Here’s a clip from a MO Collective trade alert I wrote back in May of last year on Disney (DIS).

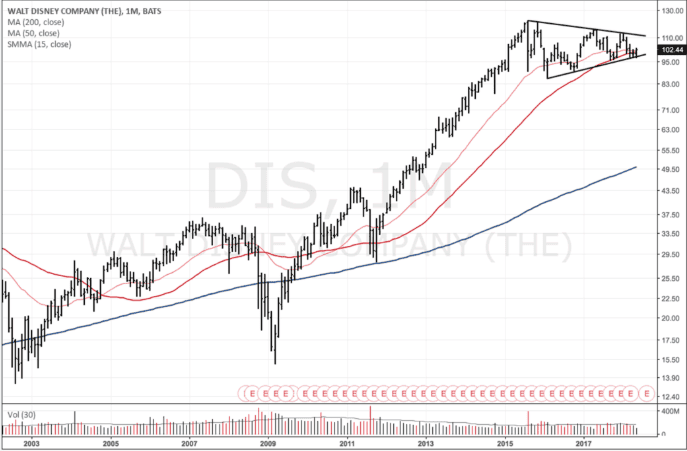

Today we’re putting on a large position in Disney (DIS). This is a trade I’ve been thinking about for a while. The chart is what first caught my eye. Here it is on a monthly basis, below.

That’s a beautiful looking 3-year coiling wedge. Long technical setups like these are some of my favorites to play as they usually precede explosive trends. They also offer us great inflection points with clear go/no-go price points in which to enter and place stops.

In addition to the great looking tape, Disney also has a very attractive developing fundamental story. The stock is trading at just 13x next year’s earnings and the company has been aggressively buying back shares. And after 3-years of little to no revenue growth, top-line numbers have begun accelerating higher again.

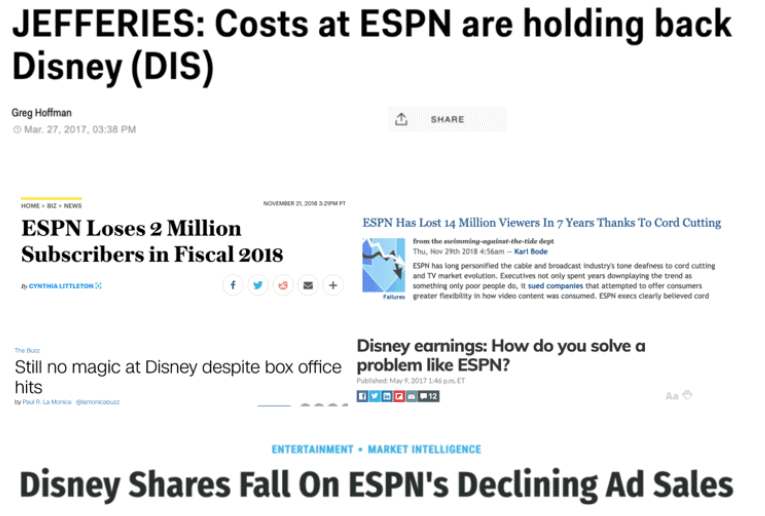

Disney is a classic case of the market latching onto a stale narrative and failing to see the changing fundamentals. The stale narrative in this case is the focus on a declining subscriber base in Disney’s media business (think ABC/ESPN), which the market is now valuing at just 2x EBITDA — which is kinda crazy…

This stale narrative was pervasive and common accepted knowledge amongst the financial media and Wall St. analysts.

Despite a clear positive inflection in the fundamentals — both income and revenues pivoted higher in the middle of last year — along with extremely positive catalysts in the company’s DTC SVOD plans, this narrative persisted and Disney’s stock price continued to languish.

