Alex here with this week’s Macro Musings.

As always, if you come across something cool during the week, shoot me an email at alex@macro-ops.com and I’ll share it with the group.

Macro Ops Special Event Next Thursday, June 28th!

Next Thursday, June 28th at 9PM EST, Tyler will presenting our trading results for the Macro Ops Portfolio — Pain + Reflection = Process.

We’ve been fortunate enough to call the macro correctly over the last 6-months which has allowed us to outperform the market by a wide margin. We’re up 12.20% year-to-date and 20% on a TTM basis. But, we’ve still managed to make plenty of mistakes which we can analyze and learn from. Tyler will discuss what worked, what didn’t, and how we can improve and adjust fire going forward — I urge everyone to sign up at the link below. He’s got an insightful presentation prepared.

Click here to register for the event!

Make sure to register and show up on time because there will not be any recordings!

Recent Articles/Videos —

Google Buys JD.com — AK discusses the implications of Google’s ownership in one of our highest conviction plays, JD.com.

Portfolio Review — AK reviews our positions in the MO portfolio along with a few new plays we’re looking at.

Coaching Paul Tudor Jones — AK sheds light on the coaching PTJ himself gets for his trading.

Articles I’m reading —

Scott Miller, who manages the value focused hedge fund GreenHaven Road Capital, gave an interview this week with SumZero and it’s a great read.

Scott is one of the best up and coming investors right now, in my opinion. Not only does he put up excellent numbers but the guy is in a league of his own when it comes to understanding and valuing businesses. His quarterly investor letters always make for an interesting and enlightening read. I’ve sourced many ideas from him over the last few years.

In the interview, Scott talks about his investing philosophy, his edge, how markets are changing, and his greatest mentors and their lessons — he also pitches an interesting microcap tech stock, ticker (SHSP). It’s a short and insight filled read that’s well worth your time. Here’s the link and here’s a section from it (emphasis mine).

Harris: What are your thoughts on the rise of quantitative strategies at the expense of more traditional value and activist strategies?

Miller: The beauty of investing is that there are many ways to make money. Renaissance Technologies has one of the best track records of any fund using any strategy, and they are using a quantitative strategy. I actually want quantitative strategies to proliferate. I want money to pile into them, gobs and gobs of it. The more money into quant strategies the better, as I think they are likely to create distortions that I can take advantage of over time. You can have your backward looking quantitative data and use that for the foundation of your decisions. I would rather understand the product, market, and management team of the companies I am investing in. Quantitative strategies tend to scale well allowing for large AUM, have a large number of holdings, and have short holding periods. Greenhaven Road is effectively the inverse of that. I want to be small, concentrated, and have a long holding period. I want to understand qualitative factors such as the competitive landscape, the customer value proposition, and the incentives of the team.

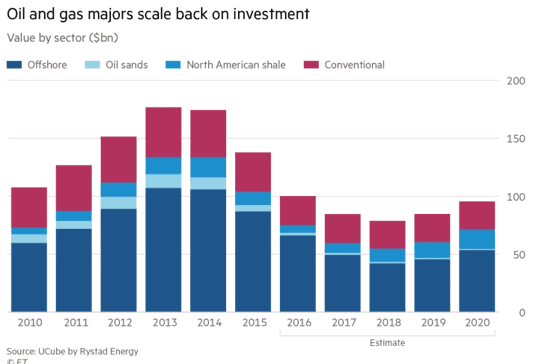

The FT wrote an important article this week discussing a long-term macro theme we’ve been kicking around for the last year or so. And that is whether or not the oil and gas industries’ unwillingness to invest in major long-term projects will lead to a supply shock and much higher oil prices down the road? We think it will…

The gist of my thinking is this:

- The energy industry and investors have largely bought into the “peak demand” narrative, that essentially says global oil demand is on a secular decline due to the rise of renewable energy and EVs.

- Because of this, energy companies are no longer making large scale investments into future capacity and instead are focusing are short-cycle projects like shale.

- Meanwhile, the digging I’ve done makes me believe that the whole “peak demand” narrative is a load of crap… similar to the whole “peak oil” narrative that captivated the market 8-years ago and predicted a quickly diminishing supply of crude and much much higher prices. The truth is, EV adoption will have a very limited impact on global oil demand over the next decade.

- What will have a HUGE impact on the price of oil is the exponential growth in energy demand we’ll see arise from the billions of people hitting the Wealth S-curve in Asia over the coming decade. This is not being priced into the market at all…

This is a long secular theme I’m tracking. And while I’ve been bullish oil and oil stocks since early last year, after the recent rise the short-term asymmetry is now not as good. Especially when short-term headwinds like a stronger dollar and slowing Chinese demand are taking into account. But, there will be A LOT of money to be made in the next cycle once this supply pinch begins to really be felt. So definitely worth keeping an eye on. Here’s the link to the article and a chart from it.

