“That’s a raisin at the end of a hotdog…” ~ Icelandic saying denoting surprise

In this week’s Dirty Dozen [CHART PACK] we talk market returns following first rate cuts, negative fiscal impulse, bad market internals mixed with high sentiment/positioning, some interesting VIX stats, and more…

1. Last week’s highlights from BofA’s Flow Show report.

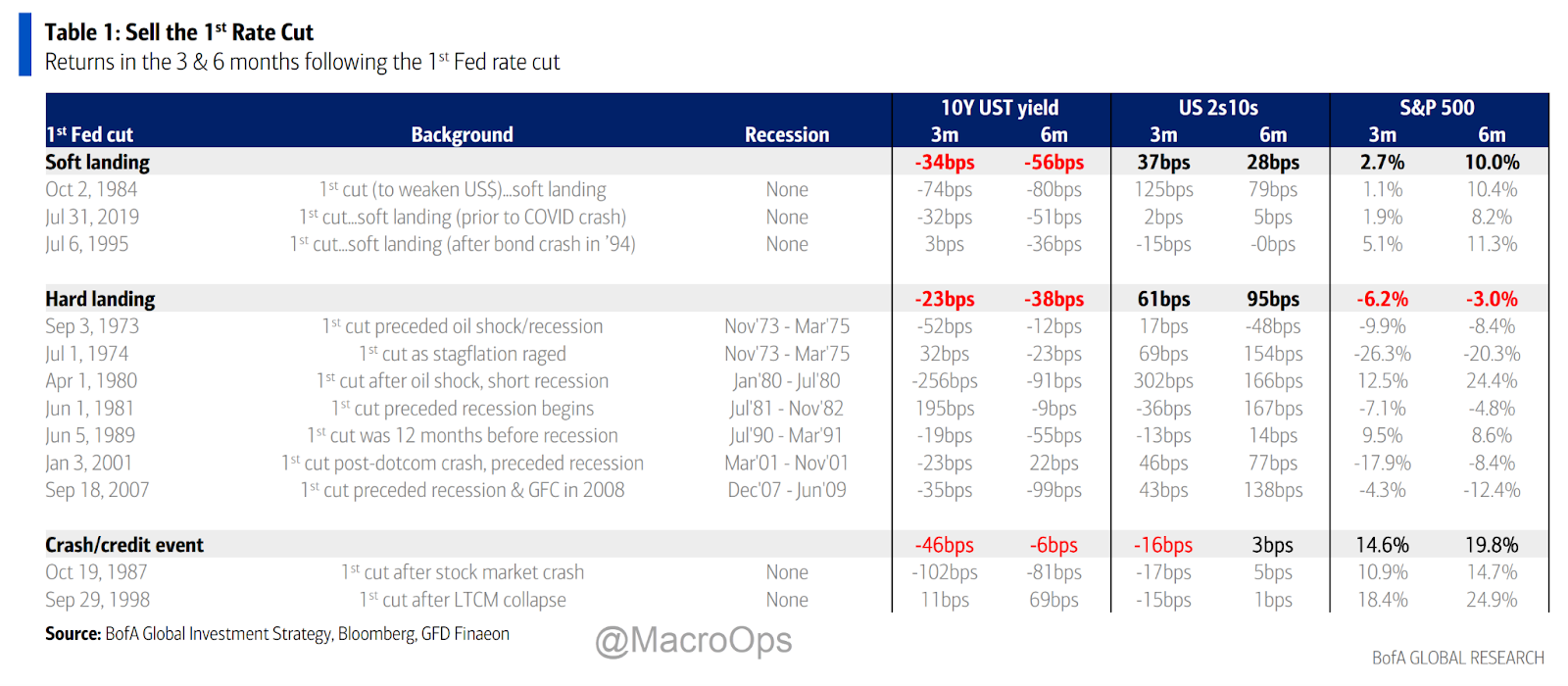

2. BofA on the three different types of rate cuts.

3. Market returns following the first rate cut in the three different rate-cutting environments.

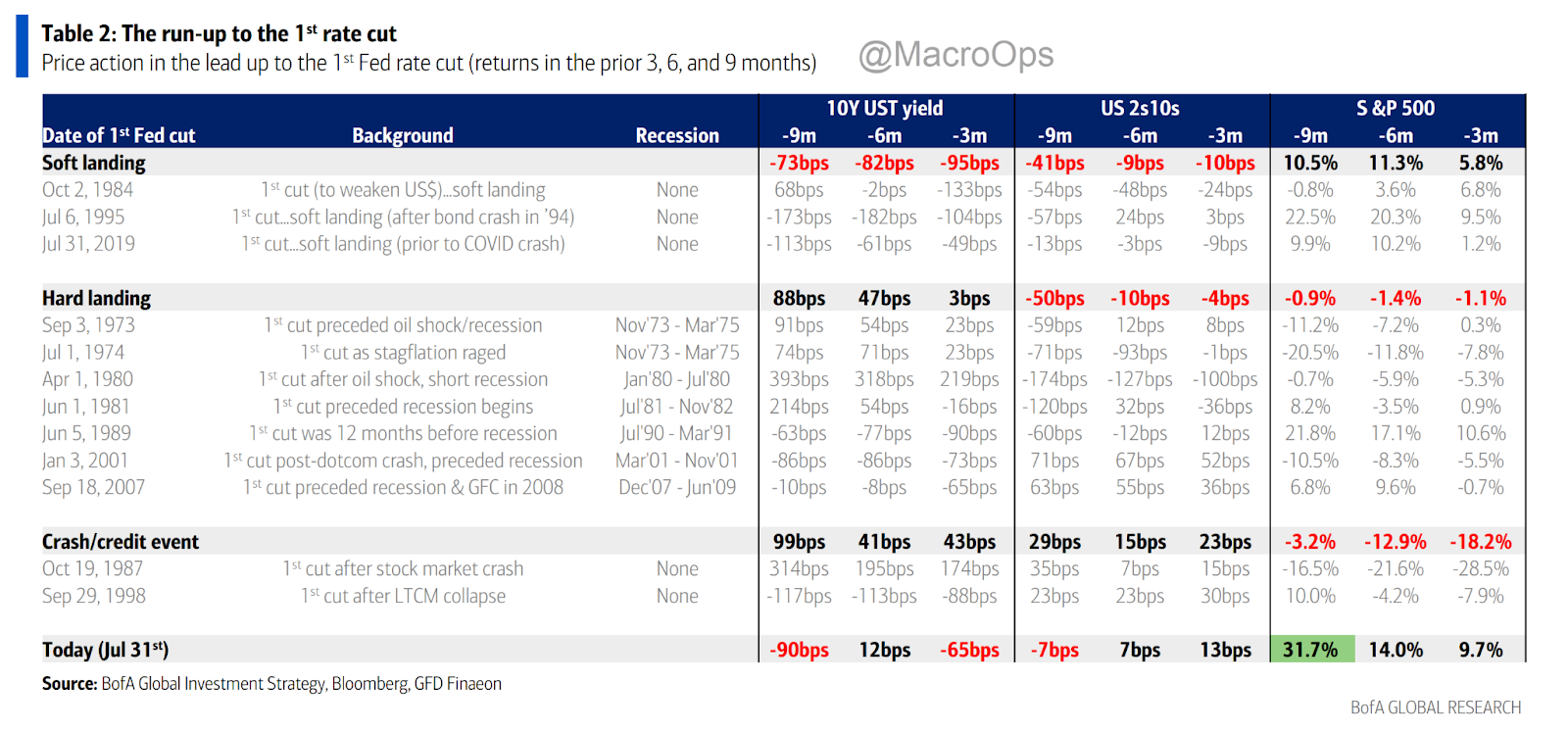

4. And market returns in the lead-up to the first rate cut. This time is the anomaly with the SPX up over +31% over the past 9 months.

