We can’t help but think of the classic 80’s comedy Airplane! when talking about aircraft lessors. The story here is just as funny. And it’s not a new story either. It’s the same thing we see over and over again. The repetitiveness is what makes us laugh.

What exactly are we talking about? We’re talking about excess. We’re also talking about piss poor planning. These often times seem to be the qualities embedded in every top level executive.

Over the last few years the aircraft leasing industry has taken off. The business is centered around leasing aircrafts to airlines. Airlines often don’t want the financial burden of buying a brand new airplane so they lease one instead. The aircraft lessor supplies the plane and the financing to cut the deal.

High oil prices and growth in emerging markets over the last decade have been a boon to aircraft lessors. The lessors sold to airlines seeking newer fuel efficient planes and also to expanding markets such as China and Brazil.

The leasing industry, riding high on budding demand, expanded inventory and fattened operations. Executives began believing that the demand growth would last forever. Just like Detroit executives believed the high-margined SUV craze would last forever. Recency bias plus greed induced myopia is never a good mix…

Not ones to learn from others past mistakes, lessors responded to the demand surge by buying a lot of planes. Having more planes meant more leases and growing profits. The classic boom part of the cycle unfolded perfectly.

But as is always the case with booms, the busts inevitably follows. Everything that’s leveraged to the hilt to capitalize on temporary excess demand suddenly becomes an anchor dragging the business down.

Lessors didn’t think about the possibility of oil prices collapsing or emerging markets faltering. But now oil prices are in the crapper and emerging markets look like a train wreck. So of course, aircraft demand has fallen off a cliff.

This is bad news for the industry because it’s got a major supply glut of brand new planes. Companies unable to move leases are stuck paying for idle (and expensive) inventory. So long to the fat profits of yesteryear.

