“Probability is not a mere computation of odds on the dice or more complicated variants; it is the acceptance of the lack of certainty in our knowledge and the development of methods for dealing with our ignorance.” ~ Nassim Taleb, Fooled By Randomness

In this week’s Dirty Dozen [CHART PACK], we talk about a housing bust in the southern hemisphere, large stock inflows, a secular peak in market multiples, reiterate our long-term bull case for precious metals, and end with a look at which sectors are leading relative EPS trends, plus more…

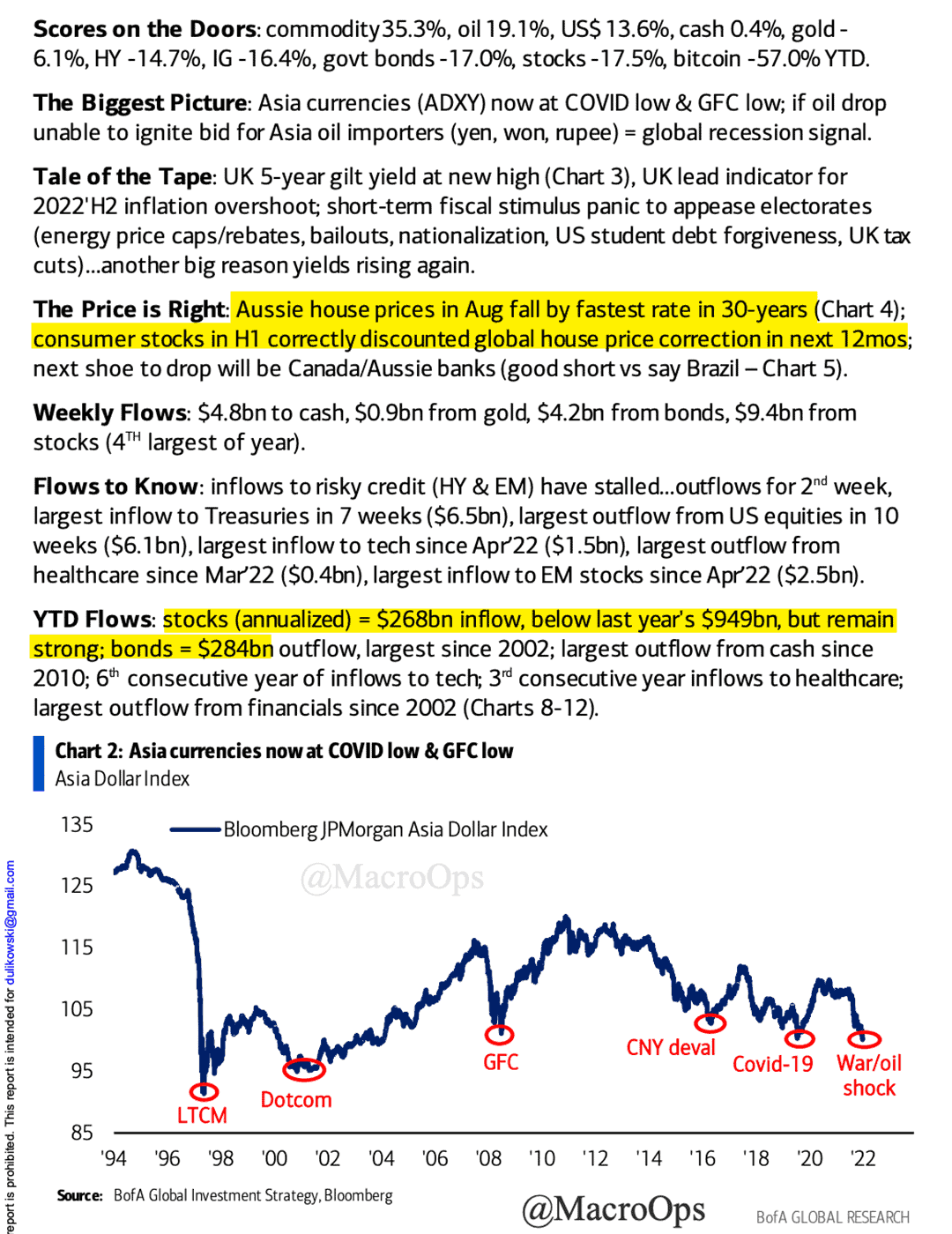

- This week’s summary of BofAML’s Flow Show (emphasis by me).

