Today we are going to cover our DOTM Strategy (DOTM stands for Deep Out of The Money options) You’ll learn how to use an OTM call option strategy to multiply your market profits.

What is the “DOTM” Options Strategy?

DOTM is short for deep-out-of-the-money. This strategy involves buying cheap calls on bullish stocks. If the stock price makes a strong move higher in a short amount of time, these call options can appreciate in value by many multiples. It’s not out of the ordinary for some of these call options to appreciate 30-50x.

Here’s an example to illustrate the power of DOTM calls.

Back in August of 2017, we issued a buy alert for Interactive Brokers in our MIR report (link here).

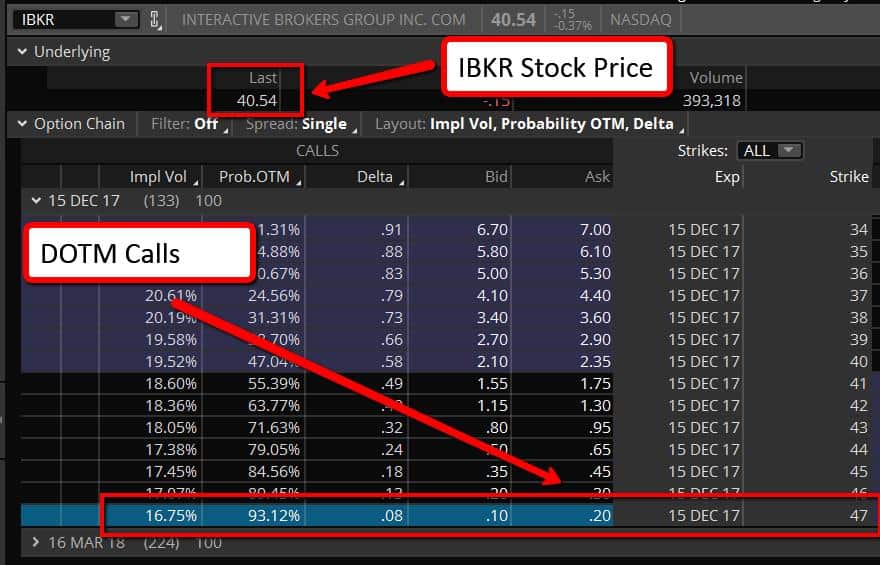

At the time IBKR traded at $40.54.

The December DOTM call options struck at $47 and were trading for just $0.20.

Had you gone out and bought plain IBKR stock at $40.54 you would have done pretty well by the end of the year. By December 15th, IBKR was trading for $60.40. A 49% gain in a few months.

But take a look at the price of the 47 DOTM calls.

Those were trading for $13.00 That’s a 6400% return in a few months. $1,000 invested in this DOTM option would turn into $65,000 in four months time….

That’s a serious difference in return.

What is OTM vs DOTM?

OTM and DOTM are two different approaches to managing and executing trades in the financial markets.

OTM stands for “Out of the Money”, and refers to a type of option where the strike price is higher than the current market price of the underlying asset. These options have a lower likelihood of expiring in the money, and as such, they typically have a lower premium or cost.

DOTM, on the other hand, stands for “Deep Out of the Money”, and refers to options that have strike prices that are significantly higher or lower than the current market price of the underlying asset. These options have an even lower likelihood of expiring in the money, and therefore, they typically have a lower premium or cost compared to OTM options.

OTM and DOTM options can be used in different strategies such as in hedging, speculation, and income generation.

Benefits of an OTM Options Strategy

- Lower cost: Since OTM options have a lower likelihood of expiring in the money, they typically have a lower premium or cost. This can make them a more affordable option for traders who are working with a smaller budget.

- Limited risk: Because the strike price of OTM options is higher than the current market price of the underlying asset, the potential loss is limited to the premium paid for the option. This can be an attractive option for traders who are risk-averse or who want to limit their potential losses.

- Profit potential: While the likelihood of an OTM option expiring in the money is lower, there is still the potential for profit if the market moves in the trader’s favor.

- Flexibility: OTM options can be used in a variety of strategies, including hedging, speculation, and income generation. They can also be combined with other options or securities to create more complex strategies.

- Volatility Play: OTM options can be used to take advantage of volatility. When volatility is high, OTM options become more expensive, and when volatility is low, OTM options become less expensive, thus providing a good opportunity for traders to make a profit.

What is an Example of an OTM Call Option Strategy?

An example of an OTM call option strategy would be if you believe that a particular stock will increase in value, but don’t want to buy the stock outright. Instead, you could buy an OTM call option on the stock.

Let’s say the current market price of the stock is $50, and you buy a call option with a strike price of $55. This means that the option gives you the right to buy the stock at a price of $55, even if the market price is higher.

