“And it is why digital transformation can be so frightening: Companies must shift their focus from what they know works and invest instead in alternatives they view as risky and unproven. Many companies simply refuse to believe they are facing a life-or-death situation. This is Clayton Christensen’s aptly named “Innovator’s Dilemma”: Companies fail to innovate because it means changing the focus from what’s working to something unproven and risky.” – Thomas Siebel

We’ve spent the last month detailing the massive AI upheaval in every industry. Whether it’s finance, education, or healthcare, every industry will feel AI’s inevitable creep.

The companies that win will adapt and invest in new technologies. Forge new business models and create insurmountable competitive advantages.

This essay dives deep into a new Artificial Intelligence IPO that has everything we want:

-

- Founder-led CEO w/ History of Success

- High Switching Cost Business Model

- First-Mover Advantage

- Long Industry Runway/Tailwinds

- Incredible Ticker Symbol

Let’s get after it!

Mr. Market’s First-Mover Pick-and-Shovel IPO: C3.AI

C3.AI (which we’ll call “C3”) is a first-mover picks-and-shovels Enterprise AI business set to IPO later this year. The company will list under the ticker “AI” (talk about first-mover advantage!).

The bull thesis is simple: Companies will need to adopt AI-based technology solutions to meet the competitive challenges of the next decade. C3 makes it easy for any business to do that.

Their solutions allow companies to develop and run full-scale, real-time enterprise AI applications.

Plus the company’s led by one of the sharpest founders/CEOs in the game, Thomas Siebel.

This essay will break down the most important aspects of the C3 thesis:

-

- Incredible corporate culture and CEO

- Massive time and money savings

- High-value land and expand growth strategy

- Strong revenue growth in long tailwind industry

Let’s get after it!

The Importance of Culture and Executive Leadership

Thomas Siebel is the founder of C3.ai. He also wrote the book on Digital Transformation. Siebel’s track record is nothing short of astounding. In 1983, Siebel joined a small database start-up, Oracle. A decade later the company did over $1B in revenues.

After cashing in on his time at Oracle, Siebel founded Siebel Systems. In Siebel’s words, his company, “applied information and communications technology to the business processes of sales, marketing, and customer service.” If this sounds like the world’s first CRM, you’d be correct.

Again Siebel found lightning in a bottle. By 1999 (only six years later), Siebel Systems generated over $2B in revenues and employed over 8,000 people. It remains the fastest growing enterprise application company of all time.

In a worlds-collide moment, Siebel Systems merged with Oracle in 2006.

Three years later, Siebel founded C3.ai in an attempt to catch the next technological wave of elastic cloud compute, big data, AI and IoT.

Siebel extrapolated his reasons for starting the company in a C3.ai interview (emphasis mine):

“I thought that this was a really exciting time in the world‚ so I put together some talent and we spent a decade and about a half a billion dollars building a software platform to allow large multinational corporations and governments to take advantage of these technologies to use industrial AI to solve problems that had never been solved and realize the social benefit that was unrealized before. But why did I do it? Obviously‚ this is not about making money. When I’m done with this‚ no matter how successful it will be – and I believe it will be successful – it’s not going to make any difference in my life. I’ll have the same wife‚ same car‚ and the same house …

Everything is the same for me‚ but for those with whom I work‚ which is 330 people today and will be 800 people in a year and probably 2‚000 people in two years‚ it will change their lives profoundly. It will also change the lives of our customers‚ whether that be 3M or the Air Force or the Defense Intelligence Agency or Royal Dutch Shell‚ and it will change their customers’ lives in a very positive way. So‚ I do this because this is my idea of a good time.”

It’s quotes like this that explain the company’s crazy-high Glassdoor and CEO ratings. Check out these stats:

-

- 89% CEO approval

- 90% of employees would recommend the company to their friends

- 4.6/5 stars with 336 reviews

Investors should always take Glassdoor reviews with a grain of salt. But given the consistency of the 330+ reviews there’s a few things we can deduce. First, people love helping their customers solve problems. You’ll read things like (real reviews):

“Meaningful work, top technology, an award-winning culture, and talented team. On top of all, frequent exposure to diverse sets of projects!”

“I have personally been able to grow so much because of all of the critical thinking and problem-solving I’ve had to do both in customer-facing projects and in internal R&D projects. The data science team managers do an amazing job guiding our personal growth and allowing us to explore all kinds of experiences.”

