I want to dive into O’Shaughnessy Asset Management’s Q4 2019 Investor Letter. It’s one of my favorites so far this quarter, and you’ll see why.

If you’re pressed for time, here’s the cliff-notes:

-

- Growth beat value, again

- Growth generated returns via multiple expansion

- Value generated returns via good business results or return of capital to shareholders

- Growth vs. Value Expectations Gap Widest Since Dot-Com Bubble

- How We Can Leverage Expectations

Let’s get to the charts …

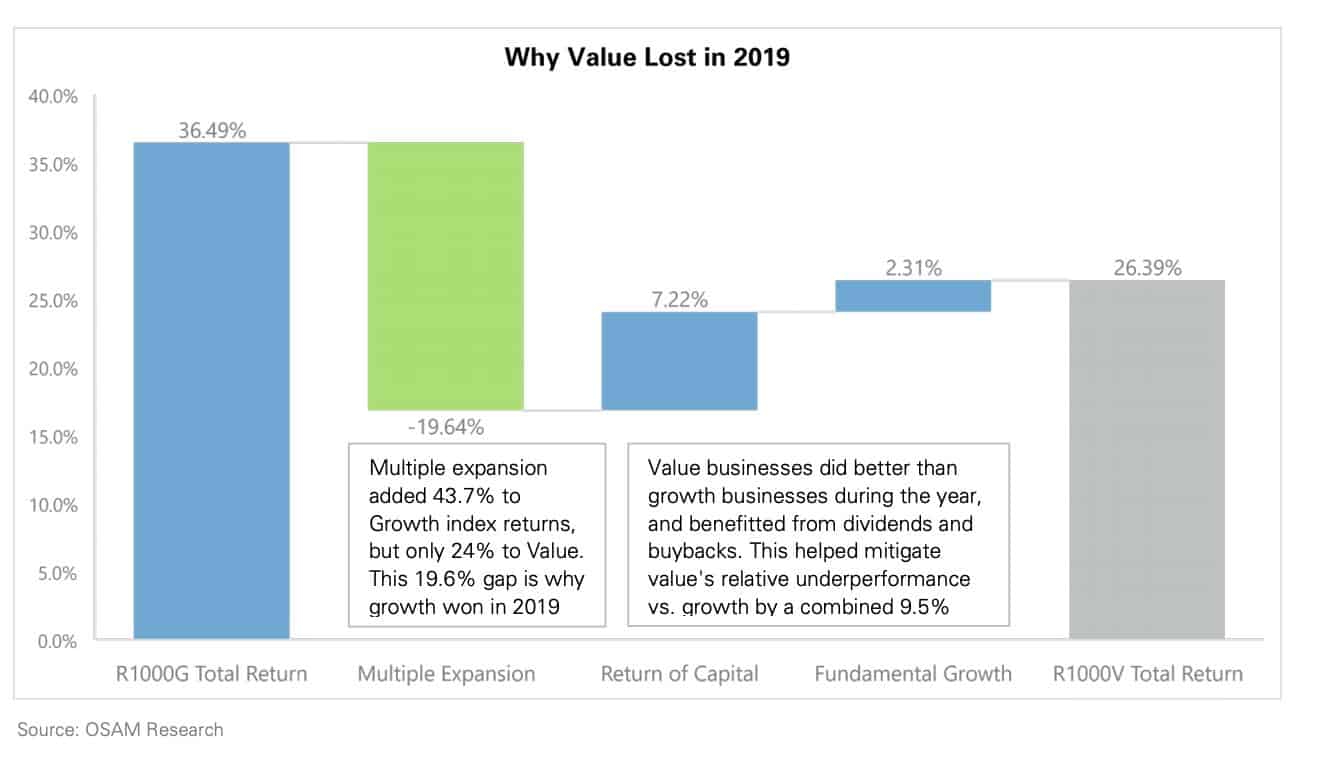

Multiple Expansion Leads The Way

The above chart show’s OAM’s breakdown of style performance for the Russell-segmented stocks. What’s important to note about this graph is the returns from multiple expansion. Russell value stocks returned -1.22% via fundamental business growth and 3.58% via buybacks and dividends.

But the greatest return factor from all Russell segments? Multiple expansion.

And multiple expansion, my friends, is the reason value underperformed growth in 2019. OSAM notes that, “Multiple expansion added 43.7% to Growth index returns, but only 24% to Value.”

That’s why growth won. But it’s more than that. As we look towards 2020 one thing remains clear: embedded expectations for growth stocks are at their highest peak.

