In our most recent MIR we talked briefly about the growth struggles of EM in the context of the Gerschenkron Growth model, using China as our example.

Our conclusion was that China, and EM in general, is set to be a dead money trade and massive value trap for the remainder of this cycle.

So let’s flesh out a little more why this is likely to be the case.

To start, what exactly separates an emerging market from a developed one? Here’s a good explanation from Eric Lonergan writing on his blog Philosophy of Money (emphasis by me).

Emerging markets are not poor countries, nor are they countries which are making economic progress. They are defined by a very specific set of macroeconomic properties, which financial markets are conscious of, but are rarely clearly articulated.

The overriding characteristic of an emerging market is that a currency devaluation is a tightening of policy. In the developed world, a devaluation is typically an economic stimulus, indeed it often coincides with an easing of monetary policy through lower interest rates or an increase in QE. The post-Brexit policy response of the Bank of England is a case in point – sterling fell sharply and the Bank cut interest rates and initiated more QE.

In emerging markets the opposite occurs. These economies usually have public and private sector liabilities denominated in a currency which they do not issue. So when the Turkish Lira falls against the dollar the burden of finance on many Turkish corporates increases. Due to their US dollar liabilities, the interest payments and capital repayments in Turkish Lira rise. That is the first way in which a devaluation is a tightening of monetary conditions.

The second mechanism is more instructive and carries important lessons for monetary reform in the developed world, and in particular how we should think about the challenges posed by the zero-bound.

Emerging markets suffer from widespread price indexation and significant inflation expectations. In other words, when the currency falls, inflation rises, and when inflation rises the economic system attempts to respond by raising wages, and then raising prices. The 1970s concept of a wage-price spiral has meaning.

Because emerging markets have widespread wage and price indexation and alert inflation expectations central banks cannot exploit ‘temporary’ increases in the inflation rate by reducing real interest rates and stimulating demand, as they do in the developed world. Central banks, as we have seen in Brazil, Turkey and South Africa, have to respond to devaluations by tightening policy in order to prevent an increase in the underlying inflation rate.

EMs have what are called soft currencies, which is one of the three subsets of currencies in the global core-periphery paradigm that we talked about in our Jan 17’ MIR Vicious or Benign? To recap, these are:

- The reserve currency which is currently the US dollar.

- Hard currencies, that come from countries that can lend to themselves at competitive rates. These tend to be net-importers of commodities. Hard currencies generally act as safe-havens during periods of risk-off.

- And soft currencies. Soft currencies tend to be commodity producers. They are countries that have to borrow in other currencies at higher rates. These currencies depreciate during periods of risk aversion.

So… EMs are countries with soft currencies whom have to borrow in foreign hard money (typically dollar or euros) and therefore run into debt repayment problems when their currencies fall AND… due to widespread price and wage indexation, suffer from higher inflation when their exchange rate drops forcing their central banks to carry out procyclical tightening (ie, raising interest rates into a crisis) which causes a spiraling negative economic shock.

These conditions are what lead to the standard balance of payment (BoP) crises that EMs go through seemingly every few years.

A typical BoP crisis looks like this:

- Rapid economic growth attracts large capital inflows from foreign investors chasing higher returns.

- This capital flows into equities and hard currency-denominated debt.

- The strong domestic growth leads to a rise in imports which creates a current account deficit (more imports than exports) which then needs to be financed by more foreign capital flows.

- Eventually, growth slows and debt reaches levels that cause foreign investors to become concerned about the country’s ability to service it and pay it back.

- This causes the hot money flows to reverse, which drive the currency down, making the hard currency debt more expensive to repay, which causes more hot money outflows, in a crushing positive feedback loop.

- This goes on until the central bank raises interest rates enough to steady the currency and domestic demand collapses which brings imports back below exports, thus balancing the current account.

This is what we’re seeing variations of occuring in EM now, specifically in Turkey and Argentina.

But here’s why this time is going to be different.

You see, in the past, an EM BoP crisis led to a painful but typically very short, economic contraction where the economies and markets experienced v-shaped recoveries. The 97’ Asian crisis being a perfect example.

They were able to do this because they were rapidly expanding their share of global exports from a low base. A devalued currency meant more attractive exports which meant rising profits and a quickly balanced current account (exports greater than imports). This enabled EMs to deleverage and grow their way out of trouble.

Sri thiruvadanthai of the Jerome Levy Institute wrote about this in one of his recent papers (emphasis by me).

Given this background, it is clear why globalization, especially the period 2000-08, was so beneficial for EMs. Globalization allowed EM exports to DMs to grow exponentially, relaxing the BOP constraint. Moreover, increased capital flows allowed EMs to build their foreign currency reserves, further weakening the BOP constraint. The process of building reserves also fueled demand for safe assets, depressing yields in DMs and extending the unsustainable process of debt-fueled growth in the DMs. However, the EM boom of the 2000s was in part supported by an unsustainable debt driven growth in the DMs. Thus, when the financial crisis of 2008-09 forced DMs to deleverage, it undermined a key pillar of EM growth. The weakness of DM growth post 2008 and the plateauing of offshoring and outsourcing meant that EM export growth hit a wall. Initially, EMs were able to counteract these headwinds by running large fiscal deficits and by turning to domestic profit sources. As we have seen in a previous section, domestic profit source growth requires domestic credit creation. Unsurprisingly, EM credit growth exploded post-2008, and not just in China. The limits of EM domestic demand-driven strategy were reached sometime in 2012-14, and since then EM economies have been struggling.