Video(s) I’m watching —

You may have seen this video of Frank Abagnale’s Google Talk doing the rounds on twitter this past week. I saw a number of people highly recommend it so I finally gave it a watch (I personally don’t have a lot of patience for videos and prefer writing). I’m really glad I did because it’s excellent.

Frank is the guy who the Spielberg movie Catch Me If You Can is based on. In the talk, he goes over his amazing life story and the lessons and values he learned along the way — he says some beautiful and powerful things about parenting and what it really means to be a man and a father. And his story is amazing; he worked in a hospital as a doctor though he never went to medical school, flew around the world for free posing as an airline pilot, practiced law without a law degree and so on… All while he was a young runaway teenager!

He spent years behind bars paying for his crimes and was eventually offered a deal to work off the remainder of his sentence assisting the FBI catch others like him. He’s stayed on with the Bureau and has now worked there for over three decades. I used to work in the same building as him and occasionally passed him in the halls, though I never had the chance to speak with, personally.

He’s a beyond interesting and surprisingly insightful guy, and his talk is well worth your time. Here’s the link.

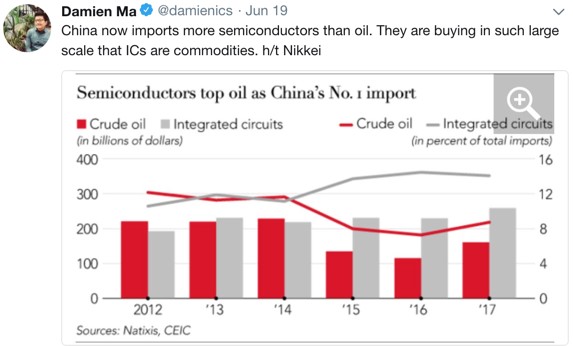

Chart I’m looking at —

China now imports more semiconductors than oil. There are two reasons for this (1) China is modernizing and its consumer base is growing rapidly, thus buying more gadgets that require computing power and (2) IoT, AI/ML, big data, autonomous driving etc… is leading to an exponential growth shift in structural demand for silicon globally.

This is a big macro theme that we’ve been tracking and it’s not one that’s being priced into the market yet, at all. But did you know, that the computing power needed to enable wide-scale autonomous driving is equivalent to over five new iphone industries being created annually. Then there’s the virtuous cycle that’s being created by the rise of big data and machine learning, where more data leads to improved machine learning which requires more compute which leads to more data capture and so on…

I think there’s some really interesting trades in a few select semi stocks at the moment.

Trade I’m looking at —

I’ve been told my entire life that I have absolutely no dress sense. Girlfriends have always complained that I dress like an old man and friends give me their hand me downs because they feel bad for me.

It’s not that I can’t afford nice looking clothes or anything. It’s just that I’ve never cared the slightest about what I wear and I loathe going shopping.

