GoodRX (GDRX) filed their S-1 earlier this week. I read It so you don’t have to (but you should). Here’s a thread on what I found interesting, fascinating and down-right incredible from the company. I’m starting at zero. Follow along here.

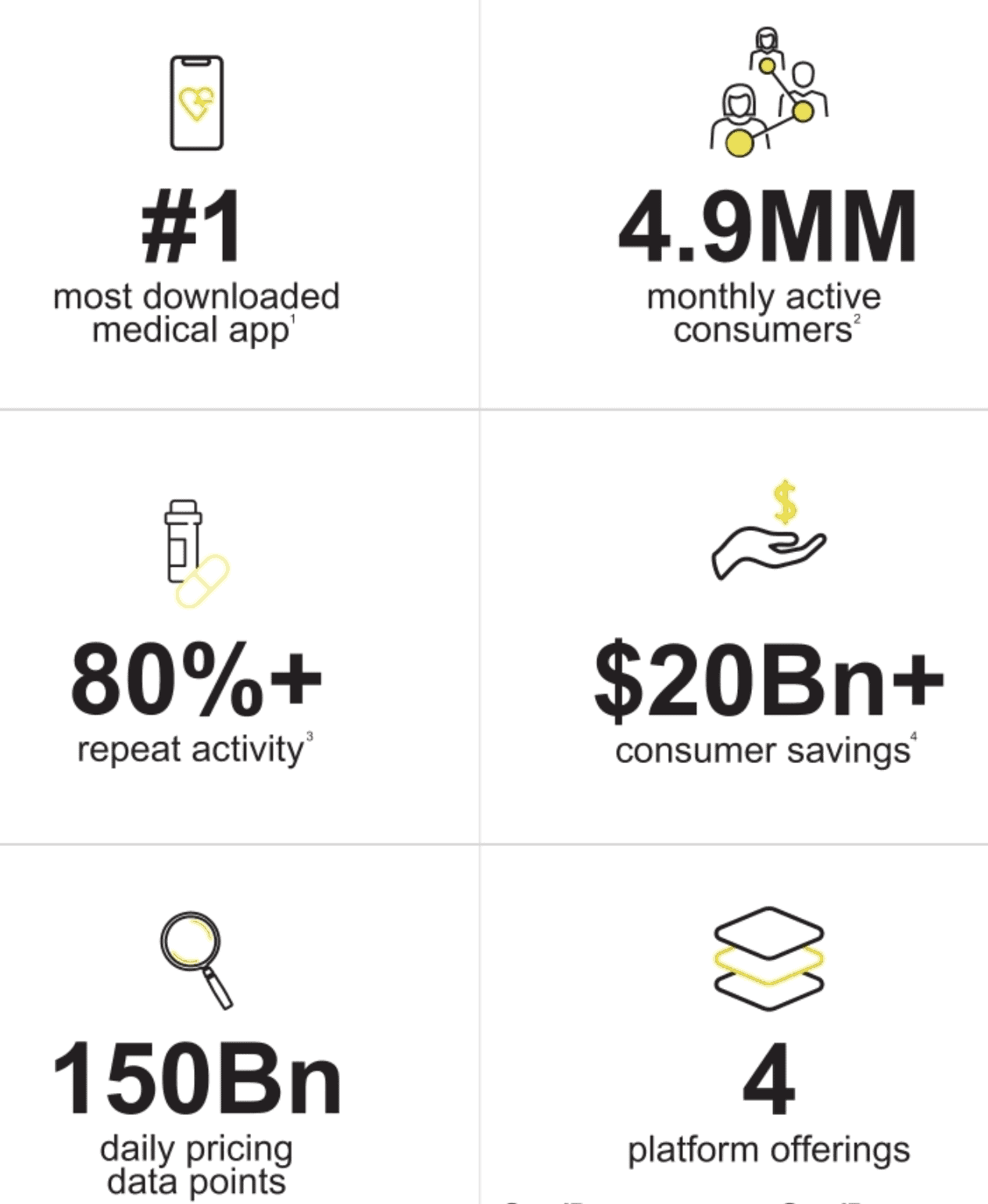

GDRX Facts & Figures

- #1 most downloaded medical app

- 4.9M Monthly Active Users

- 80%+ Repeat Activity

- $20B+ in Consumer Savings

- 150B daily pricing data points

- 4 platform offerings

- Est. Market Cap: ~$9.9B

Business Overview

Mission: To help Americans get the healthcare they need at a price they can afford.

