***Below is an excerpt from a note sent to Collective members earlier this week***

“This is my 45th consecutive year as a Chief Investment Officer. In 45 years I’ve never seen a constellation where there’s no historical analog. I probably have more humility in terms of my views going forward than I’ve ever had.”- Druck at Sohn.

You’ve all probably seen the Druck interview at the Sohn conference. If you haven’t, here’s the link. It’s one of his better talks (thread with highlights from the talk here).

Humility, practicing weak opinions weakly held, is essential in this market. The market will serve it up to you one way or another, so better to adopt it preemptively. It hurts less.

Like the GOAT said, there are zero historical analogs for what we’re experiencing today. Nobody… and I repeat, nobody… knows where this bus is headed or what path inflation will take, or at what level yields will settle.

The good thing for us is that we don’t need to know. Our approach isn’t based on knowing. It’s based on playing the meta game. On employing a framework to assess the odds and balance out our positioning accordingly.

A critical part of our process is having guideposts. Data points that tell us what’s probable so we can continuously update our views and quickly correct them when wrong. This is always important but especially so when in a bear market.

A recent example of this is the short-term Buy Signal that triggered for us on May 23rd when our systems told us that odds strongly favored a multi-week bounce in risk assets.

We got the bounce but it was more short-lived than expected. And that’s because one of our guideposts, US treasury yields, failed to settle down and hold a ceiling. When yields broke out again, it was an important guidepost telling us to go back to playing defense, and so here we are.

The SPX closed nearly -4% down today. While 10-year notes finished the day down roughly -1.25%. We typically like to fade fear and concerns around financial plumbing and other types of hysterics (example: our Sep 2019 report titled Much Ado About Nothing: Repo Rates and Doom Narratives). But what we’ve seen over the last few days is not a healthy market, and that makes me concerned.

Here’s the problem… Stocks can’t bottom until yields slow their roll. Yields won’t settle until we get visibility on cooling inflation (this will take a couple of months, at least). Until then, the Fed is strongly biased hawkish. They have to be. And they have to try to match or exceed the market’s expectations or risk easing financial conditions, which they can’t afford.

This leaves us caught in a destructive feedback loop where rising yields drive risk assets down, which creates increasing alarm over high inflation levels, which puts greater political pressure on the Fed to be more aggressive.

***Enrollment to our Collective ends this Sunday at Midnight. We won’t be running another one for a while, so if you’re interested make sure to sign up. Here’s the link.***

Bonds are supposed to act as a countervailing force to stocks. A kind of pressure release valve. When equities get dumped, bonds get bid, and yields fall. This helps establish a floor under risk assets.

Without that valve, we get air pockets (ie, what’s currently happening). This is why the above feedback loop is so concerning. And unfortunately, there are a few other developments that make it even more so.

An inevitable shift in BoJ policy…

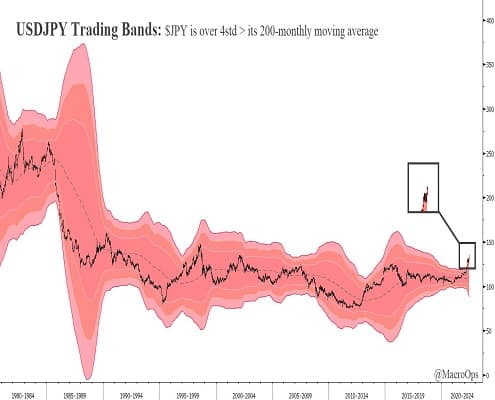

The USDJPY is over 4stdev above its 200mma for the first time in its history. It’s getting nuked because the BoJ is the last central bank standing that’s still practicing a form of yield curve control. The yen recently hit its lowest level against the dollar since 98’.