Second, employees love upper management. Confirmed via a few more reviews:

“A culture of continued education and collaboration established by the CEO has remained consistent through the years, branches, and echelons of the company. Management makes it clear that work/life balance is important and actively checks in to make sure nobody is burning out.”

“Best in class BOD. Executive team has been in place a long time. Key Execs have been with Tom since the beginning”

Third, C3.ai invests in their employees. Some reviews list a few of the company’s continuing education perks like:

-

- Cash bonuses for completing Coursera courses ($1-$1.5K per course)

- Fully funded Masters in CS at UIUC

Finally, I couldn’t publish this write-up without mentioning this employee review (emphasis mine):

“Tom Siebel is brilliant. Ed Abbo is brilliant. They have surrounded themselves with some of the brightest people I’ve worked with in a long and very successful career, and the technology stack here appears to be highly differentiated. I have never before worked for a company where the CEO reviews every deal that comes across his desk to make sure that there is enough economic value accruing to the customer that is buying that company’s product.”

Siebel isn’t ignorant to the success his company has in recruiting (and retaining) the best, most enthusiastic talent. Here’s his thoughts on the company’s Glassdoor rating (emphasis mine):

“You might be familiar with a phenomenon called Glassdoor.com where people anonymously evaluate their company. I think we’re ranked as the best place to work in the world. People love working for us because we select people who will like working at a place like ours.”

Culture matters. Leadership matters. And C3.ai has some of the best I’ve seen from an IPO. C3.ai employee reviews and Siebel interview transcripts are enough to make me want to buy. And we haven’t gotten to the actual fundamentals of the business yet!

But before we dive into the inner workings of the company, it’s important to analyze Siebel’s compensation, incentives, and ownership stakes.

Management Compensation, Ownership, and Incentives

Siebel’s 2020 compensation included a salary of $5,676 (that’s five thousand dollars) with $10.3M in option awards.

With a $5,000 base salary, Siebel clearly makes his money through capital appreciation of his underlying stock ownership.

With a $5,000 base salary, Siebel clearly makes his money through capital appreciation of his underlying stock ownership.

