fact check). Given the tremendous product success, customer satisfaction, and brand awareness we’ve documented, you’d assume an IPO would equal share price appreciation. Not quite.

My favorite part about these case studies is reviewing the initial years after a company’s IPO. We get a window into what investors thought at the time, why they invested, and why they passed.

Its first two years as a public company were rough. The stock price fell 70% from January 1973 to December 1974. WDFC didn’t break its all-time highs until 1978 — five years after its IPO. The funny part is you wouldn’t know it had you focused only on fundamental business performance. From 1973 to 1979, WDFC nearly 5x’d sales, growing from $7.3M to $35M while simultaneously increasing EPS from $0.51 to $2.22.

By the end of 1979, WDFC’s stock had risen 130%. Most investors in 1979 would’ve taken profits or trimmed their position. After all, you can’t go broke taking 130% gains. That said, there’s a vital lesson we can learn from WDFC’s early IPO years.

The Most Important Lesson: Always compare the share price growth to the core earnings growth of the underlying business.

WDFC’s share price rose 130% from its IPO to the end of 1979. Yet, at the same time, its core business earnings grew by 335% or nearly 2x as fast.

In other words, WDFC still traded ~2.2x earnings despite a 130% share price increase. That’s the power of earnings growth.

Always compare the share price growth to the core earnings growth of the underlying business.

Part 3: Expanding Products, Company Culture, & Garry Ridge

Barry resigned in 1990 with a world-beating track record. During his 17-year tenure, Barry increased WDFC’s share price by 480% or a 28% CAGR. Those are big shoes to fill.

