In his textbook study of historical inflation titled “The Great Wave,” David Fischer recounts a tumultuous period in Europe that reached its climax in 1316, writing:

Then, inconceivably, torrential rains came again in 1316. The grain crop failed a third year in a row. Europe began to experience the worst famine in its history. When other sources of food ran out, people began to eat one another. Peasant families consumed the bodies of the dead. Corpses were dug up from their burying grounds and eaten. In jails, the convicts ceased to be fed; we are told that starving inmates “ferociously attacked new prisoners and devoured them half alive.” Condemned criminals were cut down from the gallows, butchered, and eaten. Parents killed their children for food, and children murdered their parents.

Historians estimate that Europe lost over 10 percent of its population to poverty, famine, and starvation in the two years from 1315 to 1316.

This Walking Dead meets Game of Thrones crossover reality marked the end of a major epoch and a transition to an entirely new one. Which, thank God, because the Medieval period sounded like a bit much.

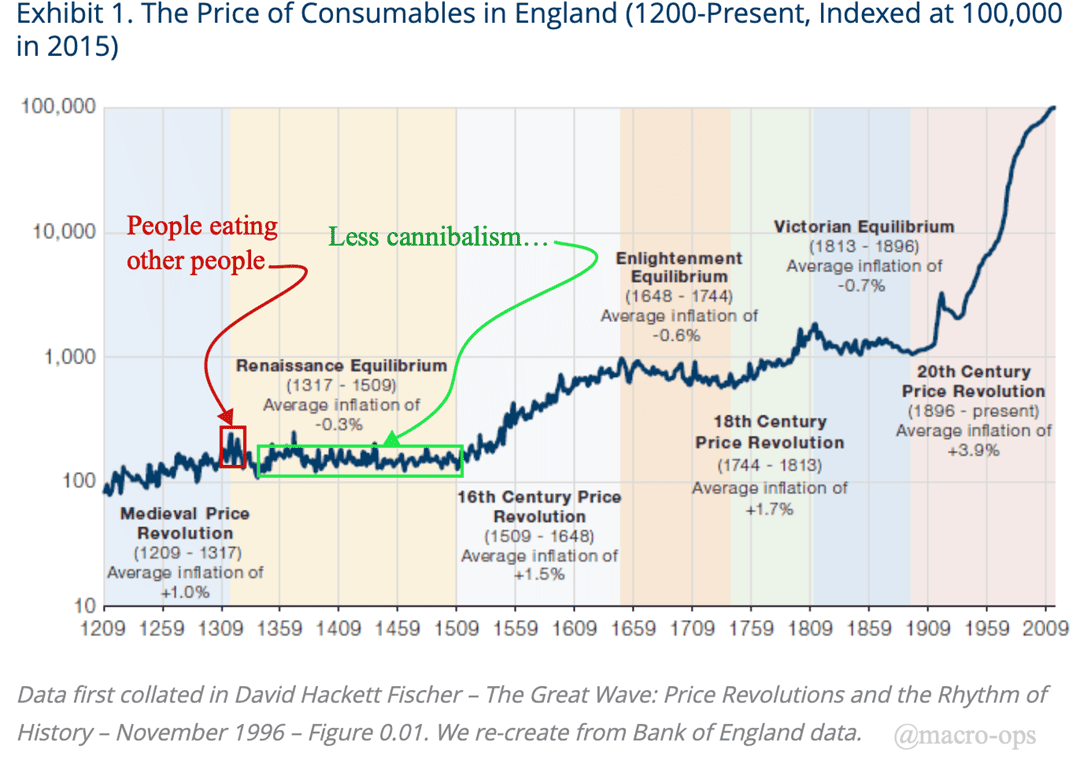

We can see this regime change in the historical prices of British consumables (chart below). The Medieval Price revolution was a century-long trend of rising volatile prices (inflation). This culminated in the dark years of the early 14th century, which helped lay the foundations for the Renaissance. A period of human flourishing, increasing socioeconomic complexity, and stable prices.

This chart is from the Man Institute builds on previous work done by Fischer (red & green annotations are by me).

What Fischer found from his study of price regimes was that there is a direct connection between prices and socioeconomic stability. He writes, “all major price revolutions in modern history began in periods of prosperity. Each ended in shattering world-crises and were followed by periods of recovery and comparative equilibrium.”

**Note: Enrollment to the Macro Ops Collective will run until the end of the week.

The Collective is our premium service that provides research, theory, and a killer community of dedicated investors and fund managers from all over the world. There’s nothing else like it on the web.