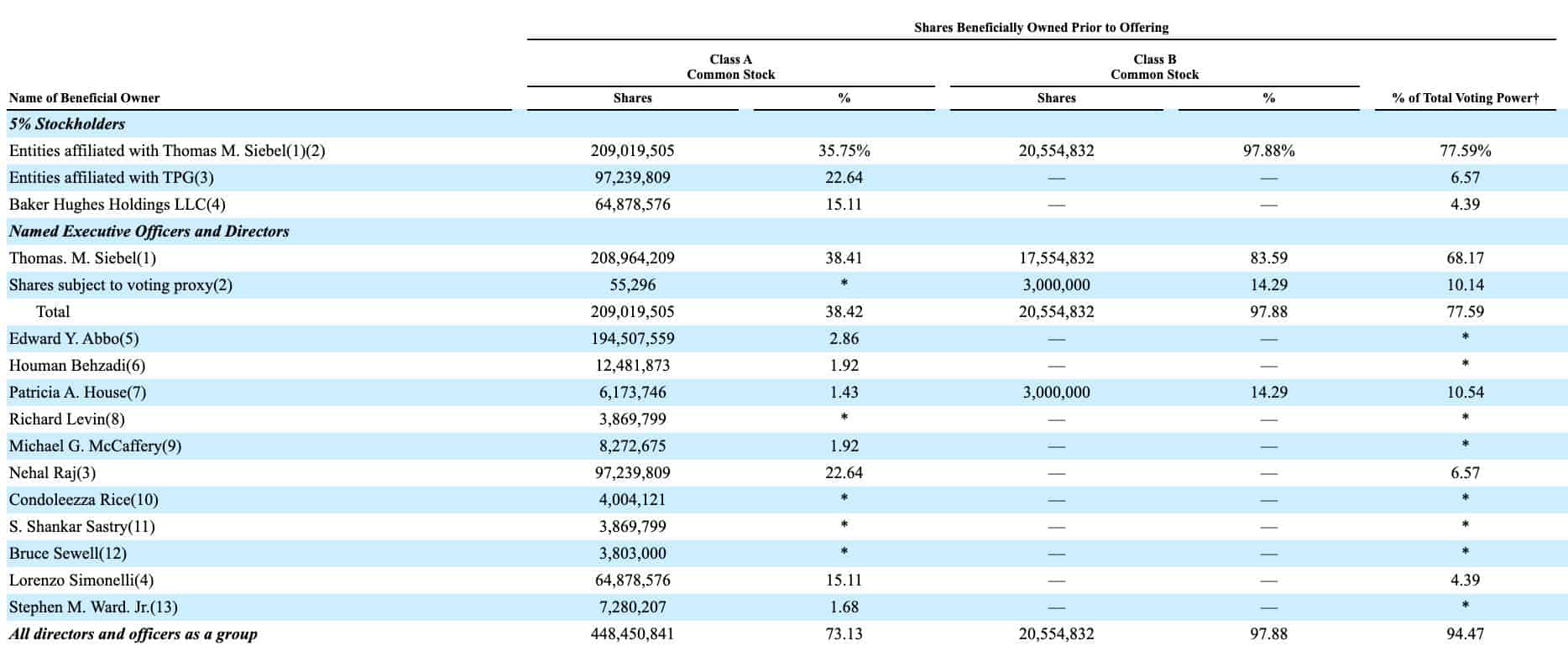

Siebel owns 38% of C3.ai and controls 78% of the voting power. Make no mistake: this is Siebel’s ship and he is the captain.

Nehal Raj (another executive) owns 23% of the remaining shares. Combined with the remaining executive ownership, insiders own 73% of the common stock.

This leaves 27% float for the rest of us.

What Is C3.ai and How Do They Make Money?

C3 helps customers develop, deploy, and operate large-scale Enterprise AI applications at a fraction of the cost compared to an in-house alternative. They do this through two business segments:

-

- C3 AI Suite

- C3 AI Applications

Siebel and company poured over $800M in R&D to develop their patented product offering.

C3 AI Suite

According to the company’s S-1 filing, the C3 AI Suite is the only end-to-end Platform-as-a-Service (PaaS) designed to develop, test, and deploy enterprise AI applications at scale.

Think of it as Enterprise AI with batteries included. Customers have access to C3’s suite of conceptual models (apps) where everything they need to run advanced AI processes is on one platform:

-

- Data objects

- Computing resources

- Data processing services

- AI and ML services

The platform comes “pre-installed” with applications (think apps on an iPhone). All the customer has to do is select the right “app” for the job. In fact, the “App Store” is a great framework for thinking about C3’s AI Suite.

The Suite allows developers (both C3’s internal and external customers) to create and customize their own applications using C3’s conceptual models. This creates an even larger library of applications (growing 4,000+ per year) and a virtuous platform cycle.

Where More apps make the platform more valuable. Which encourages more customers to use it. Which spawns more apps. Etcetera.

C3 charges a subscription for its AI Suite on a ~3-year term basis.

