From all us at Value Hive we wish you and your family a terrific Christmas Holiday!

Crazy to think that this newsletter is four months old. We’ve grown up so fast!

If you’ve got a long car ride to the in-laws, consider listening to our latest podcast episodes:

-

- Episode 2: Andrew Walker

- Episode 3: Thomas Bachrach

But it’s Christmas and we’re in the season of giving. Here’s what we got in store this week:

-

- Stan The Man’s Economic Predictions

- A Bottom’s Up Approach to Forecasting Revenues

- Buying Stocks For A Fraction

- David Flood’s latest illiquid idea

Onward!

—

December 25, 2019

Rally With Santa: If you’re a Value Hive reader, odds are you’ve heard the phrase “Santa Claus Rally”. That time of year when Santa makes it rain on your 401(k). We know its Wall Street jargon. But is there any actual evidence to back this up? Turns out, yes.

According to FINRA.org, “Since 1950, the index has delivered an average return of 1.4% in the last five trading days in December and the first two in January.”

If you’re interested in hearing more about the Santa Claus rally, the guys at Macro Ops and I did a video on it. You can find that here.

___________________________________________________________________________

Investor Spotlight: When The GOAT Speaks, We Listen

GIFs by tenor

GIFs by tenor

Stanley Druckenmiller is one of the greatest investors of all time. During his run at Duquesne Capital, The Druck generated over 30% annualized returns. That’s not a typo. The man is one of a kind. Druckenmiller sat down with Bloomberg’s Eric Schatzker to discuss monetary policy, 2020 outlook and his portfolio.

I listened to the entire interview and took notes so you don’t have to. In all seriousness, watch it.

You Get Liquidity, You Get Liquidity!

Druckenmiller points out that things are looking good in the United States. According to Druck, the economy’s fine and breadth indicators look solid. He also mentions improved global trade. On the China-US trade war, Druck said, “Everything isn’t peaches and roses, but things are de-escalating.”

Venturing beyond the US, Druck made the following observations:

-

- There’s fiscal stimulus in Japan and Britain

- There’s green stimulus in Europe

- There’s negative real rates everywhere and negative nominal rates in [many] countries

The former Duquesne manager believes we’re in a period, “of unprecedented monetary stimulus given the circumstances [around the world].”

This begs the question: Where does Druck have his money? I’m glad you asked.

A Look Into Stan The Man’s Portfolio

George’s former trading partner didn’t dive into company-specific names when asked about his holdings. But he gave us asset classes. Hints at where he’s parking his capital. On an absolute basis, Druckenmiller’s current portfolio is set for, “a benign economic outlook, and a benign market outlook.”

He stresses that his view could change tomorrow. And that’s what I love about the guy. He holds convictions but isn’t afraid to abandon them if he’s wrong. As of now, here’s what his book looks like:

Long Equities

-

- Increased exposure to stocks that will do well in a high-growth environment. Without naming companies, he mentioned Japanese equities (where have we seen that before?) and financials / banks.

- Druck’s words: “It looks more like a normal mix than a year ago.”

Long Commodities

-

- He’s long copper.

- Druck’s words: “I’m long copper because global economies will be better than IMF thinks. There’s also a kicker to copper. EV (Electric Vehicles) add around 0.50% a year to demand.

- He thinks he should be long energy.

- Druck’s words: “I don’t own energy, but I probably should. I just think there’s a real demand challenge.”

- He’s also on the board for Green Energy Defense.

- He’s long copper.

Currencies

-

- Long Canadian dollar, Australian dollar, NZD and MXN

- Druck’s words: “I’ve got some [short] pesos lying around somewhere.”

- Long British Pound heading into the election

- Druck’s words: “I had enough of a position to smile when I heard the news [of the election].”

- Long Canadian dollar, Australian dollar, NZD and MXN

Short Fixed Income

-

- Short longer-end of the yield curve and treasury market.

___________________________________________________________________________

Movers and Shakers: Customer-Based Revenue Models & Fractional Shares

GIFs by tenor

GIFs by tenor

Daniel McCarthy & Peter Fader’s piece on forecasting revenues was one of the best things I read all week. But then again, you can’t go wrong with Harvard Business Review’s material. The piece dives into a new way to forecast revenues via Customer-Based models. Let’s dive in.

Switching The Game

Customer-Based Corporate Valuation (CBCV) is better than other models. At least that’s the claim. The authors describe the model as, “a meaningful shift away from the common dangerous mindset of ‘growth at all costs’ toward revenue durability and unit economics.”

How does the model do that? By exploiting basic accounting principles, a CBCV valuation makes projections from the bottom-up. Not top-down.

But we need a few models to help us navigate the new method:

-

- The Customer Acquisition Model: Forecasts the inflow of new customers

- The Customer Retention Model: Forecasts how long customers will remain active

- The Purchase Model: Forecasts how frequently customers will transact with a firm

- The Basket-Size Model: Forecasts how much customers spend per purchase

These models help us understand the real drivers of businesses. This in turn allows us to project revenues with greater accuracy. While at the same time providing in-depth knowledge about the unit economics of any business.

That’s the key. The model works for all types of businesses. The article does note that CBCV method is easier with subscription-based models.

Let’s see it in action!

The Two-Step Model For CBCV Revenue Projections

There’s three steps to this method:

-

- Figure out total revenues from your retained customers

- Forecast amount of total revenue from new customers

- Add the two together

But we need to calculate steps one and two.

