“Replicating the post-1990 Chinese experience in those countries would amount to a 15-fold increase of steel output, a more than 10-fold boost for cement production, a more than doubling of ammonia synthesis, and a more than 30-fold increase of plastic syntheses.” ~ Vaclav Smil “How The World Really Works” via this book review by Tom Morgan (link here)

Good morning!

In this week’s Dirty Dozen [CHART PACK] I make case for why we’re likely at a short-term bottom but follow that up with the fact that we still have not seen widescale capitulation/liquidation. This means we have lower to go… We then look at oversold cyclical vs defensives, discuss the New Post-modern Era, and pitch the bull case for Micron, plus more…

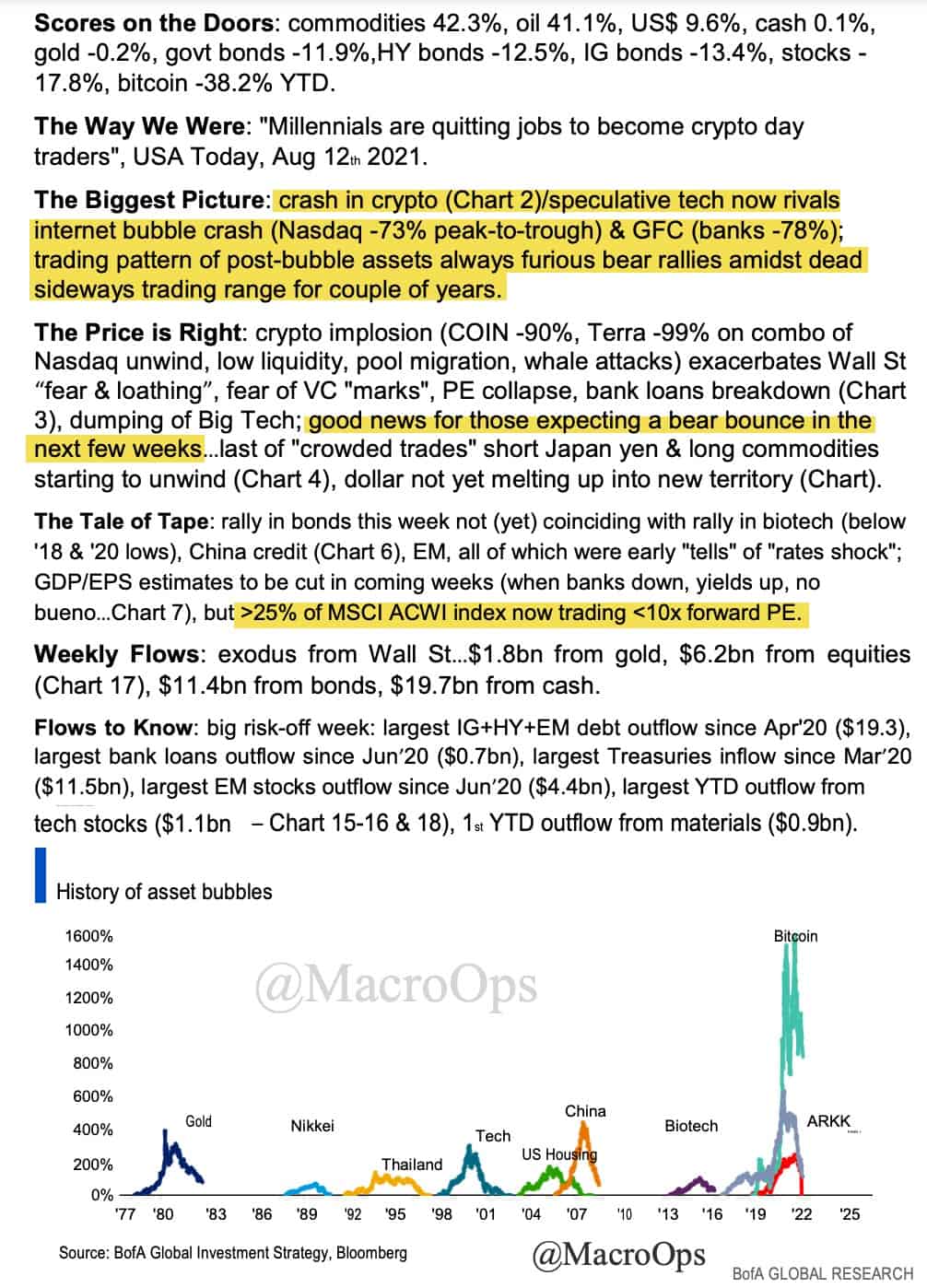

- Here’s the summary of BofA’s most recent Flow Show report summary.

