Westlake Chemical Partners LP (WLKP) acquires, develops, and operates ethylene production facilities and related pipelines for its parent company, Westlake (WLK).

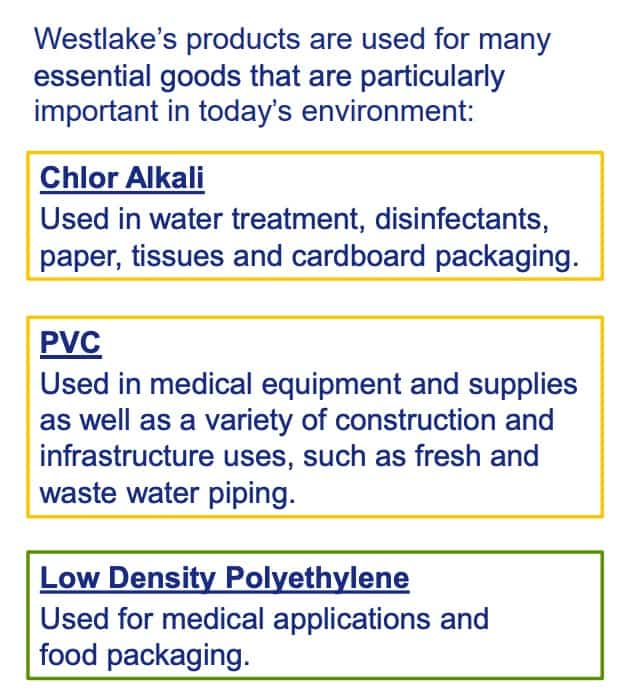

Ethylene is a key ingredient, helping create various finished goods we take for granted.

The plastic wrapping on grocery store chicken breasts? Ethylene. Those chemicals that you use to clean your pool? Ethylene. The PVC pipe plumbers use in construction? You guessed it.

Here’s how the value chain works. Ethylene comes from “Raw Feedstock,” which WLKP gets from another WLK subsidiary.

Here’s how the value chain works. Ethylene comes from “Raw Feedstock,” which WLKP gets from another WLK subsidiary.

This raw feedstock is usually called “ethane.” Ethylene can also be produced from propane and butane. Or from petroleum-derived feedstocks, such as naphtha.

WLKP then provides its parent (WLK) with all the ethylene it needs so WLK can produce the above products.

It’s like one closed-loop system.

Investors looking through the single-point failure embedded in Westlake’s labyrinth will see that WLKP is a good business generating 40%+ ROE at 40% EBITDA margins.

WLKP currently trades for ~12x earnings. As a Limited Partnership, the company pays nearly all its net income to unitholders (same as shareholders) in cash distributions. Since 2014, WLKP has increased its annual dividend payments by ~24%.

Moreover, the company has a strong balance sheet and the industry’s lowest leverage ratios (0.74x Net Debt/EBITDA). WLKP has ~$200M in cash/equivalents against $399M in long-term debt.

We believe the company has a few levers to grow earnings and distributable cash flow over the next few years. Investors should be rewarded through increased cash dividends and a potential re-rating of the stock price due to higher-than-average normalized ethylene demand from WLK.

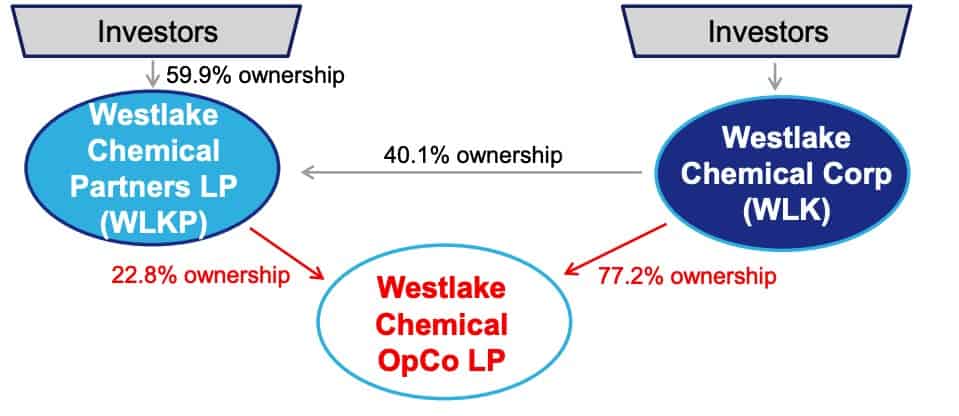

Before diving into the business and value opportunity, let’s level-set how Westlake organizes its machine. Check out the graphic below for a quick guide.

In short, WLKP owns a 22.8% interest in “OpCo.” OpCo is the company that actually provides WLK with ethylene for finished goods. Westlake Chemical (WLK) owns the remaining 77.2% of OpCo LP.

We’re not done yet. WLK also owns ~40% of WLKP, with the remaining 59.9% owned by public unitholders (you and I).