C3 AI Applications

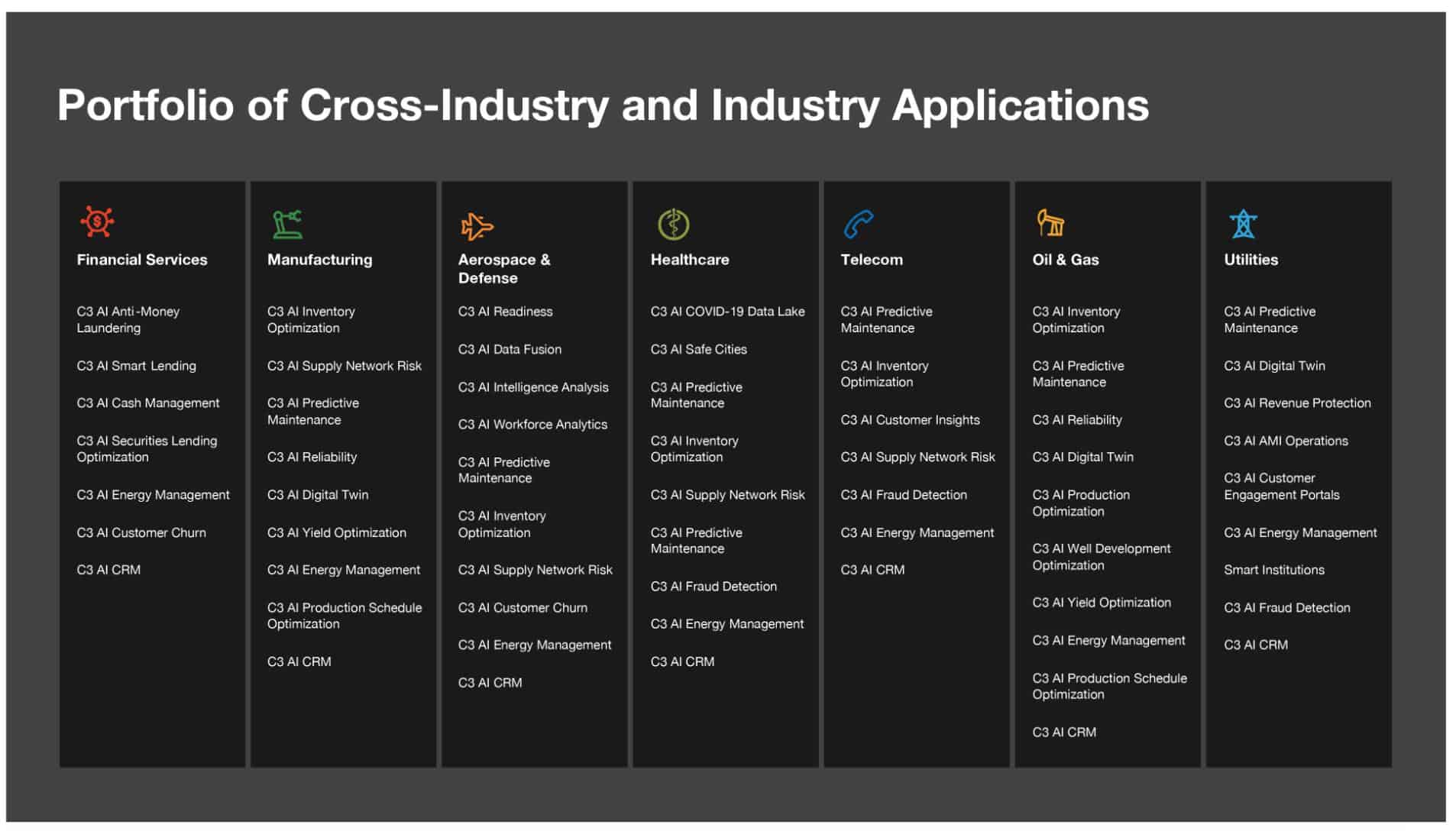

C3 also develops specific applications for its AI Suite Platform. These apps are both cross-industry and industry-specific. Customers use C3’s applications to develop and launch AI-based models and tests.

Here’s a few examples of C3’s myriad industry apps (from the S-1):

The company charges a subscription fee for its AI applications on a ~3-year basis. They also charge monthly runtime fees for C3 and customer-developed apps (based on CPU-hour consumption).

Professional Services

The company also makes money through training and assisting customers in onboarding and technical support. But this is such a small portion of revenue we won’t cover it.

How C3 Differentiates From Competition

There’s two things that make C3’s patented AI Suite different:

-

- Operability on any cloud platform and any premise (on or off).

- Massive time/code reduction

C3’s S-1 does a great job highlighting the massive time and dollar savings from using their AI Suite, including:

-

- Enabling developers to build AI applications 26 times faster and with up to 99% less code than with other technologies, by using conceptual models (including tens of thousands of C3.ai’s prebuilt models)

- Reducing the resources required to build AI applications

- Making developers more productive by allowing them to ramp quickly on new application projects, through reuse of models across applications and reduced coding requirements

- Decreasing application operating and maintenance requirements

- Accelerating the ability to enhance applications with new features

By creating a model-abstraction layer on top of all these AI applications, C3 makes it easier for developers to create models and analyze complex datasets.

Siebel and his team are well aware of the competition they face from companies trying to “DIY” their way to an Enterprise AI solution. The problem is it won’t work. And it hasn’t worked for a long time.