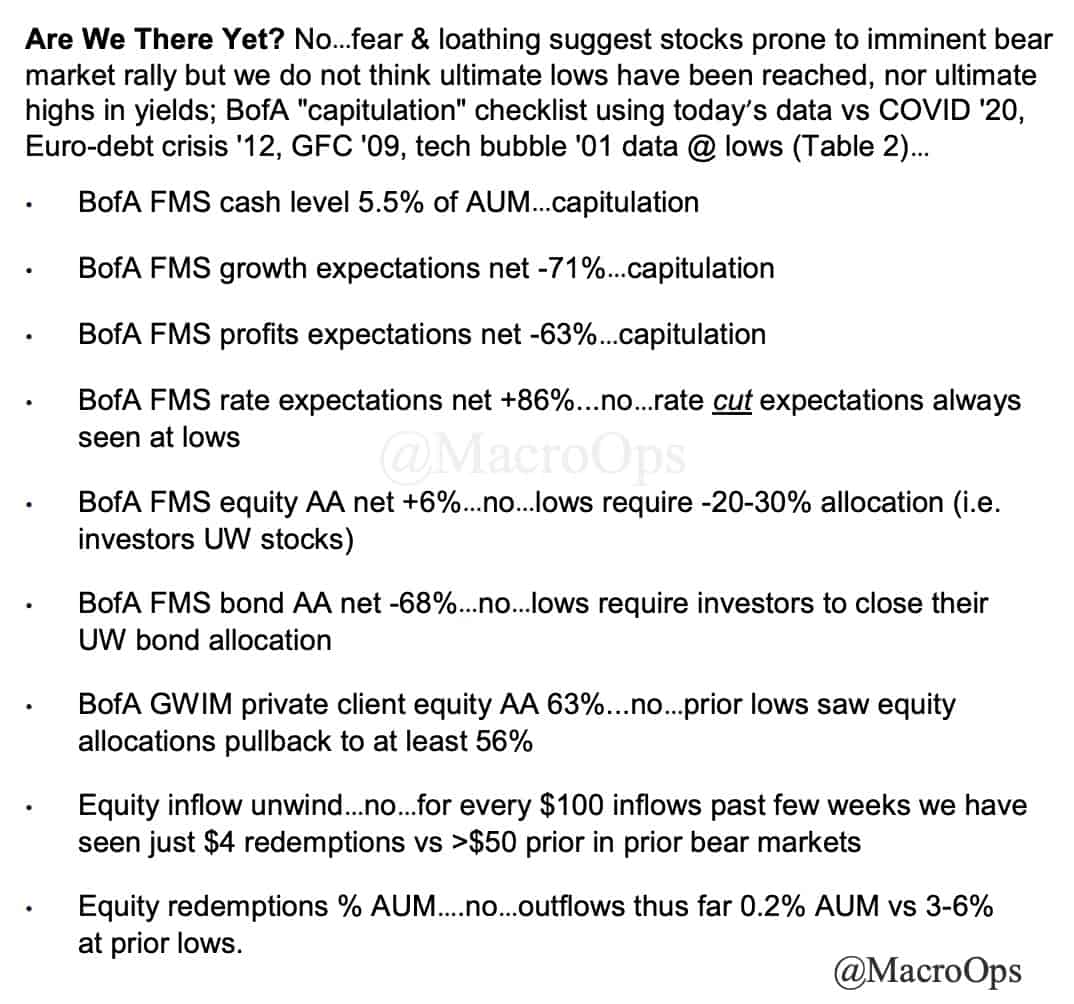

- We’ve seen a short-term flush out which should be good for a temporary bottom. But… we still haven’t seen the type of full-scale liquidations that are needed to cement an enduring bottom. We’re in agreement with BofA on their “capitulation” checklist here.

