Hextar Global (HEXTAR) engages in the manufacturing, formulation, repackaging, distribution, and agency of agrochemicals in Malaysia and internationally.

HEXTAR is a classical good co./bad co. investment idea. The company stumbled out of the gate after IPO’ing in 2009. There are three reasons the business underperformed. First, their products weren’t competitive. Second, they had a weak brand name. Third, they over diversified (read: di-worsified) into too many business segments.

The company shifted tone in 2017, selling its property development business and discontinuing its horticulture business in 2019. The company lasered its focus on its best (and fastest-growing) business segment: agrochemicals.

In 2019, then Halex bought Hextar Chemicals Limited (HCL). Halex changed their name to Hextar Global and drew a proverbial line in the sand. They would compete in the agrochemicals business without distraction.

This comes at a time when food security and agriculture is of utmost importance to both developing and developed nations. HEXTAR has strong tailwinds and a long runway for growth. Past financials don’t show the company’s optimistic (and profitable) future.

Most of the initial leg-work research was from Buy Call’s blog post (you can read here).

The Bull Thesis: Leading Crop Protector in Malaysia

Hextar is well-positioned to benefit from the ever-growing demand for secured food. The company controls 30% of the herbicide/pesticide market in Malaysia. And with their HCL acquisition, the company’s perfectly positioned to capture more market share in the coveted Indochina regions.

Buy Call’s blog mentioned four main drivers of value creation:

1. Malaysian & Indonesian Market

Indonesia is the largest producer of palm oil in the world, followed by Malaysia. Both countries account for 84% of the world’s palm oil production.

HEXTAR’s agrochemical business supplies palm oil growers with much-needed fertilizer and crop protection.

The company won a contract award with Sime Darby Plantation to supply the grower with agrochemicals in Malaysia, Papua Guinea, and the Solomon Islands.

Indonesia is in the process of replanting ~2.8M hectares of palm oil trees. Replantation programs take years to implement and offer HEXTAR a sustainable, SaaS-like recurring revenue.

2. Distribution Agreement with Sumitomo Chemical Vietnam

Agriculture is vital to Vietnam’s economy as it is a large exporter of agricultural products. Main export crops include rubber, rice, and coffee (commodities we use every day).

HEXTAR signed a Distribution Agreement with Sumitomo Chemical Vietnam (SCV) in October 2020. The agreement gives HEXTAR exclusive herbicide distribution in Vietnam for the next five years

3. Improvement in Commodity Prices

Like any agrochemical company, HEXTAR is an indirect call-option on the underlying price of its major commodity. In HEXTAR’s case, that’s palm oil and rubber.

The higher the commodity price, the better it is for HEXTAR’s business. This makes intuitive sense. Higher commodity prices incentivize growers to increase production as they generate higher yields (read: margins) on their crops. This increases the demand for HEXTAR’s agrochemical herbicides and pesticides.

4. Call Options on Agriculture Technology

HEXTAR has two call-options on the future of “AgTech”:

- Drone sprayers: Drone sprayers offer myriad advantages to human/tractor spraying, including:

- High-pressure spraying, efficient use of chemicals, more uniform spraying, reduced pesticide waste

- Biogas Engineering: Through its acquisition of Biogas Engineering Sdn Bhd, HEXTAR can harvest and convert methane gas from palm oil production and turn it into usable energy.

Malaysia’s Agrochemical Industry: High Regulation = High Barriers

Herbicides and insecticides are the two largest components of Malaysia’s pesticides sector. As we mentioned earlier, palm oil is the biggest crop in both volume and dollar value.

In 2019, Malaysia spent roughly RM 4B in agriculture expenditures.

Malaysia’s pesticide business is heavily regulated and thus prone to high barriers to entry. This is great for HEXTAR and its minority shareholders. The reason for the high barrier to entry is Malaysia’s Pesticides Act of 1974. The Act “ensures that companies dealing with pesticides obtain licenses from the Malaysia Pesticides Board and that pesticide products are both properly labeled and packaged and as effective and safe as they claim to be.”

To commercially market and sell pesticide products in Malaysia, companies need to obtain approval for product registration. This can take two years (depending on product type).

That sounds like a headache for a new pesticide company to voluntarily enter.

Since agrochemicals detract competition, there are only two ways the few players can gain an edge:

- Having the best product (quality)

- Having the best branding (consumer mind-share)

Think of Scotts Grass Seed. I have never used Scotts Grass Seed. But when I think of grass seed I think of Scott’s (SMG). That’s a powerful advantage over the competition. Why? Because there could be a better product on the shelves. But if I don’t notice (or care to notice) it doesn’t matter.

