We hope you enjoyed your extended weekend! As the weather warms up it remains harder to stay indoors. In light of that, you know how easy it is to practice social distancing in a boat? Pretty easy. Just boat six feet away from everyone else!

Before diving in, I want to take time to thank all our servicemen/women for their valiant efforts. It’s what they do overseas (and at home) that enable the rest of us to live free, full lives. We sleep easy at night knowing America’s finest are on the clock 24/7 keeping us safe. We will never be able to thank you enough.

In honor of Memorial Day, my brother and I are attempting “Murph”. For those that don’t know, it’s a workout from hell. Here’s the layout:

-

- 1 mile run

- 100 pull-ups

- 200 push-ups

- 300 air squats

- 1 mile run

Try it out this week! If you do it, email us your time! Fastest times will get a shout-out in next week’s email.

Our Latest Podcast Episodes:

Here’s what we cover this week:

-

- Greenhaven Road Partners Q1 Letter

- Gavin Baker’s Latest Talk at Columbia

- Howards Marks on Knowing What You Don’t Know

Let’s get it!

—

May 27th, 2020

Tweet of The Week:

— 𝘉𝘐𝘓𝘓 𝘚𝘞𝘌𝘌𝘛 (@billsweet) May 27, 2019

__________________________________________________________________________

Investor Spotlight: Greenhaven Road Partners

GIFs by tenor

GIFs by tenor

This week’s Investor Spotlight features Greenhaven Road Partners Fund. We hope you find one (or a few) that reach your short-list.

Greenhaven Road Partners Fund: -23.5% Q1

Greenhaven Road Partners (GRP) returned -23.5% in Q1. GRP is a unique fund-of-funds. It invests in small, one-man-shop firms that meet specific characteristics. These firms have concentrated portfolios, invest in off-the-beaten-path ideas and allocate a large portion of their personal net worth into their funds.

The letter highlights some of the funds investments (you’ve heard quite a few of these names):

-

- Laughing Water Capital

- ADW Capital

- Desert Lion

- Maran Capital

- Tollymore

- Long Cast Advisers

- Arquitos Capital

- Far View Capital

We’ve already highlighted the letters of most of these funds,so we’ll cover the ideas we haven’t heard yet.

API Group (API), ADW Capital

Business Description: APi Group Corporation provides commercial life safety solutions and industrial specialty services. The company offers specialty contracting services and solutions to the energy industry focused on transmission and distribution in the United States and Canada; and industrial services, including the retrofit and upgrading of existing pipeline facilities. – TIKR.com

You can read their S-4 filing here.

What’s To Like:

-

- Stable end-markets

- Trades at 5x free cash flow

- Essential service

- Boring business

- Forced buyers from NASDAQ listing

What’s Not To Like:

-

- 44% Unionized workforce

- Serve energy exploration end-clients (cyclical)

- $1.2B in total debt

What It’s Worth (from the letter):

-

- “Given that we believe API’s business is superior to most of its public comparables, has a proven capital allocator/owner at the helm, and has an established framework to expand EBITDA margins over the next few years, we believe the APG stock should trade at a premium to its larger peers. At only 16x 2019 EPS, APG shares would trade at almost $20/share or about a +110% return from today’s prices.”

Chart Analysis

The stock remains above the 50MA but I wouldn’t put too much emphasis on this chart. There’s not much history here.

Gym Group PLC (GYM.L): Tollymore

Business Description: The Gym Group plc operates health and fitness facilities in the United Kingdom. It operates 175 gyms. The company was founded in 2007 and is based in Croydon, the United Kingdom. – TIKR.com

What’s To Like:

-

- 20%+ 5YR Revenue CAGR

- 99% Gross Margins

- Expanding Operating Margins (18%)

- Low-cost gym offering

What’s Not To Like:

-

- Large cash inflow from “other operations” last two years

- $430M in net debt ($211M from capital leases)

- Gyms in serious question post-COVID

What It’s Worth:

Let’s assume $216M in revenue and $108M in EBITDA by 2024. Let’s also assume cap-ex hovers around 25% of revenues (historical average) over the next five years.