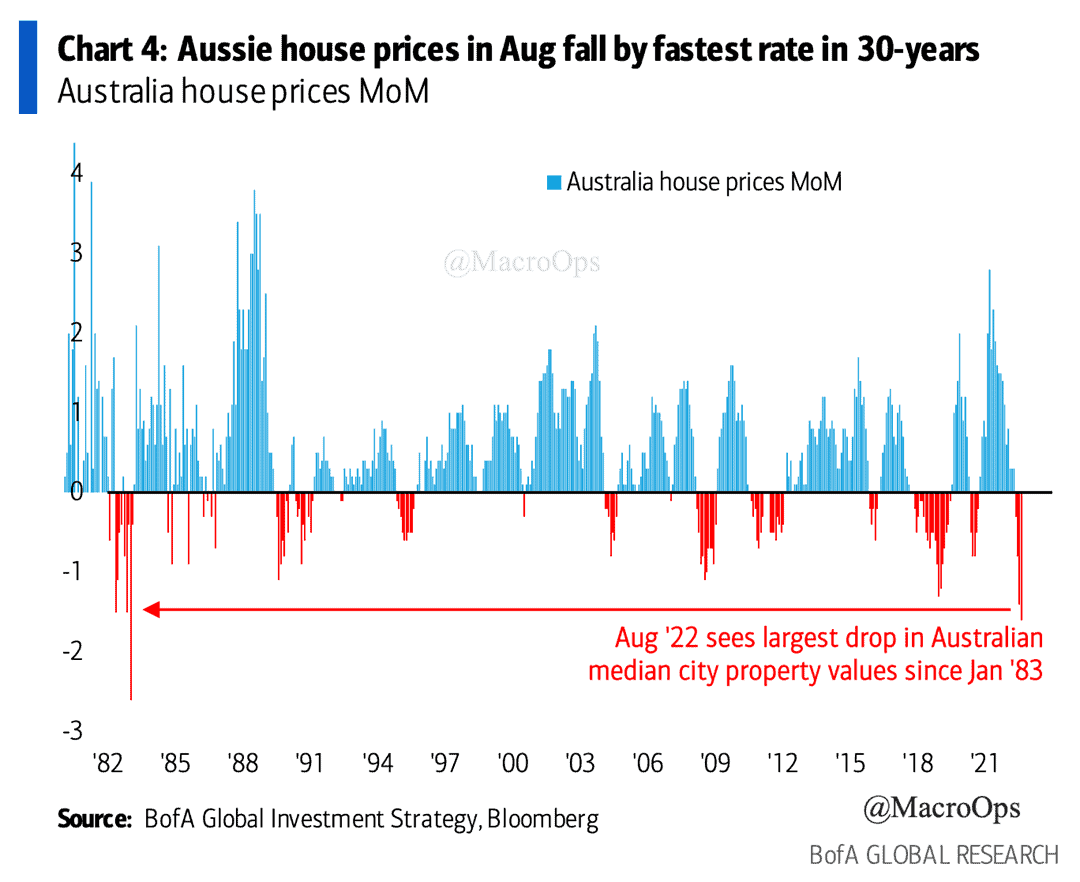

- Home prices down under are going under at their fastest rate in 30 years. I remember all the way back in 2015/16 when a cottage industry sprung up within macro Twitter, where punters were clamoring to out bearish one another on the “unfolding housing bust” in Canada and Australia.

Turns out they might not have been wrong after all, just a weee bit early. Hope they still have those shorts on ;).

