It’s important to understand how to evaluate a company. But it’s even more important to know how to evaluate other investors.

It all comes down to expectations. What is the majority expecting? How can they be surprised? These factors are what move a stock’s price.

And nowhere is this phenomenon more prevalent than in growth stocks.

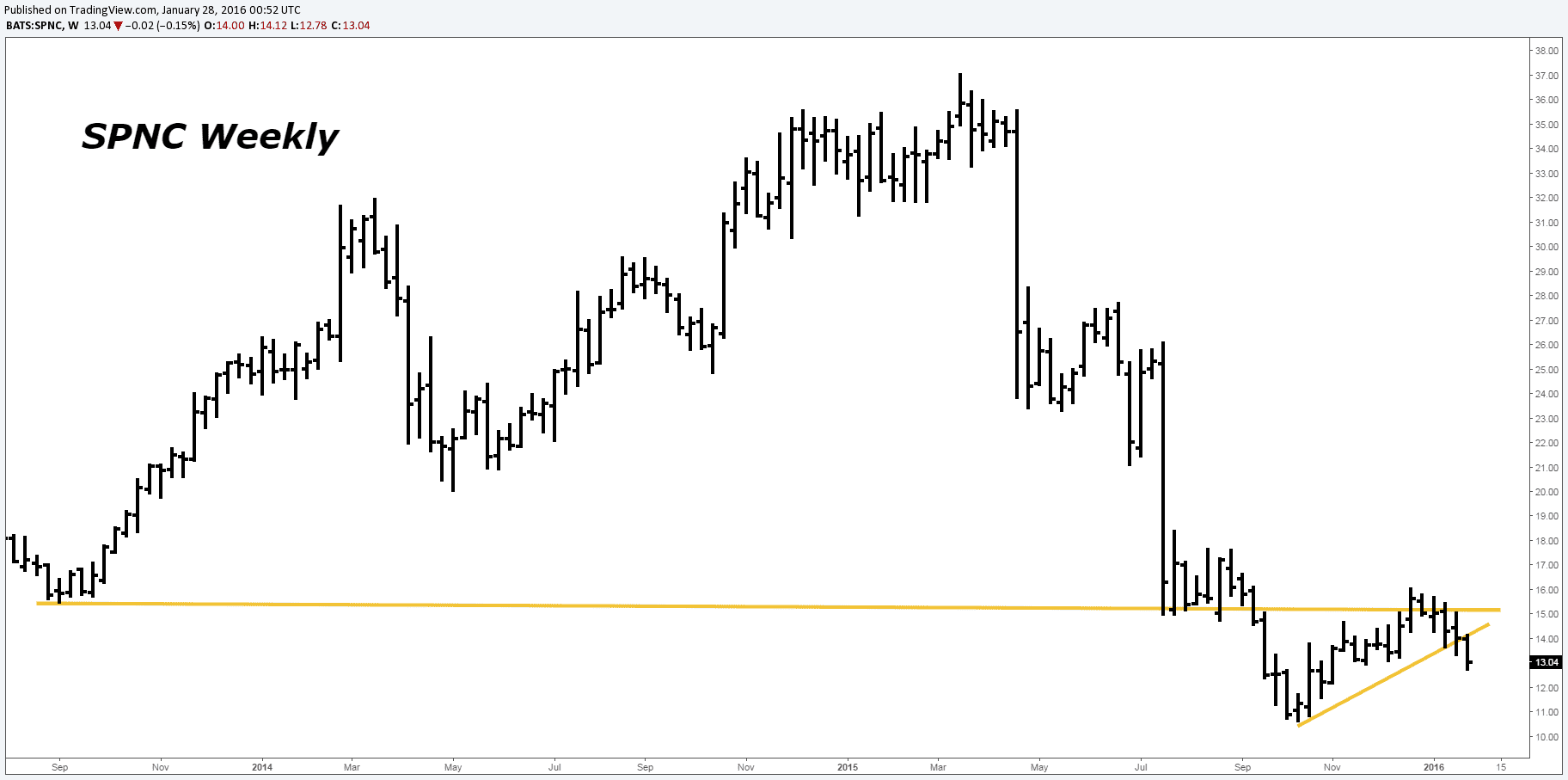

Take The Spectranetics Corporation (SPNC) for example. From 2012 to 2015, this cardiovascular medical device maker rocketed 345%.

How’d this happen? Did it have consistently strong earnings?

Nope.

SPNC has lost money for a majority of its existence. Since the IPO in 1992, it has only had a handful of quarters that were actually positive — and only just barely. The rest have been filled with losses.

The key driver that propelled SPNC all this time was expectations. Investors always believed it would eventually turn a profit. And that’s why SPNC could post loss after loss and still see its shares appreciate. For example, it reported a loss of $.05 per share in the third quarter of 2014. Yet the stock continued to shoot higher soon after. Why? Because investors were expecting a larger loss of $.83 per share. So a loss of just $.05 looked pretty good. The same thing happened in the fourth quarter of 2014. Investors expected a loss of $.06, but got a $.04 loss instead. So they were happy and the stock continued to rise.

