Summary: The primary trend in equities remainsup with seasonality strongly supportive of a rally into the end of the year. But… several surveys are showing crowded positioning, and BofA’s Bull/Bear is giving another sell signal. However, budding underlying strength, particularly from cyclicals, suggests any downside will be contained. Crude is set up for a potential double bottom amongst historic bearish sentiment, and beaten-down AI angels may be gearing up for another run.

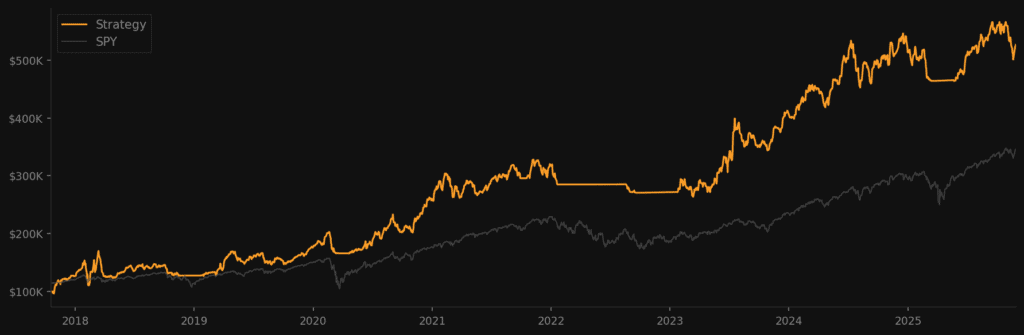

***The MO port is up +42% ytd, and we’re not seeing a shortage of great opportunities in this market. If you’d like to join me, the MO team, and our Collective of sharp, supportive investors and traders as we navigate these markets, then click the link below. I look forward to seeing you in the group.***

