Hyman Minsky is a classical go-to regarding boom-bust cycles, credit growth and financial (in)stability. This essay is a refresher on how credit cycles work and how we can apply Minsky’s framework to understand such cycles.

What is a Credit Cycle?

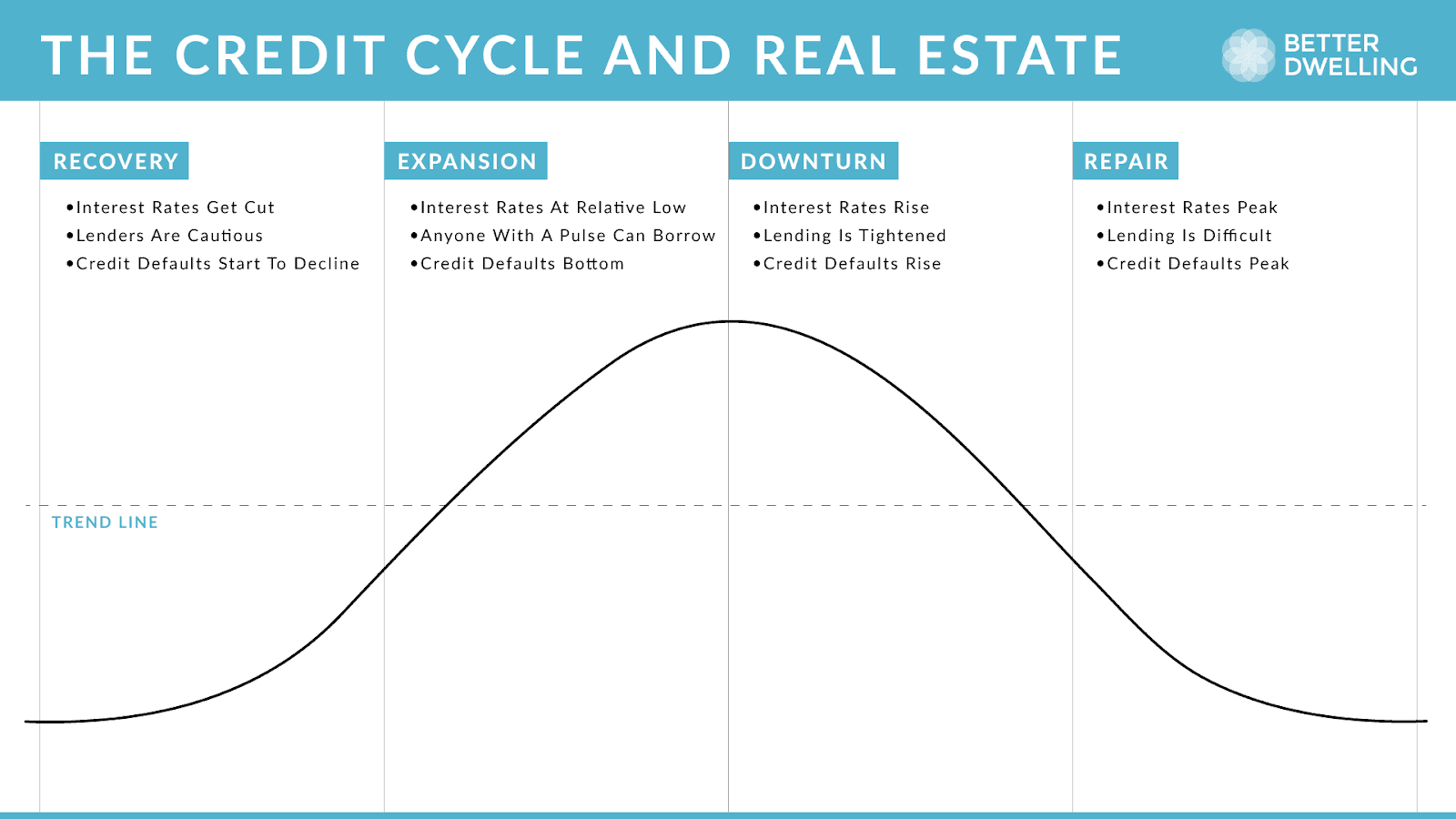

A credit cycle explains the availability and supply of credit to willing borrowers. The cycle begins with a period where funds are easy to borrow. Banks are more inclined to take on risk, generate additional returns and so on. They have lower interest rates, lower credit requirements etc.

Increased credit leads to increased risk on bank balance sheets, as well as a potential increase in inflation.

This forces banks to raise rates, requirements etc. Eventually, expectations around income growth decline, which triggers increased defaults, which then leads to tighter credit. Lather, rinse, repeat.

Credit Cycle Chart

As Warren Mosler discusses in Soft-Currency Economics, banks lend when they want to lend, without regard for the Federal Reserve’s actions. They will then borrow reserves in the interbank lending markets.

Where this gets interesting is how credit impacts valuations. This credit impact leads to vicious self-reinforcing feedback loops.

The Credit-Asset Feedback Loop

It is important to remember that the purpose of borrowing is usually consumption, or investment – i.e. some form of demand/spending. One man’s spending is another man’s income. If I pay you $5 for bread, you now have $5 to spend on whatever you want..

Assets are typically valued on cash flows. More specifically, the present value of those future cash flow streams is discounted at some appropriate interest rate. –

We see more borrowing in low-interest rate environments.. This affects asset values in two ways:

- The higher borrowing leads to higher spending which leads to higher incomes (that filter down to cash flows)

- The interest rate remaining low may have an impact on the discount rate

This causes a natural rise in asset value (rising tide lifts all ships, kinda deal). To a lesser extent, the impact is brought singularly around by leveraged speculation, where the purchase of assets is brought around by higher borrowing.