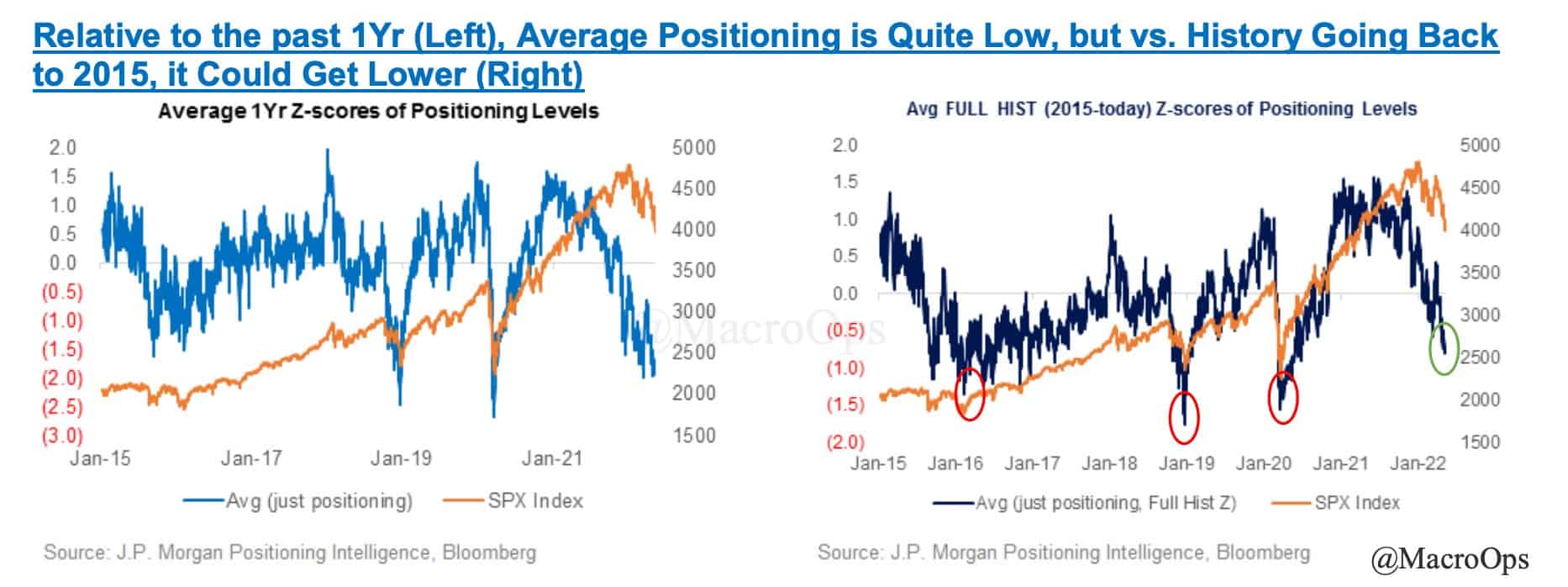

- And JPM illustrates something similar with their historical aggregate positioning showing past major bottoms took place only after more significant degrossing.

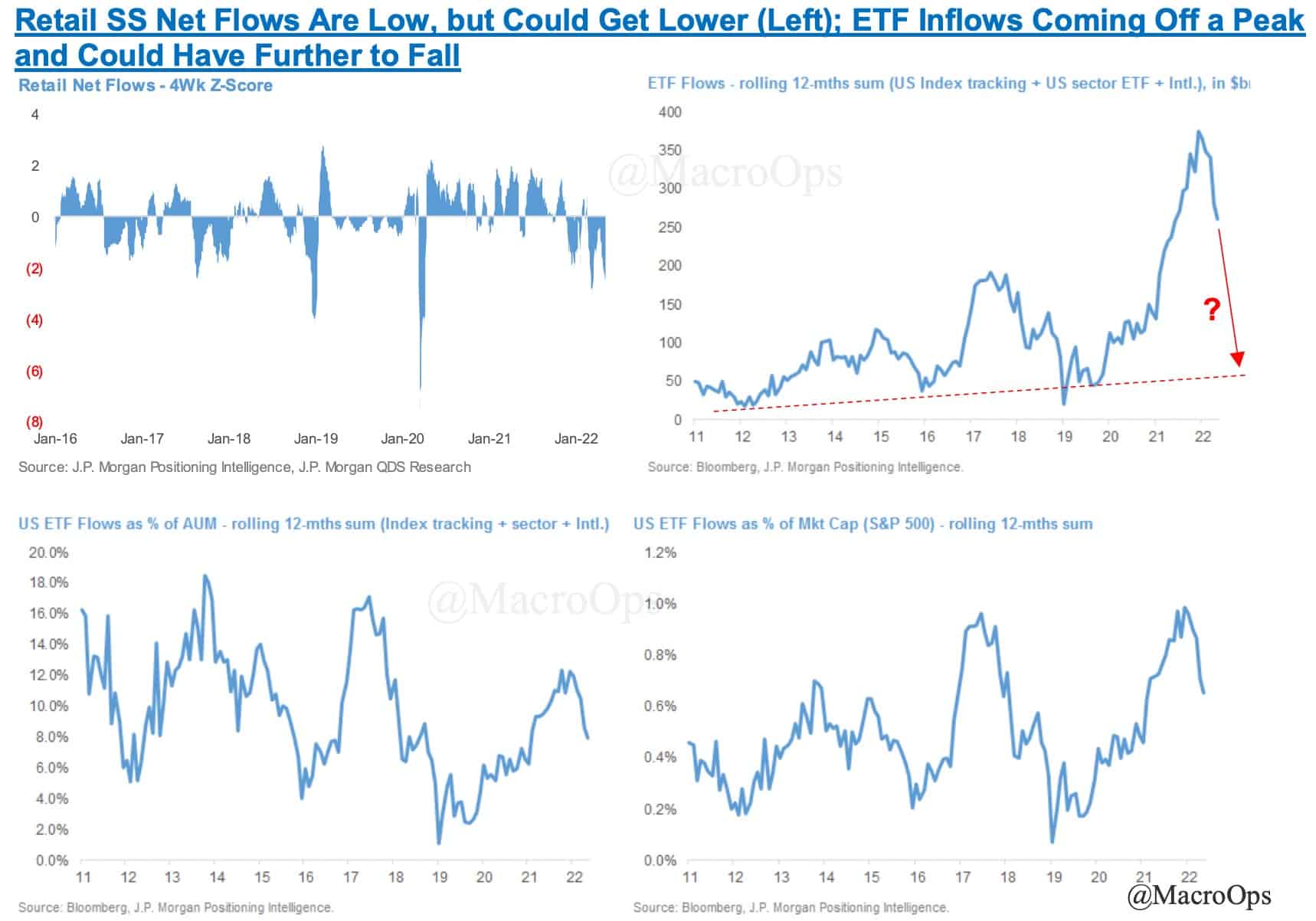

- There’s plenty of retail speculative positioning to unwind, which is something we’ve been pointing out over the last few weeks. Bizarrely, some indicators show retail is still piling into YOLO names like ARKK, GME, and AMC as recent as last week.

