EDR is an asset-light, resilient online-travel agency (OTA) rapidly growing its high-margin member subscription business while connecting the highly fragmented European airline travel industry. The company currently sports a 37% market share in Europe, 2.3x larger than its closest competition. It is also the world’s second-largest OTA by flight revenue, behind Trip.com.

COVID-19 was arguably the worst business environment EDR will ever see in its business lifetime. Yet during that time, the company expanded its market share by 600bps and grew its Prime Membership 55% YoY to hit 1M members, all without taking a single euro of outside funding.

Here’s the crazy part … Mr. Market’s current price assumes none of this positive growth actually happened.

The EDR bull thesis hinges on two simple but fundamental questions:

- 1) Will the industry (OTA) become larger or smaller post-COVID 19?

- 2) Will eDreams (EDR) become a larger or smaller player in the industry?

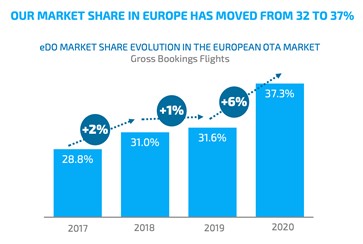

Here is what we know. First, there is tremendous pent-up demand for leisurely travel in Europe, which EDR’s own data verifies. Second, EDR gained 6% in market share during the COVID pandemic and is now a much larger player in the European OTA space.

Over the next five years, more members will choose EDR as their standard OTA thanks to its Prime Member Subscription service. EDR Prime Members receive the lowest-cost flights and discounts on hotels, car rentals, and more.

Mr. Market is oblivious to EDR’s market share gains and pent-up European travel demand. In fact, the stock currently trades at ~3.5x our estimate of 2026 EBITDA, representing a 29.4% yield.

Assuming a return-to-normal in leisure travel, further market share gains, and an increasing Prime Membership pool, we see a path towards EUR 2.68B in shareholder value, nearly 250% upside from the current stock price.

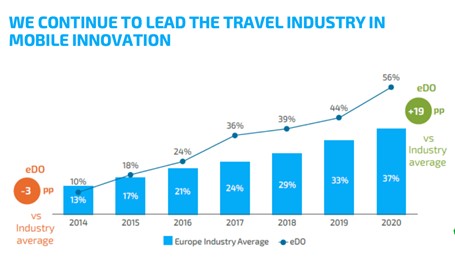

Leading The Way In Mobile OTA Flight Bookings

Europe’s airline industry is a highly fragmented concoction of 220+ airlines, with the top four airlines comprising only a 29% market share.

Such fragmentation makes booking flights, hotels, and general travel arrangements a nightmare. Contrast that to the United States, where its top four airlines equal 81% of the market share. In that instance, travelers have the luxury of coordinating with only a handful of potential airline candidates should they book independently,

This is why an OTA like EDR is so valuable in Europe. EDR’s mobile platform seamlessly connects travelers to the 220+ available airlines to coordinate flight times, airline choice, travel connections, and other must-have traveler information.

This is why an OTA like EDR is so valuable in Europe. EDR’s mobile platform seamlessly connects travelers to the 220+ available airlines to coordinate flight times, airline choice, travel connections, and other must-have traveler information.

No other European OTA comes close to EDR’s online penetration rates. Last year, the company booked ~56% of its flights through its online/mobile-first platform. The rest of the industry averaged a 37% mobile booking share. Moreover, EDR sports a 2.3x size advantage over its next closest competitor.

Thanks to COVID-19, more travelers will book online than anywhere else, placing EDR at the forefront of a new customer habit.

The company’s mobile technology platform isn’t the only reason we’re excited about this business. EDR’s secret sauce, the thing no one else in the industry is doing, is its Prime Subscription Business.

EDR’s Prime Subscription: Scaled Economies Shared

EDR is the only OTA with a Subscription-based membership offering. For ~EUR 60/year, members gain access to discounts on 100% of EDR’s flights, up to 50% discounts on lodging (hotels, etc.), an exclusive 24/7 customer service hotline, and the ability to book an entire family/group for the member-specific discount rate.

Memberships have exploded since its release in 3Q 2018, growing from 3K to over 1M. More importantly, Prime members now comprise nearly 40% of total flight bookings. EDR’s Prime membership has three distinct advantages:

- Lowers Customer Acquisition Cost (CAC) while raising Lifetime Value (LTV)

- Adds 100% margin subscription-based revenue stream

- Allows EDR to continually lower flight prices for its Prime Members

Prime Lowers CAC While Raising LTV

First, Prime membership reduces customer acquisition costs and raises lifetime customer value. This makes intuitive sense. Prime members receive the lowest-cost flights in the industry on roughly 90% of flights, so there’s no need to search any other OTA for that additional 10%.

These cost advantages make EDR the standard OTA of choice for travelers, resulting in higher mobile usage and lower incremental acquisition costs per booked flight. The below image highlights the cost savings for Prime members.

Prime Adds A ~100% Margin Subscription-Based Revenue Stream

The beauty of membership subscriptions is that its ~100% incremental margins drop straight to the bottom line. For example, EDR generates EUR 60/yr per prime member or ~EUR 1M in annual revenue at the current base. Today, the Prime business makes up ~10% of total revenues (assuming 2020’s FY figures).

Management has already said they’ll hit their internal goal of 2M Prime Members (from earnings call on May 27th, emphasis mine):

“And we are way ahead of schedule to hit our 2 million subscriber target, which we will likely meet a year ahead of schedule, latest by the end of summer 2022.”