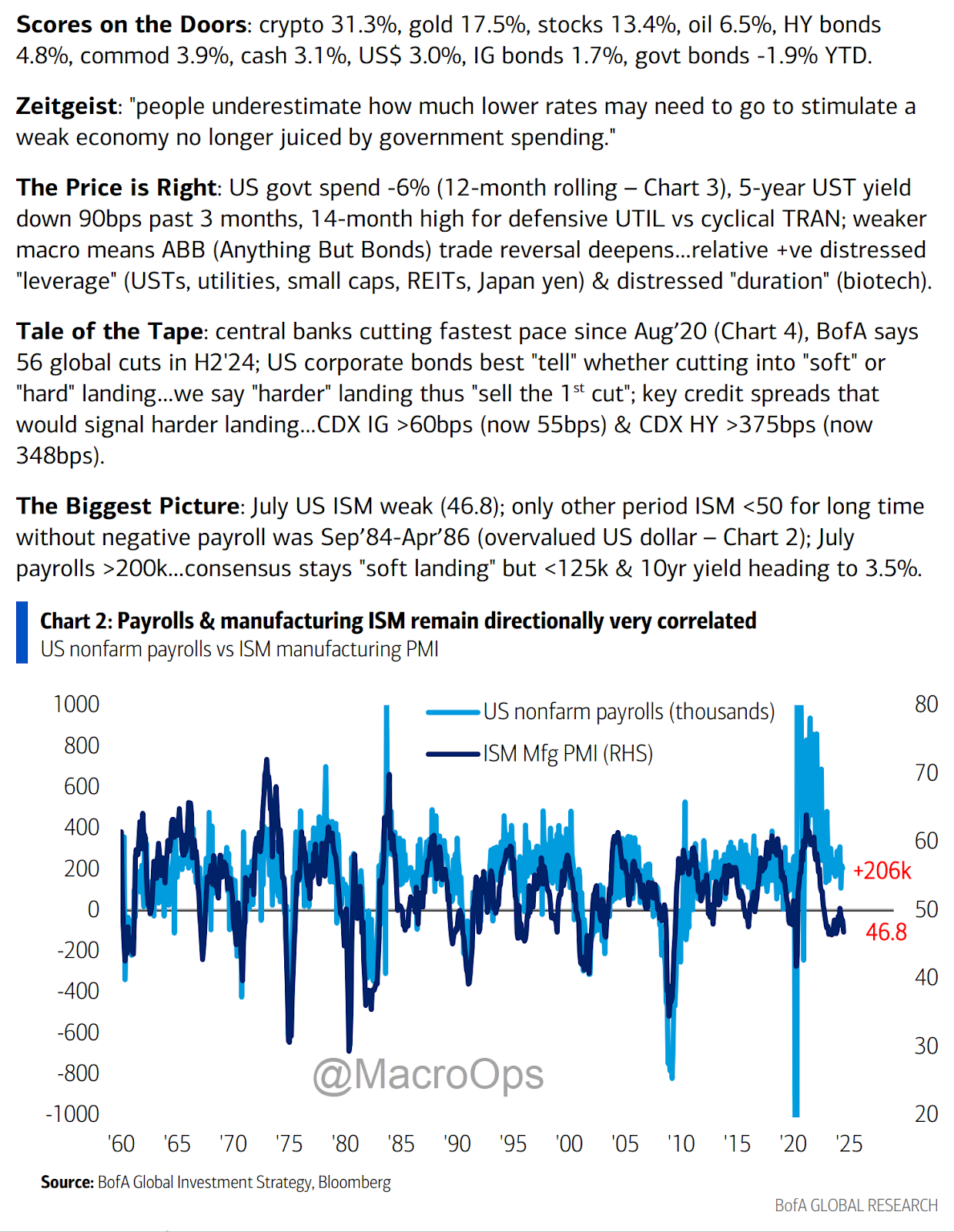

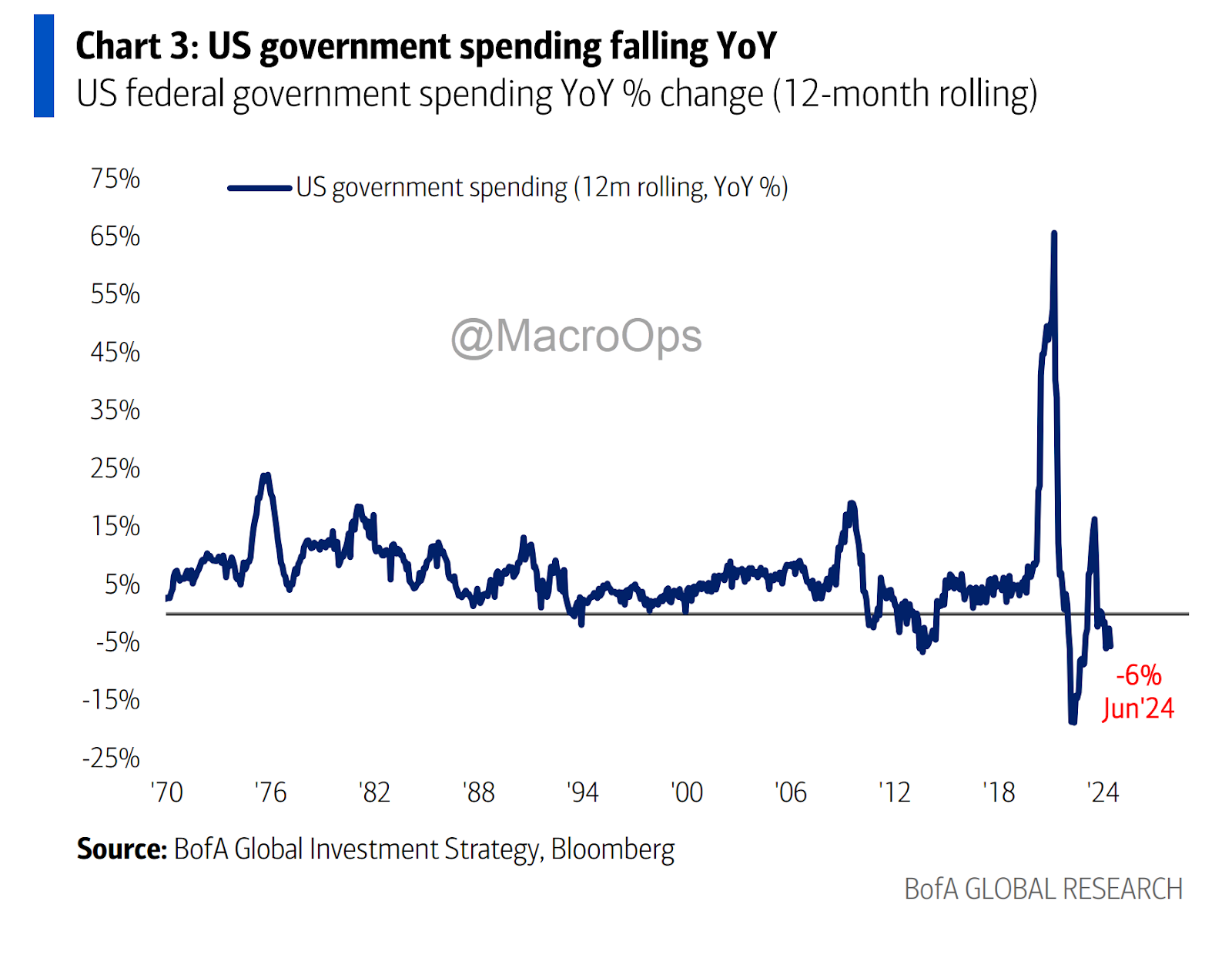

5. In markets and economics it’s not so much the level but the trend and rate of change that matters. And on that front, government spending in the US is no longer a tailwind with it declining at a -6% YoY basis.