Join The Collective

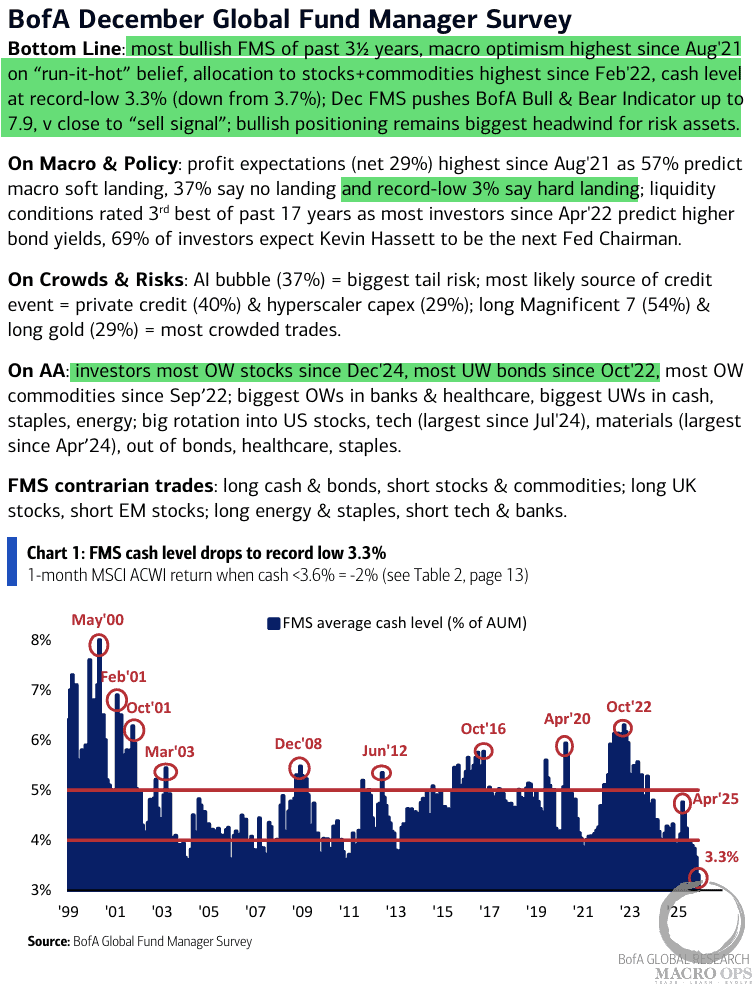

1. The latest BofA Global Fund Manager Survey came out last week. According to the report, fund managers are:

- The most bullish risk assets in 3 ½ years

- Highest macro optimism since Aug 21’ on “run-it-hot” belief

- Lowest cash level since 1998

- Investors most overweight stocks since Dec 24’

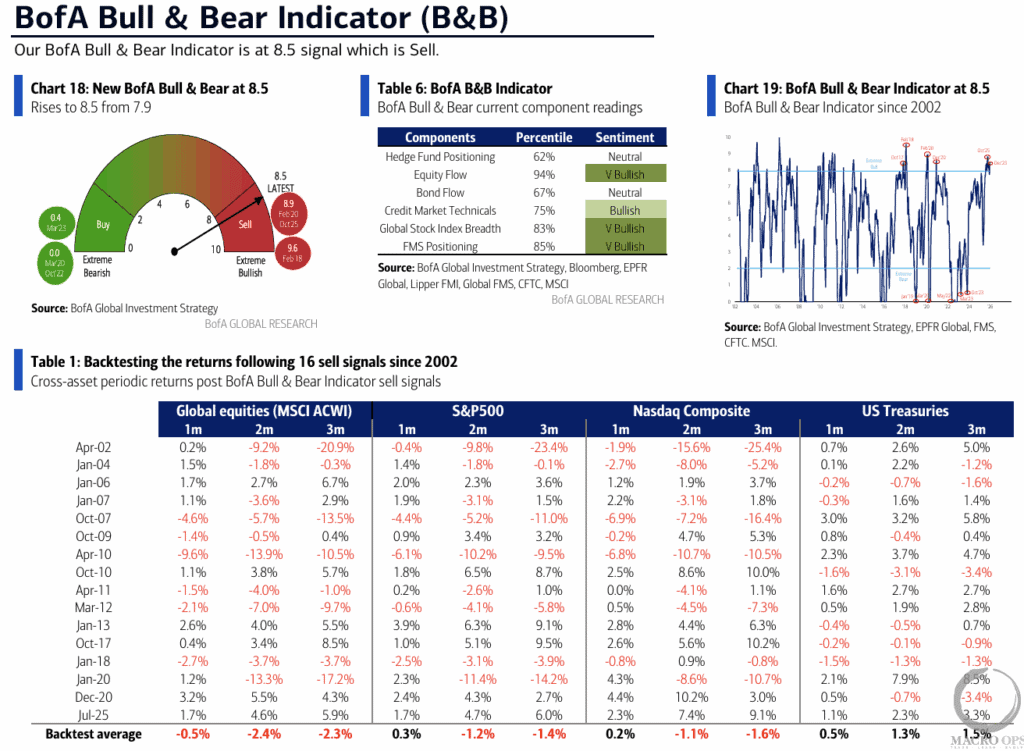

2. BofA’s revamped Bull & Bear indicator is back in “sell signal” territory on “huge inflow to equity ETFs, rising global stock index breadth, hedge funds cutting length in VIX futures.” A “Bull & Bear Indicator >8.0 = extreme bullishness = contrarian sell signal; median decline in global stocks = -2.7% in 2 months following 16 sell signals since 2002 with 63% hit ratio; max drawdowns in 1 month, 2 months, 3 months after sell signal = -4%, -6%, -9% respectively (vs. max upside foregone <2%).”