That leaves us with $46M in FCF by 2024, $63M in PV of cash flows and $390M in terminal value. That’s roughly $453M in Enterprise Value. Add cash ($3M) and subtract debt ($327) and you’re left with $128M in shareholders equity ($0.77/share).

This assumes GYM doesn’t reduce its debt over the next five years, when in fact the opposite is plausible.

Chart Analysis

GYM remains below its 50MA (bearish) in a solid downtrend. I’d like to see a strong move above the 50MA and a breakout above the 165 level.

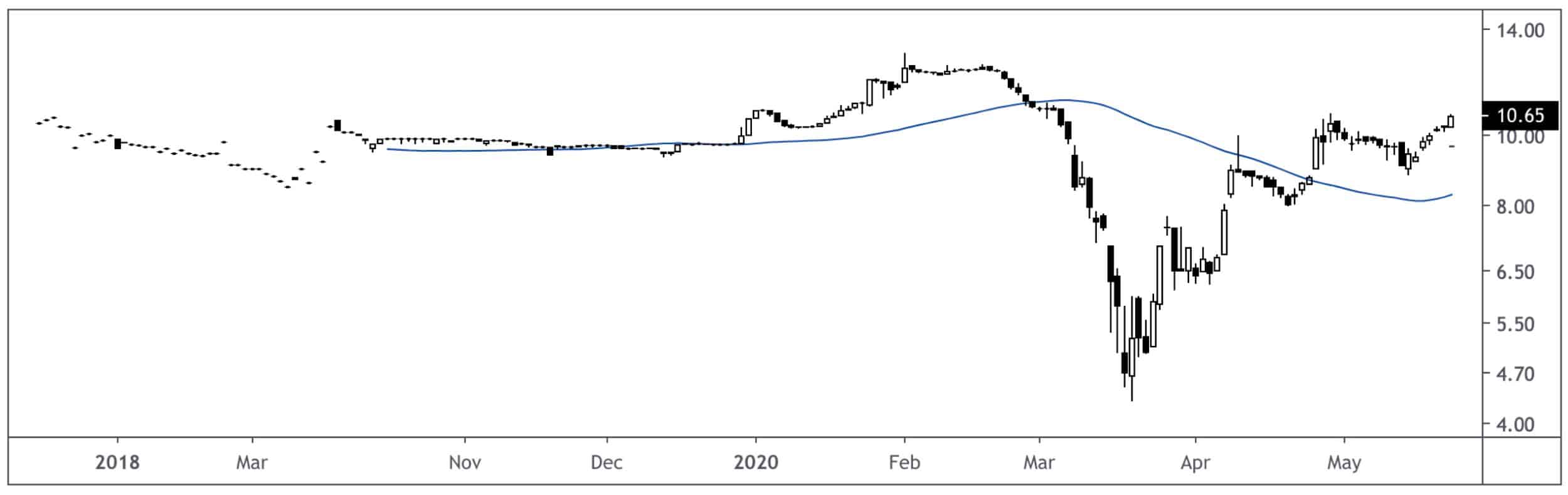

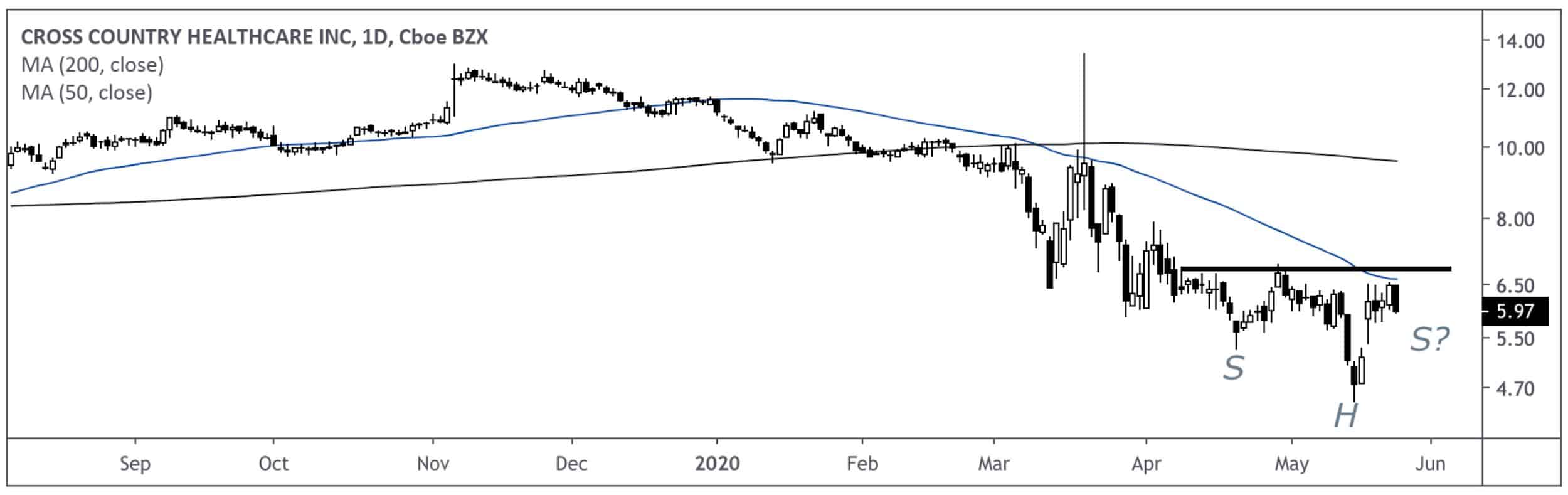

Cross Country Healthcare (CCRN): Long Cast Advisers

Business Description: Cross Country Healthcare, Inc. provides healthcare staffing, recruiting, and workforce solutions in the United States. The company operates in three segments: Nurse and Allied Staffing, Physician Staffing, and Other Human Capital Management Services. – TIKR.com

What’s To Like:

-

- 25% Gross Margins

- Reduced Total Debt/Equity

- Trades for 0.38x Revenues

- Co-founder returning to company

What’s Not To Like:

-

- Consistent laggard

- Currently money-losing

- Cash flow from ops is positive due to “other operating activities” not core biz

- SG&A margin increased while EBITDA margin decreased

Avi’s Take:

-

- “The business has some temporary COVID-related tailwinds, but also headwinds due to declines in non-COVID related emergency room visits, operations, other deferred elective procedures, and school closures. Looking through this, I observe an inexpensive yet durable, cash-flow generating founder/operator company doing the right things to weigh the odds more favorably towards profitable growth.” – com

Chart Analysis

