“The Ideal Investment over the past 60-70 years has been to buy a piece-of-crap net-net company that got acquired by a young man named Warren Buffett. And then to hold that piece-of-crap net-net as Warren Buffett did his thing. Yet that wasn’t on anyone’s Bingo Card.”

Christian Ryther is the founder and portfolio manager at Curreen Capital. The fund invests in micro-caps, small-caps, and special situations like spin-offs, rights offerings, and carve-outs throughout the UK, US, and Sweden.

Christian and I discussed many investing topics during the podcast, including:

- When flowers turn to weeds (and vice versa)

- When should you cut weeds?

- How do you know when you have a flower?

- Christian’s Upside/Downside Framework

- GetBusy $GETB and Truecaller $TRUE_B

- Christian’s Ideal Investment

And more.

Christian is in the spotlight for this week’s 3 Big Things (3BT).

3BT distills my podcast episodes into bite-sized summaries. Each piece features:

- One Conversation (Stocks, Psychology, Markets)

- One Framework (Mental Model, Analytical, Behavioral)

- One Idea (Long or Short)

Let’s dig into my podcast with Christian Ryther.

One Conversation: Christian’s Ideal Investment

I’ve asked guests the question, “What would be your ideal investment?” and Christian’s response might be my favorite (emphasis added):

“The Ideal Investment over the past 60-70 years has been to buy a piece-of-crap net-net company that was acquired by a young man named Warren Buffett. And then to hold that piece-of-crap net-net as Warren Buffett did his thing. Yet that wasn’t on anyone’s Bingo Card.”

I love this answer because it’s real and shows how much investor appetite changes over time. For example, the ideal investment 30-40 years ago looked nothing like the names current investors praise.

Thirty years from now, investors will say the same about today’s current A-listers.

So while Christian couldn’t offer his ideal investment, he described what his “best achievable success” would look like (paraphrasing, emphasis mine):

“The ideal investment would look something like this. It would be a spin-off of a smaller company from a much larger enterprise. The spun-off management team would have an excellent track record of high returns.

Ideally, this company would have low gross margins but high ROICs, allowing me to buy it at distressed market prices and high cash flow yields.

But suppose I’m being honest, even in this scenario. In that case, I’d likely hold the business for 3-5 years and then sell it for another name I wind up liking more at the time.”

Ryther mentions an important point about investing. Everyone thinks they have the guts to hold an investment through massive drawdowns and reap the rewards of multi-bagger-dom.

But the truth is that holding an investment for that long is harder than anyone thinks.

This is why I loved Christian’s response. It was honest. He knows his personality and plays within 3-5 year time horizons. Flipping ugly ducklings along the way for above-average market returns.

I love that.