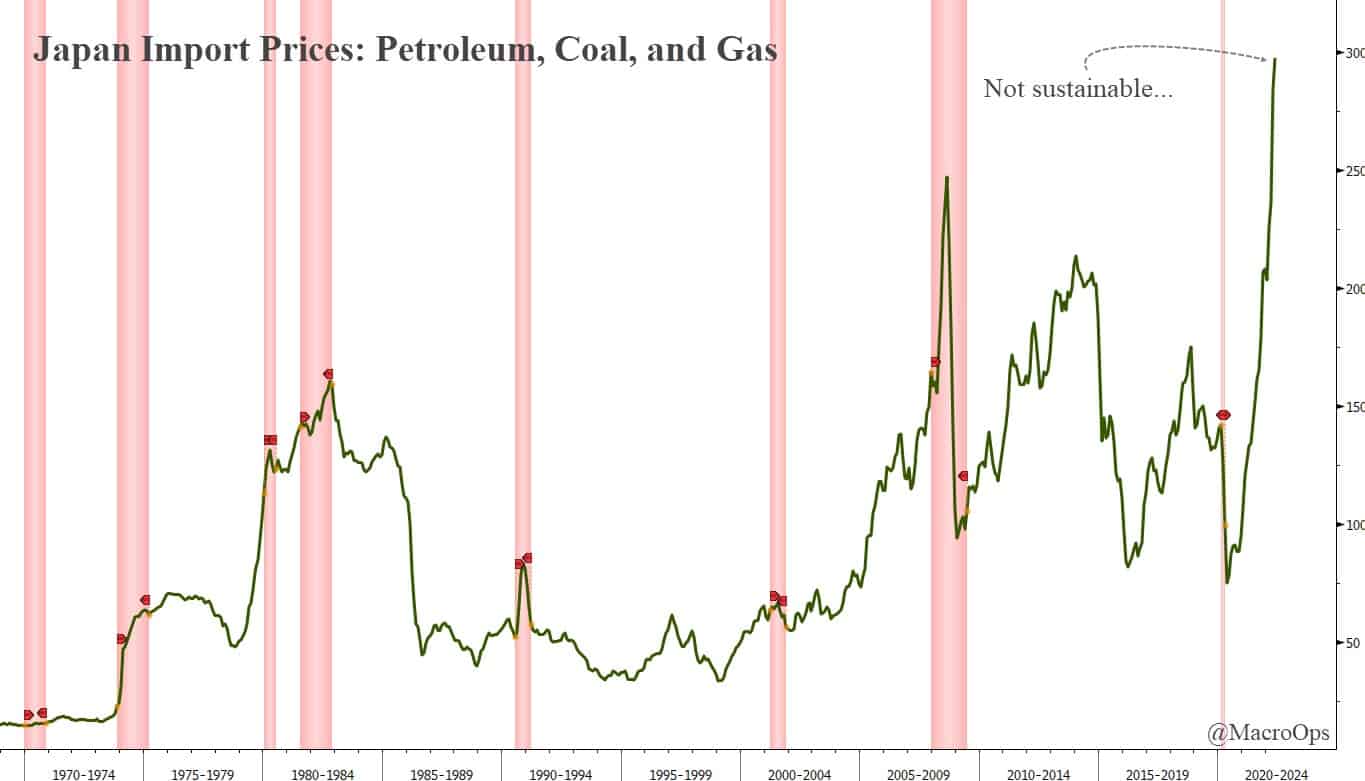

This is not ok for Japan. The reason being is that Japan is a large net energy importer. Energy, things like oil, coal, and gas, comprise over 20% of their imports. All those goods are priced in USD. They are now the most expensive they’ve ever been (see below).