This is a turnaround story led by a returning co-founder hoping to revitalize a lagging, money-losing business. If he’s successful, we should see a reversal in share price and a breakout above the resistance line.

Wouldn’t surprise me to see an inverse H&S form on this chart, further bolstering the bullish case and the completion of the turnaround project.

Naked Wines PLC (WINE.L): Far View Capital

Business Description: Naked Wines plc, together with its subsidiaries, engages in the retailing of wines, beers, and spirits in the United Kingdom, the United States, Australia, and France. It operates through four segments: Retail, Commercial, Lay & Wheeler, and Naked Wines. – TIKR.com

What’s To Like:

-

- High 20’s Gross Margin

- Total Debt/Equity of 0.31x

- 15x EBITDA

- Shift to DTC wine sales

What’s Not To Like:

-

- Money-losing in 2019

- EBIT/Interest Payments less than 2x

- Significant share price increase YTD

- Increase in cash conversion cycle from 35 to 75

Far View’s Take: “As we have seen in other industries, once consumers experience the benefits of an online model, they are unlikely to return to their prior purchasing patterns. As the leader in U.S. direct-to-consumer wine, Naked has the potential for a significant inflection in its business trajectory on a more permanent basis.”

Chart Analysis

WINE broke out of its descending wedge with a strong weekly close above the chart pattern and 50MA. The stock’s up nearly 45% since that weekly breakout. The next real resistance lies around $480 as WINE tests previous highs.

__________________________________________________________________________

Movers & Shakers: Gavin Baker & Howard Marks

GIFs by tenor

GIFs by tenor

Man do we have two great resources for you this week! Howard Marks discusses Knowing What You Don’t Know. Gavin Baker chats video games, venture capital, doing what’s obvious and technology.

