This week’s Value Hive is jam-packed with stock ideas, a public roast of WeWork (and slashing valuations!) and more Michael Burry headlines.

If you haven’t already, make sure to subscribe to this newsletter so you receive it every week, completely free.

Let’s get to it!

—

September 11, 2019

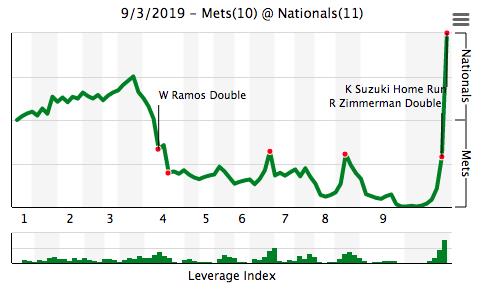

What Are The Odds?! — Late Tuesday night/early Wednesday morning, the Washington Nationals defeated the New York Mets 11-10 via a walk-off homer. Walk-off home runs happen all the time. But can you guess the Nats win probability entering the 9th inning with one man out? Answer down at the bottom!

__________________________________________________________________________

Investor Spotlight: Burry & TLRD are 13-D Official (and his love for Japan)

GIFs by tenor

Last week we highlighted Michael Burry’s public complaint over TLRD’s lack of value creation. Burry demanded a $50M buyback, continued reduction in debt and elimination of the dividend (costing $36M per annum).

This week he put (more) money where his mouth is.

Burry filed a 13D with TLRD raising his ownership take to 2.6M shares (5% outstanding).

Can Burry squeeze out returns from this melting ice cube before time runs out? He’s certainly hoping so.

Burry Loves Japanese Stocks

Making sure he stays in the news, Burry revealed another tidbit. This time, he tells us where he sees value outside the United States. The answer: Japan.

In an interview with Bloomberg, Burry revealed the eight stocks he’s long in Japan:

-

- Tazmo Co (ticker: 6266)

- Yotai Refractories Co (ticker: 5357)

- Sansei Technologies Inc (ticker: 6307)

- Tosei Corp (ticker: 8923)

- Kanamoto Co (ticker: 9678)

- Altech Corp (4641)

What does Burry see in Japan? Alex released his Friday Musings with some data to backup Burry’s bullish tilt.

Alex noted that Japan’s forward P/E ratio is one of the cheapest in the world (12.3). On top of that, Japan is one of only two major economies (Canada being the other) seeing positive economic surprises.

Alex also explains that Japanese earnings expectations are fully reset — which he argues is a great thing for forward equity returns.

While we’re at it, give Alex a follow on Twitter. He posts (in his words) mindless drivel about markets and other things.

__________________________________________________________________________

Movers and Shakers: The Roast (& Value Capitulation) of WeWork

GIFs by tenor

WeWork’s been in the news for all the wrong reasons. Between their Euro League soccer-looking CEO and incredulous valuation, the “tech” company can’t seem to get out of its way.

Unfortunately, things got worse. Way worse.

The week from hell began with Scott Galloway’s public roast of the company’s S-1. The week ended with a valuation slash so severe Ron Swanson would approve.

WeWork Loves Adam Neumann

Going through We’s S-1, Galloway noticed something peculiar. The document oozed with mentions of the company’s CEO Adam Neumann.

Now you might be thinking, “That makes sense, he is the founder of the company”. But things get weird when you compare the amount of founder mentions in We with other companies.

Check out Galloway’s comparison graphic below:

Source: profgalloway.com

Galloway goes so far as to equate WeWork’s culture to a cult around its founder. And who can blame him?

Could WeWork survive if Neumann got hit by a bus tomorrow? Taking the S-1 at face value the answer is most likely no.