It’s this type of entrenched pavlovian stupidity that creates the behavioral and positioning cascades which drive grinding bear markets.

- Our Trend Fragility indicator, an aggregate of various retail and HF positioning, sentiment, and flow indicators, fell to its 3rd %tile on Friday. Its lowest reading since the COVID bear market low.

A reading this low has a solid record of marking a temporary, if not a major bottom. Our guess is this is the former but we could easily see a 6-10% bounce in the major indices over the next few weeks. Last Friday’s 90%+ UpVol day is supportive of this.

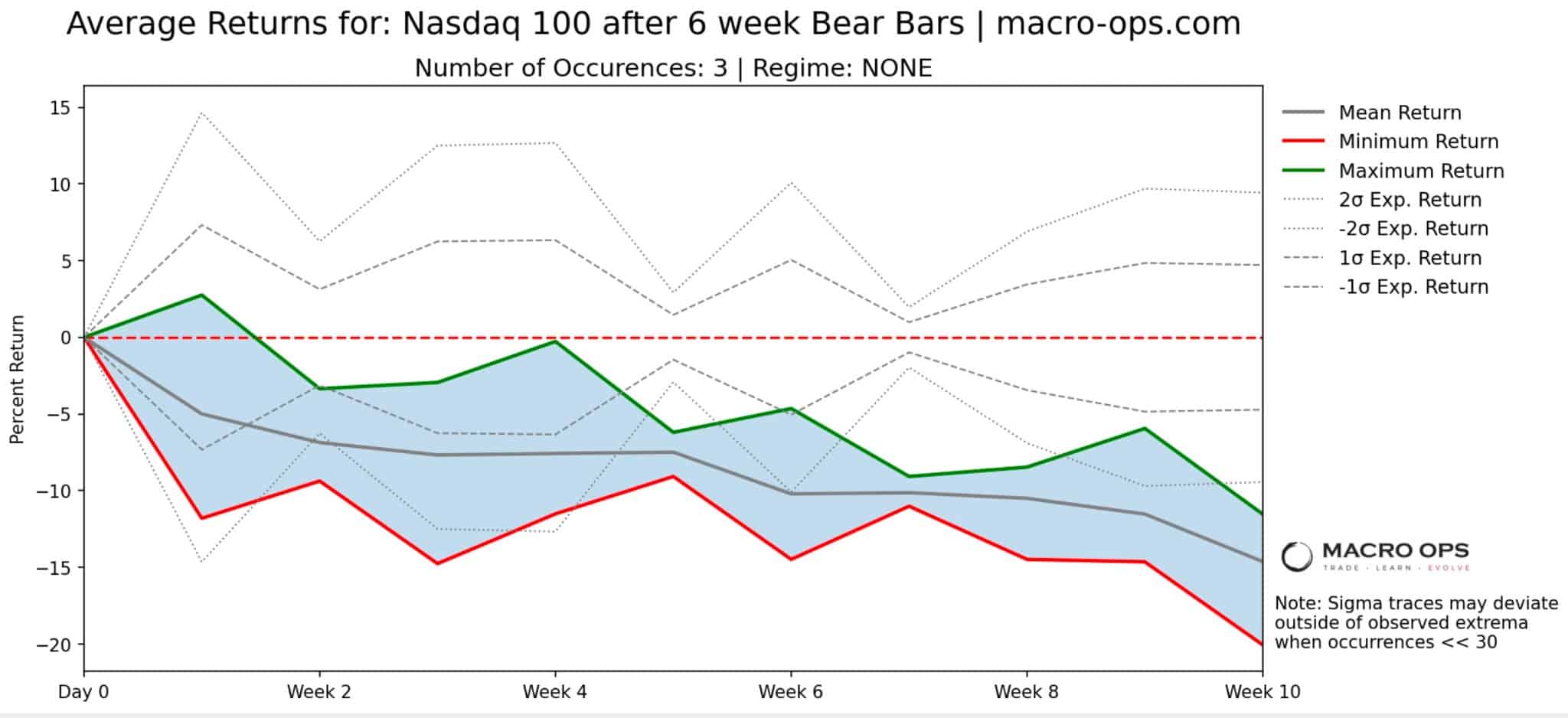

- The major indexes reversed off major support last week (chart is a weekly). Here’s a chart of the Qs… Big lower tail on last week, showing a strong bid going into Friday. However, the Nasdaq has now put in six consecutive weekly bear bars…

- Consecutive bull/bear bars show an imbalance in demand/supply. There higher the number of consecutive bars and the higher the timeframe (daily, weekly, monthly), the higher the signal of the event. Six weekly bear bars is a large bearish impulse and typically leads to more downside in the months ahead.

