The father of modern physics, Albert Einstein was unquestionably a brilliant mind. Not only did he change the world with his work in physics, but he was also an avid sailor, played the violin and shared this gem with the world:

Compound interest is the eighth wonder of the world. He who understands it, earns it … he who doesn’t … pays it.

In investment circles, Warren Buffett is most credited with exploiting the benefit of compounding and, at 88 years old, has obviously figured out how to do just that!

It isn’t too challenging to understand and agree with what Einstein and Buffet have taught us: anyone in the markets understands that compounding is a powerful force. But, for fun, indulge me for just a second while I run through some good ol’ fashioned numbers to illustrate the point.

A couple of assumptions before we begin. For simplicity, I am not factoring in inflation, down years, depressions, unusual returns, time away from the markets, commissions and fees, and/or anything that would make this a more robust system than it needs to be for purposes of this exercise. The goal is to not get bogged down with details, but to take a step back and see what compounding interest can build over the long term.

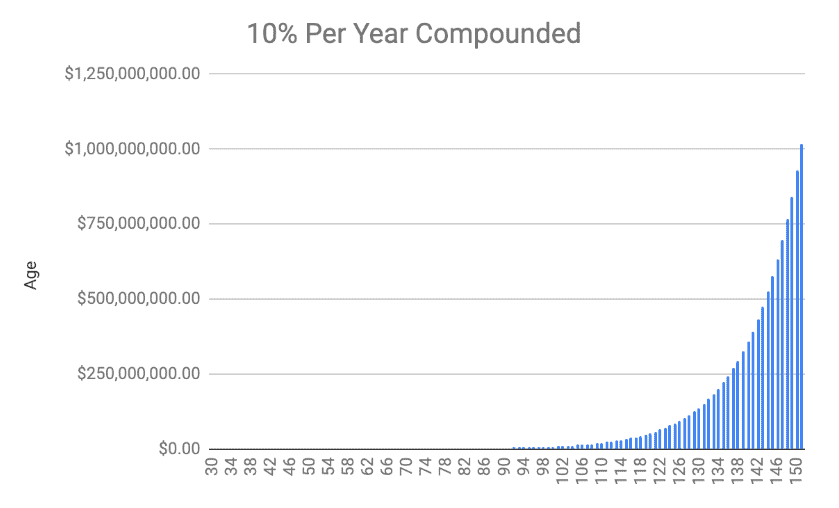

I started the test out at age 30 with $10,000. Maybe you started earlier and already have $10,000 saved at age 21, or over $100,000 by age 50. If you’re one of these magic unicorns, kudos! You are already well ahead of the game and on the road to billionaire status. For the rest of us, here is what my model revealed.

The math is simple: if compounding can put 10% per year back into our accounts, then in theory, all we have to do is live longer to cross that $1 Billion threshold.

In my model, starting at age 30 with $10,000 means by 151 years of age you’ll be a billionaire.

If you want just half a billion, then you only need to live to about 144 years old! Maybe $100 Million is more your sweet spot…that’s only to 126 years old.

Interestingly you don’t actually break the million dollar mark until your 79th year.

I’m not going to lie, it is slow going in the beginning, so it’ll be hard to keep your eyes on the prize until later in life, where the numbers really start to shoot up dramatically.

If you are 44 years old with $500,000 in assets, you reach the $100m mark on your 100th birthday! And a billion by the potentially attainable age of 124 years old.

Yes, I recognize that this simplified “all you have to do” theory may sound ridiculous, but we can all agree that if you have more time to earn, then your overall assets will grow much larger. So, it isn’t a question of whether or not the math works out (it does), but instead, how long you can live while still maintaining a high quality of life?

We need a lot of time to get to the billion dollar mark, but we also need to get there in as good as shape as possible, otherwise what’s the point? Our bodies and minds must be healthy enough to enjoy that large nest egg.

In 1955 the average life expectancy in North America was 69 years of age. In 2015, 50 years later, it was 79 years old. A nearly 15% increase. Using this metric, 50 years from now, our average life expectancy may be close to 90 years old. And it’s not crazy to think that life expectancy will exponentially increase over the next 50 years as we see rapid advances in tech and healthcare.

So there is a potential to earn a billion dollars like Charlie Munger says:

Sit on your ass. You’re paying less to brokers, you’re listening to less nonsense, and if it works, the tax system gives you an extra one, two, or three percentage points per annum.