If you want to learn more about the Collective and what it can do for you, click here.***

There’s a direct parallel with markets here. Where the market’s reflexive nature means stability always breeds instability and vice versa. Where “stable economies sow the seeds of their own destruction,” to quote Minksy, one of the few economists worth studying.

Despite some insights into historical price patterns, when it comes to the brass tacks… the big and important questions such as where does inflation come from, what causes it, why does it come and go, etc… Fischer throws up his hands, quoting the French historian Fernand Braudel and declaring the task “impossible to solve.”

He weakly concludes with seven causal explanations. These being:

- Monetarist: Understand movements in the “general price level” as changes in the value of money, caused mainly by variations in its quantity and velocity.

- Malthusian: Malthusians think of price movements in a different way as a material representation of the changing value of commodities that money might buy, caused primarily by imbalances between demographic and economic growth

- Marxist: Marxists think that price movements represent the changing terms of transactions within social systems, mainly between social classes.

- Neoclassical: Neoclassical models perceive prices as indicators of change in the flow of supply and demand, and explain price-revolutions as the result of imbalances in market-relations, caused by various demand-centered or supply-side events, or by changes in the structures of market-conditions themselves.

- Agrarian: Agrarian approaches link prices mainly to harvest conditions.

- Environmental: Environmental models understand price-movements as ecological indicators which register imbalances between human activity and its natural environment.

- Historicist models: Historicists explain things in their particulars, and think of each price-revolution as a unique event with its own ad hoc explanation.

So basically anything and everything can and does impact the trend and vol of prices.

To the reader, this is most certainly an unsatisfactory conclusion. Many of us would prefer a simpler world with direct lines of causality. But, alas, that’s not what we get in economics, and certainly not when it comes to the subject of prices.

Even though Fischer wrote The Great Wave 23 years ago, very little has changed in our broader understanding of price dynamics today.

The last two years of the lords of finance being caught embarrassingly offside by what proved to be quite dramatically non-transitory inflation is case in point. An economic paper published a few years ago quantitatively showed that the main gauges used by policy makers to understand inflation don’t actually have any signal value. So I guess this shouldn’t be of much surprise…

What then, are we humble non PhD simpletons left to do when it comes to the case of price trends and volatility?

Do we just point to random chart lines and gnash our computer keys with fervor as we share our completely unwarranted yet highly convicted hot takes about where inflation is going and why to the rest of the twitterati, as do so many suit and tie wearing blue checkmarked monkeys on the bird app?

Or do we jam our heads in sand and yell PASSIVE INVESTING!!! into the great void comforted by the last 40 years of trends along with our enviable ignorance of economic history?

Most will choose one of the above two.

Fortunately, there’s a third option.

One that requires some nuance. Some exploration of market history and the use of logic to derive at first principled mechanisms of causality.

Which is just what we’re going to do.

In the next three follow-up pieces, which will be published in the coming days. We will break down the drivers of cyclical inflation. We’ll then look at larger secular inputs into the inflation equation. And we’ll finish with a discussion on how the two interact, along with our argument for why we expect cyclical inflation to quickly drop. But then land at a higher structural level, as secular forces keep it elevated (between 3%-6%) over the next decade.

The hope is you come away with a broader understanding, a loose framework of sorts, in which to think about and understand inflation. We’ll also share the big moves and new trends to watch out for as a result of this new price regime.

And we’ll, of course, include our proprietary probit model’s read on the statistical likelihood that the western world devolves back into total chaos and widespread cannibalism…

A few quick thoughts on Powell’s remarks and the market.

Powell gave his speech at the Brookings Institute today. You can read the transcript of it here.

There’s not a shortage of strong opinions and confirmation bias being bandied about as objective interpretations of the meaning behind the words of one of our main Game Masters. I personally didn’t find the speech to be revealing. Just more of the same. Take from it what you will. What the market is saying in response, is what I find more interesting.

The Narrative Pendulum is swinging in full favor of the bulls today. Positioning, supportive technicals, and strong seasonals are all helping to propel a previously oversold and unloved market in the direction of a “soft landing” consensus.

This helped put the SPX back above its 200dma. An important resistance level we noted in this week’s Dozen (link here).

Credit spreads came in today. Semis jumped relative to the S&P. We got a 90%+ upvol day. If we get another one tomorrow, it’ll trigger an official breadth thrust, which would, of course, be bullish. So this is all good and well for the bear market rally we’ve been playing for this past month and some change.