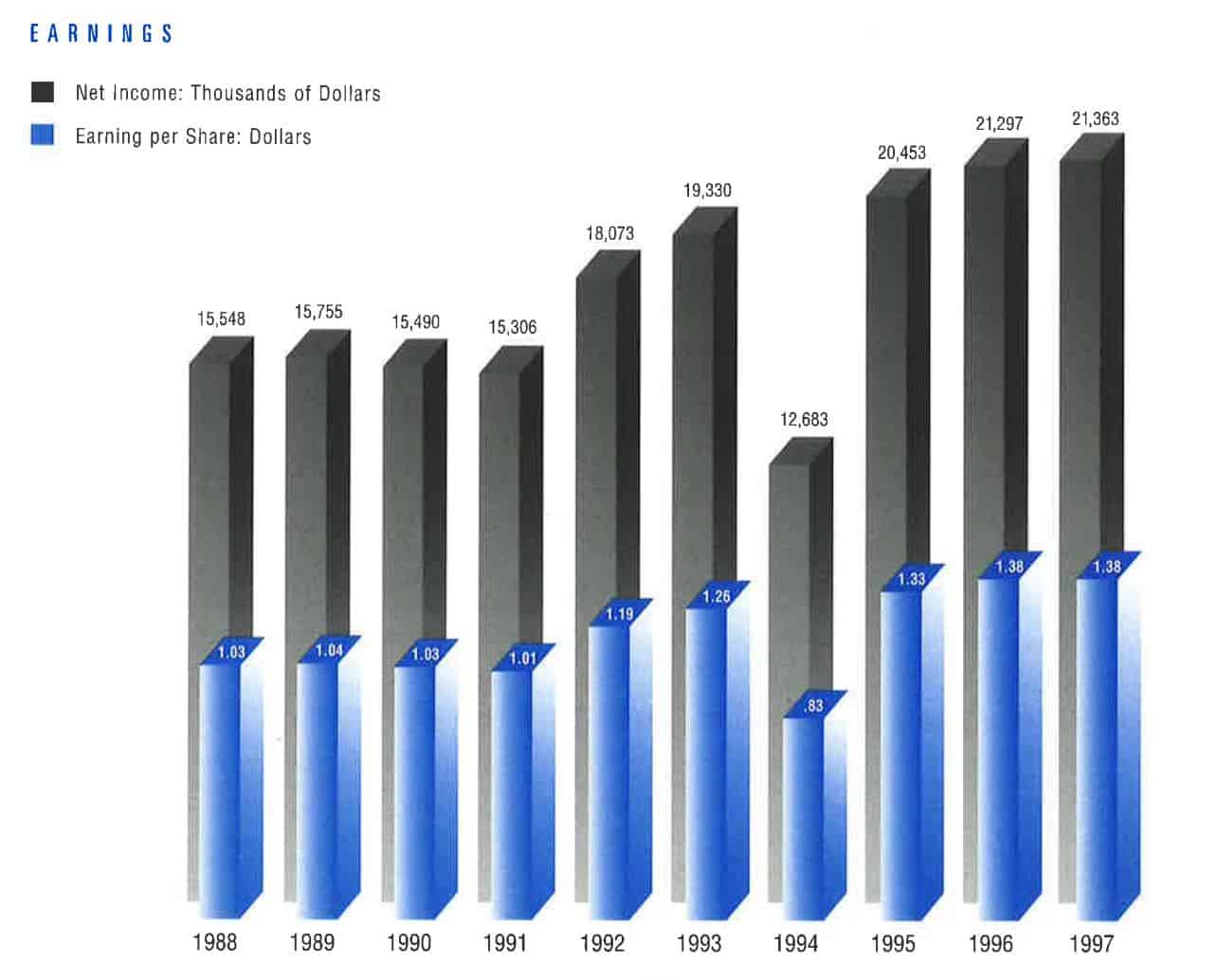

The company named Jerry Schleif its next CEO in 1990. As the new boss, Schleif did two things no other WDFC executive had done before: expand the product line and aggressively target international markets.

In 1995, Schleif expanded WD-40’s product line for the first time by adding two new brands: 3-IN-ONE Oil and T.A.L. 5. Both brands complemented WD-40’s flagship, squeak-killing lubricant. Additionally, Schleif targeted international markets and aggressively expanded WDFC’s sales efforts abroad.

The company deployed new sales force teams in France, Spain, Italy, and the Middle East. Doing so resulted in $17.5M in annual international revenue. These two decisions fundamentally shaped the WDFC company we know today.

By expanding product lines and increasing global sales, Schleif created a more robust business than before.

During his seven years as CEO, Schleif’s decisions increased sales from $91M to $137 while increasing EPS from $1.03 to $1.38. By the time Schleif retired, the company stock had returned ~127% for a ~18% 7YR CAGR.

During his seven years as CEO, Schleif’s decisions increased sales from $91M to $137 while increasing EPS from $1.03 to $1.38. By the time Schleif retired, the company stock had returned ~127% for a ~18% 7YR CAGR.

Garry Ridge took the wheel as the newest (and current) CEO of WDFC in 1998. Ridge transformed the WD-40 company in three key ways.

First, Ridge emphasized the importance of company culture and creating an ecosystem where people wanted to work and loved what they did. Second, the Australian slashed WDFC’s once-coveted dividend to make strategic acquisitions. Finally, Ridge understood the power of distribution and international expansion by opening a direct sales office in Shanghai to reach Chinese and Russian markets.

Let’s talk culture. Ridge turned WDFC from a collection of employees to one tribe. Tribal culture bleeds through every social and cultural fiber. Your favorite sports team? That’s a tribe. That stock you’ll never sell? Tribe. Tribes dictate the thoughts, actions, and memories of each member.

Ridge created a tribal family by focusing on three critical human needs:

- Purpose

- Values

- Learning Moments

The company is so serious about the tribe values that it has an entire webpage dedicated to them (see here). Employees even sign a “Maniac Pledge” that states: “I am responsible for taking action, asking questions, getting answers, and making decisions. I won’t wait for someone to tell me. If I need to know, I’m responsible for asking. I have no right to be offended that I didn’t “get this sooner.” If I’m doing something others should know about, I’m responsible for telling them.”

Ridge turned a boring widget company into a complex learning machine by emphasizing culture, ready to adapt to any industry or market change.