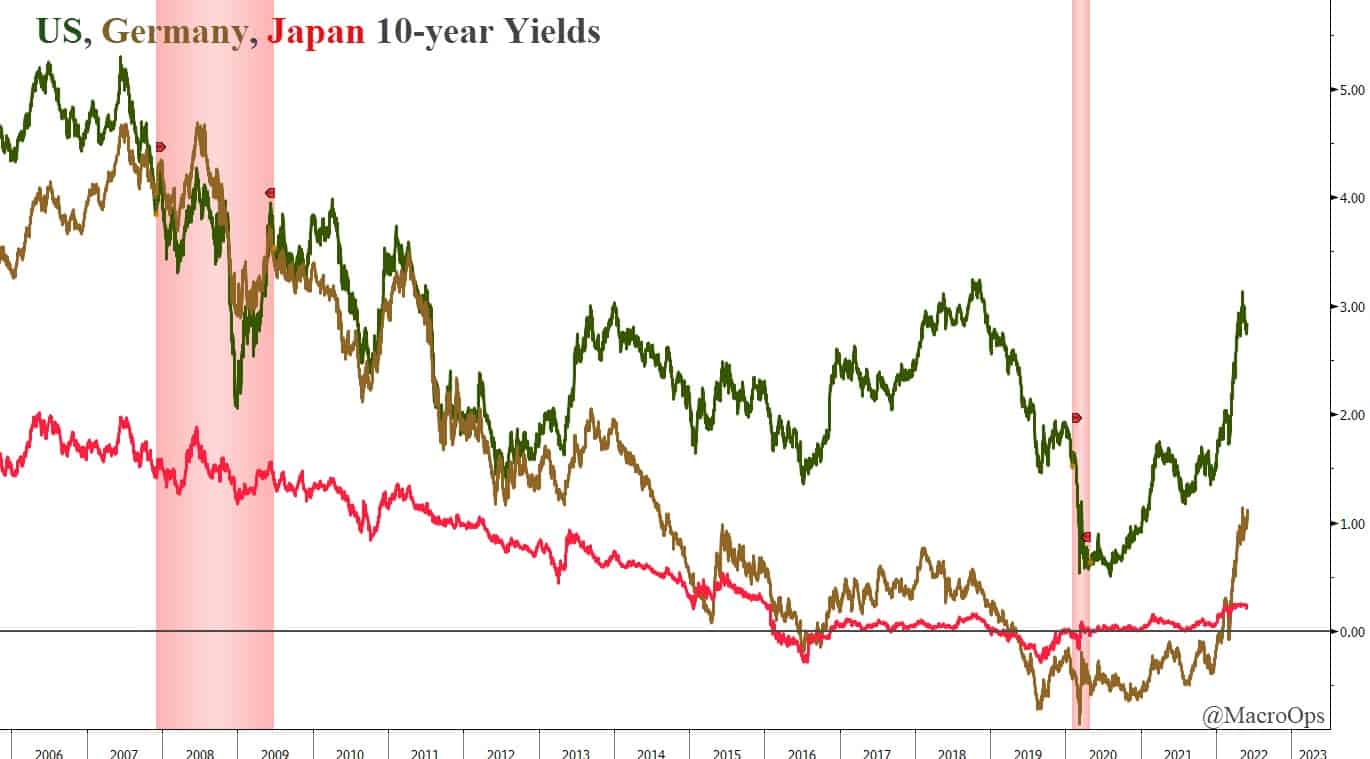

The BoJ meets this week. Japan’s 10yr yield is bumping up against its 0.25% cap for the first time since Jan 16’. This matters for markets more broadly because low Japanese yields have long acted as an anchor to those in the US.

Remember, markets are a relative game. The price of one sovereign bond needs to be looked at in relation to the price of others. Pinned yields in Europe and Japan have long kept a lid on those in the US. Inflation has forced the ECB to abandon the ship called ZIRP. Japan will eventually be forced to do the same. Currency weakness and crushing import costs will demand it.

This is an additional dynamic that risks accelerating our destructive feedback loop.

And… that’s not all.

The eurozone is a potential flashpoint for all of this.

European sovereigns can’t print their own money. That’s done by the supranational entity, the ECB. This means EU member bonds are not “default-risk free” like USTs or JGBs, since those two can always just spin up the cash cannons. Greece, Italy, etc… cannot. They are completely dependent on the goodwill of the ECB. And that goodwill is conditional upon member countries maintaining certain debt and fiscal targets.

Well, inflation is making both of these conditions indefensible for a few member countries with Italy at ground zero of it all.

The yield on 10yr BTPs has risen from 2.90% to 4.10% in just the last two weeks. Spreads on Bunds are quickly approaching their COVID wides (chart below). The ECB, under its current legal mandate, can’t do anything, other than continue to make things worse because it needs to fight inflation.

What does this mean?

Here’s the following economist and fund manager, Eric Lonergan.

What is to be done? At the moment, we are on course for a full-scale run on Eurozone sovereigns. The fiscal arithmetic becomes self-fulfilling. While Italy’s soveriegn debt stands at around 150% of GDP, yields on BTPs are everything. The yield on 10-year BTPs has already risen from 0.5% in September last year to nearly 4% on Friday. If these levels are sustained, the consequences for fiscal policy become untenable. Markets are likely to push them far higher. Italy quickly becomes a default risk, despite heroic efforts by Italy to cope with macro shocks, run large primary surpluses, and extend the term structure of its debt.

This is one reason why the western powers are working so hard behind the scenes to try and get a ceasefire in the Russia/Ukraine conflict. They’re desperate for anything to bring down inflationary pressures because they starting to see what’s coming, and it’s not good.

That’s enough doom and gloom for me today. None of the above is inevitable. The situation is dynamic and policymakers are more responsive than they used to be. Again, we don’t need to predict. We just want to be mindful of developments and the expectations that are currently embedded in markets surrounding those developments.

There are potential trades to play these trends.

We can short JGBs, short the DAX, or short EURUSD. DAX and EURUSD are deeply oversold over the short-term so not interested but will be on a pullback if we get one.

Also, just sitting in lots of cash and doing research into things to buy when the dust begins to settle is another good option (our port remains in roughly 80% cash with risk completely netted out, so we have a LOT of dry powder to scoop things up once this fire sale reaches its zenith…). Plus, we’re up 21% on the year and aren’t keen to give too much of that back trying to trade a high noise / low win rate bear volatile regime.

If we get a big multi-week rally in risk assets then I’ll get more interested in pressing on the short side. But at these levels, it’s just tough. You don’t want to short in the hole. Getting your face ripped off in a bear rally is never fun, not to mention position sizing is next to impossible.

The optimal short still seems to be in the crypto space. The crypto markets will be dead money for years. The correction there is just getting started. We’ll keep pressing our sizable ETHUSD short when given opportune technical entry points.

Honestly, one of the best trades we could all put on right now is picking up a hobby or taking a trip. It’s what Druckenmiller is doing.

In the interview, Stan said he’s “coming in every day and I’m looking at my screen but I’m pretty much taking a break. I’m waiting for a fat pitch… I want to be fresh. It has been a lot of activity in the last 4-5 months. I’m in no hurry here. I’m in the marathon and I’m not running full out on mile 16…”

I like this trade…

If you’d like to join us in our market adventures then click the link below and sign up for our Collective. We are in one of the most engaging macro environments in over a decade. There will be a LOT of money to be made and lost if you don’t know when to hedge your risk and cash your chips. Enrollment to our group closes this Sunday at midnight. So if you’re thinking about joining the team, make sure to do so before then. Hope to see you in there and happy hunting!

![]()