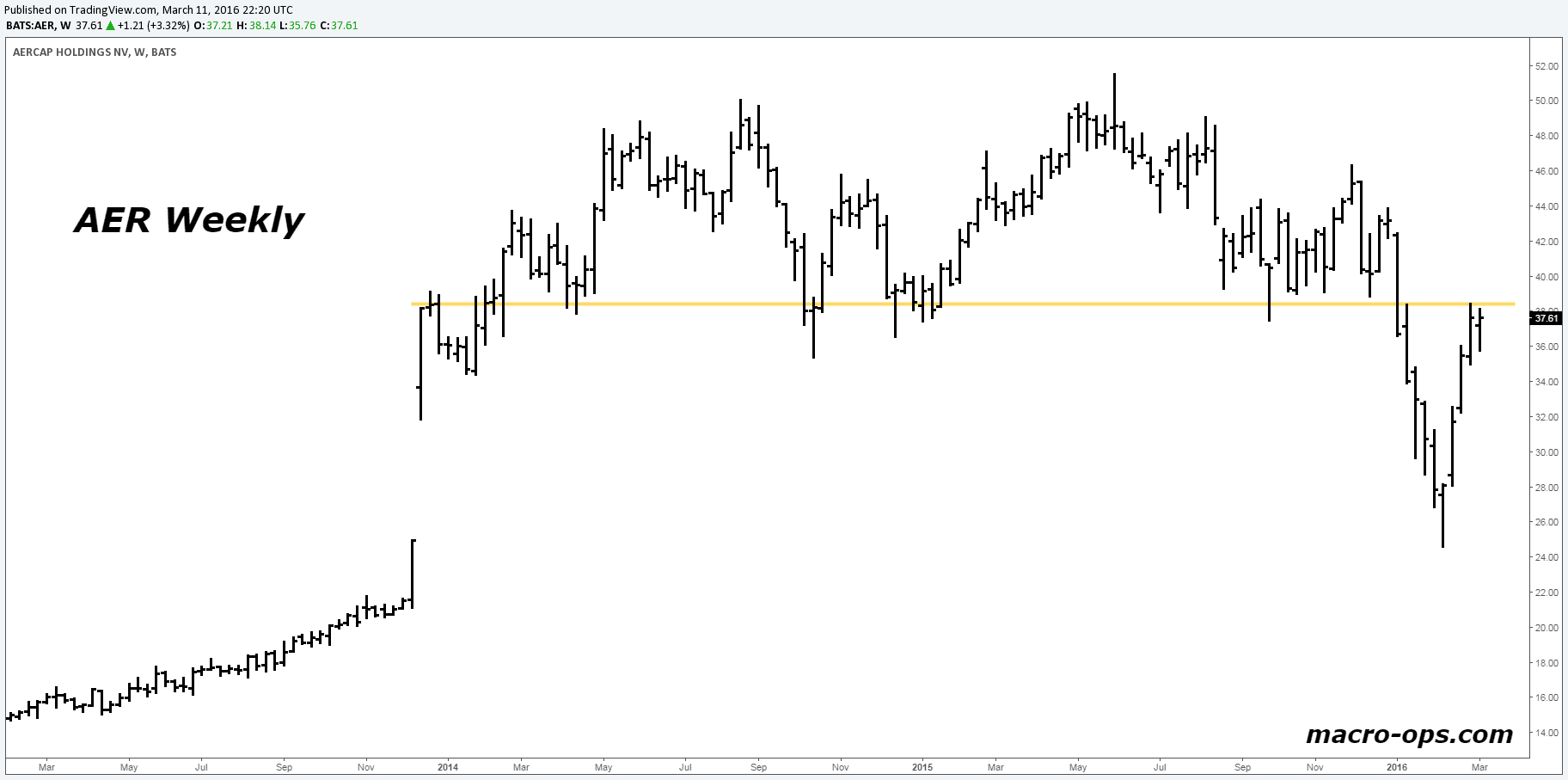

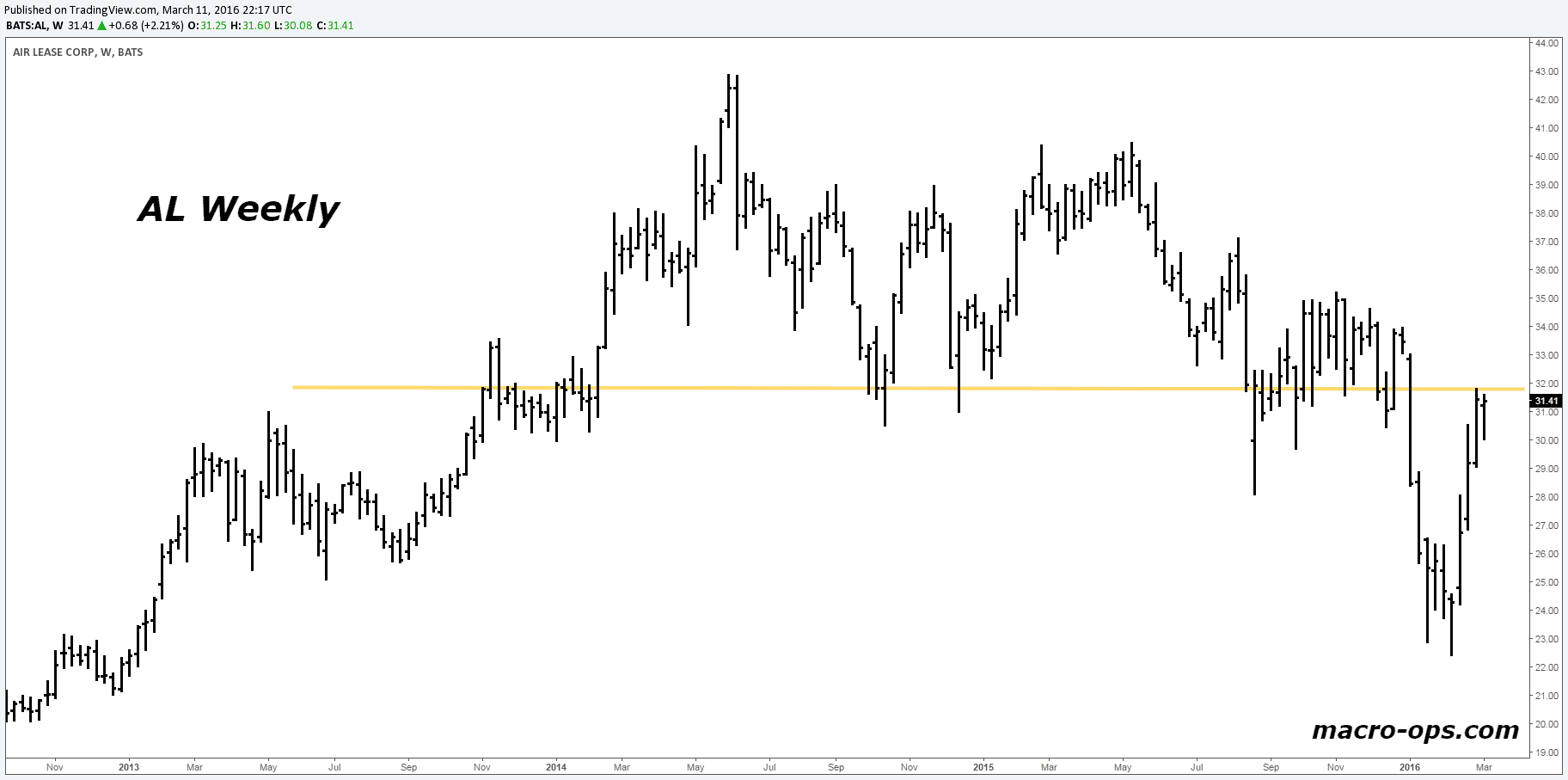

Our buddy Jamie from the Operator Community brought two specific short targets to our attention. AerCap Holdings (AER) and Air Lease Corporation (AL). Out of all the lessors we looked at it, these two had the best setups. But before we jump into technicals, let’s cover the fundy story a bit more.