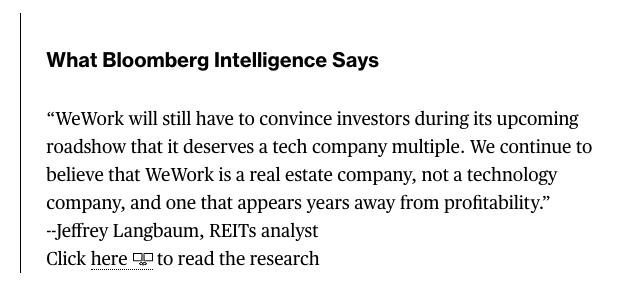

JK We’re Actually 50% Cheaper

If SoftBank loved WeWork at $47B, shouldn’t they love them at $20B? That’s the question the investment giant faces if rumors are true about WeWork’s revised valuation.

According to Bloomberg, WeWork anticipates an IPO around $20-$30B. Many analysts are anticipate the lower bound being the more realistic scenario. So why such a valuation cut?

Wall Street still thinks We is a real estate company, not a tech/SAAS business:

The company’s created accounting metrics that have Ben Graham rolling in his grave:

-

- Community Adjusted EBITDA: Standard EBITDA at first glance, but the company adds “building and community level expenses”. This is (of course) the company’s largest expense and includes tenancy expenses, utilities, internet, salaries and cost of building amenities.

- Adjusted EBITDA before Growth Investments: Standard EBITDA with a bonus exclusion of growth expenses such as SG&A, market development and pre-opening community expenses.

In other words, WeWork looks great if you remove all their operating expenses and costs of doing business. Who else is backing up the truck with me?

__________________________________________________________________________

Idea Backlog: Timber and Burgers (New band name?)

GIFs by tenor

This week we profile two ideas: Keweenaw Land Association (KEWL) and Red Robin Gourmet Burgers (RRGB). One unique asset trading at a discount to land value and the other a turnaround project.

“They Aren’t Making More Land!”

We originally stumbled upon KEWL in a Focused Compounding write-up. The idea later resurrected on Neto’s Notes. After seeing the idea twice, we knew we had to do some digging. So what’s to love about KEWL?

For starters, it fits the bill for a great value investor’s stock:

- Overlooked and underfollowed (trades on the OTC market)

- Rather illiquid trading volume (around 8K shares per/day)

- Discount to asset value (discussed below)

Valuing a Timber Company

Neto takes a differentiated approach to intrinsic value, opting for an acre-per-share metric. The math is simple:

-

- 3M shares outstanding / 184K timberland acres = 0.14 acres per share.

Think of this as our “multiple” for share price valuation. Luckily for us, KEWL appraises their land every three years, with the most recent appraisal conducted in 2018.

The 2018 appraisal valued the land at $160M (or $870/acre). Using Neto’s acre-per-share multiple we can easily figure out an intrinsic value of the land:

-

- $870/acre x 0.14 (acres-per-share) = $112/per share of timber.

Long Term Drivers

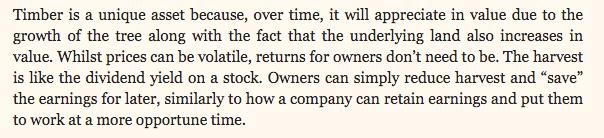

Timber is a unique asset that’s found in many Ivy League endowment funds. The asset class offers uncorrelated compared to other investment options and sports long-term tailwinds for appreciation.

Neto agrees. Check out his take on timber as an asset:

The only thing standing in KEWL’s way of realizing intrinsic value is their debt. Neto argues that the debt is more than manageable. Assuming $870/acre value of timber, the principal balance is less than 10% of the value of the timber.

A Turnaround at Red Robin (RRGB)

Red Robin makes a great burger, but as an investment, not so much. Shares are down 35% since Jan 2018. The driver of underperformance is simple: people aren’t going to their stores.

RRGB’s experienced declining same-store sales three out of the last four years (2017 being the exception). On top of that, as the CorpGov article notes, same-store guest counts dropped 6.4% over the last few quarters.

This could be an early sign of brand erosion.

So what makes Red Robin an interesting value investment idea? There’s two catalysts:

- The company is cheap

- The new CEO knows what he’s doing

Red Robin is Cheap

The company trades around 5x 2020 EBITDA and less than 1x sales. There is an argument to be made that its cheap for a reason — and we don’t disagree.