If the stock’s price increases to $60, then you could exercise your option and buy the stock at the strike price of $55, resulting in a profit of $5 per share.

Here, you are betting that the stock will increase in value, but the strike price is above the current market price, making the option “out of the money”, hence the name OTM option. If the stock doesn’t increase in value and remains at $50 or decreases in value, then you would not exercise the option, and the most you would lose is the premium you paid for the option.

It’s important to note that OTM options have a lower chance of expiring in the money, but also have a lower cost, making them an appealing strategy for traders who want to limit their risk while still having the potential for profit.

What Is Considered A DOTM Call?

A deep out of the money call is an option with a strike price that is far away (25%+) from the current price of the underlying. If you’re familiar with option greeks — DOTM calls are those with a 15 delta or less.

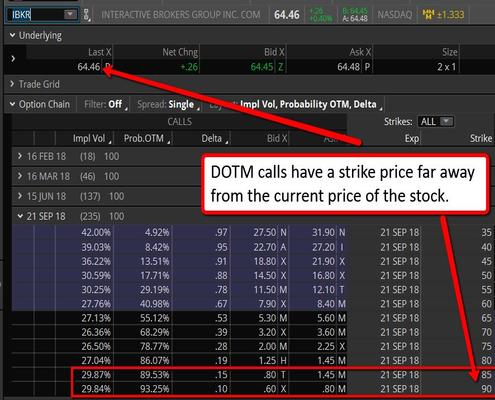

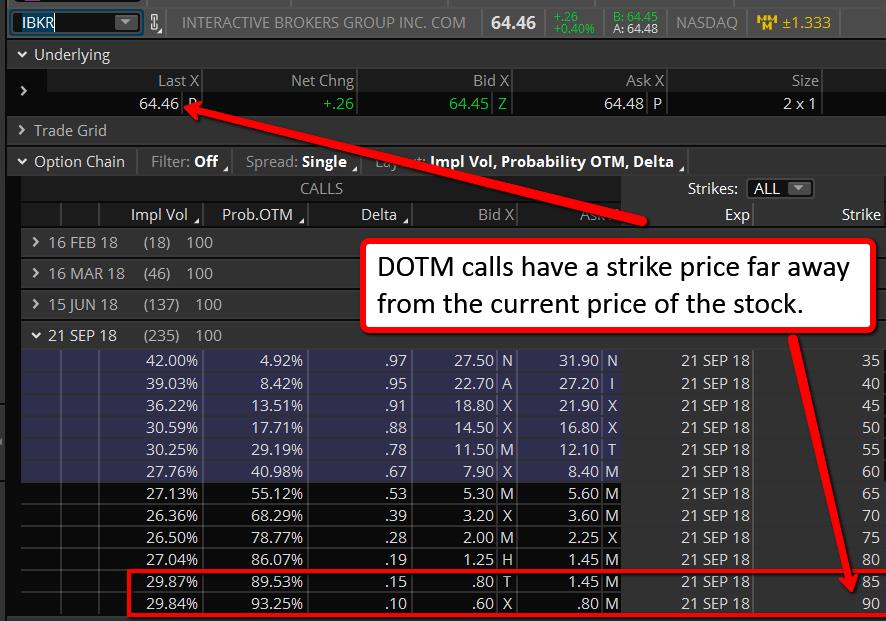

You can see in the example below that IBKR is trading for $64.46. The DOTM calls are the ones with a strike price far away from that value. The red rectangle shows that these are the calls struck at $85 and $90.

Also notice that these calls are much cheaper than the ones closer to the current stock price. The 90 call in this example trades for $.80. The 65 call trades for $5.60 — 7 times more expensive. Buying DOTM calls can be a very lucrative strategy because if we’re right about a stock trending higher these inexpensive calls give you incredible positive asymmetry versus buying ones closer to the money.

Options have a ton of expiries, how far out should you buy?

Selecting the correct tenor (time till expiration) is one of the hardest parts about option trading. We’ve spent years experimenting with different tenors for buying and selling options. After thousands of trades, and lots of time spent researching this, it’s clear to us that the best options for the DOTM strategy are those with 6-18 months left until expiry. Billionaire trader Jim Leitner agrees:

If the option maturity is long enough, trend can take us far enough away from the strike that it’s okay to overpay. ~ Jim Leitner

Short-dated options (1-90 days to expiry) don’t allow enough time for the underlying stock to capitalize on the power of its price trend. Buying these short-dated calls is a losers game because time is not on your side.

The long-dated calls on the other hand allow ample time for a stock to make its full move.

Another benefit of buying long-dated options is the convenience. We can open the trade and then let it sit for half a year or more before worrying about rolling exposure. This makes execution much easier.