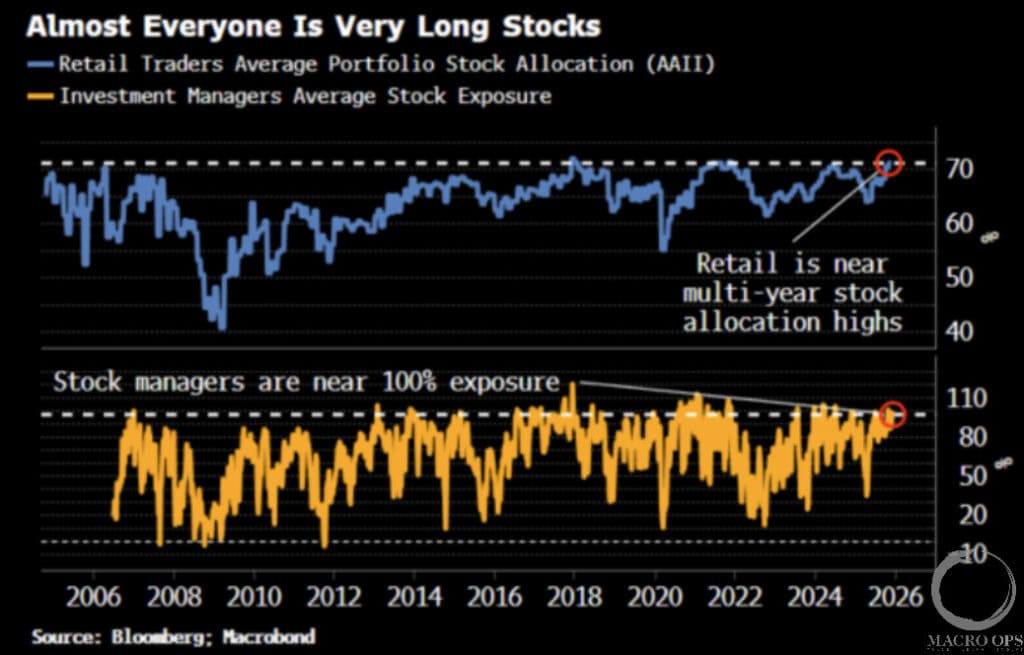

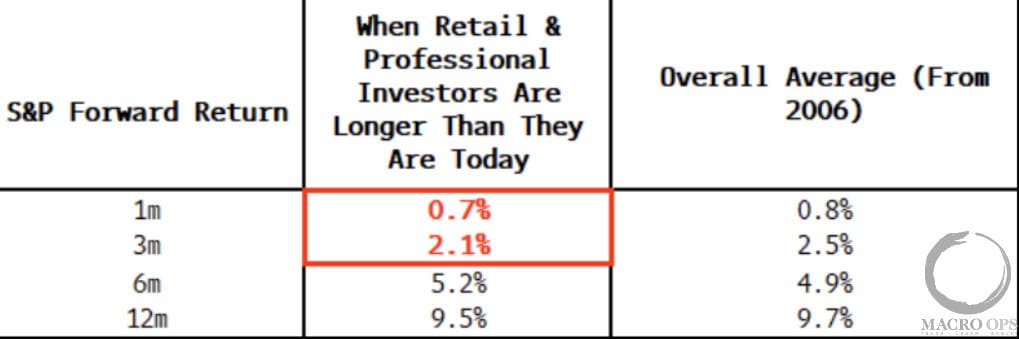

3. Also, both AAII and NAAIM show average investor stock exposure near multi-year highs (chart via BBG’s Simon White).

4. Similar to BofA’s study, White shows that SPX returns over the next 3 months tend to be poor when investors are this crowded long.