Howard Marks: Knowing What You Don’t Know

Marks is a distressed investing OG and viral book seller. His most recent discussion on investment philosophy, contrarianism and framing is worth the read.

Marks notes six insights that guided his investment philosophy to what it is today:

1. View Market Movements Constructively

Marks’ Take: “I tend to think of them, more productively, as excesses and corrections.”

2. Know What You Don’t Know

Marks’ Take: ““It’s so silly for an investor to build his investment conclusions around his view of what the disease holds when he knows nothing about it … You shouldn’t make it up on your own, you should look to the experts.”

3. Insist on a Margin of Safety

Marks’ Take: ““The expert calibrates the expression of his opinion based on how firm the evidence is … The investor should calibrate his confidence in his investment based on how much margin of safety there is.”

4. Know When To Get Aggressive

Marks’ Take: ““I think that toggling between aggressive and defensive is the greatest single thing that an investor can do, if they can do it appropriately.”

5. Be Different, But Be Correct

Marks’ Take: ““If you think and behave different from other people — and you’re more right than they are, that’s a necessary ingredient — then you can have superior performance”

6. Get Comfortable with Discomfort

Marks’ Take: ““Every great investment begins in discomfort. If everyone else didn’t hate the investments, they wouldn’t be cheap.”

Gavin Baker: Venture Capital, Tech, Video Games & Doing What’s Obvious

Gavin Baker sat down with the Columbia Student Investment Management Association for a 90 minute knowledge bomb session.

Here’s my time-stamp for the video. It’s 90 minutes long. Pro-tip: watch at 1.75x speed. It sounds normal and reduces the listening time from 90 minutes to 52 minutes.

Check out the video here. If that link doesn’t work, check out Gavin’s YT channel. The video is the latest one on his page.

-

- 12:00 – Roadmaps and Loosely-held opinions

- 23:00 – Technology

- 28:25 – Video games

- 38:00 – Winners of the video game industry

- 49:00 – TikTok

- 58:00 – Making Difficult Decisions

- 63:00 – Competition Demystified

- 68:00 – Freemium Model

- 76:00 – Venture Capital Models

__________________________________________________________________________

Article of The Week: When Safety Proves Dangerous

Farnam’s latest piece, When Safety Proves Dangerous, stabs at the heart of the COVID-19 issue. It’s a five minute read and worth every second.

There’s two ideas that resonate throughout the article:

1. Risk Compensation

Farnam’s Take: “Risk compensation means that efforts to protect ourselves can end up having a smaller effect than expected, no effect at all, or even a negative effect. Sometimes the danger is transferred to a different group of people, or a behavior modification creates new risks.”

2. Risk Homeostasis

Farnam’s Take: “enforcing measures to make people safer will inevitably lead to changes in behavior that maintain the amount of risk we’d like to experience, like driving faster while wearing a seatbelt. A feedback loop communicating our perceived risk helps us keep things as dangerous as we wish them to be. We calibrate our actions to how safe we’d like to be, making adjustments if it swings too far in one direction or the other.”

What does this mean for investors? Let’s use the two frameworks in an example.

You’re up big on the year. You’ll more than likely take bigger swings (i.e., risks) knowing you have the cushion of strong profits. That’s Risk Compensation. Don’t get me wrong. I don’t think this necessarily a bad thing. The Druck uses a similar strategy. If he’s up big he bets big.

Risk Homeostasis is a bit trickier. Let’s say we have a newly defined trading rule (i.e., seatbelt in car) of 1% risk per trade. There’s no denying the 1% risk rule is good for a trader. But what are the second-order consequences of this risk mitigation strategy? Over-trading.

Since you’re only risking 1% of your capital per trade, it could cause you to place too made trades. Even trades of the same correlation.

__________________________________________________________________________

That’s all I got for this week. Shoot me an email if you come across something interesting this week at brandon@macro-ops.com.

Tell Your Friends!

Do you love Value Hive?

Tell your friends about us! The greatest compliment we can receive is a referral (although we do accept Chipotle burrito bowls).

Click here to receive The Value Hive Directly To Your Inbox!