With the HCL acquisition, HEXTAR is well-positioned to capture the lion’s share of this uncompetitive market.

HCL: A Strong, Value-Add Acquisition

Halex bought HCL for RM 569M and changed its name to HEXTAR Global. The company split the payment between 97% stock issuance and 3% cash.

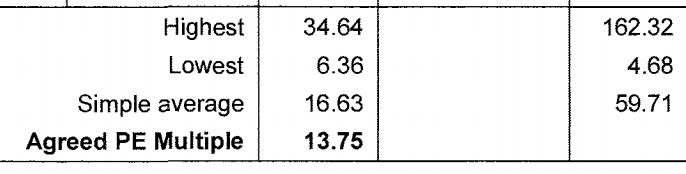

HEXTAR paid 13.75x HCL’s 2017 earnings. HCL generated RM 325M in revenue and RM 43.4M in earnings (13% net margin).

Between 2015 and 2017 HCL grew revenue at a 17.53% CAGR and net income ~32% CAGR. That’s a 0.43x PEG ratio purchased by HEXTAR. Not bad.

Management got a great price for a great business. The company paid ~37% discount to the average PE multiple for comparable companies (see table below):

PE ratios ranged between 6.36x and 35x.

This was the result of HEXTAR’s long-standing efforts to reorient its business to what they do best: agrochemicals.

The combined company creates one of the strongest agrochemicals businesses in Malaysia and Indochina. For example, before the deal, HEXTAR sported 96 agrochemical products that they exported across 5 countries (Singapore, Vietnam, Taiwan, Pakistan, and Bangladesh).

The combined company creates one of the strongest agrochemicals businesses in Malaysia and Indochina. For example, before the deal, HEXTAR sported 96 agrochemical products that they exported across 5 countries (Singapore, Vietnam, Taiwan, Pakistan, and Bangladesh).

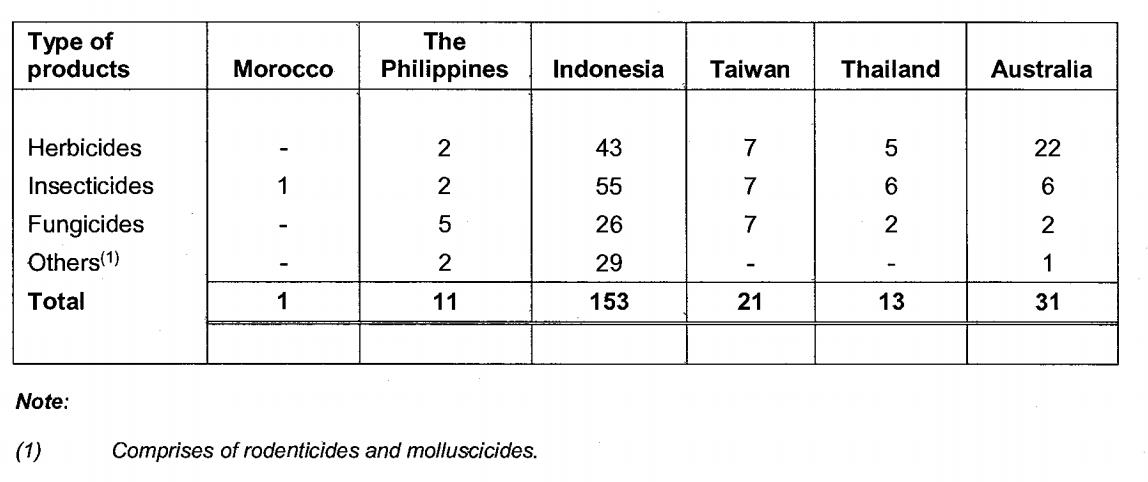

HCL is an entirely different beast. The company has successfully registered 249 agrochemical products and they export to >30 countries across the Asia Pacific, the Middle East/Africa, Latin America, and Australasia. Since 2015 the company has expanded exports to include New Zealand, Spain, Turkey, and Morocco.

HCL’s acquisition completely transforms HEXTAR’s financial statements. This is something algos and screeners won’t find. Again, backward-looking data won’t help the investor. Here’s what I mean.

HCL’s acquisition completely transforms HEXTAR’s financial statements. This is something algos and screeners won’t find. Again, backward-looking data won’t help the investor. Here’s what I mean.

Between 2015 – 2017, HEXTAR (pre-HCL) went from RM 125M in revenue to RM 69M. During the same time, they grew net losses from RM 0.368M to RM 11.9M.

Now compare that to HCL’s business:

- Revenue growth from RM 234M to RM 324M

- Profit after tax (PAT) growth from RM 25M to RM 43.4M during the same time frame.