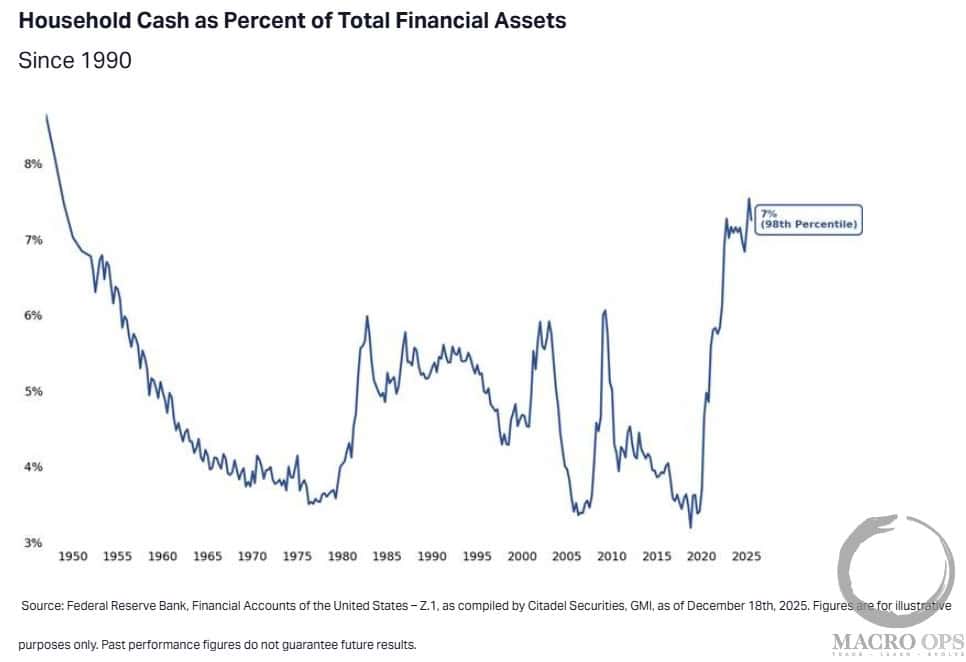

5. Citadel Securities shared an interesting report detailing the rise in household wealth, particularly from the bottom 50%, and how this is leading to increased engagement in the equity market. However, CS notes that “Despite this increased engagement, households continue to hold near-record cash balances (98th percentile historically), leaving substantial dry powder should confidence and risk appetite continue to improve. We see this “buy-the-dip” behavior, every day in our data at Citadel Securities.”

6. Admittedly, the immediate setup is a bit of a mixed bag. On the positive side of the ledger, we have constructive breadth, very strong seasonals for the next week, and most internals confirming the uptrend. On the negative side of things, we have the aggressive positioning mentioned above, along with deterioration in credit leads and high valuations.

I’ll play the market as it comes, but my base case is that we rise into the eoy, fueled by low-volume seasonal trading. Maybe poke our head above the channel line below before rolling over for a bit of sentiment and positioning washout to start the new year (SPX chart our Classical Chartist @mikegyulai; make sure to give him a follow).

7. LQD/IEF divergences can lead market corrections by a few weeks to a few months. A rule of thumb is that the longer the divergence, the larger the incoming correction will be. The current divergence has been going on for a month and a half.