And he’d know, at age 95 he’s made a lot of money just sitting on his ass and compounding.

If we want a chance to hit the $1 Billion mark we need to stay laser focused on increasing our own life expectancy.

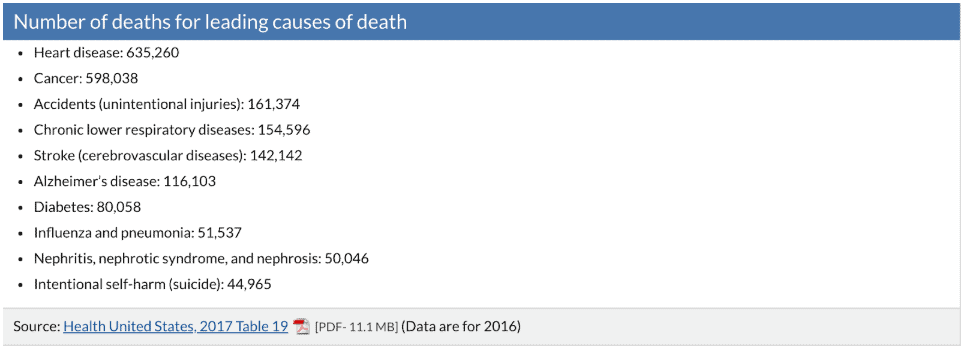

Here are the leading causes of death in the United States from the Center for Disease Control.

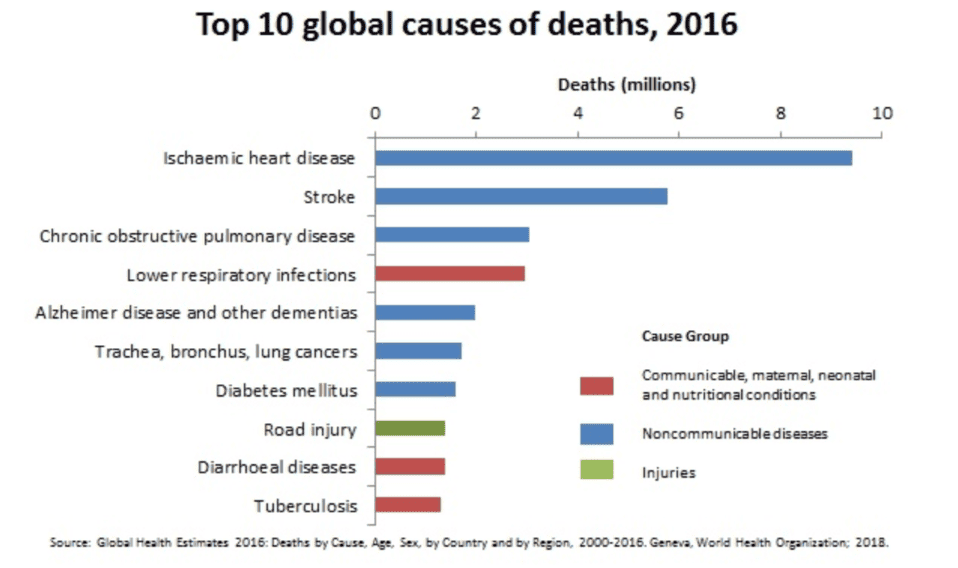

And internationally it’s fairly similar according to the World Health Organization.

Generally speaking these are common worldwide:

- Heart Disease

- Cancer

- Accidents

- Stroke

- Alzheimer and Dementia

- Diabetes

- Road Injury

- Lower Respiratory Infections

- Influenza

- Suicide

Knowing that we don’t have cures for most of these just yet, it is a bit hard to optimize against them; however, we have lots of information regarding known causes of heart disease, cancer, diabetes, alzheimer’s and the flu. If you are living in a world where chronic disease is inevitable, we should chat more. It isn’t.

We know that diet, negative environmental factors, sleep, exercise, and sense of purpose have been directly linked to the most common causes of death.

To achieve a $1 Billion net worth we have to pour our energy into making sure our body and mind stay healthy for as long as possible.

Dr. Peter Attia is the foremost expert on the front lines of longevity. If you are interested in learning all about his work in the field of longevity, I highly recommend you go down this rabbit hole – it is well worth the read, watch the video, and then get to Googling.