The S-1 notes that companies have tried to “DIY” technology stacks since the 90s. In the early days, Oracle’s competition wasn’t IBM or Ingres, but internal CIOs destined to reproduce Oracle’s solution in-house. The same thing happened when Siebel introduced the CRM. Here’s a note from the filing explaining this phenomenon (emphasis mine):

“Just as happened with the introduction of RDBMS, ERP, and CRM software in prior innovation cycles, the initial reaction of many IT organizations is to try to internally develop a general-purpose AI and IoT platform, using open-source software with a combination of microservices from cloud providers like AWS and Google. The process starts by taking some subset of the myriad of proprietary and open source solutions and organizing them into a platform architecture.”

In-house developers need structured programming to “stitch” each nascent AI tool together. That takes a lot of time and money. For example, C3 recruited an Amazon Web Services (AWS) Consultant to make a predictive maintenance application that runs on AWS.

The consultant had to make the application using C3’s architecture and their own structured programming.

The results were mind-boggling:

In-House Structured Programming (DIY)

-

- Time to complete: 120 person-days

- Cost: $458,000

- Lines of Code: 16,000

- Runs Only on AWS

C3 AI Suite

-

- Time to complete: 5 person-days (115 days less than DIY)

- Cost: $19,000 ($439K less than DIY)

- Lines of Code: 14 (15,986 less than DIY)

- Runs on any cloud platform without modification

These results explain the company’s rapid revenue acceleration and successful go-to-market strategy.

C3’s “Lighthouse” Go-To-Market Strategy

C3’s go-to-market strategy is simple. Find the best and biggest companies. Make them your customer. Do great work for them. Use them as an example to gain market share down the funnel.

The company refers to these large initial customers as Lighthouse customers.

I like this strategy because it forces the company to capture and retain the industry’s best customers. Once you gain their trust, it’s (relatively) easy to convince smaller companies in the same industry to use your product/service.

We see this strategy enacted in everyday life. How do you get a basketball team to buy-in to a new coaching system? Convert the star player. How do you get a younger child to behave? Ensure that their older sibling sets a good example.

Humans are mimetic creatures. We follow the herd. And what are companies but a consortium of herd-following humans?

C3’s Lighthouse customers include:

-

- Shell

- AstraZeneca

- conEdison

- Lyondellbasell

- Raytheon Technologies

- S. Air Force

Currently, C3 focuses on banking, oil and gas, utilities, defense, and manufacturing industries.

The best way to gauge if a customer loves your product is to see how much they use it and how much they expand usage. C3 destroys in those categories.