Why buy the DOTM calls instead of the stock?

Options take away that whole aspect of having to worry about precise risk management. It’s like paying for someone else to be your risk manager. Meanwhile, I know I am long XYZ for the next six months. Even if the option goes down a lot in the beginning to the point that the option is worth nothing, I will still own it and you never know what can happen. ~ Jim Leitner

Buying a call option defines your risk. The most you can lose on a DOTM call is the amount of premium that you pay. This makes risk management easy. We can know our risk with absolute certainty before placing a trade.

You also avoid the hassle of setting and honoring stops.

A standard stock trade with a stop can be frustrating. It’s common for a quality stock to hit your stop from random volatility and then resume its uptrend without you in it.

By using a call option you don’t have to worry about controlling your risk with stops. The DOTM call does it for you. In a sense, you’re outsourcing the risk management process to the option.

Using DOTM calls also allows you to greatly leverage your capital and amplify returns.

Since 1 call option represents 100 shares of stock you can take on much more exposure for less cash. Let’s run through a quick example.

Let’s say IBKR is trading for $64.46 and our target DOTM call option is trading for $.80

Purchasing 100 shares of this stock would cost $6,446. Replicating the same exposure in the DOTM call option would only require $80 — a fraction of the cost.

We could buy exposure to 10x more shares in the DOTM option for only $800 — still less cash than 100 shares of stock.

The cash savings we get from using the DOTM call option can be used for other trades or put into short-dated government securities to earn an additional return.

What are the downsides of using DOTM calls over stock?

Every trading vehicle has its downsides and DOTM calls are no exception. DOTM call holders are not entitled to dividends. If the company pays a dividend, only stock owners will receive that distribution.

DOTM call holders can also lose 100% despite a mild rally in the underlying stock. If the stock chops around and finishes lower than the strike price of the DOTM call it will expire worthless.