The Expectations Game

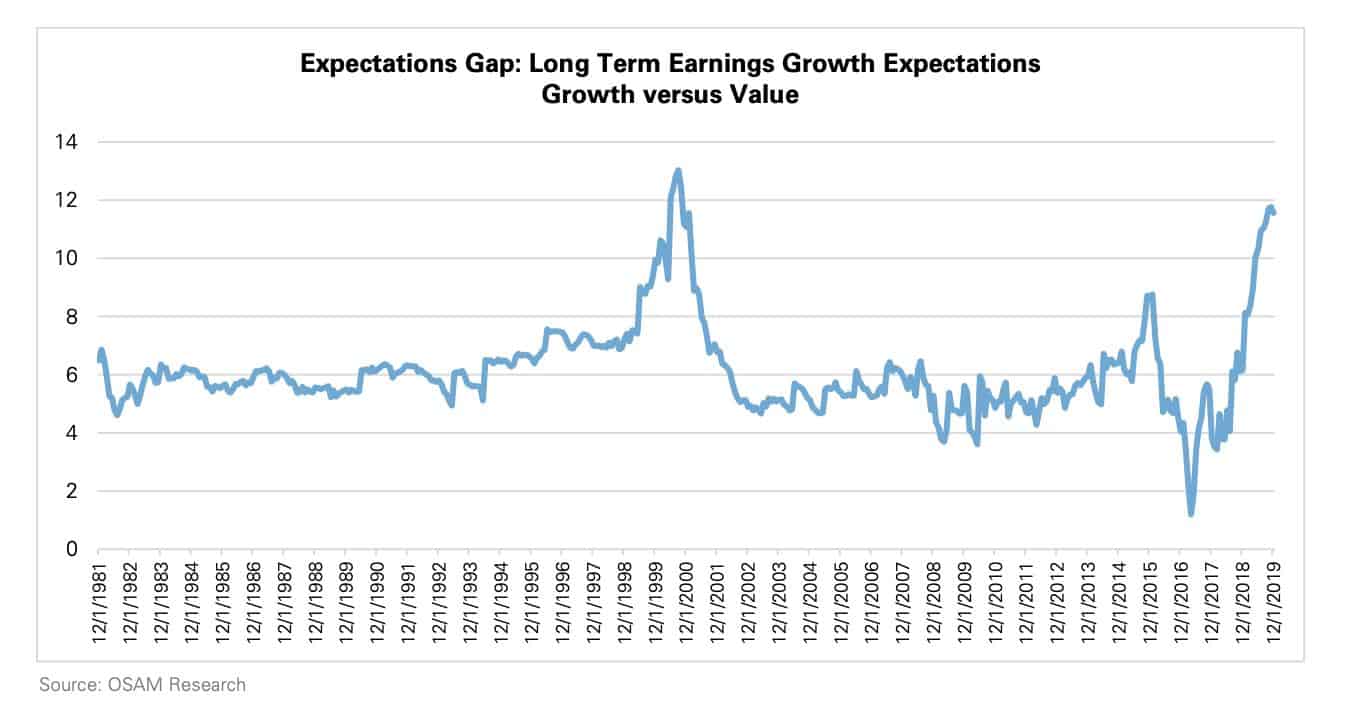

Take a look at the chart below from the letter. What do you notice?

According to OSAM research, the current long-term earnings growth expectations between value and growth is at its largest divergence since the 1999 dot-com bubble.

Embedded expectations is the key to understanding stock price movements. As the chart shows, expectations are now high for growth stocks and low for value stocks. In other words, growth stocks have high hurdle rates to clear over the next year. Value stocks? They’ll soar if they make it through the year.

But I hate this “value vs. growth” debate. Both are necessary for long-term absolute returns. In fact, if we look at stocks through the lens of expectations, we don’t need to segregate into “growth” or “value”.

Learning From The Best: Michael Mauboussin

Michael Mauboussin wrote the book on Expectations Investing. You can grab a copy here. I finished it in a couple of days. Here’s the big picture with expectations investing (from Mauboussin, emphasis mine):

“Expectations investing represents a fundamental shift from the way professional money managers and individual investors select stocks today. It recognizes that the key to achieving superior investment results is to begin by estimating the performance expectations embedded in the current stock price and then to correctly anticipate revisions in those expectations.”

Mauboussin doesn’t mention the words “growth” or “value”. And there’s a reason for that. Behind every stock price is an expectation of the future. That expectation is binary. It’s either better or worse than the company’s past performance. According to Mauboussin, if we want to generate outsized returns, we need to be on the right side of expectations.

How To Profit from Embedded Expectations

Now that we know the expectations gap, we can develop a simple, robust investment strategy. All we do is look in the low expectations pool. Find the lowest decile of expectation stocks, and project what Mr. Market thinks will happen over the next five years (or so).

This is easier said than done, of course. But it’s the mindset that matters. Changing your perception of stock prices from random gyrations to embedded expectations gives you a leg up on almost everyone.

Once you find a low-expectations stock, use a DCF to figure out what Mr. Market’s expecting the company to do over the next few years. Do those assumptions seem unreasonably pessimistic? How low is the company’s hurdle to beat Mr. Market’s expectations?

The lower the expected performance, the higher the expected return if we’re right.

Concluding Thoughts

O’Shaughnessy’s Q4 letter gave us the map to find low expectation stocks. They’re hiding in the value corners. Mauboussin on the other hand, gave us the tools to take advantage of O’Shaughnessy’s research insights (i.e., expectations investing).

This is our playbook for 2020, are you ready?

Have a great weekend!

That’s all I got for today. Shoot me an email if you come across something interesting this week at brandon@macro-ops.com.

Tell Your Friends!

Do you love Value Hive?

Tell your friends about us! The greatest compliment we can receive is a referral (although we do accept Chipotle burrito bowls).

Click here to receive The Value Hive Directly To Your Inbox!