In other words, EDR expects Prime membership to grow ~100% from now until next Summer. If they do that, they’ll generate ~EUR 120M in membership revenue. The company’s current market capitalization is only EUR 750M.

In other words, EDR expects Prime membership to grow ~100% from now until next Summer. If they do that, they’ll generate ~EUR 120M in membership revenue. The company’s current market capitalization is only EUR 750M.

This is where things get exciting for EDR, its customers, and shareholders. Let’s assume the company hits 2M subscribers by May-June 2022, and from there, grows ~35% per year till 2026. By that time, EDR would have ~6.64M Prime Members generating nearly EUR 400M in annual revenue. So you’re paying ~3x 2026E EV/Sales for the Prime membership business while getting all flight revenue for free.

Prime Allows EDR To Charge Lower Flight Prices

EDR’s Prime Membership is a fantastic example of Scaled Economies Shared. Here’s how it works. More members equal more significant amounts of 100% margin revenue. The company can then use that additional revenue to charge lower prices for its flights because it makes up that lost margin in its subscription business.

Cheaper flights incentivize more customers to join EDR’s Prime Membership. You can see the power of that flywheel.

Thinking About Prime Membership Revenues Going Forward

Over time, EDR’s Prime Membership allows it to charge the lowest prices for its flights while still making a positive net margin. How can any other OTA compete at that point?

Management has already said they’ll hit their internal goal of 2M Prime Members (from earnings call on May 27th, emphasis mine):

“And we are way ahead of schedule to hit our 2 million subscriber target, which we will likely meet a year ahead of schedule, latest by the end of summer 2022.”

In other words, EDR expects Prime membership to grow ~100% from now until next Summer. If they do that, they’ll generate ~EUR 120M in membership revenue. The company’s current market capitalization is only EUR 750M.

This is where things get exciting for EDR, its customers, and shareholders. Let’s assume the company hits 2M subscribers by May-June 2022, and from there, grows ~35% per year till 2026.

By that time, EDR would have ~6.64M Prime Members generating nearly EUR 400M in annual revenue. So you’re paying ~3x 2026E EV/Sales for the Prime membership business while getting all flight revenue for free.

EDR Poised To Capture Pent-Up Demand

As we mentioned earlier, EDR gained 600bps in market share from 2019 to 2020. With a 37% market share in Europe, the company is best-positioned to capitalize on the pent-up travel demands for 2022-forward. And if the US is a decent proxy, Europe’s rebound will be huge.

As we mentioned earlier, EDR gained 600bps in market share from 2019 to 2020. With a 37% market share in Europe, the company is best-positioned to capitalize on the pent-up travel demands for 2022-forward. And if the US is a decent proxy, Europe’s rebound will be huge.

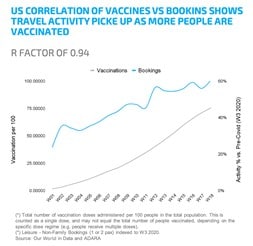

The company sees a 0.94R correlation between those vaccinated and the percentage bookings compared to pre-COVID levels. Put simply, more vaccinations equals more bookings (see below).

EDR’s top European countries have already surpassed the US’s speed of vaccination, and 36% of its core market has received at least one vaccination.

Thinking About The Range of EDR Outcomes

While it’s impossible to predict EDR’s future using 2020/early-2021 data, there are two ways shareholders can win big. First, at ~5.3x our estimate of 2024 EBITDA, the company is a logical take-private target for some of the larger online travel-based companies. The most prominent names include Airbnb (ABNB), Expedia (EXPE), and Booking.com (BKNG).

EDR’s two largest shareholders are private equity companies, Permira Advisers (27% ownership) and Ardian (16% ownership). Both PE companies will eventually want liquidity for their LPs and a decent ROI. This makes a buy-out the most logical outcome for EDR’s largest public owners.

Luckily shareholders don’t need a buy-out to generate an excellent return. Over time, the market will realize EDR’s tremendously unfair competitive advantage in its mobile platform, and Prime Subscription shared economic model. The company will continue to take market share by offering the lowest-cost flights and a seamless booking experience in a highly fragmented industry.

Analyst estimates for the next two years point to EUR 440M in revenue by 2023 with ~17% EBITDA margins (EUR 75M). After 2023, we’re assuming a 30% revenue CAGR with ~22% run-rate EBITDA margins (in line with historical averages). That gets us nearly EUR 1B in revenue and EUR 220M+ in EBITDA.

EDR has a EUR 770M market cap (EUR 6.80/share * 110M shares). Add in another EUR 500M in net debt, and you get EUR 1.27B in Enterprise Value. In other words, you can buy EDR today for ~3.5x our 2026E EV/EBITDA.

What would a reasonable buyer pay for this business? Let’s assume BKNG or ABNB wanted to take EDR private after five years. What multiple would they pay? The average EV/EBITDA multiple is ~15-17x. Assuming the low-end of that range (15x),, we’d end 2026 with ~EUR 2.68B Shareholder value (~EUR 26/share) or a 248% upside from the current price.

This valuation doesn’t come without risks. While the company didn’t need to tap credit markets during COVID, they are highly leveraged (~5x normalized Net Debt / EBITDA). The company has no short-term debt and favorable long-term debt covenants. As travel demand returns and Prime Memberships increase, EDR should have the cash to reduce its net debt burden if it wants.