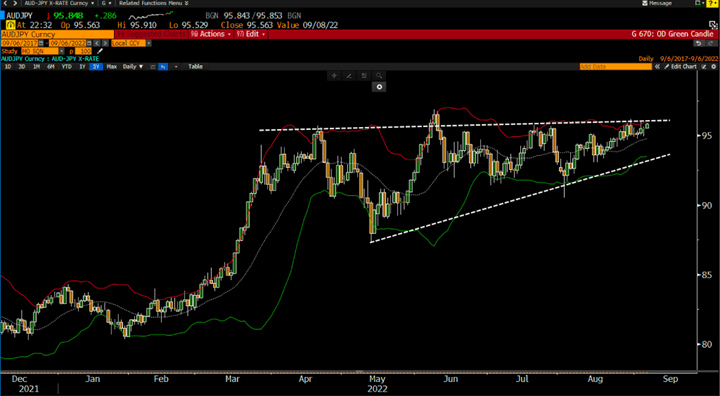

- Despite falling home prices, the AUDJPY pair looks like a nice long. Granted, every DM currency looks like a good long against the JPY.

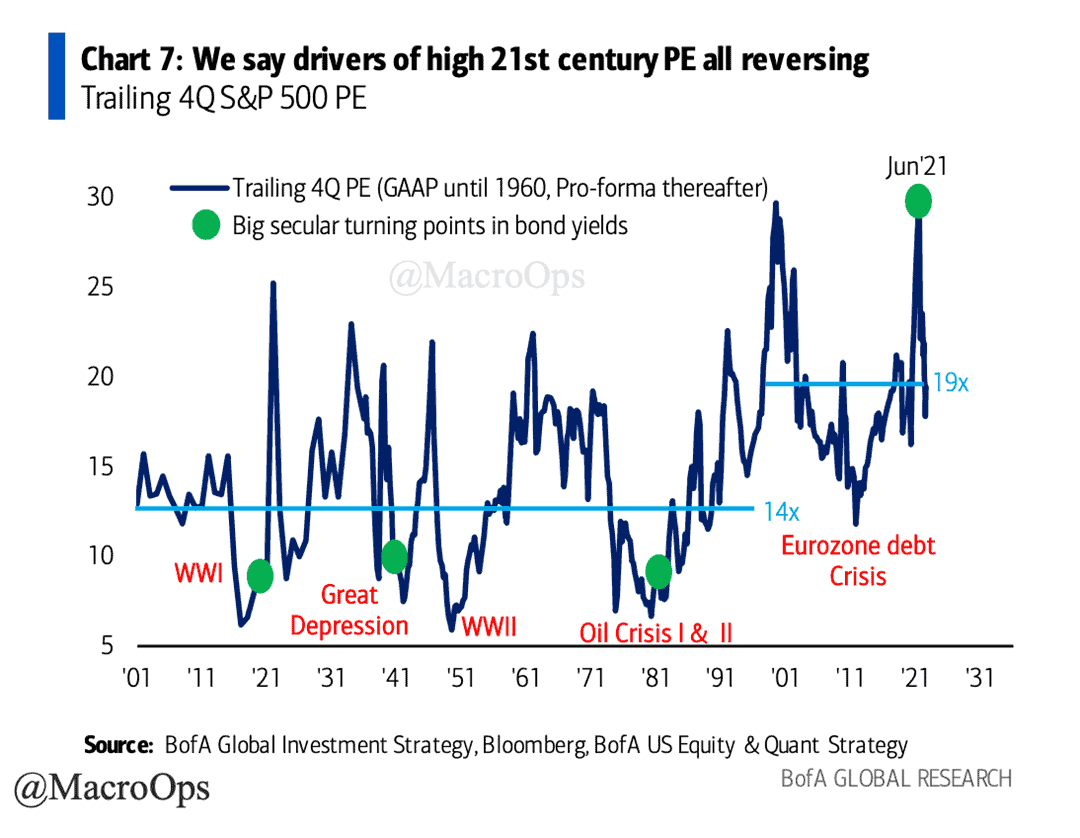

- This chart from BofA shows the SPX’s TTM PE over the last 120 years. Their argument is that the market’s multiple has been high for the past 30 years due to secularly declining inflation and interest rates. And now that these are turning up, we should see multiples compress to their longer-term average range.

- I’m sympathetic to this view though I’m not anchored to anything in this environment. Everything is too path dependent, and so much of what matters in these markets comes down to impossible to forecast variables (Chinese monetary & fiscal policy, winter weather and energy demand/supply, DM policy responses to everything and anything, etc.).