Restaurants don’t make the best investments. Maybe they deserve to trade at such a low multiple?

Given the poor performance and deteriorating brand, it doesn’t make sense to compare RRGB to other fast/casual dining competitors (SHAK, MCD, SBUX, etc.). They’re not on that level.

Paul J.B. Murphy III is a Stud

The data suggests it’ll take quite the effort to turnaround RRGB. Picking Paul Murphy III is a good start.

Murphy’s held two leadership roles in the past, both generating positive returns for shareholders:

-

- CEO of Del Taco Restaurants, Inc. (TACO)

- Executive Chairman of Noodles & Company (NDLS)

Murphy led TACO through a SPAC IPO in 2015 through 2017. During that time, Murphy helped the taco joint deliver 11 quarters of sames-store sales growth, generating over 30% returns for shareholders (15% CAGR).

After positive results at TACO, Murphy lept to NDLS in June 2017. He led the company to four straight quarters of positive same-store sales. Share prices rose over 50% while Murphy was at the helm (over 20% CAGR).

Can Murphy repeat his past success with RRGB? Time will tell. But if you’re a believer in his past success, 5x 2020 EBITDA smells like a cheap call option on his operational success.

__________________________________________________________________________

Podcast of The Week: Get Stuff Done!

GIFs by tenor

We’re big Tim Ferriss fans at Value Hive, and his latest podcast with David Allen is no exception.

David Allen is a management consultant, executive coach and author of the best-seller Getting Things Done: The Art of Stress-Free Productivity. Ferriss does an excellent job of squeezing out nuggets of gold in the 1 hour 43 minute interview.

Some high-level topics of discussion include:

-

- Your mind’s made for having ideas, not for holding ideas

- Best tips for renegotiating agreements

- Pros and cons of keeping track of information digitally vs analog format

- The capture list

- The two minute rule

- Emptying the in-basket

- Top-down vs. bottom-up systems

Much of what Allen has to say relates to value investing and investor psychology.

We all want to be more productive at analyzing a company, reading annual reports and structuring our days.

_______________________________________________________________________

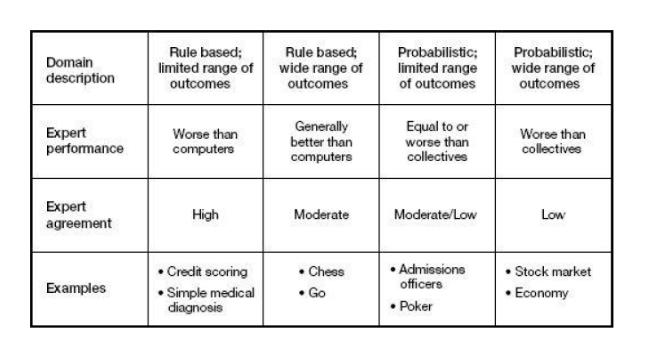

Who Won Twitter? — The Expert Squeeze

Acquirer’s Multiple sent out a great link on Michael Mauboussin’s The Expert Squeeze and Man Versus Machine.

What is the Expert Squeeze? According to Mauboussin, its when “people stuck in old habits of thinking fail to use new means to gain insight into the problems they face.”

Mauboussin claims that experts do well with rules-based problems with a variety of outcomes — even better than computers.

Here’s a handy breakdown of domains, rules and outcomes and which area experts shine in:

While you’re at it, give Michael Mauboussin a follow on Twitter. You’ll thank us later.

_______________________________________________________________________

Bonus Round

Source: fangraphs.com

Source: fangraphs.com

If you guessed the Nats win probability to be 0.03% with one-out in the bottom of the 9th, you’d be correct.

Note how the above graph looks eerily similar to that deep value stock you forgot about diligently held on to as it got bought out.

Tell Your Friends!

Do you love Value Hive?

Tell your friends about us! The greatest compliment we can receive is a referral (although we do accept Chipotle burrito bowls).