So far it’s working (really) well.

The company estimates 18M of their customers could NOT have afforded to fill their Rx without the company’s savings tools.

How GoodRX Makes Money

Receives fees from partners, which is mostly Pharmacy Benefit Managers (PBMs) when customer uses GDRX code.

Fees are % of fees that partners earn OR a fixed payment per transaction.

Recurring nature to GDRX model as code is saved to consumer profile.

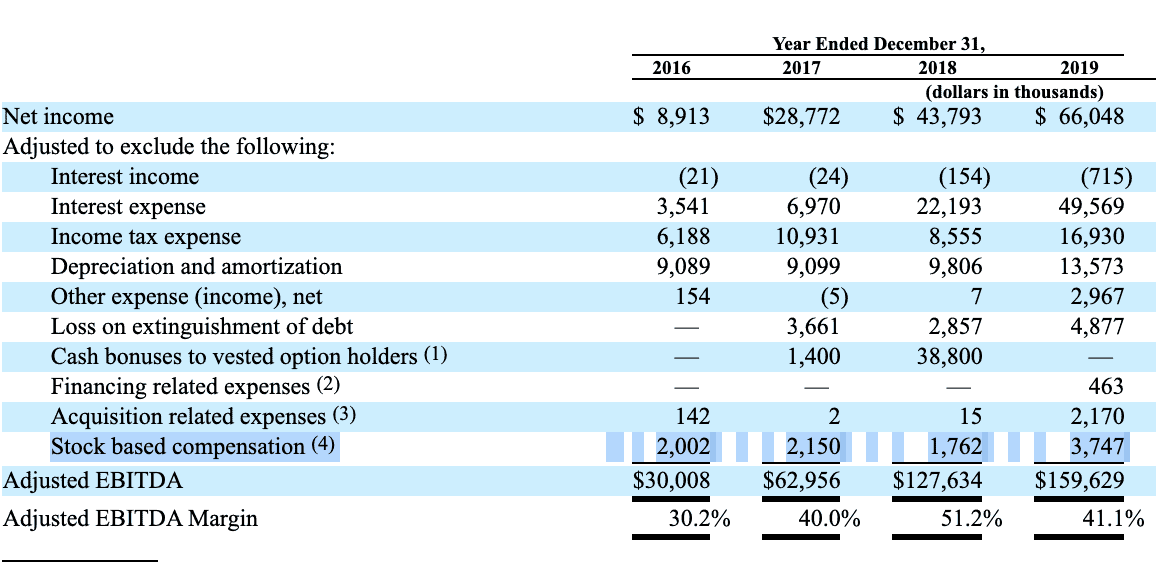

Financial Results

- GMV via prescription offering: $2.5B

- Compounded annual revenue growth rate: 57% since 2016

- Generated $388M Revenue in 2019

- Generated $66M Net Income in 2019

- 2019 Adj. EBITDA: $160M

Solving Healthcare Consumer Issues

GoodRX notes 5 major healthcare consumer “lacks” in its S-1:

- Lack of Consumer-focused solutions

- Lack of Affordability

- Lack of Transparency

- Lack of Access to Care

- Lack of Resources for Healthcare pros

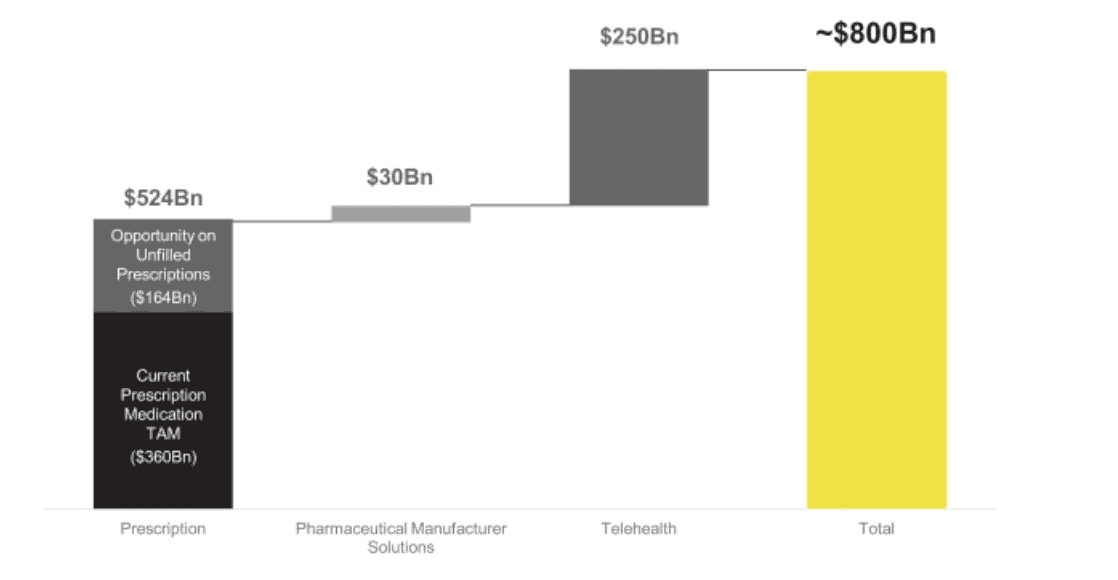

GDRX Total Addressable Market

GoodRX estimates their TAM around $800B. That’s a HUGE number.

Here’s how it breaks down:

- $524B Prescription Care

- $30B Pharma manufacturer solutions

- $250B Telehealth

Initial Surprises: Telehealth is nearly 32% of TAM

The GoodRX Value Proposition

It’s the coveted win-win-win:

– Consumers: Simpler, more affordable Rxs

– Healthcare Pros: Increased medication adherence and greater price transparency (also links w/ EHR)

