The Palindrome (Soros) once said, “The generally accepted view is that markets are always right — that is, market prices tend to discount future developments accurately even when it is unclear what those developments are. I start with the opposite view. I believe the market prices are always wrong in the sense that they present a biased view of the future.”

George Soros on Markets

That last part is very important. Do you know what Soros means when he says the market is wrong because it’s biased about the future?

I’ll tell you. It’s an important concept to understand. And a helpful mental model to use in today’s choppy market action.

The market is supposed to be a forward discounting machine. It’s supposed to look out into the near future and make judgements on things like revenues, margins, earnings, inflation, the discount rate, potential risks, geopolitical shocks etc… and then make bets on what the proper value (the price paid today) is for those future cash flows.

That’s no easy task… it’s a lot of things to take into consideration. The market and economy is a complex beast. There’s a lot of unknowns and unknown unknowns. And like the great sage Yogi Berra once said “It’s tough to make predictions, especially about the future.”

To top things off, we (as in, we humans) abhor uncertainty. We can’t stand it. It drives us bonkers. Especially if it’s uncertainty surrounding something that’s a strong emotional trigger — like our finances or the stock market.

So here we have a problem. The future is hazy. The market is complex. The future path of the stock market is hazy and complex, i.e. it’s uncertain. Humans hate uncertainty. Round peg + square hole.

But the human mind is inventive when it needs to be, especially with the right incentives. Like making a lot of money in the stock market.

So to get around this seemingly intractably uncertainty-judgement issue, the majority of market participants simply extrapolate the present into the future. They take the hard numbers; the revenue growth, margin trends, and current cash flows. And just extend them out a few years. Boom… problem solved… no more uncertain future. Good earnings today = good earnings tomorrow. Money in the bank.

This is called anchoring. It’s a cognitive bias where we overweight the first or most easily available information when making judgements. It’s a useful heuristic and works pretty well, most of the time. Especially in markets. Financial and economic data tends to trend once it gets going. Kind of like Newton’s First Law.

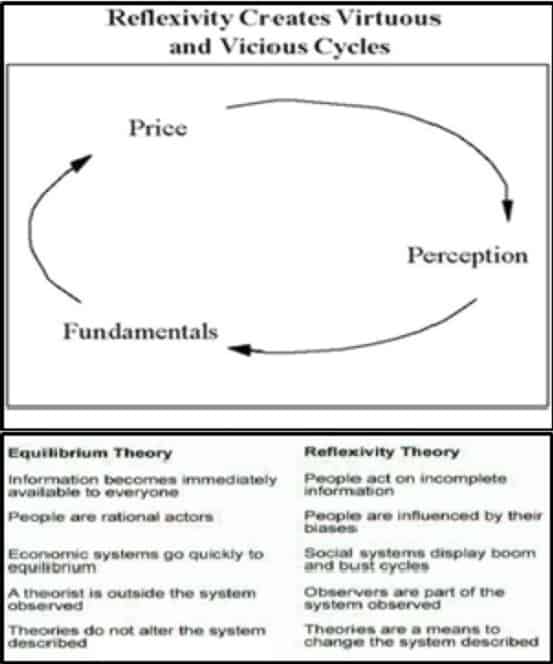

The problem is, markets are reflexive. Meaning, our observations of the market affect the market itself, which in turn affects our observations and so on. Do you smell what I’m cooking?

George Soros on Reflexivity In The Market

This manifests itself in situations like the following.

The longer we see positive earnings growth, the more market participants begin bullishly extrapolating this earnings growth into the future. This results in the buying of more stock, which drives valuations up, and thus creates a market that’s now more incentivized to maintain and propagate the bullish narrative… and more importantly, slap on cognitive blinders to new info that may threaten this narrative.