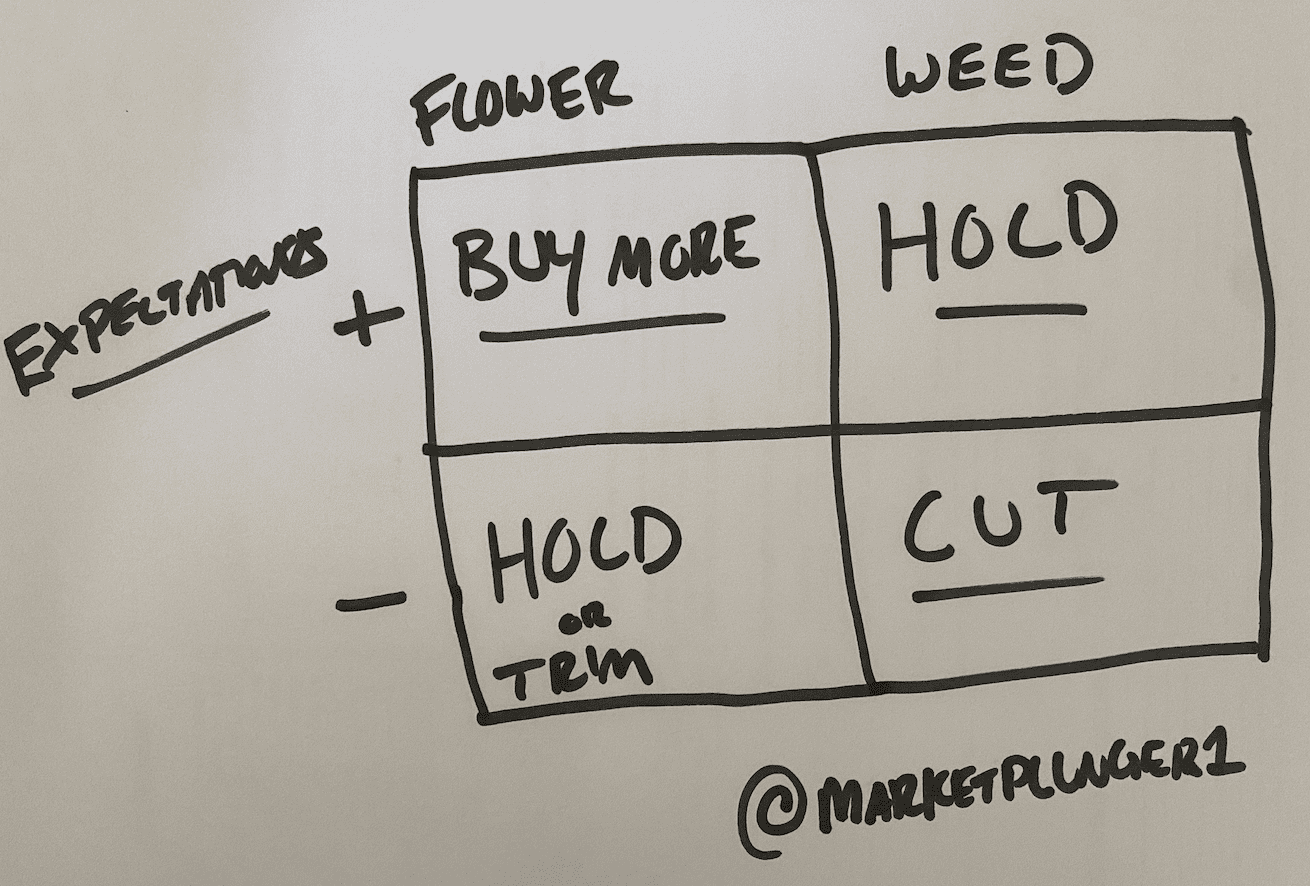

One Framework: Water The Flowers & Cut The Weeds

Every trader knows the phrase, “cut your losses and let your winners run.” Peter Lynch argued a similar philosophy for investors. He suggests investors should “water your flowers and cut your weeds.”

While both claims sound identical, there is one key difference.

Traders use price action to determine when to exit losers and keep (or add to) winners. Just set a stop-loss, a profit target, and forget it.

Investors, however, rely on underlying business performance to guide their decisions. As long as the business improves, the stock price can do whatever it wants.

Now that we understand this distinction, what separates weeds from flowers? Christian defines weeds and flowers as (emphasis mine):

“A “flower” is an investment where things are going as well as you expected, or even better. A “weed” is an investment where things are not going as well as you expected.”

Remember, these are expectations regarding underlying business performance, not stock price movement.

You must set expectations before making an investment. Otherwise, it’s like shooting an arrow at a target you hope appears 40-yards away. Assuming you’ve documented your investment’s expectations, it’s decision-making time.

We can think about Ryther’s Water The Flowers Framework through a Decision Matrix, which outlines the four decisions we have as investors.

No bonus points for artistic talent.

The above matrix simplifies (as best it can) the investor’s decision framework. When a flower performs above expectations, you buy more.

Conversely, when a weed performs below expectations, cut it. Those are the easy decisions.

Hard decisions come when a flower reports below expectations. Maybe for the first time since you’ve bought it. Ask yourself, “does this quarterly’s underperformance permanently impair the company’s long-term bull thesis?”

If the answer is “Absolutely not,” hold the stock. If it’s “Maybe, but I would need a couple more negative quarters to confirm,” trim the stock.

On the other hand, investors can hold weeds that crush expectations. You might have a flower on your hands. Or it might be a turnaround situation where you bought a weed expecting a future flower.