– Healthcare Co’s: Reach & provide affordable solutions (Rxs) to customers

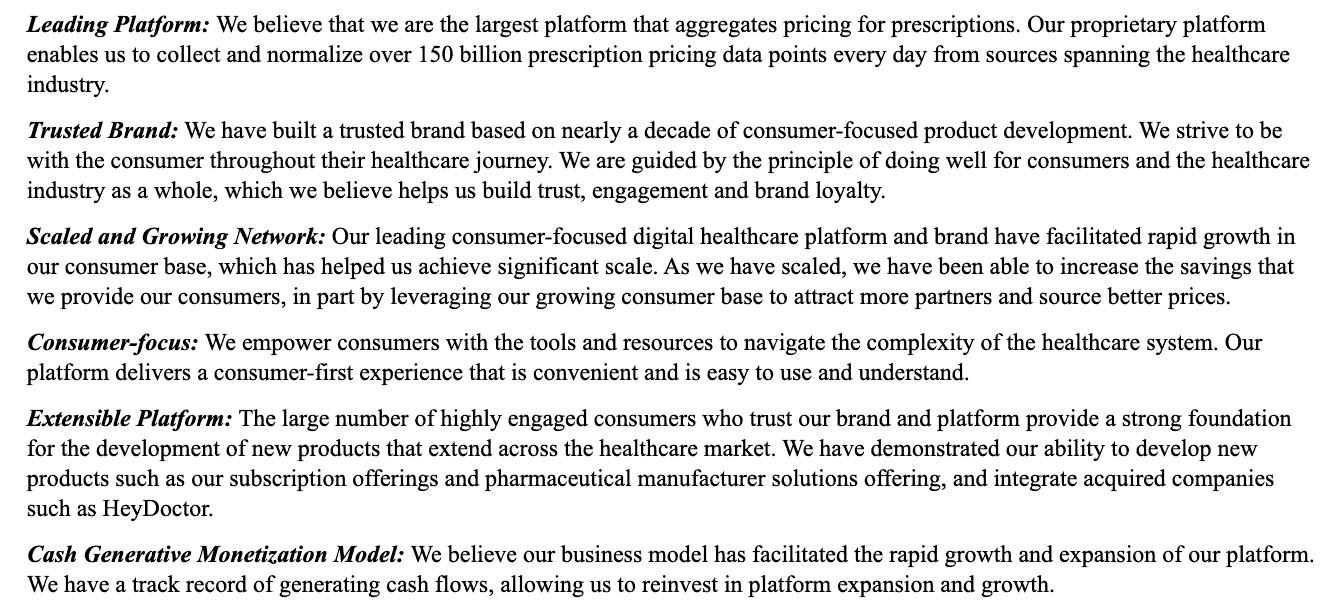

What Makes GoodRX Different

There’s six strengths that reinforce GoodRX’s powerful network effects:

- Leading platform

- Trusted Brand

- Scaled & Growing Network

- Consumer-focus

- Extensible Platform

- Cash generative monetization model

See image for descriptions…

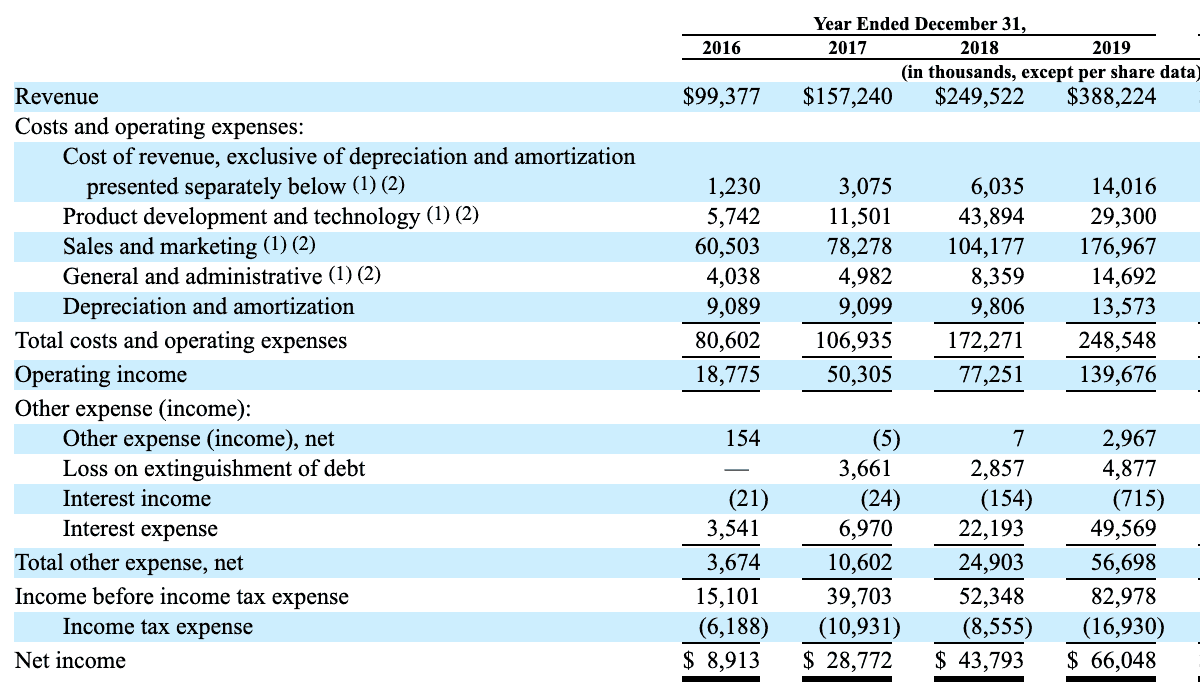

Analyzing Income Statement

– GDRX grew revenue from $99M in 2016 to $388M in 2019 (crazy growth)

– Biggest operating expense currently: SG&A, which was 46% of revenues last year

– Operating Margin: 36% (real nice)

– Pre-Tax Earnings: $83M (21% margin)

– EPS grew from -$0.11 to $0.19 in four years (w/ growing share count)

– 2019 EPS of $0.19 is computed using weighted average shares post-IPO.