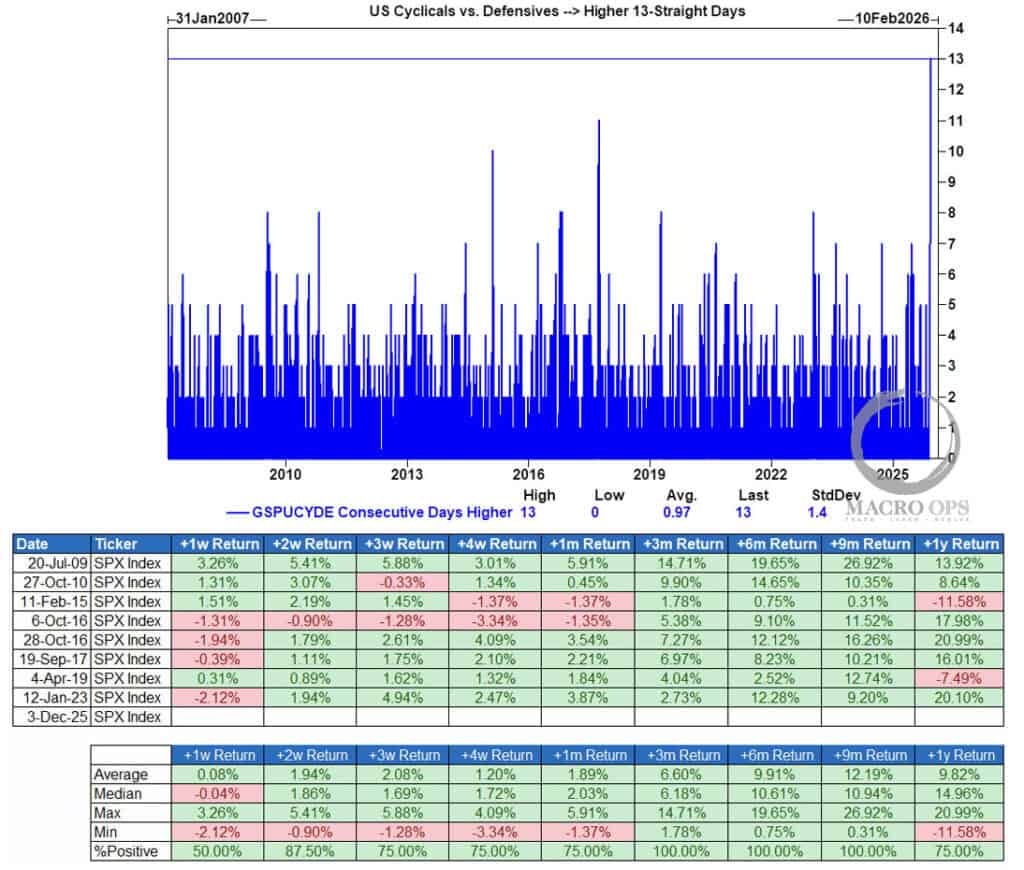

8. I don’t believe a significant correction is inbound, though. I think it will stay contained (sub-10 %). There’s just too much underlying strength for things to dump hard. For instance, Cyclicals vs Defensives just put in a rare string of consecutive outperformance.

GS notes that “when we look at every period since 2007 where cyclicals beat defensives in long streaks (8 straight gains or more), the 3-9 month returns for the S&P are almost always positive — and often very strong. It’s one of the cleaner signals we have that the market is sniffing out better macro conditions before the data fully reflect it.”

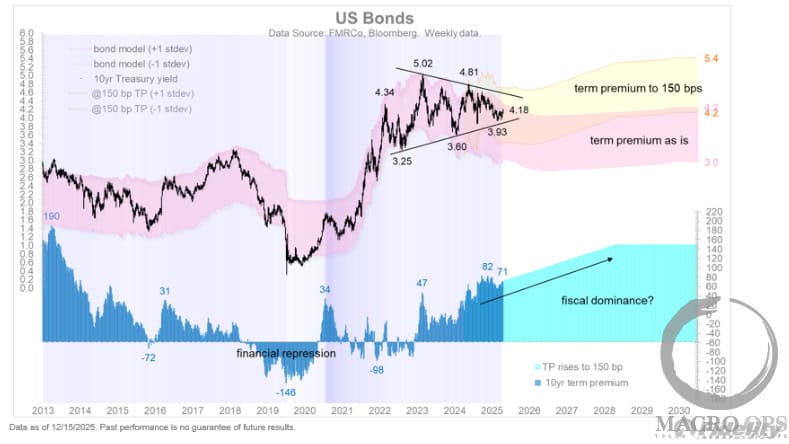

9. We expect US growth to surprise to the upside in 26’, and with a new Fed chair likely to pin the front end to the floor, we should see the term premium rise. A continued bear steepening is what the charts are saying (chart via Jurrien Timmer).