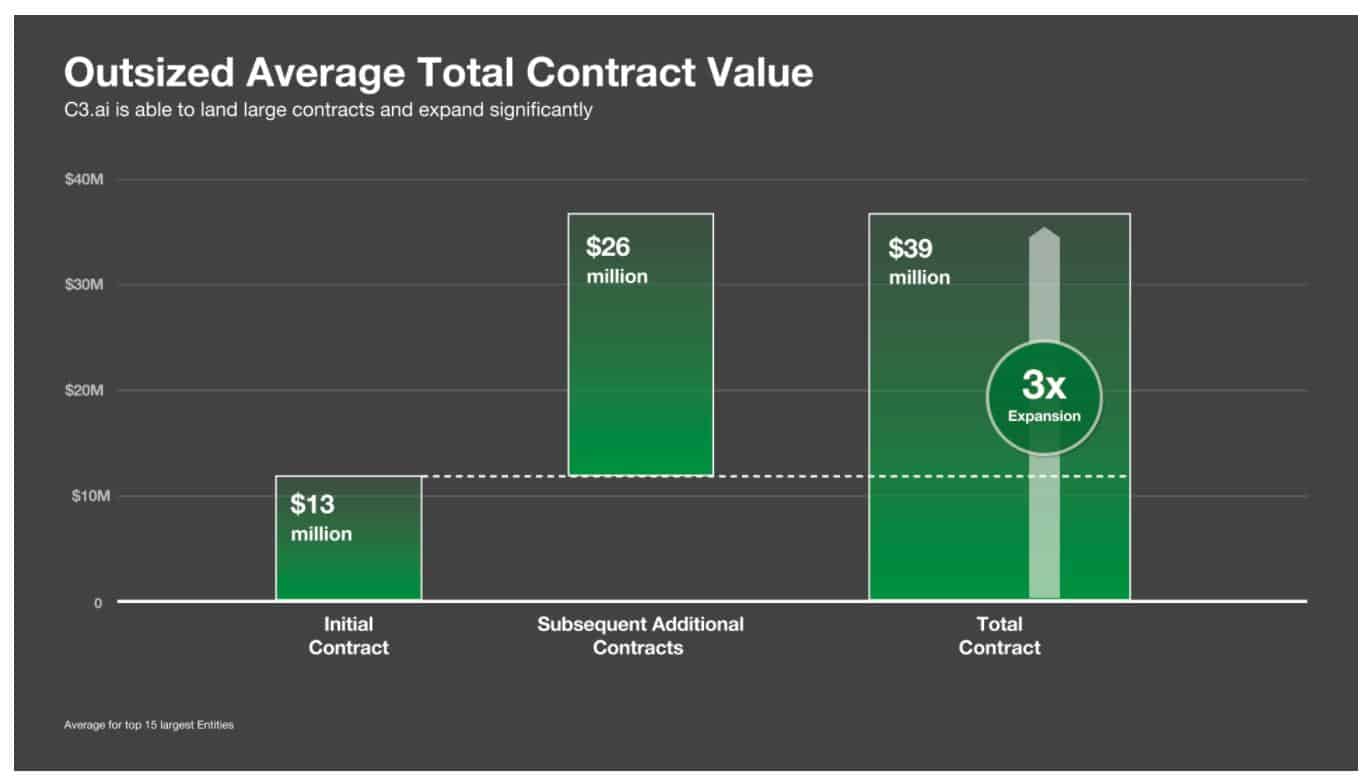

Start Big, Grow Bigger

C3’s customers start with an average initial purchase of $12.8M. Here’s the secret sauce. Customers end up paying 3x their original purchase price in add-on services/fees over the length of their subscription.

Here’s what that looks like:

-

- Initial Purchase: $13M

- Add-on Contracts/Fees: $26M

- Total Contract Value: $39M (3x original price)

This means companies use the product, see the value, and increase C3’s penetration throughout their entire company. In turn, it creates a stickier, higher-switching cost product.

Check out a few of these examples from C3’s largest customers:

-

- Large Integrated Energy Company: 4.3M euros in year 1 to 35M euros by year 4

- Large Global Financial Institution: $31M at year 1 to $39M by year 2

- Large Global Oil and Gas Company: 1.8M euros at year 1 to 25.4M euros at year 4

- Large Global Energy Company: 19.4M euros at year 1 to 43.1M euros at year 4

- Major Government Agency: $6.2M at year 1 and $14.9M at year 3

Decreasing Sales Cycles = Increased Priority / Adoption

Historically C3 experienced long sales cycles. For instance, the company’s average sales cycle spanned 13 months in 2016. This isn’t surprising. Companies take a while to adopt new technology like Enterprise AI.

Over time, most companies recognize the need for it and hasten their adoption schedules. That’s exactly what C3’s seen in their sales trends.

At the end of 2019 C3’s sales cycle shrank from 13 months to 4.8 months. According to the S-1 filing, the reduction in sales cycles relates to:

Increased prioritization of Enterprise AI, increasing corporate mandates for digital transformation, increased brand recognition and increasing number of C3.ai customers (lighthouse model).

The twin-engine of outsized/expanding contract values and decreasing sales cycles leads to rapid revenue growth.

C3’s Rapid Revenue Growth

C3’s grown revenues from $33M in 2017 to $157M in 2020 (88%, 48% and 71% YoY growth, respectively). Put another way, the company generates more revenue per quarter than they did in all of 2017.

The company’s growth plan includes capturing more SMB customers, adding new AI Suite applications/products, and increasing use-cases with existing customers.

Things get exciting when you think about C3’s customers’ tendency to buy 3x their original contract value in add-on services over time. The company has an internal KPI to track its performance: Remaining Performance Obligations, or RPO.

C3 defines RPOs as (from the S-1):

“The amount of our contracted future revenue that has not yet been recognized, including both deferred revenue and non-cancelable contracted amounts that will be invoiced and recognized as revenue in future periods … RPO excludes amounts related to performance obligations and usage-based royalties that are billed and recognized as they are delivered. This primarily consists of monthly usage-based runtime and hosting charges in the duration of some revenue contracts.”

