Telefonica Brasil (also called Vivo) is Brazil’s largest telco operator with a 33% market share. Vivo boasts 96M total accesses, 3.7M fiber-to-the-home connections, and passes 16.3M homes.

The company’s core businesses include mobile, handsets, FTT (fiber-to-home), digital services, data and ICT, and Internal Protocol Television (IPTV). These core businesses generate ~90% of Vivo’s revenue.

Our Variant Perception: On the surface, VIV is just another telco company with its consortium of fixed, mobile, and fiber businesses. Yet look deeper, and you find a company rapidly transforming into a digital, one-stop-shop hub for its 96M Brazilian customers.

Vivo’s core businesses generate sustainable cash flows that allow the company to invest in its digital transformation. These investments include an e-Health platform and major FinTech initiatives like consumer loans and credit cards. The end game is a Vivo-first Super-App for every consumer’s need.

At the current stock price, you’re getting the entire Digital Services business for free.

Vivo generates gobs of cash and sports one of the most robust balance sheets we’ve ever seen in a telecom operator. Vivo makes enough money to reinvest in its fiber growth, accelerate its digitization efforts, and pay shareholders an 8% dividend yield while buying back 5M+ of its shares.

Vivo’s stock price collapsed nearly 40% since January 2020, thanks mainly to the Real’s depreciation versus the dollar. So what do we get at these market prices?

Mobile accounts for ~65% of Vivo’s revenues. Last year the company generated BRL 43.12B in revenue or roughly BRL 28B in mobile revenue. Assuming a historical 40% EBITDA margin on our mobile revenues gets us ~BRL 11.2B in EBITDA.

In other words, you can buy Vivo’s market-leading mobile business for ~7x EV/EBITDA and get every other business segment (fixed, handsets, digital services, data & ICT, and fiber) for free.

Assuming steady-state top-line growth and ~40% EBITDA margins, Vivo should generate nearly BRL 53B in revenue and BRL 24B in EBITDA by 2025.

At a very conservative 7x EBITDA multiple, you get over 100% upside from the current stock price. But, of course, that’s not including the 8% dividends you collect while you wait.

Vivo’s Two Core Businesses: Mobile & Fixed

Our variant perception hinges on Vivo’s core idea to create a digital hub or SuperApp-like experience for its customers. The more customers it captures, the more easily it can convince its existing users that Vivo is all they need.

The company has two primary weapons for customer acquisition:

- Mobile Pre-paid/Post-paid user growth

- Fiber-to-the-home connections and homes passed growth

Let’s dive into each business segment.

Vivo’s Mobile Business: Pre/Post-Paid & Handsets

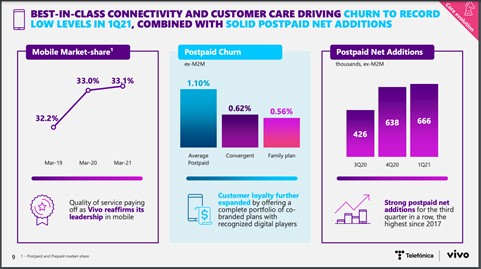

Vivo’s Postpaid business generates ~70% of its mobile business revenue and commands ~37% of its market. ARPU’s have increased each of the last four quarters, and average churn rates remain ~1%. Moreover, the company’s increased net additions each of the previous three quarters, with Q1 recording its highest net addition since 2017.

Not to be outdone, Vivo’s prepaid segment boasted strong QoQ results in Q1 2021. Prepaid revenues grew 4% vs Postpaid’s -0.6%. Plus, the segment experienced a 28.8% increase in digital top-ups.

This means Vivo customers are consuming more data from digital sources and increasing the adoption of Meu Vivo (Vivo’s e-Care app, which we’ll examine later). Along with increased top-ups, the company saw an 8.3% increase in customers topping off.

Said plainly, more customers are using more data than ever before to consume more significant amounts of digital content.

The company also generates revenue from selling handsets. Yet it’s such a small part of total sales that it’s not worth discussing in-depth (if you’re dying to know, read the 20-F).

Alright, onto the second segment: Fixed Revenue

Vivo’s Fixed Business: Fiber, IPTV, and Data/Digital Services

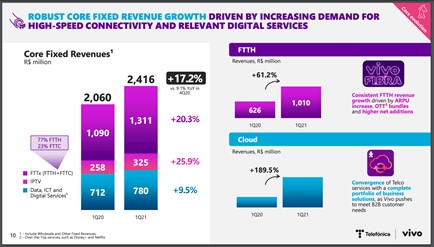

Vivo’s core Fixed business is comprised of FTTH/FTTC (also called FTTx), IPTV, and its Data, ICT, and Digital Services segments. As of Q1 2021, FTTx generated ~54% of Core Fixed revenues, followed by Data/Digital Services at 32% of revenues.

The company’s FTTH segment benefits from two main tailwinds: increased demand for fiber and higher-value customers to drive ARPU. For example, Vivo set a record in Q1 by adding 368K net homes on its fiber (up to 2.1x from Q1 2020).

Of those new additions, 30% required at least 300Mbps internet speeds and Video OTTs (like Netflix & Disney+). Faster speeds and broader video offerings equal higher revenue per household. In fact, Vivo increased its FTTH ARPU by 16%, from R 82 in 2020 to 95 in 2021.

Of those new additions, 30% required at least 300Mbps internet speeds and Video OTTs (like Netflix & Disney+). Faster speeds and broader video offerings equal higher revenue per household. In fact, Vivo increased its FTTH ARPU by 16%, from R 82 in 2020 to 95 in 2021.