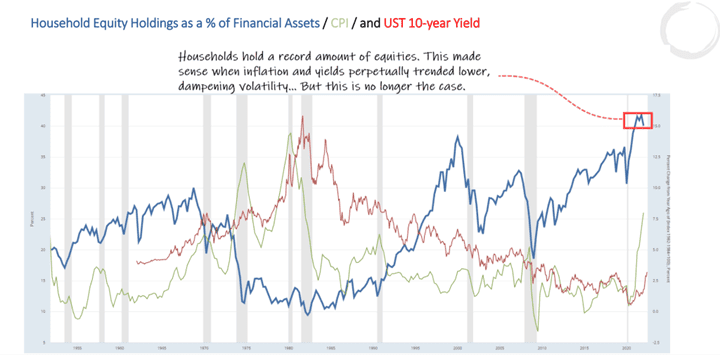

This chart mirrors the one above. And if you believe we’ve crossed high noon of the long-term debt cycle (which I do), then you’d expect the mix of financial assets held by households (which is essentially another way of saying that you expect inequality to come down) to start swinging the other way over the next decade or two.

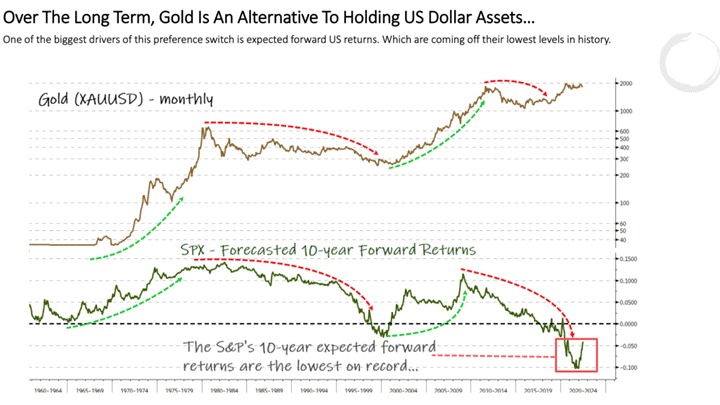

- I’m not interested in being too active in the stock market right now. Noise is too high versus signal. Not a great +EV environment for our style of trading. So I just continue to watch some areas of the market that I have high conviction in over the next few years. Precious metals sit at the top of this list.