As we’ve explained, high oil prices are a big driver of aircraft demand. Expensive oil means greater fuel costs. With high oil prices it’s cheaper for airlines to buy a new plane versus operating an old one.

For example, a new Boeing 787 Dreamliner is 16% cheaper to fly than an old school B767 from 1982. Other newer planes like the Boeing 737 Max and Airbus A320neo were saving up to three bucks a gallon on flights. With savings like that, new planes made sense.

But this was when oil was trading above $90/bbl. Which isn’t the case anymore. Now, with cheap oil, the cost savings have reversed. Older planes have become more economical. Nobody needs a fancy (and expensive) new plane.

Companies with older fleets are less likely to upgrade. When they run the costs with low fuel prices, it makes sense to keep flying older planes.

If they have to replace an old plane for other reasons, they’re no longer forced get a new fuel efficient plane. Lower oil prices means fuel issues aren’t as pressing. They can buy used planes that have similar fuel consumption rates. This is a much cheaper option.

Recently, Delta purchased a used 777 jetliner for $7.7 million. You know how much a brand new 777 costs? $277.3 million. Big difference. A used plane costs only three percent of a new one. If you can get away with that kind of savings, why wouldn’t you?

Demand from emerging markets is suffering too.

Wealth management firm Canaccord Genuity recently warned that the United Arab Emirates’ Etihad Airways and Russia’s Aeroflot are likely to defer new plane orders due to poor economic conditions. (I bet Putin doesn’t mind though. He prefers shirtless horseback travel anyway.)

As Aircastle (another aircraft lessor) CEO Ron Wainshal explained:

“The demand for planes is a concurrent economic indicator. Economic activity and airplane travel tend to go together.”

If emerging markets are hurting, you can bet they don’t have much demand for new aircrafts. And this is a problem because they’ve been the primary driver of growth in aviation markets. For example, in 2014, Air Lease got 22.1% of its revenue from China. The year before Chinese revenue was only 15.5%. That’s a growth rate of over 40% a year.

But China is slowing, along with the rest of emerging markets. And it’s not getting better anytime soon.

The recent Singapore airshow should serve as a warning of things to come. The airshow is one of the largest in the world and Asia’s biggest. Normally there are tons of deals made and planes sold. But this year’s aircraft orders were pathetic. The deal flow amounted to $12.3 billion, nearly a 75% cut from the deals made in 2014. Shukor Yusof of the aviation consultancy Endau Analytics explained:

“This airshow [was] the most quiet and most muted in terms of sales and buzz. There are far too many aircraft orders already from the region, so we [saw] airlines do the sensible thing and not [get] carried away by placing more orders.”

There’s that oversupply problem again.

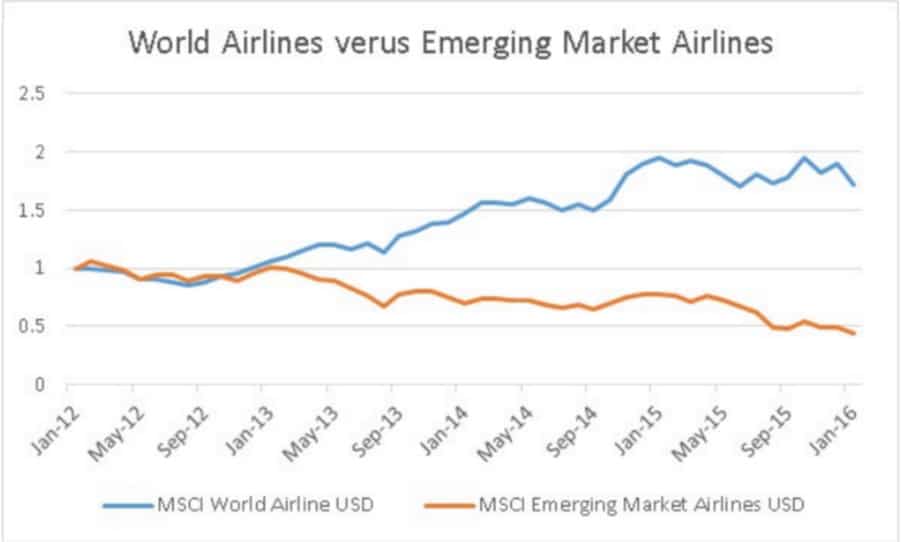

You can see below how emerging market airlines are struggling. Especially when you compare them to the rest of the world.