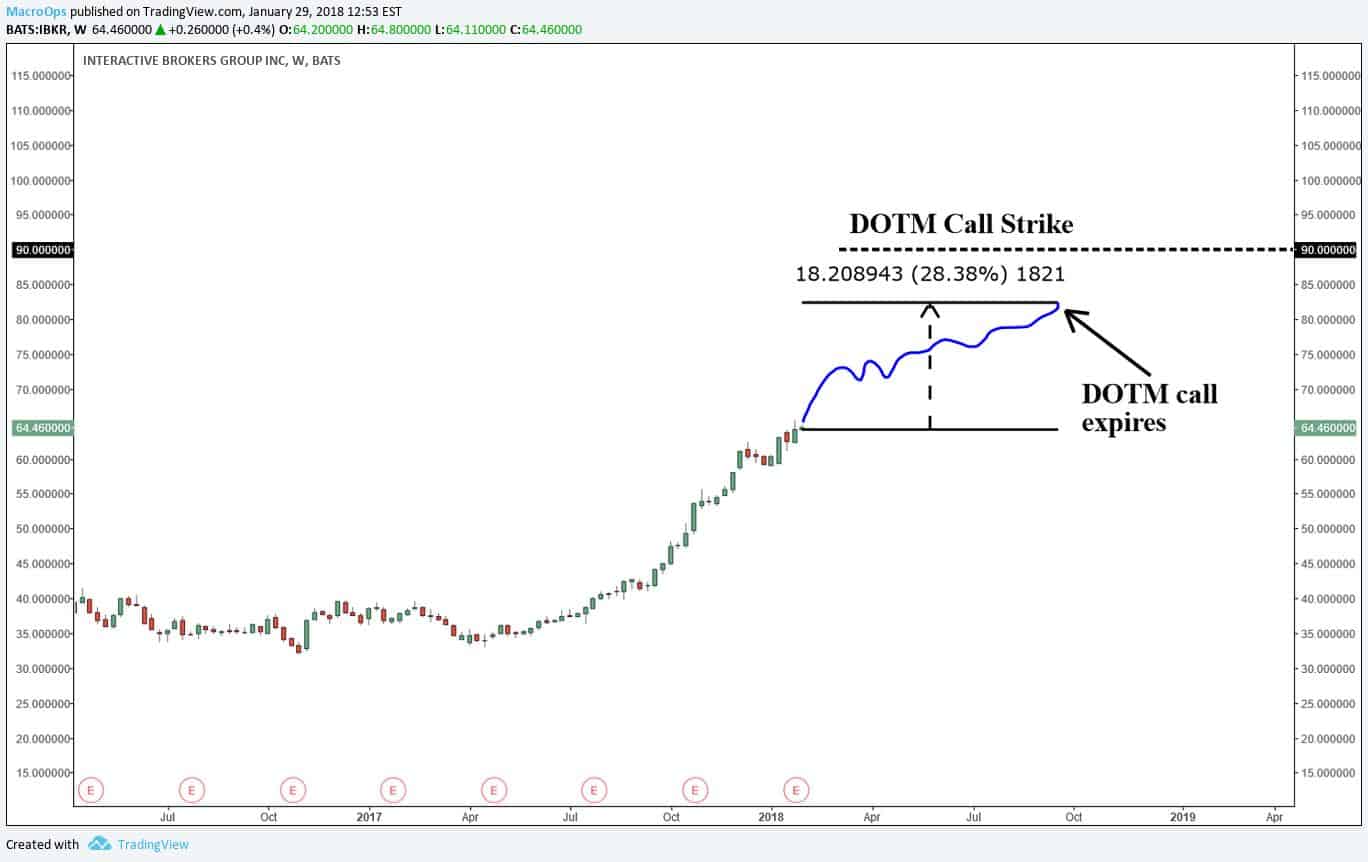

In the example below, IBKR traveled up 28.38% by the time the DOTM option expired. But because the strike on the DOTM call was at $90 (above the current price of the stock) the option expires worthless.

In this situation the stock owner would have a 28.38% gain while the DOTM call holder would have a 100% loss.

Can this strategy be executed on any stock that has a bullish outlook?

No, not all stocks have liquid DOTM call options with 6 months or more until expiry.

Market makers only list options on underlyings that have a lot of public interest. These companies will usually have a market cap of $10 billion or higher.

What’s the ideal trade/investment case for this strategy?

Every play has its own nuances but here are the three primary things we like to see before placing a DOTM trade.

-

- Stock has strong positive price momentum (ie, bullish trend)

- Stock has a great fundamental narrative supporting the strong trend

- Option volatility is moderately priced (20-50% implied volatility reading)

How do you size a DOTM options trade?

Sizing depends on the individual’s risk tolerance. In the Macro Ops portfolio we usually put anywhere between 0.5%-1.00% of our portfolio into one DOTM option.

Why does this strategy work, what is the theory behind it?

The Black-Scholes model assumes that all stocks have an equal chance of going higher as they do lower. The math behind Black-Scholes implies that trends don’t exist and that day to day fluctuations are random.

Take a look at the probability distribution for April calls on Apple stock, below. The pink shaded area represents the likelihood that Apple falls into that particular price range by expiration. You can see that it’s a fairly symmetrical bell curve. The amount of shading on the right is about the same as the amount to the left. Also note that the market implied forward price is right near the price that Apple was trading at the time of this snapshot (October 30th, 2017).

Now let’s say we believe Apple actually has positive price and fundamental momentum. We believe trends exist and that Apple will continue its uptrend over time. If our assumption is true, the probability of the stock moving higher than it is today is much greater than what the above distribution implies.

The correct distribution should instead look something like this.

The red shading represents the probability of Apple reaching those prices if we assume that the current trend persists. The difference between the red and the purple areas are what we call edge.

The market is implying a low probability of higher prices while we think the likelihood is significantly higher. We can buy the DOTM calls in this situation and show a profit over time.

Also, notice that the “custom” forward price is higher than the market implied price. The option market always assumes no trend — and in this hypothetical example, we think otherwise.

It’s important to understand that these edges, i.e. the discrepancy between the red area and the purple area, are more likely to occur in options with more than 6 months left to expiry. Long-term momentum is a factor that the options market regularly ignores.

Who on Earth is selling these cheap call options to us?

Whenever you’re trading derivatives it’s important to understand the psychology and reasons behind the other side of your trade. Derivative trading is a zero-sum game. One side needs to lose for the other side to win.

So who’s willing to sell us DOTM calls that have the potential to 50x?

Option market makers.

A market maker’s goal is to collect the bid ask spread on an option’s price. They aren’t in the business of guessing what the final value of the option will be. They don’t want risk associated with movements in the underlying stock.

To protect against this risk they do something called “delta hedging.” Delta hedging offsets the directional risk of an option. When market makers sell DOTM call options they delta hedge them by buying stock. As the underlying stock trends higher and higher they buy more and more stock to offset directional risk.

At the end of the trade they are left with a really large loss on their short call but at the same time a really large gain on their long stock hedge. The two P&Ls cancel each other out and the market maker is left with the tiny gain from the original bid/ask spread.

The real “losers” in this trade are the market participants selling their stock to the market maker who’s delta hedging. These sellers of stock missed out on a nice bull trend.

~~~~~~~~~~~~~~~~~~~~~~~

If you’d like to learn more options strategies, including how to use options to bet on volatility, check out our free Options guide here.