FTTH demand will increase as more Brazilians choose faster internet speeds to consume more significant amounts of digital content (NFLX, etc.). As the largest telco in the country, Vivo is one of the few telcos that can meet the demand through its extensive fiber investment.

Vivo’s end game is simple. Get enough customers/households on the Vivo “rails” system and cross-sell them with other digital-based one-stop-shop offerings.

Let’s see what the end game looks like.

Vivo’s End Game: Creating A Super-App

Charlie Munger once said of management, “show me the incentive and I’ll show you the outcome.” The quote could easily read, “Show me the customer distribution channel and I’ll show you the Super-App.”

Vivo is perfectly positioned to create its own Super-App. For example, it has access to 96M individuals and connects 3.7M households to the internet while passing through another 16M+. In addition, Vivo already offers extensive billing capabilities, providing payment alternatives for customers without a bank account.

Its Meu Vivo e-Care app allows customers to pay phone bills, share internet, and view plan benefits, with 18.6M unique users. Moreover, Vivo is the 3rd largest traffic portal in the country, with more than 200M monthly visits through its Terra subsidiary. Finally, Vivo has over 1,600 physical retail stores, making it one of the largest retailers in Brazil.

Of course, this doesn’t guarantee Super-App success. But it does reveal all the ingredients necessary for a Super-App to work.

Vivo has four new business segments (on top of the factors mentioned above) that should bolster its Super-App chances. They are:

- Vida V

- Vivo Pay

- Vivo Money

- Vivo Itaucard

Let’s break each down.

Vida V

Vida V is Vivo’s e-Health platform. Powered by Teladoc, Vida V allows anyone to instantly schedule doctors’ appointments, pre-screen symptoms via AI, and request prescriptions right on their phone.

Vida V is Vivo’s e-Health platform. Powered by Teladoc, Vida V allows anyone to instantly schedule doctors’ appointments, pre-screen symptoms via AI, and request prescriptions right on their phone.

Vida V users will also gain access to discounts in 27K+ drugstores throughout Brazil, whether or not have you have a private healthcare plan.

Vivo Pay, Vivo Money, Vivo Itaucard

Vivo’s free digital account for all things money. Not exclusive to Vivo customers, Vivo Pay users can shop online with virtual prepaid cards, transfer cash to other banks, and pay bills or top-up. Inside Vivo’s finance offering is Vivo Money.

Vivo Money offers personal loan services, starting with postpaid and hybrid customers. The app provides easy, 100% digital loans with highly competitive interest rates. In addition, Vivo’s grown its credit origination business 2x from December 2020 to March 2021 and 2.5x from October to December 2020. Finally, there’s Vivo Itaucard, a co-branded credit card with Itau Bank.

The goal with the Itaucard is to stimulate sales in Vivo’s physical stores and digital marketplaces. Vivo Itaucard credit cards allow for flexible, 21-month installments and offer up to 10% cashback on specific products and services (most likely Vivo-owned products).

A Cash-Generating Machine Waiting For Inflection

If Vivo’s Super-App works, Digital Service revenue will slowly gain a more significant portion of total revenue. When it does, gross and EBITDA margins should increase as its Digital Services revenue is higher-margin than the more capital-intensive Mobile/Fixed units. Until then, the company’s content with generating R 11B+ in annual free cash flow from its two core businesses.

Vivo is an excellent business with sticky customers and excellent service. The company will continue to lay more fiber, connect/pass more homes, and command a more significant share of Brazil’s fiber infrastructure. However, churn rates should decline in its mobile business as Vivo offers a more substantial number of services like 5G and its marketplace of Vivo apps.

Remember, at the current market price, Mr. Market is assigning a $0 valuation on Vivo’s Digital Services business. In other words, we’re not paying for any future Digital Services growth at today’s price. So it’s a free call option.

A shift in revenue from mobile/fixed to Digital Services will bolster gross/EBITDA margins. Our base case assumes zero EBITDA margin expansion over the next five years with ~4% annual revenue growth. In this case, we end 2025 with R 52.8B in revenue and R 22B in EBITDA.

Assume a ~7x multiple on 2025 EBITDA, and you get ~R 154B in Enterprise Value. Subtract another R 6B in net debt (this includes capital leases), and you have R 148B in market cap or ~$17/share (100%+ upside).

Short-Term Catalyst: BRL/USD Pattern Breakout

We could see a short-term price catalyst thanks to the BRL/USD currency pair. The pair’s chart looks ripe for a reversal breakout favoring higher BRL prices (see below).

Should we get a clear breakout, it would signal risk-on for BRL-denominated assets, like VIV.

Also, note that this pattern could roll over, and BRL could continue its downtrend, which would act as a significant headwind for VIV’s share price appreciation.

Closing Thoughts

Vivo is a great business with sticky customers and excellent service. The company will continue to lay more fiber, connect/pass more homes, and command a more significant share of Brazil’s fiber infrastructure. Churn rates should decline in its mobile business as Vivo offers a more considerable number of services like 5G and its marketplace of Vivo apps.

Investing in Brazil carries its domain-specific risks, including:

- Political

- Currency

- Governance

Mr. Market has discounted these risks and more In the current stock price. VIV is unlike any other telco. Remove its capital leases, and it has a net cash position. Finally, VIV has a history of returning capital to shareholders in dividends and share buybacks.

Just imagine the return investors could see if the company’s Super-App kicks off and the stock re-rates towards its peers.