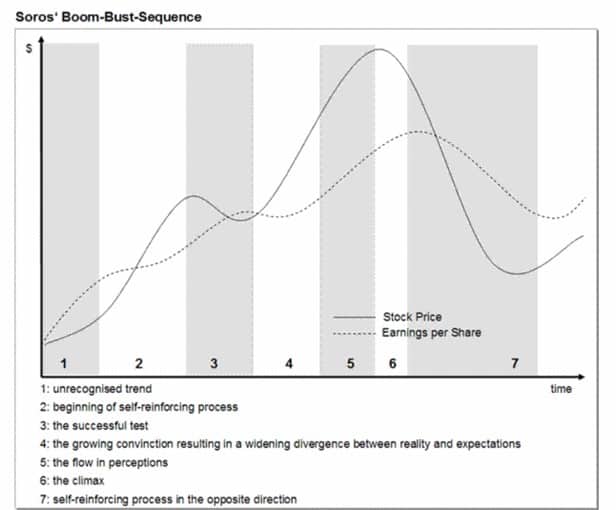

Soros’ Boom Bust Sequence

So the narrative and the market form a self-sustaining feedback loop that goes on and on. It occasionally gets tested by disconfirming evidence. Each test it survives, the stronger the reflexive relationship becomes. As each dip bought leads to more confidence that so to will the next one and the one after that. Extrapolation ad infinitum…

This is why Soros said the market is always wrong because it presents a biased view of the future. The market is always biased in the direction of the established trend. Because it utilizes anchoring and extrapolation to form judgments instead of objectively and equally measuring the weight of available information.

And like I said, this works most of the time. But when it doesn’t, it really doesn’t…

As traders, we always need to be cognizant of the trend. As well as the key data points that are the foundations of the driving narrative of that trend. But we also need to objectively look out into the future to see if any freight trains are headed our way that could derail the narrative.

Just the process of gaming numerous potential scenarios is a valuable exercise as it keeps our minds fresh, open, and unwedded to a single narrative or outcome.

Market Wizard, Bruce Kovner, attributed this process as one of the main reasons behind his enormous success. He said:

I’m not sure one can really define why some traders make it, while others do not. For myself, I can think of two important elements. First, I have the ability to imagine configurations of the world different from today and really believe it can happen. I can imagine that soybean prices can double or that the dollar can fall to 100 yen. Second, I stay rational and disciplined under pressure.

What we’re talking about here is playing the game at Keyne’s second and third levels… Playing the player… Understanding what the market is focusing on and what exactly is being priced in. Then weighing that against the incoming data and gaming alternative futures to the one the market is focused on and thinking about what catalysts could trigger a phase shift.

Is this easy? No, of course not.

But there are a number of tools and models we can use to make this scenario gaming a more fruitful exercise. One of these is to focus on the second-derivative of data. That’s the trend in the rate of change instead of the trend in the absolute number.

This is important because trends lose steam before they turn. The market focuses on the growth — it wears the bullish blinders — while we want to keep our eyes peeled for a potential slowdown, or a change, in that growth. This will tip us off to a coming trend change in the data. A trend change that could destroy the narrative and cause a phase shift.

This is why we look at year-over-year data versus absolute numbers. It’s not the absolute level it’s the relative rate of change over time that matters.

Soros’ Boom Bust Framework

Every bubble has two components: an underlying trend that prevails in reality and a misconception relating to that trend. When a positive feedback develops between the trend and the misconception, a boom-bust process is set in motion. The process is liable to be tested by negative feedback along the way, and if it is strong enough to survive these tests, both the trend and the misconception will be reinforced.

If a self-reinforcing process goes on long enough it must eventually become unsustainable because either the gap between thinking and reality becomes too wide or the participant’s bias becomes too pronounced. Hence, reflexive processes that become historically significant tend to follow an initially self-reinforcing, but eventually self defeating, pattern. That is what I call the boom/bust sequence.

Boom And Bust Meaning

Two trends are always interacting with one another, in a reflexive loop. One trend is reality and the other is a misconception of that reality. As global macro traders, we need to focus on both. And the best way to view “reality” is by measuring it at the second derivative level.

You now know what the market’s potential misconception is. As well as how growth-trends are unfolding.

There are a number of sizable trends that are about to develop… along with massively asymmetric trades that are soon going to catalyze.