The formula for step 1 is simple:

-

- Multiply the current customer base by your historical retention rates

- Then, multiply that number by the historical average revenue per customer (ARPU)

Formula 2 follows a similar pattern:

-

- Multiply acquisition trend average by ARPU

Further Research Ideas

A customer-based method of valuation paints a clearer picture into two things:

-

- Drivers of revenue

- Unit economics.

The HBR article is the tip of the iceberg. The two men teamed up to write two academic papers, which you can find below:

I’ll dive into those this week.

Fractional Shares Hit Mainstream Brokers

Robinhood now offers fractional share purchases, joining Schwab and Square in the fun. There’s both good and bad consequences of fractional share ownership. As value investors, can we take advantage of this added wrinkle?

The Good: Spreading the Opportunity

Fractional shares is the latest effort to make stock ownership more universal. Jack Dorsey, CEO of Square notes that fractional shares, “make building wealth accessible to more people.” And that’s true.

Now, people that want to buy Amazon (AMZN) stock can. Even if they lack the thousands of dollars. There’s no doubt this move will send a wave of retail money into the markets. But at what cost?

We can apply similar logic to fractional shares as we did zero-commissions. On one hand, it’s great for retail traders. But on the other hand, does it encourage “dumb” money to enter the markets? And if so, is that a net positive to value investors?

The Bad: Dumb Money Climbs Higher

Fractional shares will increase the amount of “dumb” money markets. There’s also the argument that if someone can’t afford the average stock price ($67 – based on 2013 data), they shouldn’t be in the markets. Instead, they should park that money in a savings account.

While I’m not a financial advisor or financial planner (and I don’t play one on TV), there’s weight to that argument.

The Reality: It Doesn’t Affect Our Stocks

Yet at the end of the day, this is a net positive for the investment community. It opens doors to people that wouldn’t otherwise learn about financial markets. Most of all, this doesn’t affect the stocks that we look at. Small, illiquid, micro-cap names have no need for fractional share ownership.

___________________________________________________________________________

Resource of The Week: An Interview w/ Bruce Greenwald

GIFs by tenor

GIFs by tenor

Bruce Greenwald is a value investing legend. He’s author of Value Investing: From Graham to Buffett and Beyond. He also teaches at Columbia University.

Greenwald sat down with Tano Santos to chat all things value investing. Here’s a break-down of my favorite topics (from show-notes):

-

- The value investing oral tradition (10:30)

- Applying a value orientation to your investment search strategy (12:11)

- Why you need to be a specialist (13:24)

- What you can learn from Warren Buffett about specialization (14:56)

- Paul Hilal’s approach to investing by first spending the time to learn (16:28)

- How to approach the valuation of a moat business (24:11)

- The factors to consider when calculating your return (26:51)

- Why you have to pay attention to management behavior (30:48)

- The importance of active research for value investors (34:14)

It’s a tremendous interview.

___________________________________________________________________________

Idea of The Week: David Flood’s Latest Net-Net Idea

GIFs by tenor

GIFs by tenor

David Flood is a private value investor based in the UK. If you haven’t heard (or read) his material, check out these resources:

-

- Podcast with Stig & Preston

- David’s website, Elementary Value

I’m working with David to get him on our podcast. Details to follow!

NOL Stub Below Net-Cash

David’s latest write-up covered Origen Financial (ORGN). The company is small, $2M market cap. What’s interesting about it, you ask? According to David, the stock trades for a mere 0.75x net cash.

ORGN also has another thing going for it: NOLs. NOLs (or Net-Operating-Losses), shield any future income from taxes. You can also monetize them.

David estimates the company has around $15.6M in NOL on the balance sheet. Whether they monetize them or not is up for debate. What’s not up for debate is the discount to cash, and the reduced cash burn to $20K per-quarter.

The stock trades around $0.09/share with little volume. Oh, and 30% bid/ask spreads.

I’ll leave you with this quote from David (emphasis mine):

“On a per share basis if we include the marked down value of the NOL’s and the Net Cash I get a rough value of around $0.277 per share. Assuming we apportion no value to the NOL’ s then I get a rough value of $0.123 per share.”

___________________________________________________________________________

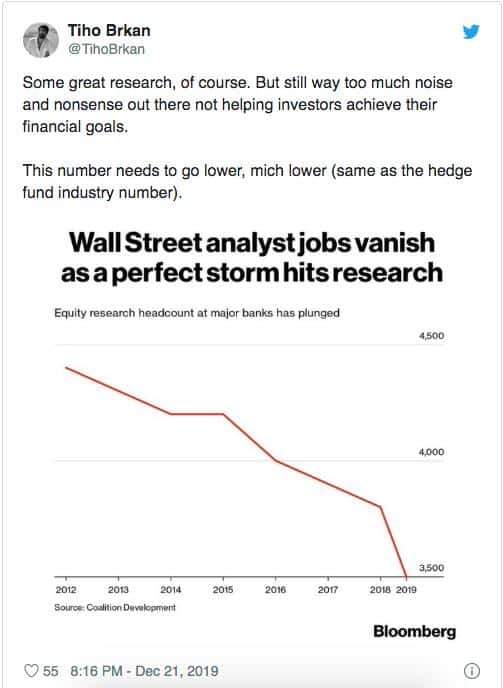

Tweet of The Week: Tiho Brkan on Wall Street Analysts

That’s all I got for this week. Shoot me an email if you come across something interesting this week at brandon@macro-ops.com. Have a great Christmas holiday.

Tell Your Friends!

Do you love Value Hive?

Tell your friends about us! The greatest compliment we can receive is a referral (although we do accept Chipotle burrito bowls).

Click here to receive The Value Hive Directly To Your Inbox!