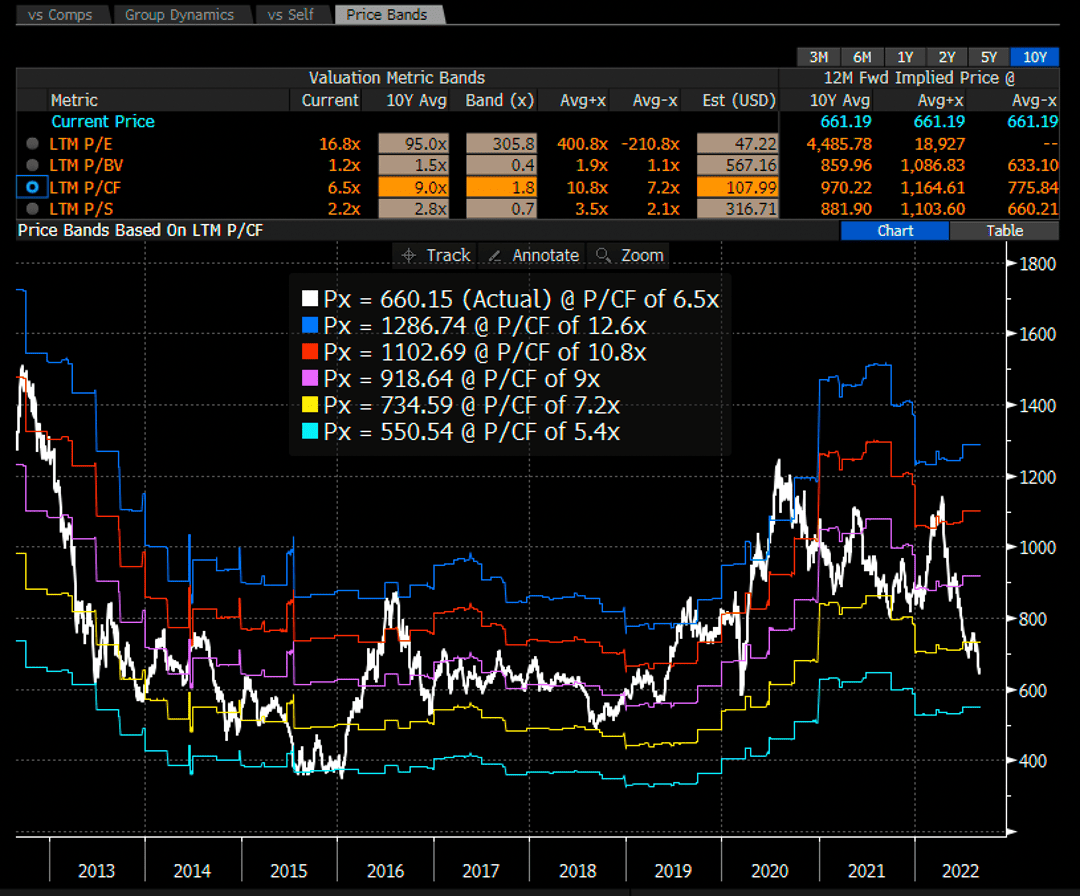

- TTM Price to cash flow multiples for gold miners are at 6.5x, nearing 2tsd below their 10yr rolling average.

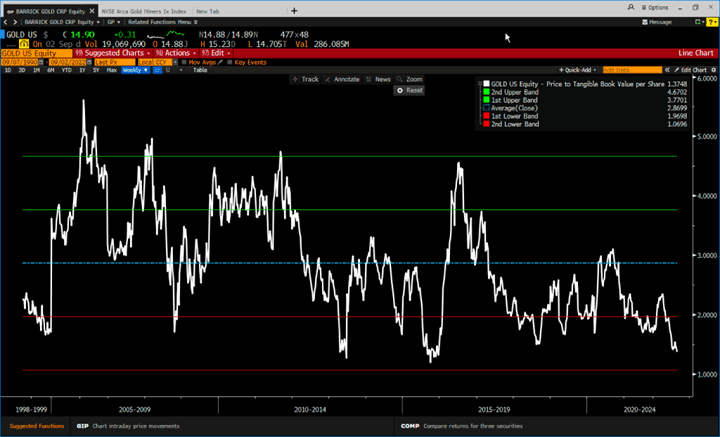

- Barrick (GOLD), one of the larger gold miners by market cap, is trading at a P/TBV that is nearing 2std below its 25yr average.

