Alex here with this week’s Macro Musings.

As always, if you come across something cool during the week, shoot me an email at alex@macro-ops.com and I’ll share it with the group.

Recent Articles/Videos —

The Human Trader’s Secret Weapon – Alex explains the three different types of investment edges and how humans can use a few of them to identify and hold onto long-term compounders.

Articles I’m reading —

Hayden Capital’s latest investor letter is out and as always, it’s a great read. Fred Liu, Hayden’s managing partner, has quickly become one of my favorite investors to follow. Each of his letters offer a master class in fundamental value investing. In his latest, he talks about the global competitive landscape, investing in China, and then discusses two compelling long theses for both Amazon (AMZN) and iQiyi (IQ). Here’s the link and a cut from the letter.

Few investors have the opportunity to look across borders, and thus their knowledge base is extremely siloed (for example, “US Small Cap Consumer”). I firmly believe this creates an opportunity for longer-term investors who are willing to break this mold, and be open-minded enough to recognize that sometimes the US business models & practices aren’t always best.

In particular, I’ve spent a lot of time studying China. This isn’t just because of my family background there (although it helps) – but rather because I believe successful business models are a function of evolution & adaptation – aka [survival of the fittest] X [access to capital]. My theory is the business models that can scale globally, and create astronomical wealth in the process, are those that have been battle-tested thoroughly in their domestic markets first. Think of it as a Darwinist process, where out of 1,000 startups, the weakest business models will fail, and only the strong adapt, survive & get funding. By the time they arrive on the global stage, they’re already the best of the best in their home country, and thus have a strong chance of having evolved the best model for succeeding elsewhere too. It’s even better if that home country was populous, entrepreneurial, had demanding customers, and formidable competitors who put up a fight. For this reason, it’s also more likely that the best business models from a >1 Billion population market will be more durable than one from a 5 million population market.

Speaking of China… Here’s a very long, very detailed, and super intriguing analysis of Alibaba’s (BABA) most recent 20-F (link here). BABA’s financials are a riddle, wrapped in a mystery, inside a giant convoluted 920 entity globe spanning Chinese Communist Party entangled esoteric financially leveraged turducken ponzi-looking thingamajig….

Seriously, there’s some strange things going on over at Jack Ma’s chinese empire. The entire piece is worth a read if you’re into this sort of thing (I am). Here’s a section from the post.

We covered the incestuous relationship between Wazu Media, Jack and Simon Xie in last year’s Finding Inner Peace in Dharamasal 20-F post. I’d encourage you to re-read it…..it’s pretty entertaining even if I do say so myself.

In a nutshell, Simon got Jack to spend US$ 1 Billion of US Shareholder’s money on “Wealth Management Products” to use as collateral so that an unnamed Chinese banker would make Simon a loan to buy a minority interest in “Wasu Media”.

There’s no change described in the structure of this absurd deal in this year’s 20-F. Simon still owes the US$1 Billion to the unnamed Chinese banker and he’s still paying the interest on the loan using the money from his other loan directly from Alibaba. The money drawn on this RMB 2 Billion Line of Credit given to Simon Xie (to pay the interest on the Billion US dollar loan keep this thing afloat) has increased by another RMB 400 Million to RMB 1.137 Billion. So it continues to bleed.

So Alibaba is on the hook for both the principal and interest. Tell me again, one more time, why we need Simon Xie involved?

This example is not even close to being the biggest head scratcher. There are many many more… BABA is a hedge fund hotel, trades at 12x revenues, and is currently teetering on critical support. Puts maybe?

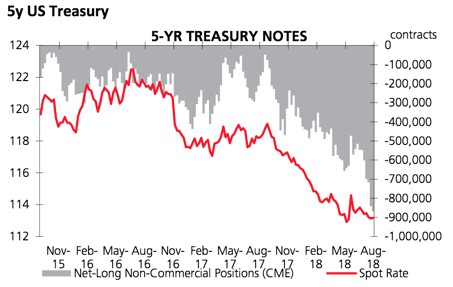

Chart I’m looking at —

I’m considering buying 5yr Treasuries here for a punt. Short positioning is stretched and from a technical standpoint, it looks like price really wants to rise (yields down).

This chart offers a good R/R for an entry with a tight stop. I think it runs to at least its 50ma (red line).

Podcast I’m listening to —

This week I listened to the Capital Allocators podcast with guest Ben Reiter. This interview was so so good. Ben Reiter is a writer for Sports Illustrated and the author of Astroball: The New Way to Win It All. He’s the guy behind the 2014 SI issue entitled YOUR 2017 WORLD SERIES CHAMPS; a crazy prediction (the Astros were one of the worst teams in baseball) that ended up becoming true.

They talk about how big data and statistical analysis are evolving the game of baseball. It’s like Moneyball but on steroids with teams now analyzing all types of esoteric data in order to try and gain an edge. And the secret sauce that made the Astros so successful was their use of qualitative data (input from seasoned baseball scouts) on the intangible things that separate good players from great ones.

The discussion might as well have been about markets and investing — there are tons of parallels. Definitely check it out, it’s worth a listen. Here’s the link.

Trade I’m considering —

I’m closely watching a list of “fallen angels” which are great companies / value stocks that have fallen 30+% over the last few months. All great stocks go through periods of large drawdowns like this and it’s healthy, just as long as the business fundamentals are still sound (which they are for each of the stocks below).

These large pullbacks are the result of profit taking which leads to momentum and trend followers exiting, which eventually drives the stock down to a point where value investors come back in and scoop it up. Then the process repeats.

A few of the stocks on my “fallen angels” list are Fiat (FCAU), Interactive Brokers (IBKR), and Gaia (GAIA). I’ve owned all three in the past and have been waiting for a sizable pullback to get back in. I only hope the selloff continues a bit more so we can get even better deals.

Quote I’m pondering —

Most people’s lives are virtual monuments to cowardly indecision. Ah, that we lack the courage of our romantic convictions; and thereby miss the wine of life, forgoing the very thing that makes living worthwhile. ~ Hunter S. Thompson

Don’t lead a life of quiet desperation. Go and get after it….

That’s it for this week’s Macro Musings.

If you’re not already, be sure to follow us on Twitter: @MacroOps and on Stocktwits: @MacroOps. I post my mindless drivel there daily.