– Six-month ended YoY: $0.09 vs. $0.15 in 2020 on $15M more income

– SBC: <1% of revenues

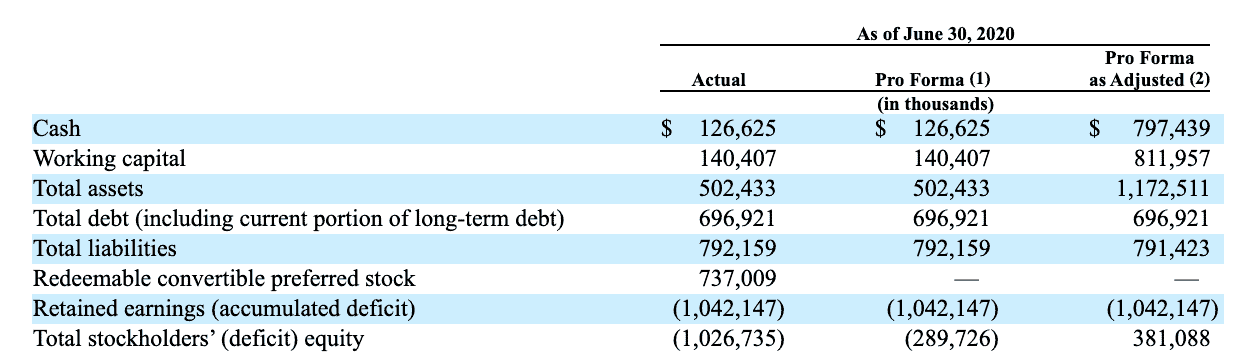

Analyzing Balance Sheet

– $126M in actual cash

– If you adjust for the pro-forma IPO, they get nearly $800M in cash

– Total Debt (incl. LT debt): $700M

– Total Est. Capitalization: $1.078B

– Financed Biz via Cash from Ops (crazy, right?)

See breakdown below …

(Debt & Contractual Obligations)

