If you’re reading this, congrats! You survived your New Years Eve party. We’re excited for the new decade at Value Hive. In four months we’ve grown our subscriber base, started a podcast and solved world hunger met tons of interesting people.

Our goal for the next decade is simple: Deliver curated, value investing news straight to your inbox. For free. Forever.

Before we dive into this week’s issue, check out our latest podcast episodes:

-

- Episode 4: Callum Laing

- Episode 5: Darren Fong

Here’s what we got in store this week:

-

- Steven Wood’s Plan For 2020

- Machines Beat Analysts

- Cyclical Stocks Win Big

- Value Investing in Japan & Europe

Let’s get after it!

—

January 01, 2020

New Year New Me: We didn’t always celebrate New Year on January 1. In fact, our ancestors celebrated at a much different time. Here’s your first trivia question of the new decade … What date did people celebrate New Years before we switched to January 1?

This is the hardest one yet, so good luck!

___________________________________________________________________________

Investor Spotlight: Greenwood’s Purpose Driven Decade

GIFs by tenor

GIFs by tenor

Steven Wood ended 2019 with an inspirational call-to-action. The end of 2019 marked a full decade of Greenwood’s business history. Steven’s ringing in the New Year with a defined mission statement and purposeful vision.

The Catalyst He Always Wanted

Steven reaffirmed Greenwood’s purpose and goals for 2020 in his latest blog post. Here’s the mission statement:

“Our purpose is to be the catalyst that helps our investors, companies and team members perform at the top end of their range of possibilities.”

Most retail investors can’t enact change within a public company. A 5% position in a $5M nano-cap company requires a $250K investment. That’s a lot of money for retail investors.

But there’s one part of Steven’s mission statement weekend warriors can use. It’s the idea of thinking in possibilities, not binary outcomes.

Thinking In Possibilities

Stocks are ownership shares in actual businesses. Because of this, there’s a myriad of outcomes that can arise over time. When analyzing a stock, you should think of the various downside and upside potential. Suggesting one downside case and one upside case isn’t enough.

There’s a few ways I’ve added possibility-analysis into my process:

-

- Run multiple DCF and EV/EBITDA valuation models

- Look at the ranges a stock has traded in the past

- Read more bear thesis write-ups on my long ideas

Where Steven Wants To Enact Change

Steven mentions three companies in his year-end blog post:

-

- TripAdvisor (TRIP)

The stock is at its lowest level since 2013. The last time the stock was here, it shot to over $100/share. I’m not saying that will happen this time. But it’s worth thinking about.

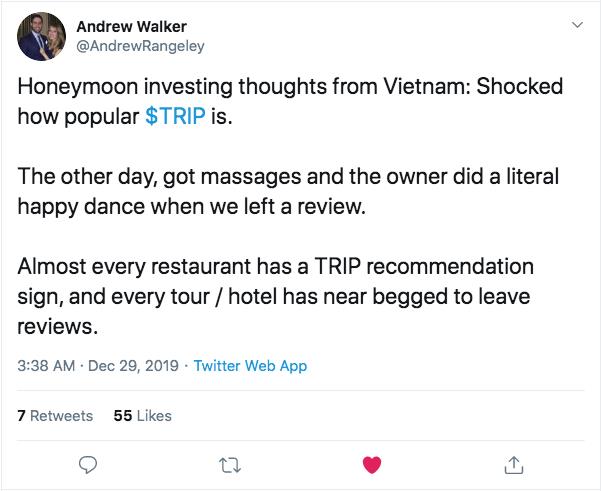

Steven isn’t the only value investor thinking about TRIP. Andrew Walker (@AndrewRangeley) tweeted his thoughts on TRIP after his honeymoon to Vietnam:

The stock trades for 36x current earnings. Expensive on the surface, I know. But looking a year out, the company appears cheap at 16x earnings and 7.5x EBITDA.

-

- Rolls Royce (RR.)

Rolls Royce (RR.) stock hasn’t moved since 2012. The S&P’s up over 140% in the same time frame. Not good! What’s to blame for the laggard performance?

RR isn’t operating well. Here’s the lowlights of the last year’s performance:

-

- Gross margin down ~10%

- Operating Profit down from $1.1B to -$1.1B (7% to -7% margin)

- EPS down from $1.89 to -$1.21

- ROA down to -8% (from 12% in 2017)

Revenues continue to grow. It’s gross profit and operating profit that are the problem. If Steven can fix things at RR, he should see handsome profits.

It wasn’t that long ago when RR generated near $1.5B in operating profits (2013).

-

- Short Boeing (BA)

Boeing’s another stock that’s gone nowhere over the last two years. The stock trades within a well-defined (tight) range. Steven’s short BA for a plethora of reasons, which you can find here. He’s also a public critic of BA’s management change:

___________________________________________________________________________

Movers and Shakers: Robots Win & Cyclical Stocks Outperform

GIFs by tenor

GIFs by tenor

If you’re a Wall Street analyst at a big investment bank, you may want to skip this section. An MIT forecasting model produced better sales projections than human analysts. This isn’t surprising. And we’ll see why this is a good thing for value investors, like ourselves.