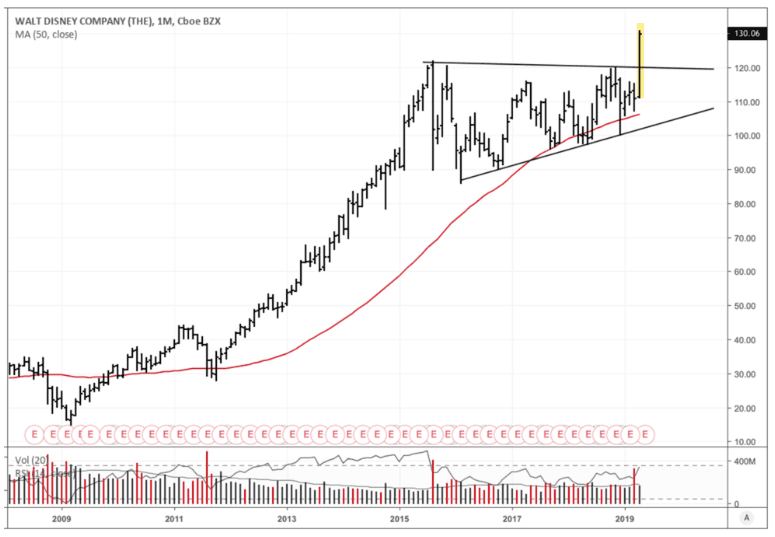

That is of course until last week when the stock finally gapped up and out of its 4-year trading range. This move has been accompanied by a complete and total shift in the popular narrative from “Disney as an out of touch legacy media business with a gangrenous ESPN division” to “Disney is a Netflix killer and the new hot growth stock”.

The only notable cause of this shift was Disney’s Investor’s Day the day prior to the breakout (here’s the link to the presentation and slidedeck). But hardly anything new was announced at the event other than frivolous details. Pretty much all of it was a rehash of what the company’s been communicating for the last 18-months and yet here we are, not only has the narrative changed but so has the trend in price.

What’s going on?!? Why do markets do this time and time again where they ignore the obvious shifting landscape and instead willingly latch onto bygone narratives that no longer reflect reality?

Let’s discuss…

In our December 2017 MIR I included the following section from Yuval Harari’s book, Sapiens (emphasis mine):

Sapiens rule the world, because we are the only animal that can cooperate flexibly in large numbers. We can create mass cooperation networks, in which thousands and millions of complete strangers work together towards common goals. One-on-one, even ten-on-ten, we humans are embarrassingly similar to chimpanzees. Any attempt to understand our unique role in the world by studying our brains, our bodies, or our family relations, is doomed to failure. The real difference between us and chimpanzees is the mysterious glue that enables millions of humans to cooperate effectively.

This mysterious glue is made of stories, not genes. We cooperate effectively with strangers because we believe in things like gods, nations, money and human rights. Yet none of these things exists outside the stories that people invent and tell one another. There are no gods in the universe, no nations, no money and no human rights—except in the common imagination of human beings. You can never convince a chimpanzee to give you a banana by promising him that after he dies, he will get limitless bananas in chimpanzee Heaven. Only Sapiens can believe such stories. This is why we rule the world, and chimpanzees are locked up in zoos and research laboratories.

We are genetically programmed to buy into the popular narratives that are shared by the crowd.

The German Physicist Max Planck quipped that “A new scientific truth does not triumph by convincing its opponents and making them see the light, but rather because its opponents eventually die, and a new generation grows up that is familiar with it”. This is where the saying “science advances one funeral at a time” comes from.

I think a similar dynamic plays out in major trend changes and popular market narrative shifts. And no, I’m not implying that new trends are caused by investors dying off. Rather, it’s that narratives eventually exhaust themselves by driving every seller who is going to sell, to sell, or vice-versa for buyers in a bullish narrative.

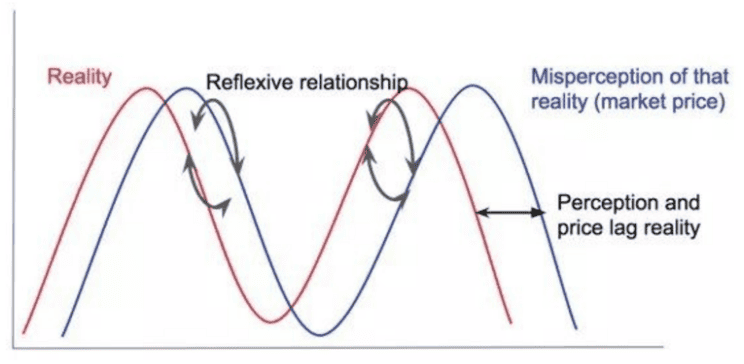

Price and narratives work in a reflexive relationship where both drive each other in a continuous and cyclical boom/bust process throughout multi-fractal timescales. The diagram below shows what this process looks like.

Since the two are self-reinforcing and all market participants suffer from cognitive shortcomings such as anchoring and confirmation bias, the availability heuristic, and so forth. It’s only natural that narrative and price trends would continue on well in advance of their past-due date — Tesla being an obvious current example of this.