- <1YR: $41M

- 1-3YR: $85.6M

- 3-5YR: $82.7M

- >5YR: $711M

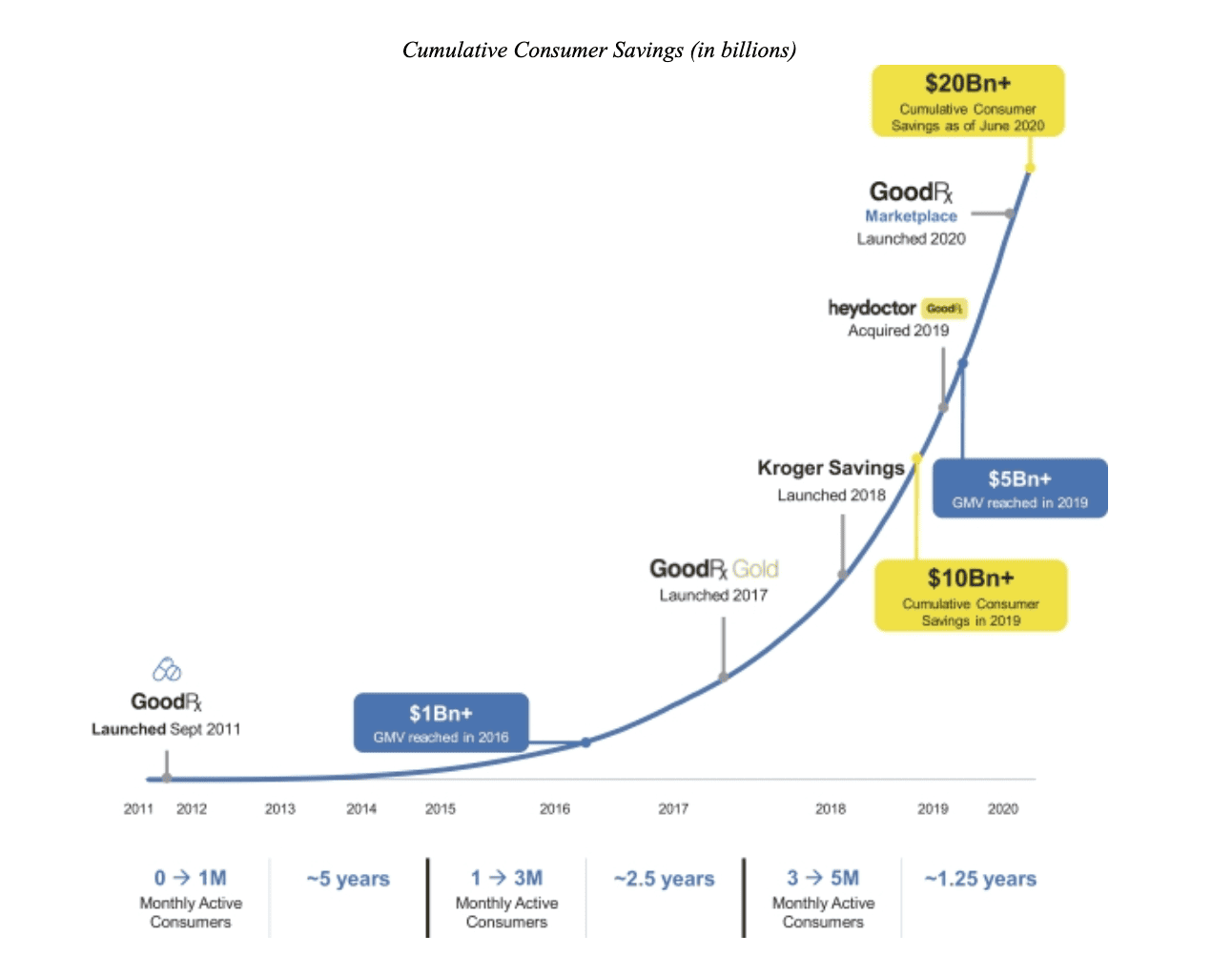

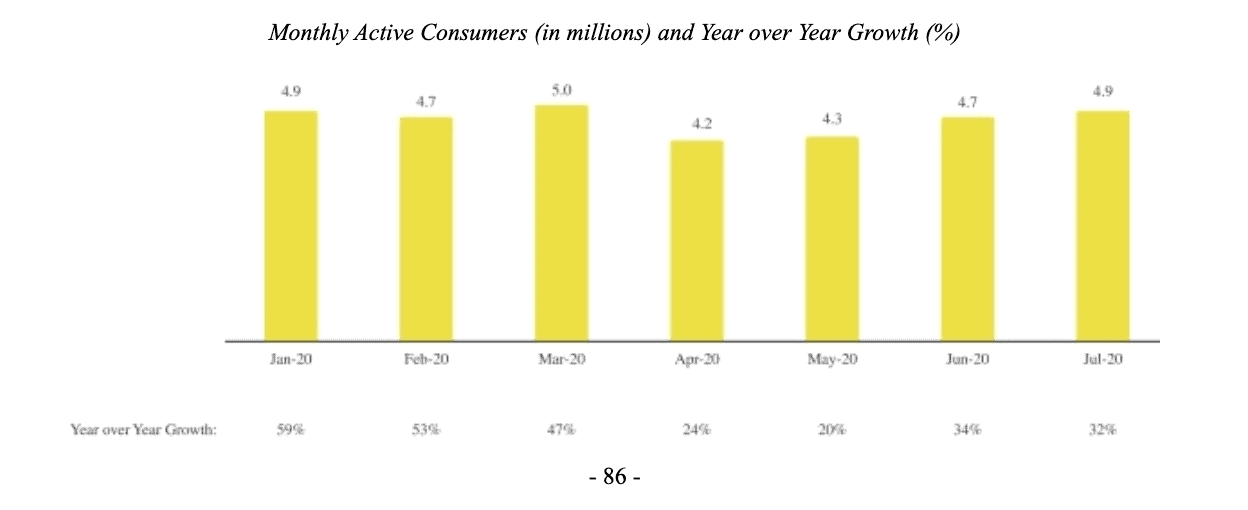

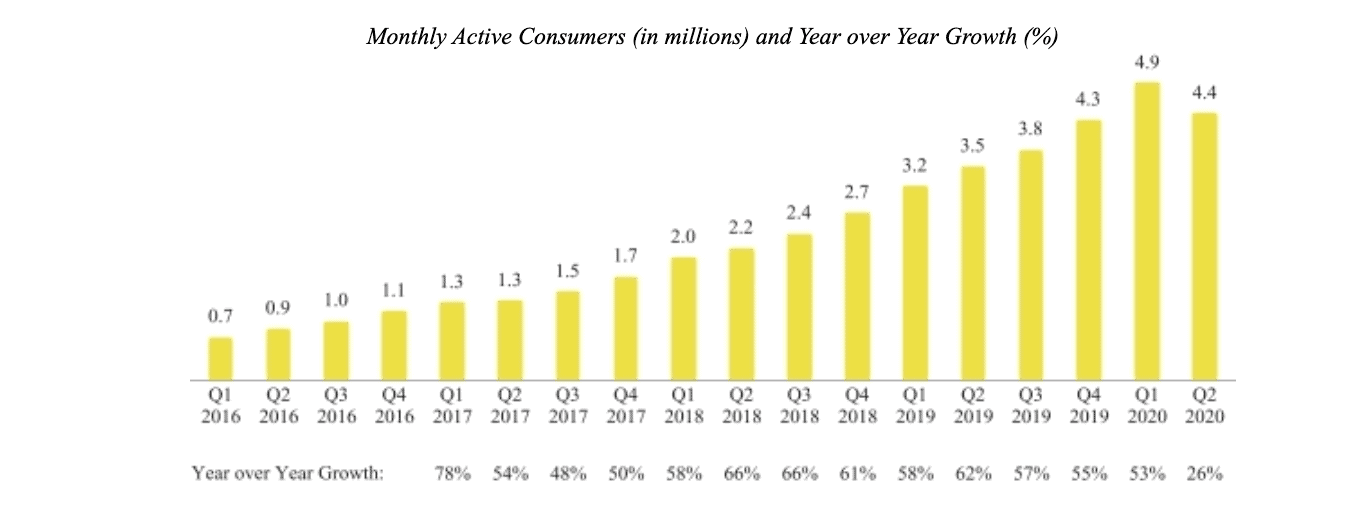

GDRX Key Operating Metrics

One of the most important KPI’s to measure for GDRX is Monthly Active Users (MAU).

GDRX’s MAU trend is absolutely incredible:

– 2016: 718k

– 2017: 1.28M

– 2018: 2.02M

– 2019: 3.18M

– 2020: 4.88M

Where Will Future Growth Come From?

GDRX outlines 3 ways to grow revs outside Rx codes:

– Subscription offerings: Gold, Kroger Savings

– Pharma Manufacturing Solutions: Provide low-cost solutions to expensive brand-name meds

– Telehealth: Online visits / marketplace

Recap: How To Track GDRX Bull Thesis

– Monitor MAU growth & Repeat Activity

– Size + Strength of Healthcare Partner Network

– Growth of Platform & Telehealth

Meet The Founders (Letter Analysis)

– Making healthcare easy is *crazy* hard

– Consumers (insured or not) needed tools to help

– Reduce cost of nearly every generic drug by >70%

– Prices are less than typical insurance

Thinking About GDRX Valuation

At the current estimated IPO price and shares, GDRX will trade roughly:

– 25x 2019 Revenues

– 62x 2019 EBITDA

– 119x 2019 Pre-tax Profits

They’re also growing 57% compounded since 2016.