MIT Model: 1 – Humans: 0

MIT is at it again. This time their research team developed an automated model to forecast business sales.

In true Dwight vs. Computer fashion, MIT went head-to-head with human analysts. The results weren’t pretty for us humans.

The task: Predict earnings of more than 30 companies

The result: Model outperformed combined analyst estimates 57% of the time

Here’s the kicker. The computers worked with less data than their human counterparts. The analysts had access to alternative data. Such data included:

-

- Credit card purchases

- Location data from smartphones

- Satellite images of retail parking lots

The computers only had access to public information. And they outperformed the analysts.

This makes me wonder … how much value-add is this ‘alternative data’ if it fails to beat a computer using public data?

What This Means For Analysts

It’s clear that computers can perform most tasks better than humans. Yet when it comes to investing and analysis, it’s hard to find places computers don’t have an edge. But there are places where humans remain advantaged. They include:

-

- Small, private market businesses

- Micro-cap and nano-cap public companies

- Illiquid/dark/grey stocks

Stay in these markets and you won’t have to worry about computers taking over. These markets don’t have adequate data to feed models. The information arbitrage advantage endures.

Verdad Capital: Contrarian Investing in Cyclicals

Blackstone, KKR and Texas Pacific Group. What do these PE funds have in common? They all made stupid money buying cyclical, commodity companies at the bottom of a cycle.

Verdad Capital’s newsletter offers a couple examples:

-

- Blackstone’s $640M investment in Celanese (returned 4x)

- KKR & Texas Pacific Group’s power plant investment returned 6x original price in less than a year

Buy … High? Sell … Low?

Cyclical companies are a bit different. They’re cheap when they look expensive. And they’re expensive when they look cheap.

In other words, cyclical stocks will trade for higher multiples at the bottom of a cycle than at the top. Let’s pick up from Verdad’s letter (emphasis mine):

“For example, when oil prices were below $37 a barrel (bottom quartile), Exxon traded at an average multiple of 8.2x, but when oil prices were above $88, Exxon’s EBITDA multiple fell to an average of 5.7x. Similarly, when the number of new homes under construction was below 772,000 (bottom quartile) DR Horton and Lennar traded at average multiples of 21.7x and 34.5x, but they reverted to 8.1x and 9.4x respectively when the number of new homes under construction surpassed 1,072,000 (top quartile).”

This is important to understand. As value investors we have a tilt towards investing in low P/E or low EV/EBITDA companies. Yet with cyclicals, we need to reverse that thinking.

How To Take Advantage of Cyclicality

Verdad offers clues on how to profit from these industry cycles, saying “While investing in cyclical industries ten years ago would have been a poor decision, our research suggests some opportunities may exist today.”

Verdad sees opportunity in semiconductors and independent power producers. They offer a final reminder to investors:

“Some investors avoid these cyclical industries because of their wild and unpredictable fluctuations, but these data suggest that using economic data to evaluate investment opportunities in cyclicals and buying at economic troughs can provide above-market returns.”

___________________________________________________________________________

Resource of The Week: Job Satisfaction & Firm Value

Looks like scanning Glassdoor reviews before making investments pays off after all! Early this week I stumbled upon The Link Between Job Satisfaction and Firm Value, With Implications for Corporate Social Responsibility. The whitepaper reveals a link between job satisfaction and firm value (stock performance).

There’s clear limitations to the research. Not every company was surveyed, the criteria for “best places to work” is subjective, amongst other things. Nevertheless, here’s what the returns looked like from the best places to work:

-

- 380bps alpha over the risk free rate

- 230bps alpha controlling for industries

- 290bps alpha controlling for firm characteristics

One of those “Best places to work” companies was Google. So there’s a bit of an outlier issue.

But the point remains. When given the choice, invest in places that love their employees, and their employees love them.

___________________________________________________________________________

Idea of The Week: Gems in Japan and Europe

GIFs by tenor

GIFs by tenor

valueDACH released their latest interview with Alex Roepers. Alex is founder of Atlantic Investment Management. Alex chatted about the following topics during the 24-minute interview (via YouTube description):

-

- Why Alex thinks Europe is currently a candy story

- Alex’s view on Japan.

- Changing use of cash in Japan.

- Alex’s view on ETFs.

- An overview about his white paper “Putting Things into Perspective: Compelling Value Opportunities in a Growth Market”

You can’t go wrong with a valueDACH interview. I’m excited for their content in 2020.

___________________________________________________________________________

Tweet of The Week: Long Cast Advisors Asking The Real Questions

That’s all I got for this week. Shoot me an email if you come across something interesting this week at brandon@macro-ops.com.

Tell Your Friends!

Do you love Value Hive?

Tell your friends about us! The greatest compliment we can receive is a referral (although we do accept Chipotle burrito bowls).

Click here to receive The Value Hive Directly To Your Inbox!