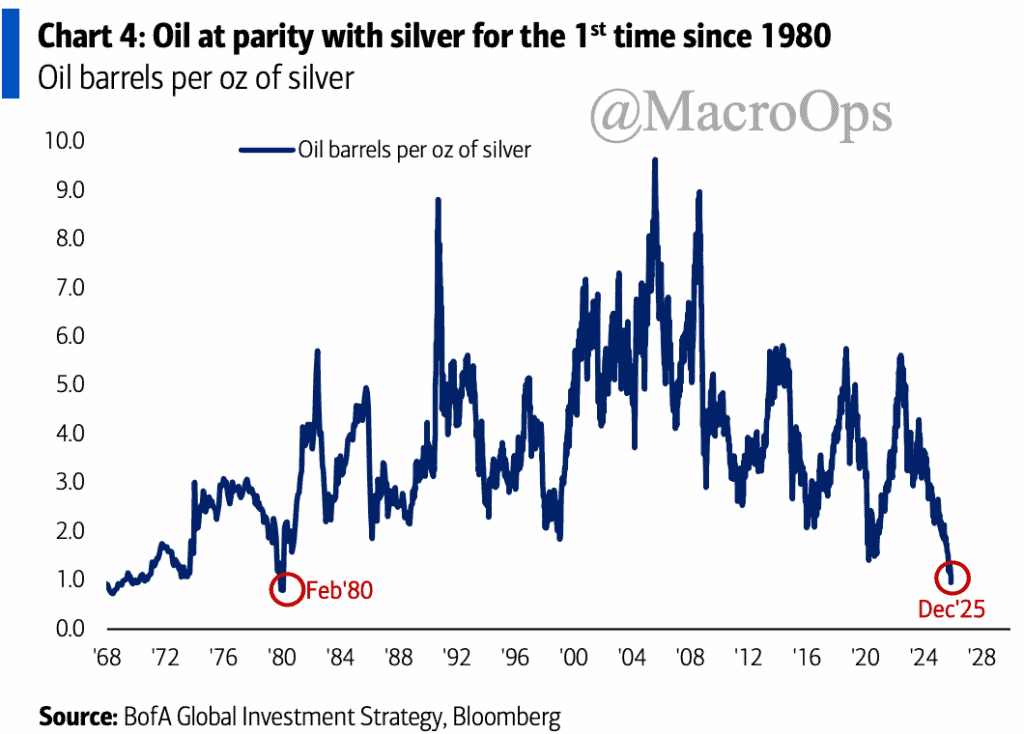

10. We have buy stops on crude here to see if it can pull us in long. Last week, I pointed out the historical extremes in bearish positioning. This is amidst a backdrop of rebounding global growth. The trend isn’t great, so trying to put on tactical longs here is a bit like spitting into the wind, so we’re keeping sizing small. But we’ll see if crude can hold this double bottom.