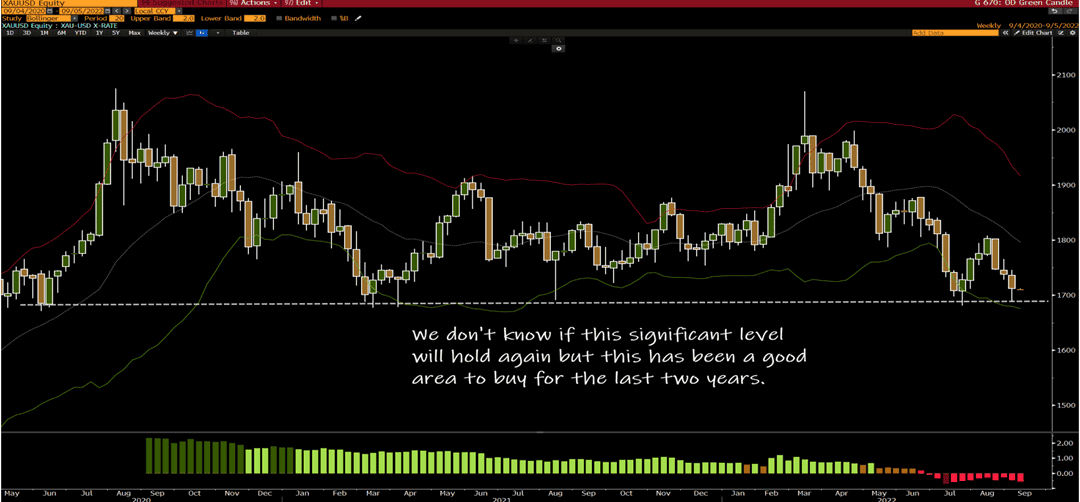

- Gold traded down to the lower bound of its 2yr+ sideways range last week. This has been a good spot to buy over the past few years. It may be a good time to buy here. I don’t know. I don’t have strong conviction on where gold goes over the next few weeks to months. But, 1-2 years out, I’m very bullish.

We just need the dollar to stop its rise and real yields to settle, and then it’s game on.

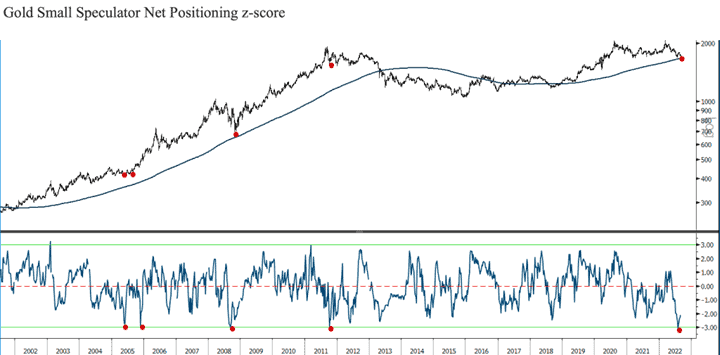

- Net small specs in gold fell to 3std below their 12m avg last week. Red dots mark past instances.

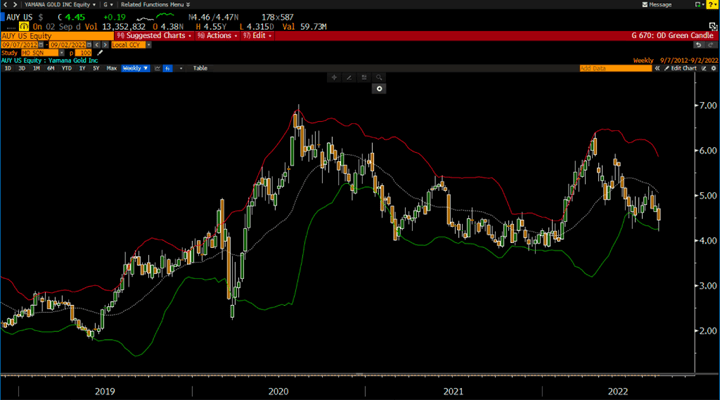

- AUY is one of the few large-cap PM miners that’s positive on the year. It’s one of my favorite miners for both fundamental and technical reasons.

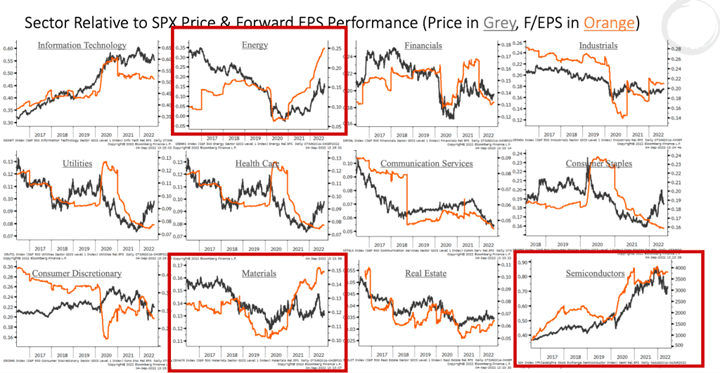

- Energy and materials remain the only sectors of the market with positive relative forward EPS trends. So if you’re wondering where to focus your efforts, those are good places to start.

One interesting thing is how well Semi relative N12M EPS has held up. You wouldn’t expect that, considering SMH is down 30%+ ytd. I remain a long-term bull on the space for the reasons I outlined in Underwriting The Future.

Thanks for reading.

Stay frosty and keep your head on a swivel.