There’s a research paper titled “Memetics Does Provide a Useful Way of Understanding Cultural Evolution” (h/t Jim O’Shaughnessy) which dives deeper into how narratives (aka, memes) spread. It’s a super interesting paper and I suggest you read it in full (here’s the link).

The paper discusses the origins of the term ‘memetics’. A word coined by Dawkins in his landmark book The Selfish Gene. Dawkins argued that “Darwinism is too big a theory to be confined to the narrow context of the gene.” He believed in Universal Darwinism as a general principle where whenever information, in any form, is “copied with variation and selection, then you must get evolution.”

The paper goes on to posit that memes, a word that stems from the Greek root mimēma which means “that which is imitated”, and can be thought of as the cultural transmission of packets of information, are not only the evolutionary force behind human culture (i.e., language, art, music etc…) but might have been a fundamental driving force behind human physical evolution, as well.

Essentially, what this means, is that we humans physically evolved to be optimized for imitating one another and transmitting memes. The paper notes that in line with this “prediction is that the parts of the human brain that maximally increased in size should also be those involved in imitation, and this has been confirmed by brain scanning studies (Iacoboni et al 1999).

Here’s a section from the paper which lays out exactly what all this might signify (emphasis by me).

A common objection to memetics is that it undermines human autonomy and the creative power of consciousness, and treats the human self as a complex of memes without free will. These ideas follow naturally from the universal Darwinism on which memetics is based. That is, the idea that all design in the universe comes about through the evolutionary algorithm and is driven by replicator power. This means that human creativity emerges from the human capacity to store, vary and select memes, rather than from some special creative spark, or power of consciousness (Blackmore 2007). The human self may also be a construct of memetic competition, surviving because it protects and propagates memes, including the many memes that make up a person (Dennett 1995). In this view the self is not a continuously existing entity with consciousness and free will but is a persistent illusion. This memetic view of human beings as the evolved creation of two replicators may be unsettling but it has the advantage of uniting biological and human creativity into one, and providing new ways of understanding human nature, self and consciousness.

This is kind of heady stuff and I’m not sure I fully believe in it but the concept is an interesting one and certainly has descriptive power for how we act in the aggregate.

Moving back to how we can think about this on a more practical note. Jim O’Shaughnessy I thought did a good job of summing up the intersection of memetics and markets in a recent tweet. He said “In non-academic speak: Many times, markets move from heterogeneous to homogeneous caused by consistent information cascades that compel people to copy other’s behavior. For example, after writing a scathing paper on the prospect of internet stocks, I founded an internet Co.”

Essentially, few things are more compelling than a popular narrative. It’s tough, if not outright impossible to completely remove ourselves from the ‘Herd’. We’re all a part of this Grand Collective Intelligence and are literally wired at the genetic level to be so.

This is why popular market narratives can persist — and often do — well past the point of no longer describing reality. Memes have a momentum all their own. And it often takes repeated bludgeoning from reality for them to die off and be replaced with a new one.

As participants in this game who are all equally susceptible to the same pull and sway of memes, all we can do is remind ourselves of our cognitive foibles, try to stand back and observe the observer, and continuously stress-test our opinions against the data and the market.

Studying the trading greats, you find that nearly all of them had an uncanny ability to get outside themselves and more objectively view their thinking. George Soros put it like this.

I am outside. I am a thinking participant and thinking means putting yourself outside the subject you think about. Perhaps it comes easier to me than to many others because I have a very abstract mind and I actually enjoy looking at things, including myself, from the Outside.

And in order to help combat the pull of popular market memes, he would begin his research from the starting point that the market was wrong. Soros said:

The prevailing wisdom is that markets are always right. I take the opposite position. I assume that markets are always wrong. Even if my assumption is occasionally wrong, I use it as a working hypothesis.

So that’s that.

For those of you wishing to dig more into memetics after reading the above paper, I’d recommend picking up The Diffusion of Innovation by Everett Rogers. It’s essentially a textbook on how ideas spread and there’s an extremely useful concept in it called The Adoption Curve (here’s a short Youtube video overview) with obvious applications to markets (I plan to write more on this soon).

Lastly, if you’d like to dig more into Disney and the new direction the company is headed in, then check out Ben Thompson’s latest Stratechery write-up (link here) and, of course, Matthew Ball’s recent work (link here).