A large impetus to the next thrust higher in European equities will be the final round of French elections this Sunday.

We’ve covered the rise of populism and how it affects markets for some time now…

If Macron should win Sunday, as we expect, the populist threat will likely recede for the time being. The next contentious European election is Italy’s. But that’s not until the middle of next year. The Eurozone should be safe until then.

As we discussed in last month’s Macro Intelligence Report (MIR), the populist movement is cyclic with a tendency to swing back down towards its longer-term trend.

A Macron win will be a huge narrative boost that’ll clear a major roadblock keeping investors out of European equities. The elections are partly why US investors have been pulling money from European ETFs in 13 of the last 16 months.

Macron winning will also boost the euro against the dollar. This will raise total returns for those buying European stocks and create the possibility of a positive, although temporary, feedback loop.

As we’ve previously discussed, there’s still plenty of room for performance reversion to occur between the US and Europe. The chart below, via the CFA Institute, shows the rolling 10-year performance difference between the two. The blue line indicates when European stocks outperform US stocks over the previous decade. The red line shows when US stocks come out ahead. And the green line shows when US equities outpace European markets to an extreme — which is what we’re seeing today. As the writer of the article Michael Batnick notes, “In the 44 previous readings when the spreads reached 100%, European stocks went on to outperform for the subsequent 10 years.”

Data coming out of Europe is largely supportive of the recovery narrative as well. RBC’s economic coincident indicator is in a strong uptrend.

First quarter earnings for European stocks are coming in solid. In total, first quarter earnings on Europe’s STOXX 600 are expected to increase a solid 10.5% over the year prior. The companies that have reported so far have seen above average revenue and earnings growth.

And finally, we can’t forget to look under the hood of European liquidity conditions.

Just like in the U.S., credit spreads have continued to narrow in the Eurozone since the bottom in 2016. Liquidity conditions favor risk-on assets.

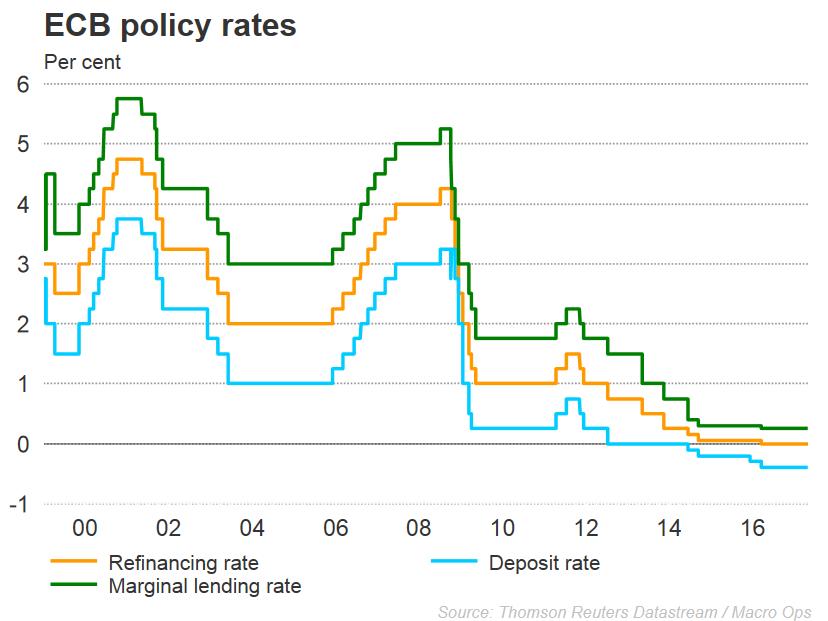

The other obvious thing to pay attention to alongside our liquidity indicator is ECB policy. As long as Super Mario keeps rates low, the system will remain liquid. As of right now the ECB has never been more dovish. All three rates are at all time lows…

If history rhymes (it usually does) there’s edge in betting on higher prices for Europeans equities in the months ahead. Favorable liquidity conditions place a bid under stocks as capital allocators take cheap money and pile it into higher returning assets.

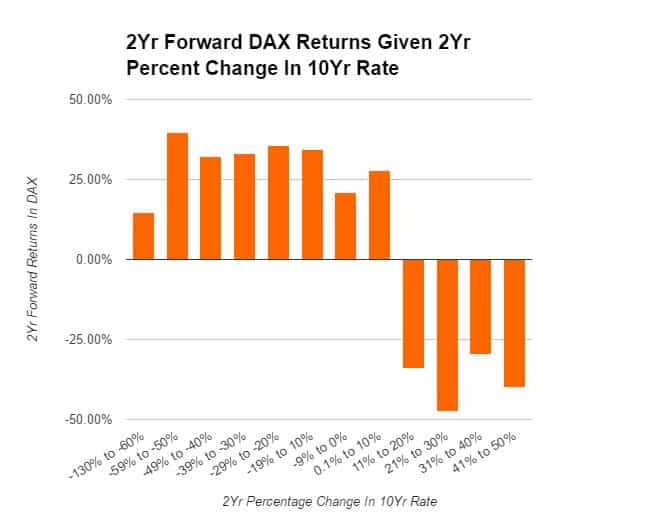

One thing we like to do at Macro Ops is verify our macro assumptions with historical data. It keeps us honest and free of incorrect biases.

Recently Operator Junaid from London helped crunch the numbers (from 1992 to present) on forward equity returns given various changes in interest rates.

We used the DAX as a proxy for European equity performance and the 10yr rate on Bunds was used for rates. Rate changes are in percent terms, not absolute terms. For example, a rate increase from 1.00% to 1.50% is a 50% increase in interest rates.

In the chart below you will see different rate regimes on the x-axis. For example, the -59% to -50% regime includes all occurrences since 1992 when the 10Yr German interest rate fell anywhere between 59% and 50% over the course of two years.

The y-axis then plots the 2yr forward returns of the DAX given the interest rate regime.

It ain’t hard to see that falling rate regimes are good for equities while rising rate regimes are bad. You can see in the chart that as soon as the rate regime turns positive (the 11%-20% increase regime) stocks suck.

According to our study, if rates have been downtrending, the probability of DAX trading higher is 88.89%. That probability plummets to 36.51% if rates have been increasing over the last two years.

Right now we’re in the midst of an ultra dovish regime. This means we should play for higher equity prices over the next 2-years. As long as liquidity remains favorable, stay biased to the longside.

All in all, the broader environment is supportive of higher European equities. And though we don’t believe this is the start of a new cyclical bull in Europe, there should be enough tailwinds to advance the stock market well into the end of the year.

But of course, there’s always that chance that Le Pen surprises with a victory. And with the way politics have played out over the last year, it really wouldn’t be that crazy.

A Le Pen win would significantly distort the market outlook in Europe and especially its currency. It could also roil markets around the world.

We’ll be buying long dated bond futures going into the end of the week. The ETF alternative is the iShares 20+ year Treasury Bond (TLT). This will hedge out our long exposure over the weekend and protect our downside should there be a Le Pen upset and subsequent large selloff next week. If Macron wins and markets go on a relief rally, we’ll quickly close out the position Monday morning. We shouldn’t lose much on the trade.