EM’s structural growth limitations can be boiled down to the following:

- EMs are BoP constrained. Since they have soft currencies — meaning, they can’t finance current account deficits in their own money — they can’t grow faster than their exports for an extended period of time. Because, a current account deficit leads to a build-up of hard currency debt, hot money outflows, and a BoP crisis.

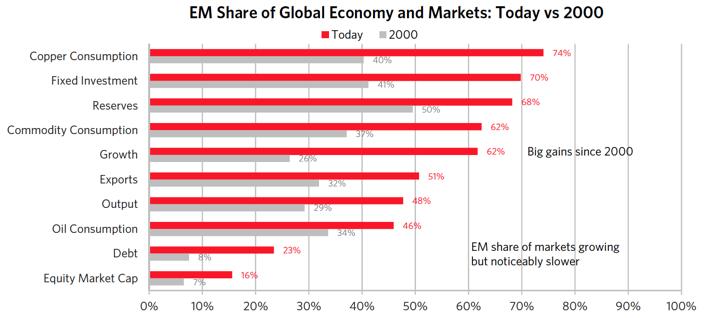

- EMs have maxed out their market share of global exports. EMs now comprise over 50% of global non-commodity exports (see chart below) and further export share growth will likely be from one EM cannibalizing another. Globalization has peaked and with increasing trade tensions, we should even see a reversal of some of the outsourcing and offshoring that’s occurred over the past two decades.

- EMs are facing a significant debt burden amid tightening global liquidity. EMs are weighed down by a large amount of debt which they’ve accumulated in financing their current account deficits over the last decade, and much of this debt is dollar-denominated. Rising US interest rates and a strengthening dollar will continue to put pressure on EMs going forward.

(Image via Bridgewater)

(Image via Bridgewater)

Then of course there’s a deleveraging China, which has been a big source of demand growth for EMs over the last decade but won’t be any longer.

So EMs are in a tough spot going forward. They need to rebalance their economies and boost domestic demand since they can no longer rely on exports as a serious source of growth. But, until they can get other countries to accept their currencies as payment, they will remain BoP constrained by their soft currency which won’t allow them to grow faster than their export growth. Which, as we’ve discussed, is going to be low.

I see a lot of investors and financial journos talking about how now is a good time to buy EMs. They’re all playing off the old EM playbook and are expecting a V-shaped recovery which is not going to materialize. What will, is a slow-moving economic contraction with occasional country-specific crisis that will frustrate investors trying to bottom pick.

Select EMs will make for incredible asymmetric investments once the next cycle begins in a few year’s time. By then, I expect the narrative to have completely flipped from where it is today, and EM, in general, will be a hated and completely discarded asset class. That’s when it’ll be a good time to buy.

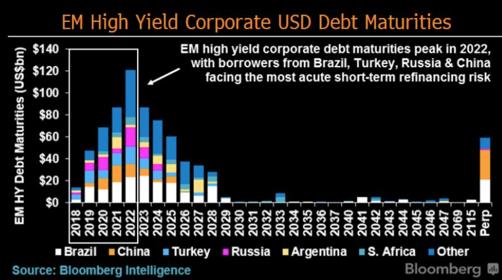

Lastly, here’s some good charts that show some of the headwinds EM is up against in the coming years.

A large amount of EM corporate high yield USD debt is maturing in the coming years. As the dollar continues to strengthen, the global dollar shortage will become more apparent and EMs will suffer for it.

(Image via Bloomberg)

(Image via Bloomberg)

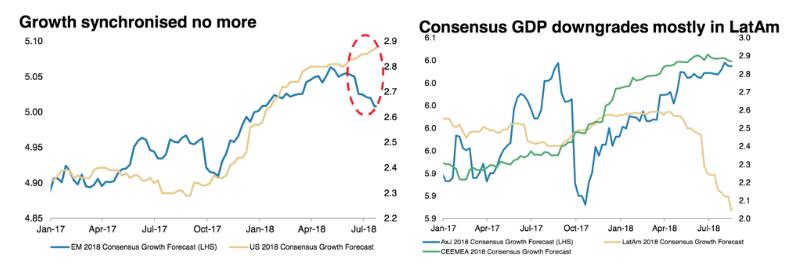

Global investors put money in EM stocks and bonds (which are generally seen as riskier) because they are chasing higher relative growth and thus, higher returns. When their growth is declining relative to that of DMs then there’s little reason for investors to invest in EM. This is part of the core-periphery paradigm (charts via MS).

Over the last few years, there’s been a huge amount of hot money flowing into EM equity and debt. There’s still plenty of capital that needs to be unwound.

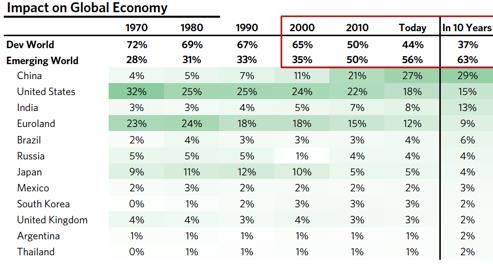

There’s going to be a reflexive global growth feedback loop in all this. EMs today make up a much larger share of global growth than they did 20-years ago. A slowdown in EM will drive a slowdown in developed markets which will reduce EM export growth, further constraining their ability to grow and so on.

(Image via Bridgewater)

(Image via Bridgewater)

(Image via Bridgewater)

(Image via Bridgewater)