However, this also possesses a self-reinforcing mechanism. The rise in asset prices causes collateral values to rise, which in turn leads to elevated credit extension.

This then causes spending to rise, and this causes asset prices to rise. This creates another self-reinforcing loop until interest rates rise, collateral requirements rise or some sort of event forces greater delinquencies. We’ve seen various cases of this behavior.

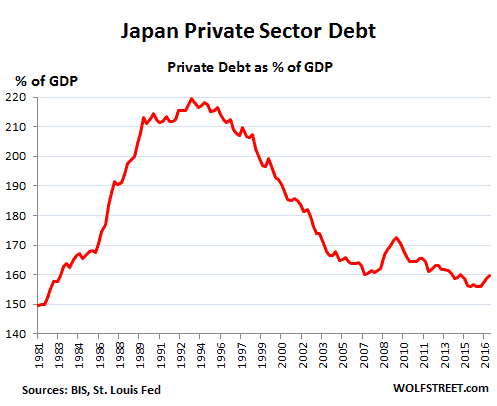

The Japanese Experiment, the 1980’s

Japan had a policy of window lending, where the Bank of Japan would handpick which sectors/industries received funding. This led to various issues across Japan and some ridiculous valuations. For example, the Imperial Palace in Tokyo was worth more than the entire state of California.

The Japanese government had put together an incentive structure that fostered “investment”, speculation and easy access to credit. This led to excessive access to credit. Here’s a great chart showing what happened:

The cycle broke when the BoJ tightened, and asset prices had collapsed by 1992. The decline in asset prices brought various problems, including the high rate of NPL (non-performing loans) for various financial institutions, and the government stepped in to begin the process of what is widely known as the “zombification” of Japanese companies.

Who was Hyman Minsky?

Hyman Minsky was an economist with unorthodox ideas. Ideas about the importance of a central bank playing the role of lender of last resort, while stressing against the dangers of over-accumulating private debt in financial markets.

Some of his ideas can be found in Why Minsky Matters by Randall Wray. Here’s an example of one of his “unorthodox” ideas:

“Minsky’s extension was to add the financial theory of investment, stressing that modern investment is expensive and must be financed—and it is the financing that generates structural fragility. During an upswing, profit-seeking firms and banks become more optimistic, taking on riskier financial structures. Firms commit larger portions of expected revenues to debt service. Lenders accept smaller down payments and lower quality collateral.”

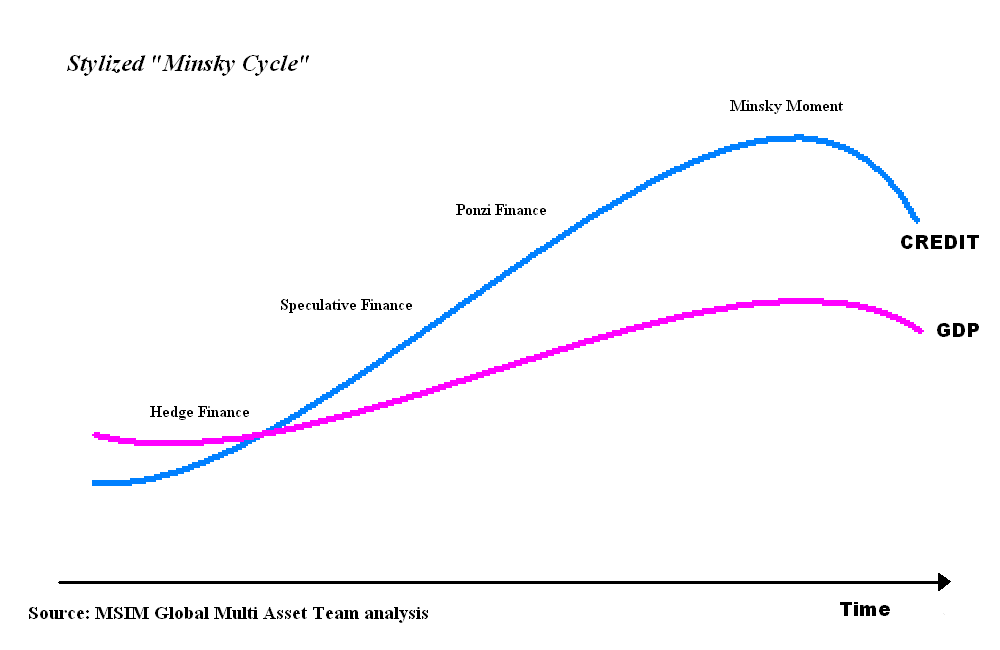

Minsky Cycles

Minsky’s cycles can be stylized to the following diagram:

The important part is his simple idea of how stability breeds instability. The issue with stability is it changes expectations, which leads to substantial changes in lending. People have a tendency to extrapolate recent events far into the future. If we haven’t had a recession recently, people will assume the good times will continue.

This means people (and banks) are more eager to borrow. Banks assume the periods of stability continue and are willing to make riskier and riskier loans. The scene of the housing market is “rock solid” in The Big Short comes to mind.

A Minsky Moment

Eventually, this comes to a “Minsky Moment”, and it begins to unravel – and defaults rise. Banks cut back risk, and this slowly feeds on itself till the Federal Reserve (or other central banks) step in or the government steps in to help the financial system remain solvent – this phase of the business cycle is what scared Hyman Minsky so much, that he issued warnings against high levels of private debt.

Now, where are we at the moment? It’s a lot harder to tell where we are while looking at the windshield – and some part of the Fed’s policy is reacting to inflation caused by higher demand as well as supply constraints.

At this point, it becomes more debatable, but yet we’re seeing the housing market pulling back a bit more, as well as revolving credit (shorter-term loans, etc) is expected to decrease.