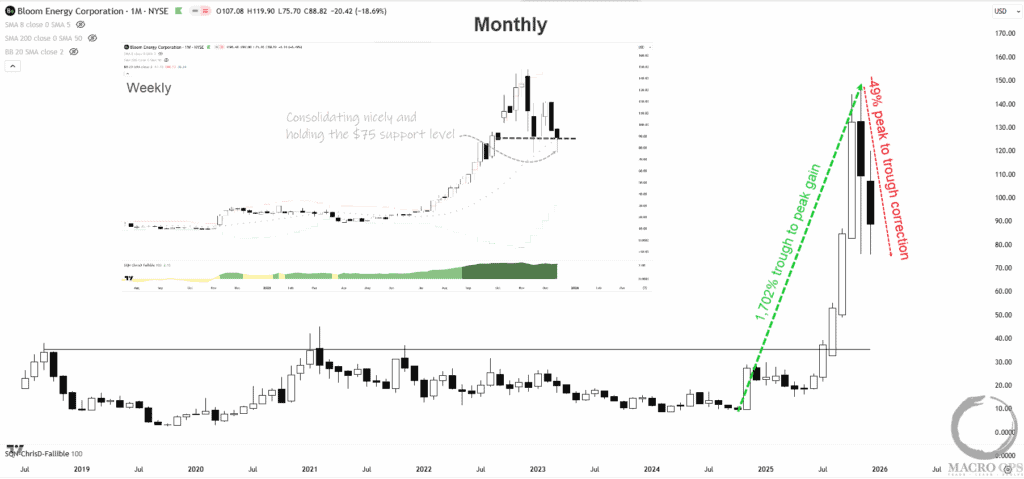

11. The AI trade isn’t over. This cycle still has some legs. We’re keeping a close watch on ancillary AI names that have corrected after a large run. One of my favorites is Bloom Energy (BE), which has sold off 50% from its recent peak after a quick 1,702% run-up—big props to fellow Collective member @VBK for nailing this one early on.

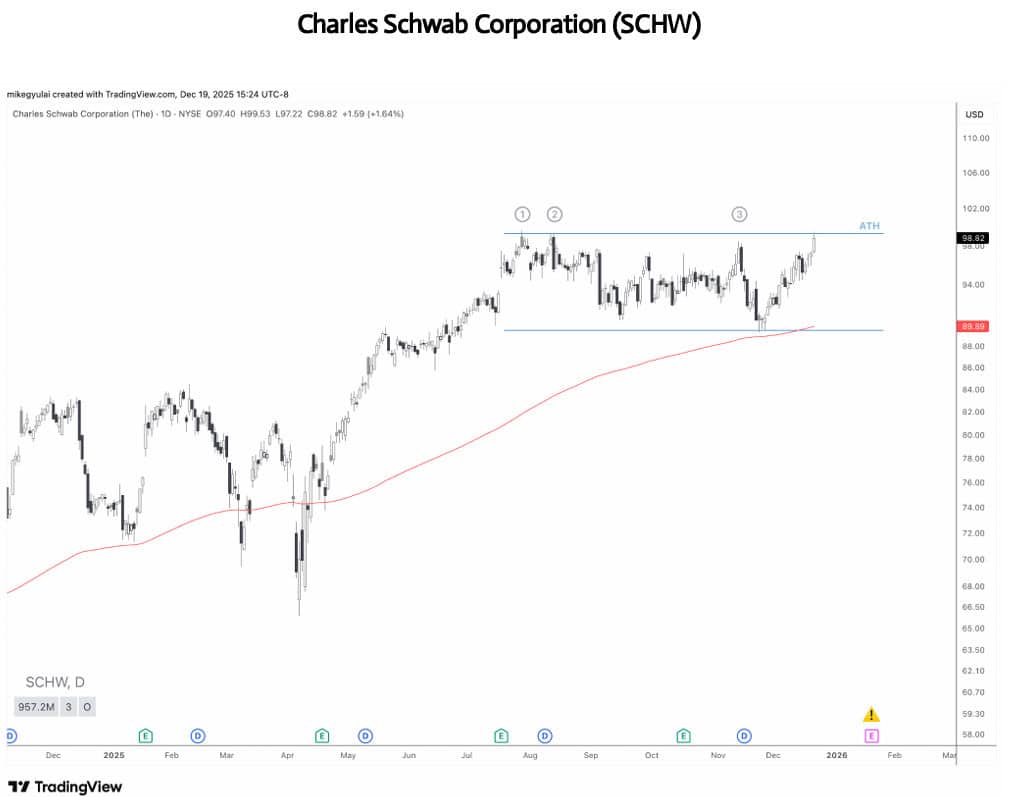

12. The rise in household wealth and greater market involvement is a cyclical tailwind for brokerage stocks, like SCHW. Mike G shared this one in his excellent weekly “This Infinite Game.”

Join The Collective

Thanks for reading.