Think of RPO as accounts receivable or deferred revenue. The only twist is RPO includes non-cancelable contracted amounts. That means the company will, at some point, collect that outstanding revenue. It’s important to note that RPO doesn’t include run-time fees for usage-based services.

These revenue segments will grow significantly over time as the company adds services and apps to its platform. RPO won’t recognize this which will understate total outstanding revenue.

C3’s Financials

The company generated $157M in revenue and lost $71M in operating income in 2020. We expect the company to continue showing operating losses as it invests heavily in R&D and customer acquisition. Historically, C3’s spent 41% of its revenue on R&D investments.

For example, the company spent $95M in Sales and Marketing last year, or 60% of revenues. That number will decline over time and show C3’s massive operating leverage. Once they hit critical mass, they won’t need to spend as much to acquire customers. Their lighthouse model will put them as the go-to company for Enterprise AI pick-and-shovel software.

Looking further up the income statement, C3.ai does ~78% gross margin on their subscription revenue and 71% Gm on their professional services. Again, professional services are a small portion of total revenue (14%).

Investors will likely value the company based on its EV/RPO, or expected RPO over the next 5-10 years. This makes sense as RPO is a “leading indicator” of future revenue growth.

Let’s move to the balance sheet.

C3 has $114M in cash and another $175M in short-term investments. This gives them ~$290M in liquid assets against $121M in total liabilities. That’s a strong balance sheet.

Of course, no matter how much we love a company, price matters. Let’s see where C3 will likely IPO and what it means for its market cap and valuation.

C3.ai IPO Price & Subsequent Valuation

The company’s offering 15.5M Class A shares with prices ranging from $31-$34/share. This will bring the total number of Class A shares to 93.9 with an additional 3.5M Class B shares post-IPO (total of 97.4M shares outstanding).

At $31-$34/share you’re looking at an estimated market cap of $3B – $3.3B and ~$2.9B EV ($109M net cash).

Those reading with calculators will clamor, “Brandon, you’re telling me C3.ai will be valued at 19x EV/Sales at IPO?”

Welcome to 2020.

But again, we’re thinking about what the company can do over the next five to ten years. We don’t care about last year, this year, or next year.

The company’s grown revenues at a 94% CAGR since 2017. If we assume the company grows revenue at a 50% CAGR for the next five years we get $1.4B in revenues by 2025. I know, 50% CAGR seems ridiculous.

But C3.ai is just now capturing the lower end of the market while increasing penetration rates in their largest lighthouse customers. To get to a 50% 5YR CAGR we estimated 60% growth in 2021, 55% growth in 2022, 50% growth in 2023, 45% growth in 2024 and 40% growth in 2025.

At $1.4B you’re looking at 2.15x EV/Sales for a fast-growing, first-mover, high switching cost business led by one of the sharpest founders in the game. That sounds crazy cheap when you consider what the company should trade for in five years with those numbers.

If C3.ai gets to >$1B in revenues by 2025, what is a reasonable EV/Sales multiple? 5-7x? That puts us at $7B-$12B in market cap.

Risks

There’s a few main risks with the C3.ai investment outside the normal “technology changes faster everyday” mantra.

First, the company generates a significant portion of its revenue from a small cohort of customers. This will change over time as they penetrate smaller markets. That said, I’m not worried about this risk because their largest customers have increased their usage and spending with C3.ai over time.

Second, C3.ai faces legions (pun intended) of competition from internal IT departments, open-source providers, public cloud providers, and legacy data management product providers. We laid out the case for why these competitors won’t take share, but who knows what AMZN has up its sleeve with AWS. Or Microsoft with Azure for that matter. Which brings us to our third risk.

C3.ai isn’t widely known compared to AMZN or MSFT’s product offerings. If the company fails to reach brand recognition it could stay small and keep a limited number of customers. This then reinforces the first risk of customer concentration.

Concluding Thoughts

C3 is one of the most exciting new IPOs we’ve researched in a long time. It’s one of those companies that got you excited the more you read about it. They have everything we want in a long-term, high conviction bet:

-

- World-class Founder/CEO with ample skin in the game and a great work culture

- Sticky, high switching cost product

- High margin, pick-and-shovel business for a massive digital transformation

C3’s suite of products will generate significant value for their customers over the next 5-10 years. If they penetrate smaller markets and continue to grow their usage with existing customers, equity owners will be happily rewarded with $7B-$12B in shareholder value.