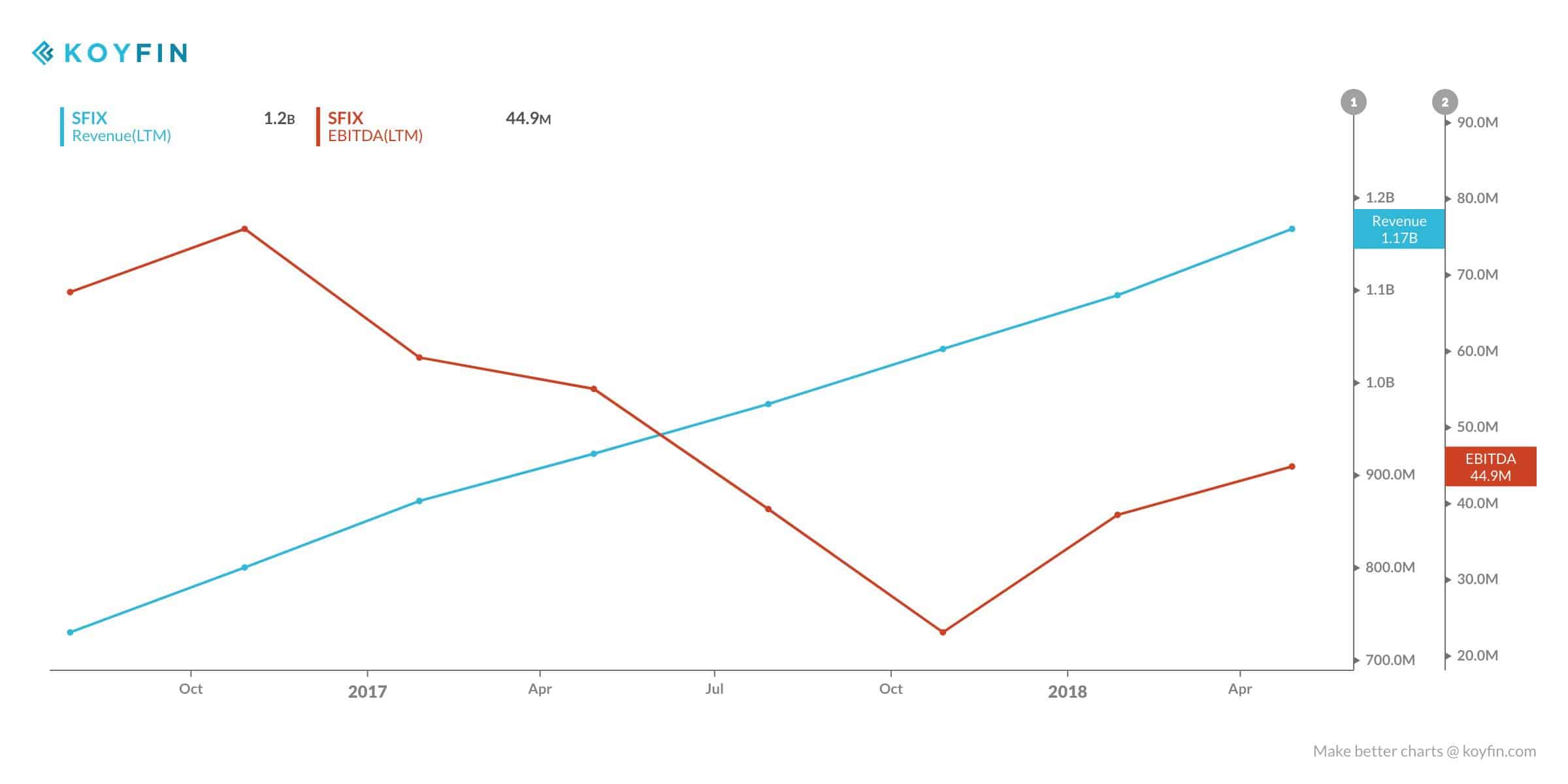

My wife long ago gave up on trying to drag me to the mall. But recently, she found a compromise in a new startup called Stitch Fix (SFIX). StitchFix is a US based online data-driven retailer. They allow you to select your style on their website and then send you an assortment of clothes, picked by a stylist with your style in mind, and then ship you these clothes at a regular interval of your choosing (ie, every month, two months, or quarter). You pay for the clothes that you like and send the others back in a prepaid shipping bag. The process is easy.

I’ve been using the service now since the start of the year. I like it. I don’t have to go shopping at a store to try on clothes. I get clothes that check my requirements (meaning, they’re comfortable and practical). And I appease my wife by no longer dressing like a total scrub.

SFIX IPO’d just last year. The chart recently broke out of 7-month coiling triangle pattern on strong volume.

They’re seeing strong sales growth and are already profitable.

Bill Miller’s hedge fund is a large holder of the stock. Here’s what one of his PMs wrote about SFIX in a recent post.

We’d heard fabulous things about the company and its CEO Katrina Lake from Bill Gurley at Benchmark Capital who was an early venture backer. It priced below the initial range as Blue Apron’s disastrous IPO and fears about ramping marketing spend concerned prospective buyers. At the IPO price of $15, we were able to buy it at only 1x expected fiscal 2019 (ending Jul 2019) revenues. For a company that had clearly demonstrated profitability, making it to $1B in revenues on only $42M in venture investments, we believe that valuation was quite a deal. Stitch Fix looks to transform apparel retail. As a long-time customer who buys most of her clothes from Stitch Fix, I can attest to their value proposition. While we’ve already done quite well with the stock at $25, we look forward to a long investment in the company.

I’m just digging into this stock and still have some thinking to do. I’m trying to figure out if there’s any realistic network or scale effects from becoming the dominant player in this space — they’re far from being the only business doing this. But the chart and fundamentals look good and at 2x sales the price seems reasonable when their growth is taken into account.

Quote I’m pondering —

This is so true.

The biggest secret in this game is that there is no secret.

We’re all just grasping for straws. The greats are just good at minimizing losses when they’re wrong and maximizing gains when they’re right. That’s really all there is to it.

Also, Jawad Mian is a great follow on twitter if you’re not already.

That’s it for this week’s Macro Musings.

If you’re not already, be sure to follow us on Twitter: @MacroOps and on Stocktwits: @MacroOps. I post my mindless drivel there daily.