But the situation changed when first quarter 2015 earnings rolled around. SPNC reported a loss of $.30. This missed the street’s expectation of a $.24 loss. The company also missed on revenue. Revenue came in at $57.4 million when investors were expecting $60.6 million.

After beating estimates time and time again and running up 345%, SPNC finally missed. It failed to meet expectations. The result? Its stock tanked over 20% the next day.

Growth investors are fickle. Either you “wow” them every earnings report or they drop you faster than a ton of bricks. And that’s exactly what happened here. The reason SPNC’s stock price was so elevated was because investors expected exponential improvement. This improvement was supposed to eventually lead to huge profits. There was a large factor of hope propelling the company’s share price. But the minute SPNC missed estimates and failed to live up to the dream, it was knocked down hard.

It’s dangerous for a growth company to tamper with the “hope” that propels it. Questions start to arise among investors. Is this really a future winner? Are the current losses worth it? Why is revenue faltering? When confidence is lost, share prices usually take a huge haircut.

Second quarter 2015 earnings made things even worse. SPNC actually beat on earnings, but missed on revenue once again. They also lowered their revenue guidance for the rest of the year. Investors’ confidence was already shaky. But this earnings report pushed it over the edge. SPNC’s share price fell almost 35% after the report was released.

The stock continued lower until third quarter 2015 earnings. By that point, since its early 2015 high, SPNC had lost over 70% of its value. But fortunately, third quarter earnings met expectations. The stock price rebounded. After multiple disappointments, investors were finally satiated with a report that wasn’t “too bad”. Expectations and the company’s performance finally lined up for once. And so the price rebounded.

But now the share price is breaking down again. What gives?

The problem is that the dream behind SPNC is severely injured. Even with the latest earnings meeting expectations, the growth story is crippled. The past disappointments sobered SPNC investors up. And now as they objectively look at the company, they see it’s a mess fundamentally.

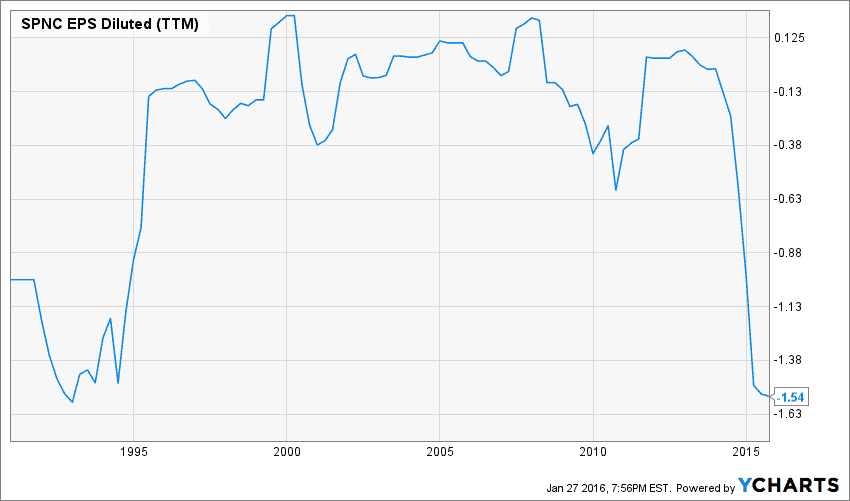

Spectranetics has been public since 1991. That’s 25 years on the market. And in 25 years, the company has been barely able to turn a profit. Just take a look at their earnings per share history below:

EPS was stable for some time. And during those years, revenues were growing. So investors were satisfied. But now since 2013, EPS has fallen off a cliff. It’s dropping to some of the lowest levels in the company’s history. And this is during a time when SPNC is consistently lowering its revenue guidance. So investors get a company that’s losing increasing amounts of money while its revenues decline. This deal is clearly not attractive.

On top of that, SPNC’s debt situation is terrible. The company is highly leveraged at a debt-to-equity ratio of 2. Most other competitors in its industry are below 1. For example C R Bard (BCR) has a ratio of .947. And Medtronic (MDT) is at .686. SPNC is far exceeding industry debt levels.

Growth stocks are some of the best investments in a bull market. But they’re always on thin ice with investors. That’s how it goes when companies play the expectations game. And this game only becomes harder in a bear market like the one we’re currently entering. As entire indices start to roll over, companies like Spectranetics with negative earnings and high debt become investor kryptonite. The parabolic run a growth stock like SPNC has in a bull market, usually gets reversed in the bear.

Our team at Foundation believes SPNC has a lot further to fall. Our price target is $8.00. This would be a decline of another 33% from current levels.