A lot of airlines around the world have reported higher capacity with a lower load factor. Load factor is the measure of an airline’s ability to fill its seats. This means their supply has grown faster than passenger demand, causing them to lose money. All the big boys — JetBlue (JBLU), American Airlines (AAL), and United Airlines (UAL) — expect revenues to drop anywhere from 6-8% in the first quarter. And Delta Airlines (DAL) expects per passenger revenue to drop 2.5 – 4.5% this quarter.

Boeing recently announced cuts to the production of its 747 and 777 models to deal with the lower demand. This is a bad sign for the industry. But it’s the first step in reducing the glut that built up over the years. It will take some time to correct itself. And the pain will be real.

Another major problem is the amount of debt involved in the aircraft leasing business. Check out the debt-to-capitalization ratios for some of the bigger lessors:

- Aercap Holdings (AER) = 78%

- Air Lease (AL) = 72%

- Aircastle (AYR) = 69%

These levels aren’t unusual for this industry. Airplanes are big purchases and require a lot of financing.

But this is still a lot of debt for a company to service. Especially when that company’s cash flows are getting squeezed from both ends (with lower sales and higher costs maintaining idle inventory).

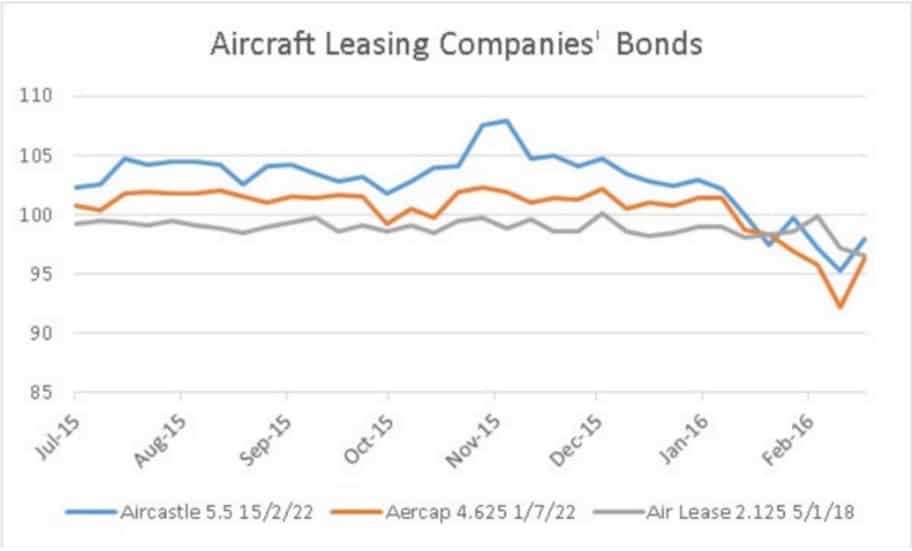

So if things get bad enough, servicing debt could become a problem. Due to this growing concern, lessors’ bonds have been getting hit. This is a signal that “smart money” sees potentially large risks ahead.

It’s funny, nowadays you can’t mention debt without mentioning China. It’s no different here.

As we explained, a lot of demand for airplanes is coming from emerging markets, especially China. China’s response is to take advantage of the increasing demand. We’re now seeing a lot of Chinese companies jump into the airline leasing business.

The Chinese domestic share of the aircraft leasing market has shot up from 7% in 2007 to 40% today. Chinese regulators spurred this on by relaxing lending rules in 2013 and 2014. This helped create nearly 500 new leasing companies. And this year, one of the biggest Chinese lessors, BOC Aviation, is planning to go public with a $3 billion listing. Four of the top 15 lessors in the world are now Chinese firms, including BOC.

One reason the growth in China has been so explosive is because the Chinese government guarantees all their bonds. Growth is easy when money is free.

These new Chinese firms mean increased competition in the global aircraft leasing space. There will be more supply pushed into the market, driving profits lower for everyone.

A perfect storm has formed and is headed for aircraft lessors whom have grown fat and complacent off of unusually good years. There is going to be a massive culling. Many of these lessors will be fleeced.

Our targets of choice to play this correction are AerCap Holdings (AER) and Air Lease Corporation (AL). Both have broken down from large multi-year topping patterns. Recent retraces were violent, but these rallies brought the price right back to the initial support line, which is now acting as resistance.

This bull rally has created a great opportunity to put on a short position to ride the wave down. Careful though. Bear markets are volatile and tricky for inexperienced traders. When shorting, be sure to take profits quicker than otherwise.

When it comes to aircraft lessors, we tend to agree with the CounterPoint segment from Airplane!

“Shanna… they bought their tickets, they knew what they were getting into. I say, let ’em crash!

The price of these stocks ran up due to excess. And now they have to correct. We say let ‘em. We’ll profit nicely from the crash.