The recent bullish action in the markets makes it fitting that we play devil’s advocate – something we at Macro Ops refer to as “Red Teaming.”

We’ve been bearish when it comes to the overall markets for about a year now. And we still believe the bearish hypothesis is the most probable outcome. But the unrelenting retracement in credit and equities over the past month forces us to investigate the bull position – one must always respect price.

Our team at Macro Ops usually view markets through the lens of liquidity (e.g. cost of money + spreads). The liquidity model we built has predicted future market returns to a remarkable degree, but our modeling has become more convoluted now that interest rates are near zero and the real cost of money is negative. There isn’t much past data we can use to evaluate this type of environment (other than the Great Depression). What’s more, this environment makes game treeing policy decisions a tough code to crack, since actors have more incentive to take extreme measures in both directions. So although our model is still sound, it’s prone to give off false signals. Put another way, it’s hard to determine with full confidence where the market ends up 6-9 months from now.

In 2014 the U.S. began a short-term tightening cycle when the Fed started cutting QE. This tightening is not only evident in the Wu-Xia shadow rate but also in wider junk bond spreads and a stronger dollar. Most tightening cycles like this one run until the economy starts heating up again and there’s a shift back to short-term easing.

But there are some exceptions to this rule. And this cycle could be one of them. The problem with this recent tightening cycle is that it was sparked by ideological reasons, NOT because the economy was redlining with rising inflation. The way the fuse was lit may lead to its shortened duration.

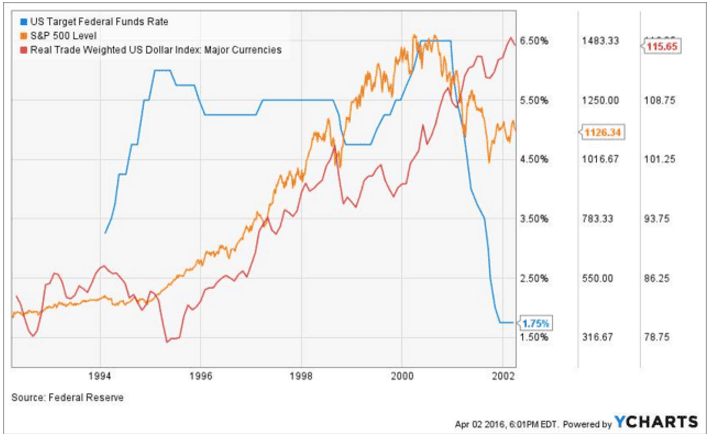

An economic parallel (though nothing close to perfect) is the mid-to-late 90’s. During this time, Greenspan raised rates from ’94 to mid ’95. He then held them steady before gradually cutting them by 125 bps until early ’99.

During this period, the dollar, which was on a tear, experienced an abrupt retracement. Speculative debt rebounded and temporarily increased liquidity. The market shot up, forming the tail end of what became a blow-off top. This was all before rates were raised again to control an overheating market – leading to the crash.

The initial reluctance to follow through on tightening is what elicited an aggressive bull charge in the late 90’s. So the question today becomes, are we easing too soon yet again and falling for the same thing twice?

During the last Fed meeting, Yellen had some very dovish comments and cut the forward guidance on the rate path in half.

There is speculation that at the last G20 summit, Europe, China, Japan, and the U.S. formed a “Stealth Plaza Accord” – potentially agreeing to turn the dollar around and keep it in a “sweet spot”.

This would ease conditions in China (whose currency is pegged to USD), relieve pressure on commodities (and therefore commodity producing countries), and ease global credit conditions (since the Fed is basically the world’s central bank).

Japan and Europe would partake in the accord because they are equally terrified of the tightening impacts of a rising dollar and the threat of a Yuan devaluation – which, as asset manager Hugh Hendry noted, would throw the world into a “Mad Max-like situation”.

Whether this “Stealth Plaza Accord” actually occurred is anyone’s guess. Then again, how could these topics not be discussed by world leaders? The U.S. dollar could simply be retracing because it was long due for a correction. Either way, the results are the same: markets, commodities, and emerging market equities all have rallied.

So if the “data-dependent” Fed is easing with current inflation numbers, the next question becomes, how much will Yellen let inflation redline? Our guess is that with her history of decisions, she’ll keep the needle in the red.

Could this temporary easing in conditions muster enough strength to launch the markets to new highs? There’s no way to know. But if the S&P (NYSEARCA:SPY) has a weekly close above 2100, we wouldn’t hesitate to place some bets to the long side. If the S&P hits new highs, there’s actual potential that the market shoots vertical (for a short period) in a buying spree that creates a 2000-style blow-off top.

But this short-term bullish scenario doesn’t alter the long-term bearish outlook on the market. Truth be told, it makes the bearish case even more severe. The equilibrium disparity between market valuations and future returns will only balloon, increasing the likelihood of a much larger dislocation in the future (i.e. more painful market crash).

Greenspan was rightfully derided for juicing the markets to excess in the 90’s. Back then, Yellen was actually goading him to ease more. So it’s not by any means a stretch of the imagination to think Yellen can out-Greenspan the man himself.

During the 2000’s, the bubble was primarily confined to tech. But this time it’s ubiquitous. What followed the tech unraveling was a deliberate inflation of the housing bubble (just like Krugman called for). But what’s left to inflate this time around when markets crash?

If the running of the bulls does start up again, we’ll hop on the Soros-style false trend and profit (with very tight risk-management, of course).