Enlabs (NLAB.OM) offers entertainment through various products, including casino, live casino, betting, poker, and bingo under various brands. The company is also involved in delivering sports results and technical solutions in the online gaming industry. It operates in Sweden, Malta, Baltics, and internationally.

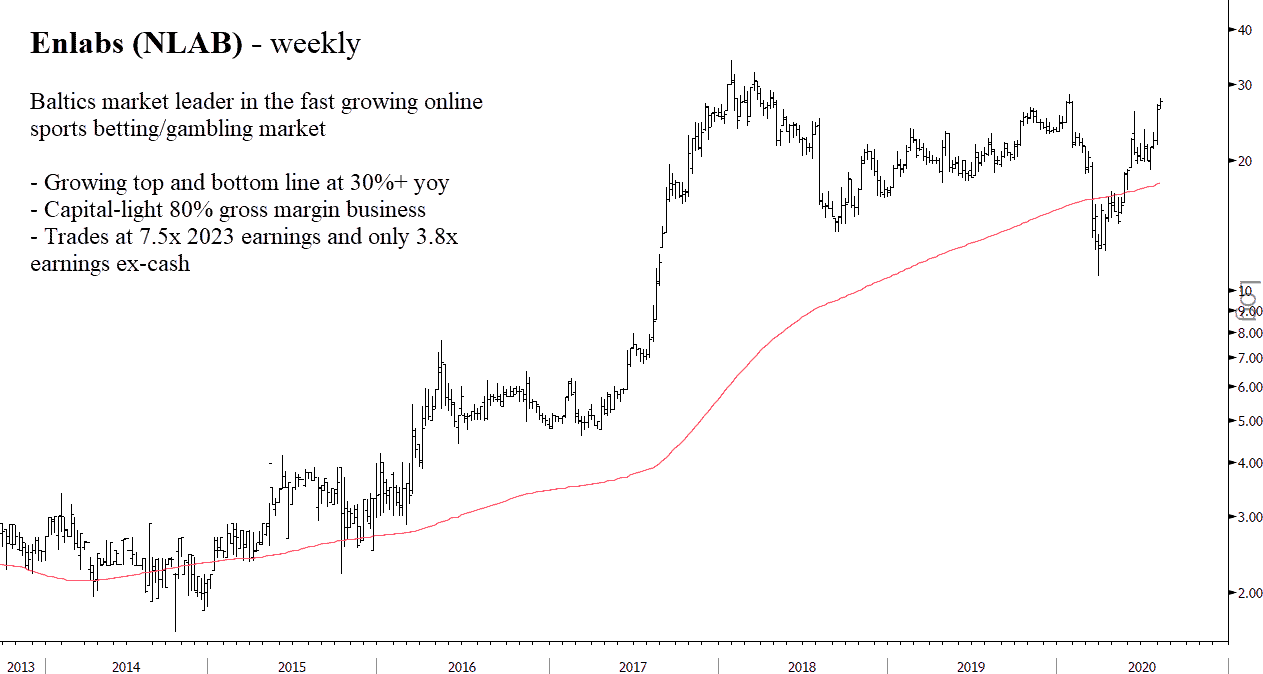

Thesis: NLAB is the Baltics market leader in the highly regulated, high barrier to entry and fast-growing online sports betting/gambling industry. The company commands 25% market share in the Baltic region and has its sights set on global expansion. NLAB’s growing earnings & revenues 30%+/annum while sporting 30% EBITDA margins. You can buy this business for 15x normalized earnings, well below industry/market averages. Management owns a decent chunk of stock and has zero debt.

The Core Business: NLAB’s core business is Optibet, it’s online gambling/sports betting platform. It’s a capital-light, 80% gross margin business. The company invested a ton of money to create a new, proprietary platform that can seamlessly integrate into new countries and regulation standards. Think of it like plug-and-play for online sports betting. The core business should continue its 30% growth as the Baltic sports the fastest internet and highest mobile data usage per capita in Europe.

Competitive Advantages: NLAB benefits from a first-mover advantage in many of its regions. Given the finite amount of betting licenses, the ability to move quickly within compliance is paramount. NLAB’s latest platform, along with its dominant market share in the Baltics create an easy choice for regulators when it comes time to hand out licenses.

NLAB Risks

Penetration Failure: NLAB fails to penetrate new markets like Sweden, Belarus and the US

No Relaxation in Legal Gambling: Countries fail to remove restrictions on legal sports betting/gambling

Cash-Burning Acquisitions: NLAB acquires companies that aren’t accretive to bottom-line, thus buring cash that could’ve been used to bolster core biz/platform

Valuation

Scenario 1: NLAB continues its revenue/earnings path for the next five years. We’d get 2024 with $118M in revenues, $29M pre-tax profit and $24M in FCF: $5.58/share (196% upside)

Scenario 2: NLAB grows 2020 revenue 30% but 0% for the remaining four years. This gives us $56M in revenues, $14M pre-tax profit and $15M FCF: $3.05/share (62% upside)

Scenario 3: NLAB loses 13% per year in revenue, giving us $21M in revenues, $5.21M in pre-tax profit and $4M in FCF: $1.48/share (21% downside).