If you’d rather just read an abbreviated version, here are a few of Dr. Attia’s suggestions:

- Fast – 12-16 hours per day is good for metabolic health and weight management and something that can be practiced everyday. I’ve been doing this for about 15 years now, off and on.

- Fast – A more challenging fast that lasts 2-3 days. It isn’t a complete fast, it is a fast mimicking diet called Prolon which increases autophagy or simply a cleaning of the bad stuff by your cells. And finally a 4-5 day Prolon fast really increases stem cell based rejuvenation. Research this before you undertake it.

- Eat whole foods, the stuff our grandparents would recognize.

- Drop the sugar and keep insulin low.

- Sleep more and sleep better.

- Drink more water.

- Don’t Smoke.

- Exercise, and focus on strength/resistance training above all other forms of exercise.

- Live for something, have a mission!

- And if you live in the United States, stay off the Opiates.

What’s the payoff? Well, you’ll feel better almost immediately, but you also may have a shot at compounding your face off to a $1 Billion net worth!

In summary, start purchasing cash flow producing assets, let them compound, don’t fiddle with them, eat less, exercise more, sleep more, drive safely, and live for something! Write to me when you turn 150 and cross the $1 Billion line so we can celebrate!

Age Assets

30 $10,000.00

31 $11,000.00

32 $12,100.00

33 $13,310.00

34 $14,641.00

35 $16,105.10

36 $17,715.61

37 $19,487.17

38 $21,435.89

39 $23,579.48

40 $25,937.42

41 $28,531.17

42 $31,384.28

43 $34,522.71

44 $37,974.98

45 $41,772.48

46 $45,949.73

47 $50,544.70

48 $55,599.17

49 $61,159.09

50 $67,275.00

51 $74,002.50

52 $81,402.75

53 $89,543.02

54 $98,497.33

55 $108,347.06

56 $119,181.77

57 $131,099.94

58 $144,209.94

59 $158,630.93

60 $174,494.02

61 $191,943.42

62 $211,137.77

63 $232,251.54

64 $255,476.70

65 $281,024.37

66 $309,126.81

67 $340,039.49

68 $374,043.43

69 $411,447.78

70 $452,592.56

71 $497,851.81

72 $547,636.99

73 $602,400.69

74 $662,640.76

75 $728,904.84

76 $801,795.32

77 $881,974.85

78 $970,172.34

79 $1,067,189.57

80 $1,173,908.53

81 $1,291,299.38

82 $1,420,429.32

83 $1,562,472.25

84 $1,718,719.48

85 $1,890,591.42

86 $2,079,650.57

87 $2,287,615.62

88 $2,516,377.19

89 $2,768,014.90

90 $3,044,816.40

91 $3,349,298.03

92 $3,684,227.84

93 $4,052,650.62

94 $4,457,915.68

95 $4,903,707.25

96 $5,394,077.98

97 $5,933,485.78

98 $6,526,834.35

99 $7,179,517.79

100 $7,897,469.57

101 $8,687,216.52

102 $9,555,938.18

103 $10,511,532.00

104 $11,562,685.19

105 $12,718,953.71

106 $13,990,849.09

107 $15,389,933.99

108 $16,928,927.39

109 $18,621,820.13

110 $20,484,002.15

111 $22,532,402.36

112 $24,785,642.60

113 $27,264,206.86

114 $29,990,627.54

115 $32,989,690.30

116 $36,288,659.33

117 $39,917,525.26

118 $43,909,277.78

119 $48,300,205.56

120 $53,130,226.12

121 $58,443,248.73

122 $64,287,573.60

123 $70,716,330.96

124 $77,787,964.06

125 $85,566,760.47

126 $94,123,436.51

127 $103,535,780.16

128 $113,889,358.18

129 $125,278,294.00

130 $137,806,123.40

131 $151,586,735.74

132 $166,745,409.31

133 $183,419,950.24

134 $201,761,945.27

135 $221,938,139.79

136 $244,131,953.77

137 $268,545,149.15

138 $295,399,664.07

139 $324,939,630.47

140 $357,433,593.52

141 $393,176,952.87

142 $432,494,648.16

143 $475,744,112.97

144 $523,318,524.27

145 $575,650,376.70

146 $633,215,414.37

147 $696,536,955.81

148 $766,190,651.39

149 $842,809,716.53

150 $927,090,688.18

151 $1,019,799,757.00