We’re already fairly tactically long through our index futures and single name positions. So we won’t be adding here. We want to see how things shake out over the coming days as moves around Fed comments tend to be quite noisy.

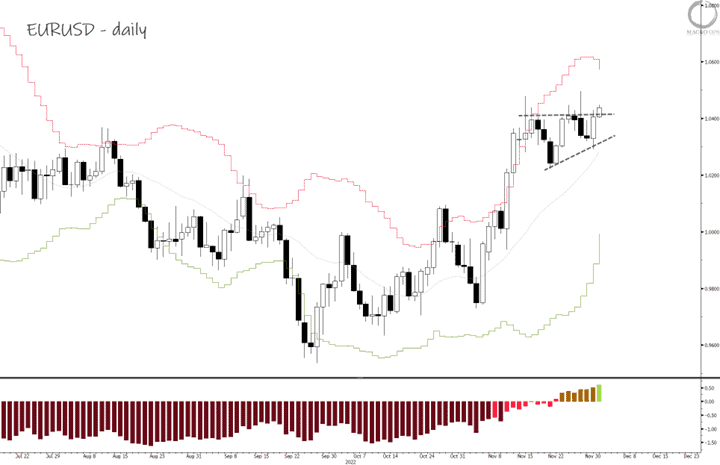

We will be taking a swing at EURUSD this week. The euro shows a strong tendency to rally in December, as I pointed out Monday (link here). The pair is breaking out of a bull flag within a Bull Quiet regime.

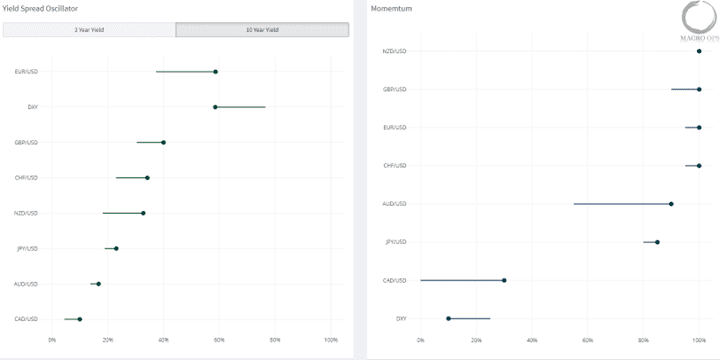

And it’s showing the strongest yield spread momentum out of all the DM pairs.

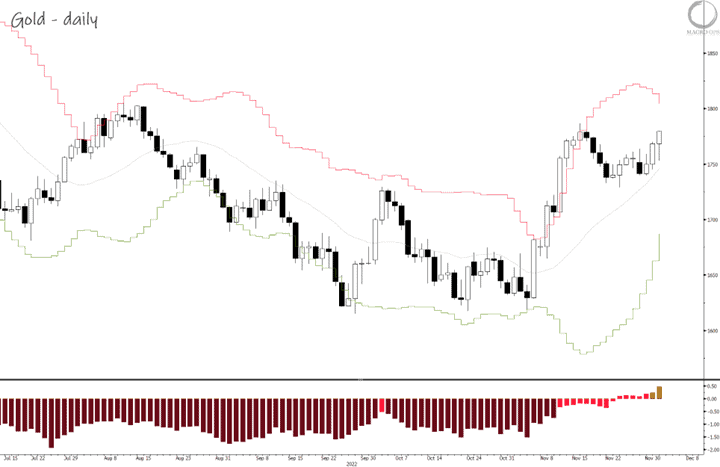

Lastly, we’ll be adding to our long precious metals positioning this week. This time using the futures (we’ll send out a trade alert when we execute).

Gold and silver are moving closer to Bull Quiet regimes. And their tapes are showing increasing bullish dominance, which is what you want to see at the start of a larger bullish trend. We expect PMs to be one of the best-performing assets over the next couple of years, so we’re willing to be a bit more aggressive in building up size in this trade.

We’ll send out more info to the Collective when we make these moves!

**Note: Enrollment to the Macro Ops Collective will run until the end of the week.

The Collective is our premium service that provides research, theory, and a killer community of dedicated investors and fund managers from all over the world. There’s nothing else like it on the web.

If you want to learn more about the Collective and what it can do for you, click here.***

Thanks for reading.

Stay frosty and keep your head on a swivel.