How HEXTAR Captures Long-Term Value From HCL

The acquisition allows HEXTAR to merge its existing agrochemicals business into HCL’s (much better) one. In doing so, management believes the “old” agrochemical business can resemble that of HCL. Here’s why (via merger announcement):

- Old business (Halex) leverages HCL’s customer network in >30 countries. This allows HEXTAR to cross-sell their “old” agrochemical products to HCL’s existing customers.

- Plug into HCL’s extensive R&D capabilities to create new value-added services like spectrometer analysis and product registration.

- Benefit from economies of scale and operational synergies via production processes and capacity, R&D investments, and general administrative functions.

The now larger company also benefits from better-negotiated prices from suppliers and customers for raw materials. But is this true? Did HEXTAR see those coveted synergies?

Narrative To Numbers

I’m skeptical whenever companies do large acquisition deals and promise “synergies” and “economies of scale”. Yet HEXTAR walks the walk. The benefits of the HCL purchase flow through to the income statement.

For example, check out the company’s last five consecutive quarterly revenue growth figures:

- 8%

- 4%

- 7%

- 5%

- 8%

Increased revenue from HCL’s core business? Check.

Next, let’s see if the company’s gained synergies. If this is true, we’d see it in gross margin expansion as the company grows revenues (I.e., administrative spending consolidated, R&D investments via one channel, etc.).

Since the acquisition in April 2019, HEXTAR’s increased Gross Margin 600bps (16% to 22%) and operating margin 300bps (from 10% to 13%).

Here are HEXTAR’s thoughts on the acquisition in their 2019 annual report (emphasis mine):

“In overall, the Group had on 30 April 2019 witnessed a tremendous corporate milestone to solidify its position as a leading and the biggest producer of agrochemicals in Malaysia. The business combination had given the Group the ability to enhance the competitiveness in agrochemical business by increasing product range and extending distribution network especially the presence in the new markets”

So far management’s walked the walk and talked the talk.

The New HEXTAR: Leading in Agrochemicals w/ Call Options

HEXTAR has three business segments:

- Agrochemicals

- Consumer products

- Smart Agriculture

The company’s Consumer Products segment makes disposable healthcare products like wipes, tissues, and cotton-based products. This segment burned almost RM 8M in operating losses in 2018. In 2019 they only lost ~RM 2M on RM 26M in revenue. Over time as the company consolidates from two plants to one, we should see Consumer Products turn PAT profitable.

Smart Agriculture involves HEXTAR’s investments in drone technology and 5G agriculture.

For our purposes, we won’t cover these investments and assign a $0 value to this segment in our valuation.

Whether this segment is worth $0 is up for debate (highly unlikely).

Valuation: Buy One, Get Two Free

With HEXTAR you can pay for the agrochemicals business and get its two other segments (Consumer Products and Smart Agriculture) for free.

The best way to value HEXTAR is on an Agrochemicals basis only. Anything else we get for free is a cherry on top.

We’ll start with 2019 revenues of RM 322M. The company’s estimated to end FY2020 with RM 400M in revenue (20% growth). From there we’re assuming an average revenue growth of 13% to get RM 590M by 2024 (~1.5x 2024 Sales).

Over time, HEXTAR’s gross margins should resemble HCL (~22%-23%). This gives us RM 136M in gross profit. Operating expenses have averaged 8-9% in the last few quarters. Staying with that trend gets us RM 83M in EBIT by 2024 (9x EV/EBIT), RM 75M in pre-tax cash flow, and RM 60M in PAT.

Adding back D&A, NWC, and subtracting cap-ex gets us ~RM 70M in free cash flow (10% FCF yield).

At 10% FCF yield, HEXTAR passes the Bill Miller test of buying companies at >7% FCF yields (S&P average).

Risks

- Customer Concentration

HCL has a high customer concentration. As of 2017, its top four customers accounted for 29% of revenue. Losing one (or a few) of these customers will have heightened negative consequences to the top-line.

- Foreign Exchange Risks

HEXTAR imports most of its raw materials which are denominated in USD.

- Commodity Prices

This is a given in any agriculture-related business. Lower palm oil and rubber prices will harm the company’s revenues, margins, and profitability.

- The impression of Herbicide / Pesticide Products

Scan any Whole Foods and you’ll find droves of people armed with pitch-forks to defeat having pesticides in their food. In short, the organic movement is sweeping the nation. Organic markets remain a niche category in Malaysia/Singapore.

Said another way, it’s not big enough to worry about it for the next 5-10 years. There’s also a great PDF for anyone interested in the Malaysian organic food market. Read it here.