One Idea: Truecaller (TRUE_B)

Truecaller provides a mobile app to identify spam and scam callers. The company is both profitable and growing like a weed.

Christian invested in TRUE_B because the company solves a large and frustrating problem: spam callers.

Here’s Christian’s thoughts on TRUE_B in his Q4 2021 letter (emphasis mine):

“I like that Truecaller is a fast growing, profitable business that is successfully addressing a large problem. Scam and spam phone calls are profitable, and I think that this will drive continued innovation by scammers and spammers.

Governments, phone manufacturers, phone operating system companies, and phone networks can and will continue to stymie the efforts of phone scammers and spammers. Still, this fight is a cost center for them, and innovation is an expense. For Truecaller, fighting spam and scam callers is a profitable business, where money spent to innovate can deliver a high ROI.”

Android and iOS rule changes also reinforce TRUE’s competitive advantages. Back to Ryther’s letter (emphasis added):

“Rule changes by Google’s Android and Apple’s iOS have made it difficult for new entrants to begin combatting scam and spam calls – apps can no longer just take their users’ contact lists to quickly build a database of phone numbers.

This means that the existing caller ID apps have a substantial advantage over new entrants in building and maintaining a database of phone numbers worth answering.”

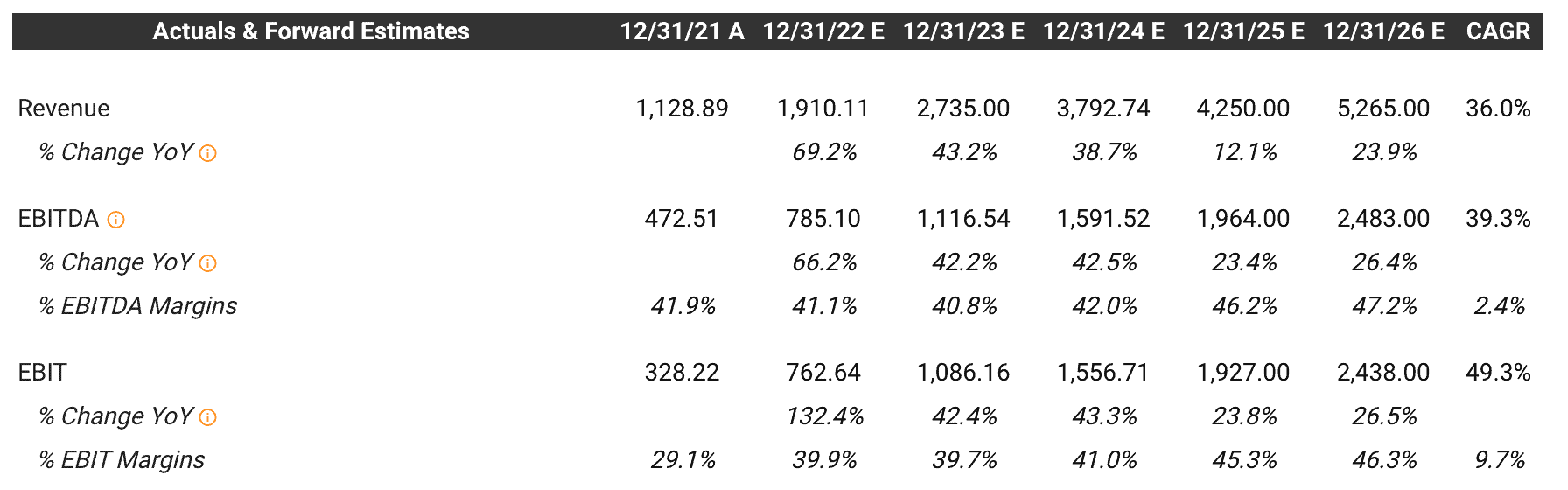

The company currently trades at ~11.5x NTM Sales and a 2.2% FCF yield. You’re paying for a 36% 5YR estimated revenue CAGR and near 50% EBITDA margins (see TIKR estimates below). Is it worth the multiple?

Wrapping Up: Where To Learn More

Thanks for reading, and I hope you learned something. Check out these resources if you want to learn more about Christian, his investment process, and his fund, Curreen Capital:

Enjoy the rabbit hole!