Clear as mud, right?

While confusing, it’s important to nail these percentages because they determine how much cash flow we (as public unitholders) are entitled to. That’ll make more sense later.

Alright, onto the OpCo business.

WLKP owns three main assets:

The partnership’s three ethane-based processing facilities produce ~3.8B lbs of ethylene.

That’s a lot of (potential) PVC pipe.

WLKP uses these assets to sell ethylene to WLK and other third parties. WLK relies heavily on WLKP’s ethylene supply for all its products (polyethylene, Styrene, PVC, and Building Products). This reliance comes from “Not In My Backyard-ism” or NIMBYISM. WLKP’s ethylene assets are conveniently located near WLK’s PE production facilities.

Additionally, WLK is starving for ethylene products. Despite access to WLKP’s 3.8B lb capacity, WLK still requires ~2B more pounds of ethylene annually that WLKP can’t yet fulfill.

WLK also owns nearly 80% of the partnership, and they want those sweet distributions! WLKP knows this and structures lucrative deals for themselves (hence the 40% ROEs and 40% EBITDA margins).

Let’s break down that deal.

WLKP and WLK entered into a 14-year Sales Agreement in 2014 (at WLKP’s IPO). In short, the agreement states that WLK must provide a $0.10 per pound margin on 95% of WLKP’s processed ethane.

Let’s use an example. Say WLKP will generate 100lbs of ethylene in 2022. Of that 100lbs, WLK will pay at least a $0.10 per pound margin on 95lbs. WLKP is free to sell the remaining 5lbs to third parties at spot prices.

This creates a floor for WLKP and their 3.8Blbs of ethylene capacity, which provides stability in earnings and distributable cash flow. It doesn’t matter how much ethylene WLKP produces in a given year. WLK must purchase 95% of the volume at a $0.10 per pound margin.

We see the power of this earnings stability over time, too. For example, since 2014, WLKP has increased its distributable cash flows from <$20M to over $65M in 2020. Look up “stability” in the dictionary, and you’ll likely find this picture below (WLKP’s quarterly distributions).

Stability is noteworthy, and at 12x earnings, investors should generate a decent return. But what about future growth? What levers can WLKP pull to accelerate distributions and increase its share price?

The company outlined four main growth levers:

Levers 2 and 3 are self-explanatory, but let’s quickly review them. WLKP can expand organically by increasing the amount of ethylene it can process in its facilities.

It can also expand by buying/partnering with new processing facilities. For example, WLK has a joint venture with Lotte Chemical to build a new 2.2B lbs ethylene cracker processing facility. WLKP could eventually acquire an ownership stake in that.

However, I want to focus on levers 1 and 4, as they are the least capital-intensive.

Increased ownership in the OpCo would mean a more significant percentage of the OpCo’s net profits, which means higher distributions for public unitholders. WLKP has done this in the past. In 2015 they bought 2.7% more of OpCo for $135. Then in 2017, they bought another 5% for $229M. Finally, in 2019 they purchased an additional 4.5% for $201M.

Then there’s margin expansion. Remember the $0.10 margin floor WLK must pay WLKP on 95% ethylene volume? Well, data suggests WLKP could raise that floor. Check out the graph below.

Notice how often ethylene margins are above the $0.10 floor in the Sales Agreement. WLKP could potentially renegotiate a higher base, say, $0.15. That would mean greater stability on higher profit margins — a killer combo.

As we mentioned earlier, the apparent risk is the single-point failure system that is WLK. WLKP generates basically all its revenue from WLK. Any severe slowdown in WLK demand will directly impact the partnership’s profits.

However, WLK is also a good business with a solid balance sheet. Since 2011, WLK has compounded revenues at 12.5%, EBITDA at 20%, and FCF at 25%. Additionally, WLK has nearly $2B in cash on the balance sheet, while FFO covers interest payments 14x over.

WLK is a cyclical business. There’s no way around it. Will it have trough earnings years? Yes. Could a given year’s sales, margins, and cash flows decline or be lumpy? Of course.

Ten years from now, WLK should sell more ethylene-based products than today. Housing demand is a rough (yet applicable) proxy for ethylene-based product demand as WLK sells Building Products and PVC pipes for construction.

Let’s assume WLKP grows net income by ~3% over five years. That gets us ~$94M by 2026.

Let’s also assume the company pays out ~80% of its net income as cash distributions to unitholders, or ~$72M/year. That gets you ~$2/share in annual cash distributions per year.

Today, you can buy the business for $29/share. Assuming < GDP net income growth and an 80% payout ratio, investors get ~35% of their money back within 5 years.

Within five years, WLKP could pay off most of its LT debt, expand WLK’s base profit margin, and generate even higher distributions for unitholders.

So will you get a 25% CAGR at today’s prices? No. WLKP is a good business trading at a reasonable price with a ~7% dividend to boot. Over time, shareholders should be rewarded.

Disclosure: Fund(s) managed by the author own shares in WLKP.