- Like the Nasdaq, small-caps reversed off major support.

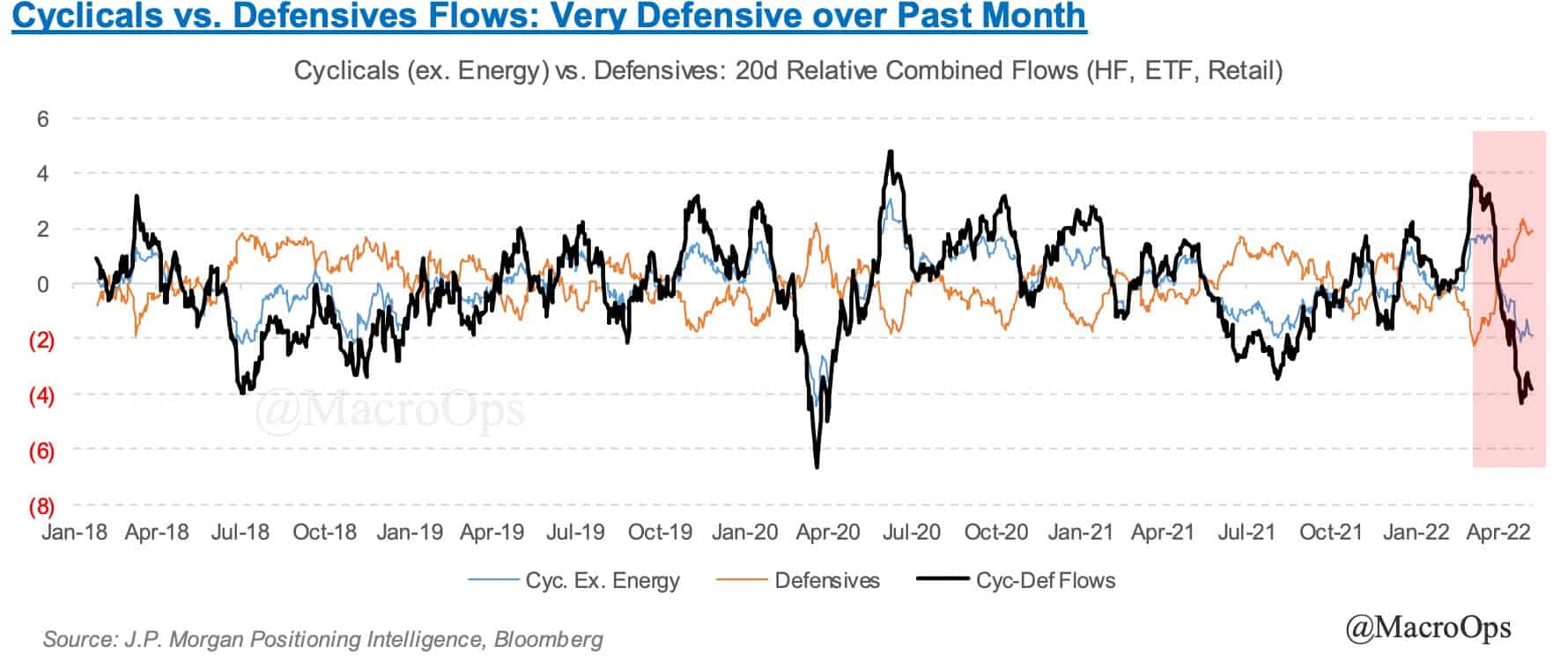

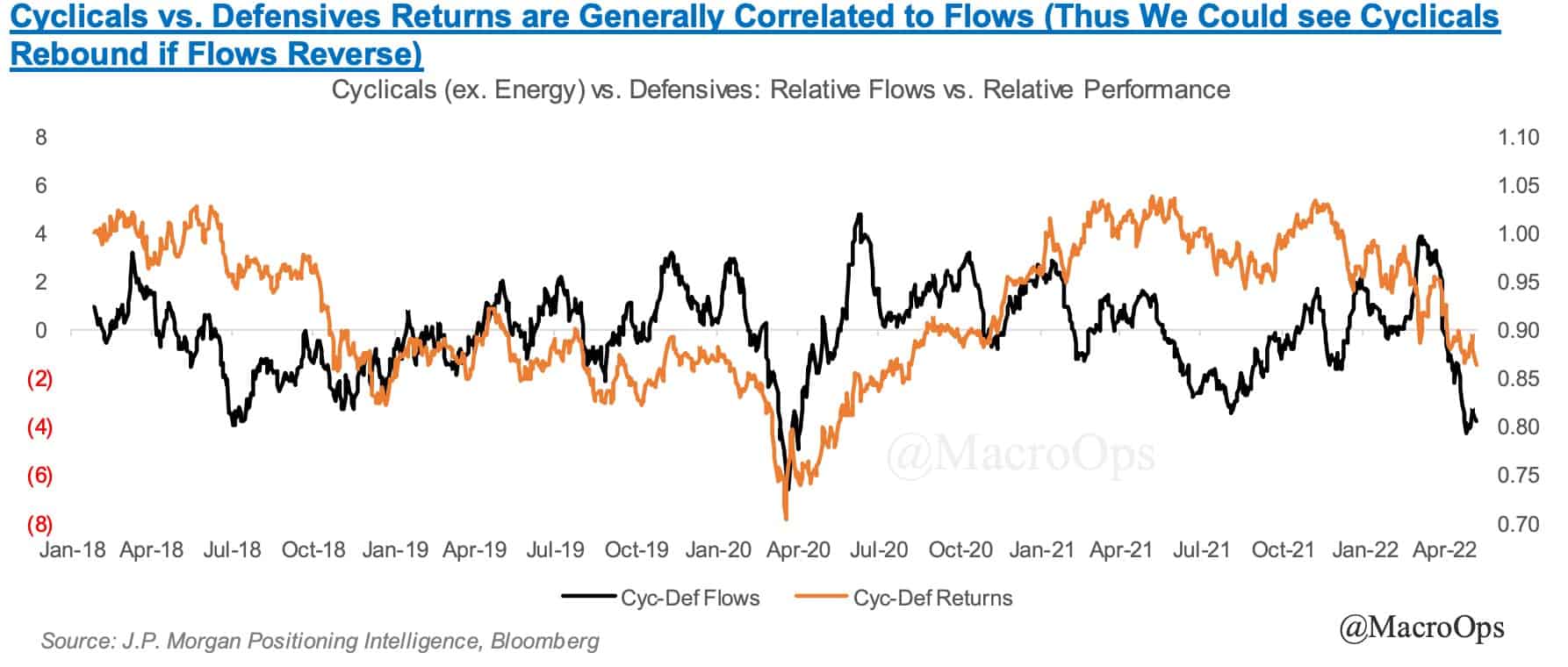

- These charts from JPM show investor flows into Defensive relative to Cyclicals are hitting extremes. If the market doesn’t completely crap the bed here then we might be in for some strong mean reversion favoring cyclicals for a bit.