Next is the company’s aggressive acquisition strategy. Ridge did what other WDFC wouldn’t dare — he slashed the dividend to buy other businesses. In April 2001, WDFC bought Global Household Brands for $72.9M, $66.8M of which was paid in cash. Ridge followed through on his plan to transform WDFC from a “brand fortress” into a “fortress of brands.”

This subtle yet stark difference had significant implications for the company’s balance sheet, which Ridge leveraged to make such deals. A far cry from John Barry’s “We have plenty of money — We don’t need the funds for growth so we decided we’d give it back to the people who own the company” era.

By the end of 2001, WDFC’s long-term debt stood at $76.6M — up from $10.6M at the start of the year. Ridge continued to buy companies with leverage and balloon long-term debt. Despite the high debt burden, WDFC still paid ~50% of its earnings as dividends.

International sales boomed as the company financed its “fortress of brands.” According to the company’s 2008 Annual Report, over half of WDFC’s revenues came from international markets. A first in the company’s storied history.

By 2014, Ridge increased revenues to $380M generating 50% gross margins with more than $40M in net income (10% margins). Suppose there’s a secret sauce to the company’s revenue expansion, its distribution channels. Ridge explains the power of WDFC’s distribution strategy in a 2001 Barron’s Article (emphasis mine):

“Take a terrific company like Stanley Tools. They sell a huge selection of different products from hammers to screwdrivers and the like to consumers via one channel, hardware outlets. But if you go to a supermarket, there’s no Stanley presence.

It’s sort of like the funnel you use to fill a gas can, with lots of products going down one chute. But WD-40’s is built on an upside-down funnel, with 43 years of experience selling one product into multiple outlets. No other product, with the possible exception of Duracell batteries, even comes close to matching that.”

Did you catch that? Reread this part, “with 43 years of experience selling one product into multiple outlets.” WDFC spent four decades perfecting the craft of sales distribution with its signature WD-40 can. This product singularity allowed it to create an uncompetitive sales channel that made a more robust and profitable business when bootstrapped with other products. Ridge’s “fortress of brands.”

Through tribal culture, strategic acquisitions, and an unmatched distribution network, Ridge took WDFC to heights never thought possible for a single-product company.

Today, the company generates over $480M in annual revenue across 176 countries while sporting 50%+ gross margins and 20% operating margins. During his tenure, Ridge increased shareholder value by ~775%. That’s a ~34% 23YR CAGR.

The Most Important Lesson: Industry-leading product distribution is one of the most resilient yet least discussed competitive advantages

WDFC had the best product distribution channels in its industry. As such, it could out-sell its lower-priced competition purely based on ease-of-purchase. Simply put, you could buy cans of WD-40 in more places than any other competing lubricant. That level of scaled distribution covers myriad product sins.

For example, consumers might not care that a product is comparatively worse if they’d have to work harder to buy the competitor. Distribution advantages are so powerful because it’s the most challenging part of a consumer-focused product to get right. It requires personal relationships, years of communication, and a robust sales and marketing department. All of which need loads of capital.

Conclusion: 68 Years of History In Three Bullet Points

If we can distill the three most important investing lessons from 68 years of WD-40’s operating history, it’s this:

- Look for products/services that are 5-10x better than any alternative.

- If a stock’s earnings rise faster than its share price, the business probably still represents a good value investment.

- Industry-leading product distribution is one of the most resilient yet least discussed competitive advantages.

WD-40 survived (and thrived) because it did each of these three things better than its competition. Its product was 5-10x better because there was nothing like it on the market. Consumers loved it, which led to revenue and earnings growth faster than its share price.

Finally, the company leveraged four decades of single-product distribution channels to create a highly scalable and unfair product placement advantage. The sum of these factors is a 13% CAGR over 48 years.

WDFC is the first company in our newly-created Investment Case Study Series. Think of these case study lessons like puzzle pieces, with each lesson a part of a giant puzzle. The more pieces we collect, the better our chances of finding the right one to fit a specific spot (I.e., a new investment opportunity).

We’re excited to share our investing lessons with you, and please let us know which company we should study next!