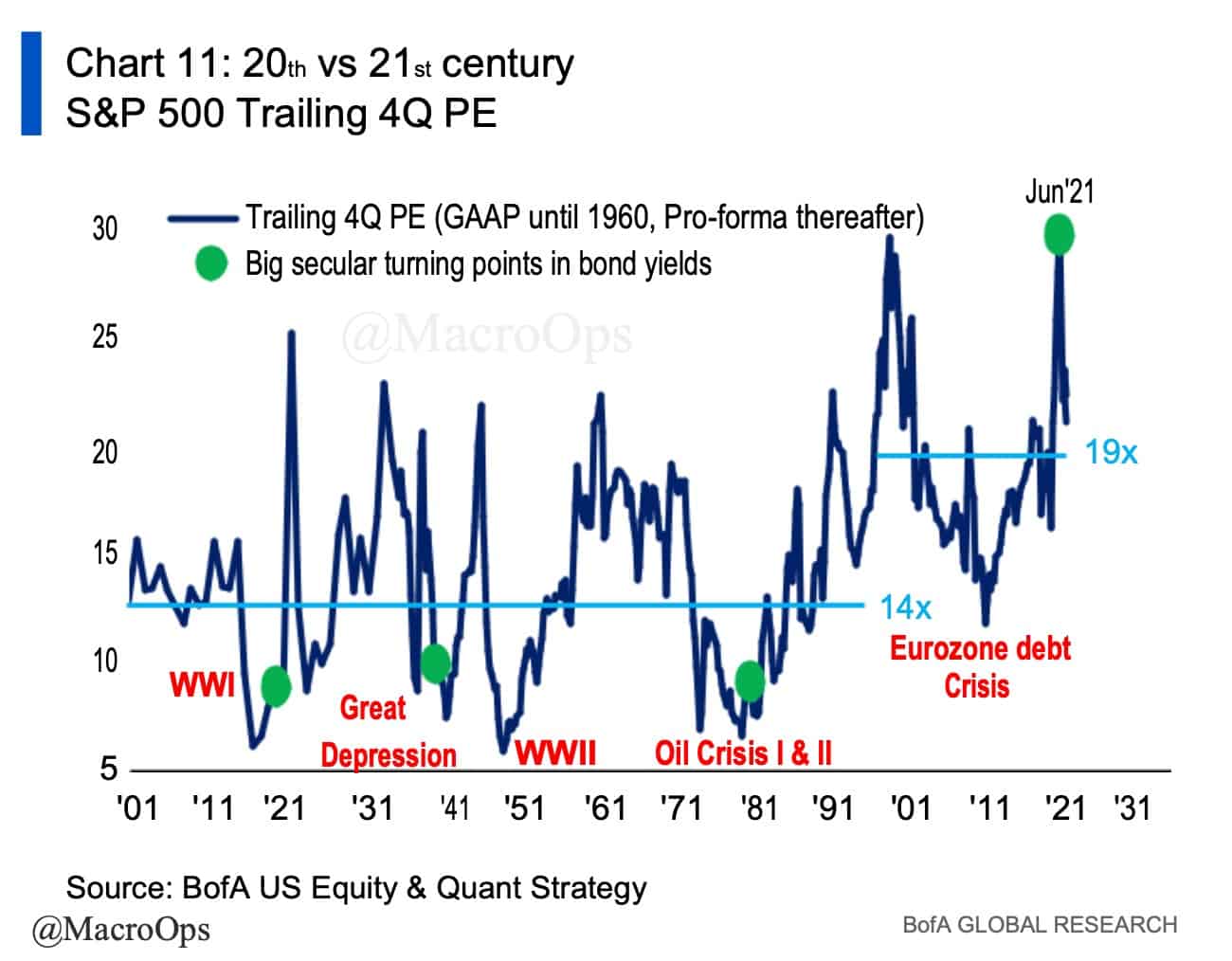

- From BofA: “20th vs 21st century: trailing PE for US stocks in 20th century averaged 14x vs 19x in 21st century thus far; we believe secular inflation driven by trends in society (inequality), politics (populism/progressivism), geopolitics (war), society (inequality & inclusion), environment (net-zero), economy (end of globalization, demographics (China population decline) means higher inflation, rates & reversion of PE to norm (14-16x past 120 years – Chart 11); why we think SPX 3600-3800 potential entry-level, though likely undershoots (note average bear decline = 37.3% & avg duration = 289 days (Table 3) = today’s bear ends Oct 19th ’22 with S&P500 at 3000, Nasdaq at 10000…”

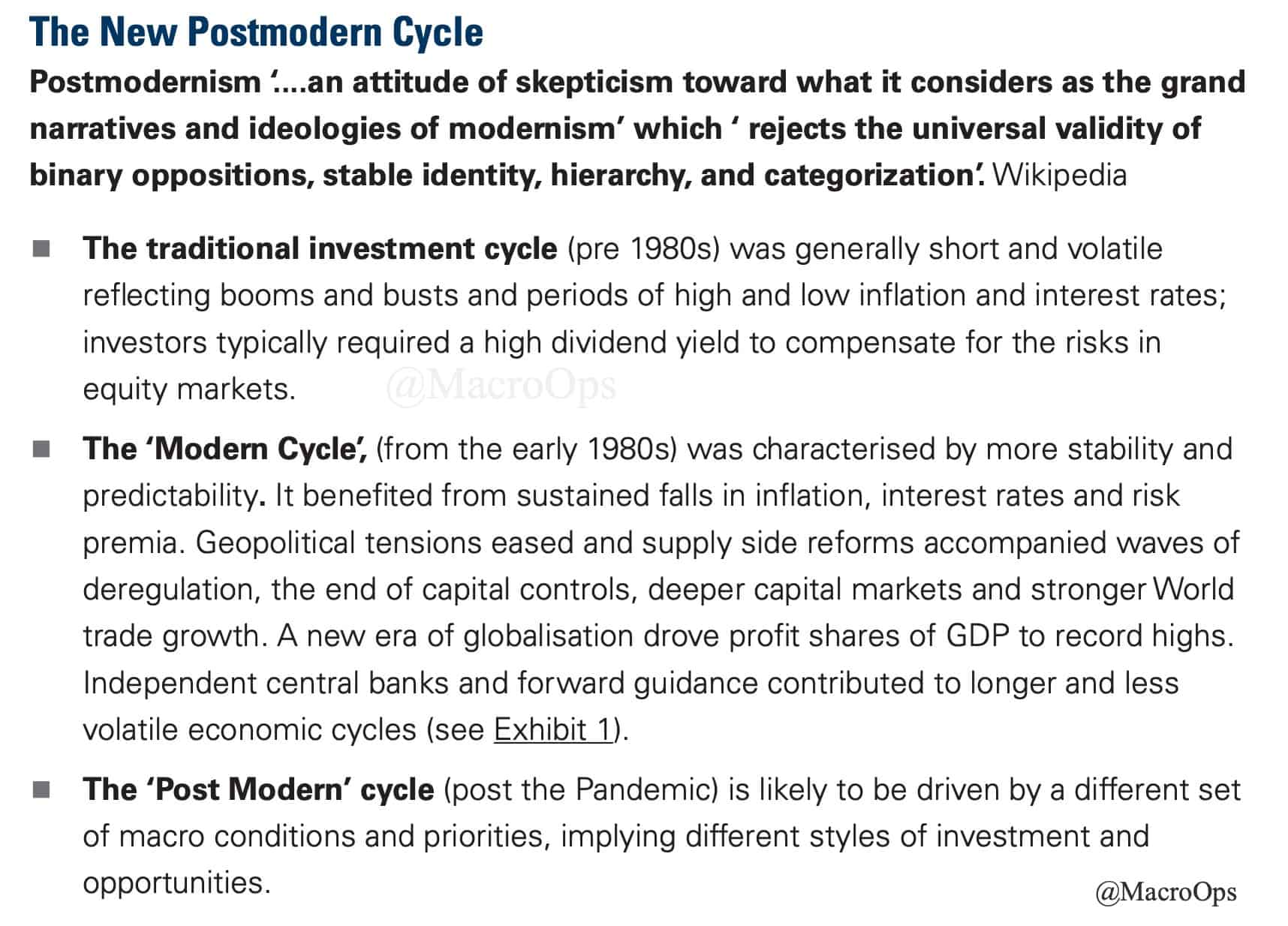

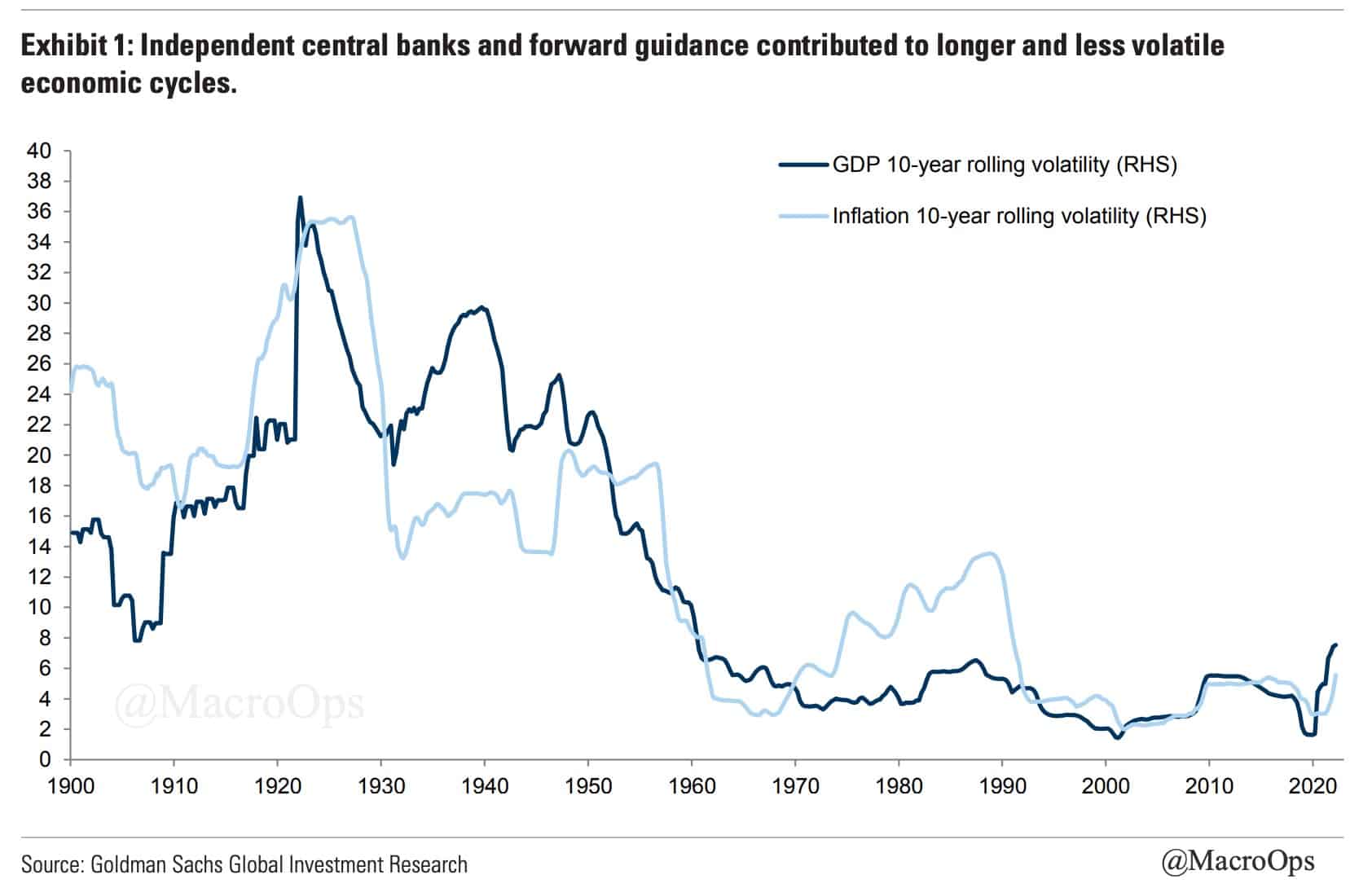

- GS suggests we’re moving into a “New Postmodern Cycle”. I agree, but think it’s important to understand the difference between narrative adoption and large secular changes such as those they’re suggesting. Narratives swing back and forth much faster than changes on the ground actually occur. And narratives such as “The New Postmodern Cycle” are quickly becoming consensus…

- If the cyclical trade does come back in favor then Micron (MU) might be worth a look. The company is about as cheap as it gets. It’s trading at 3.4x NTM’s EV/EBITDA. It’s at major long-term support (chart below is a monthly). And the secular case for being bullish DRAM and NAND is still very much in play (read: Underwriting the Future).

Thanks for reading.

Stay frosty and keep your head on a swivel.