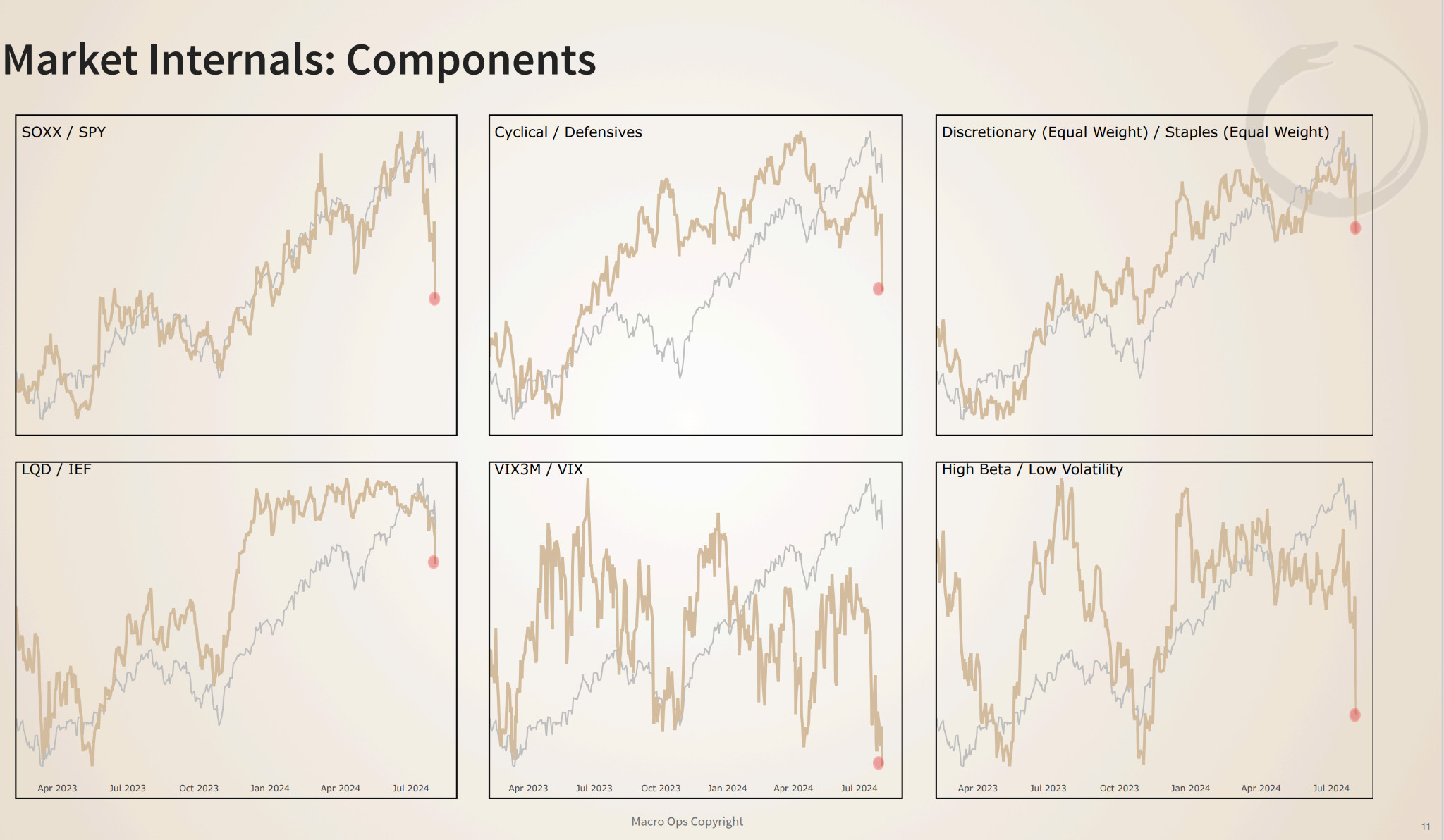

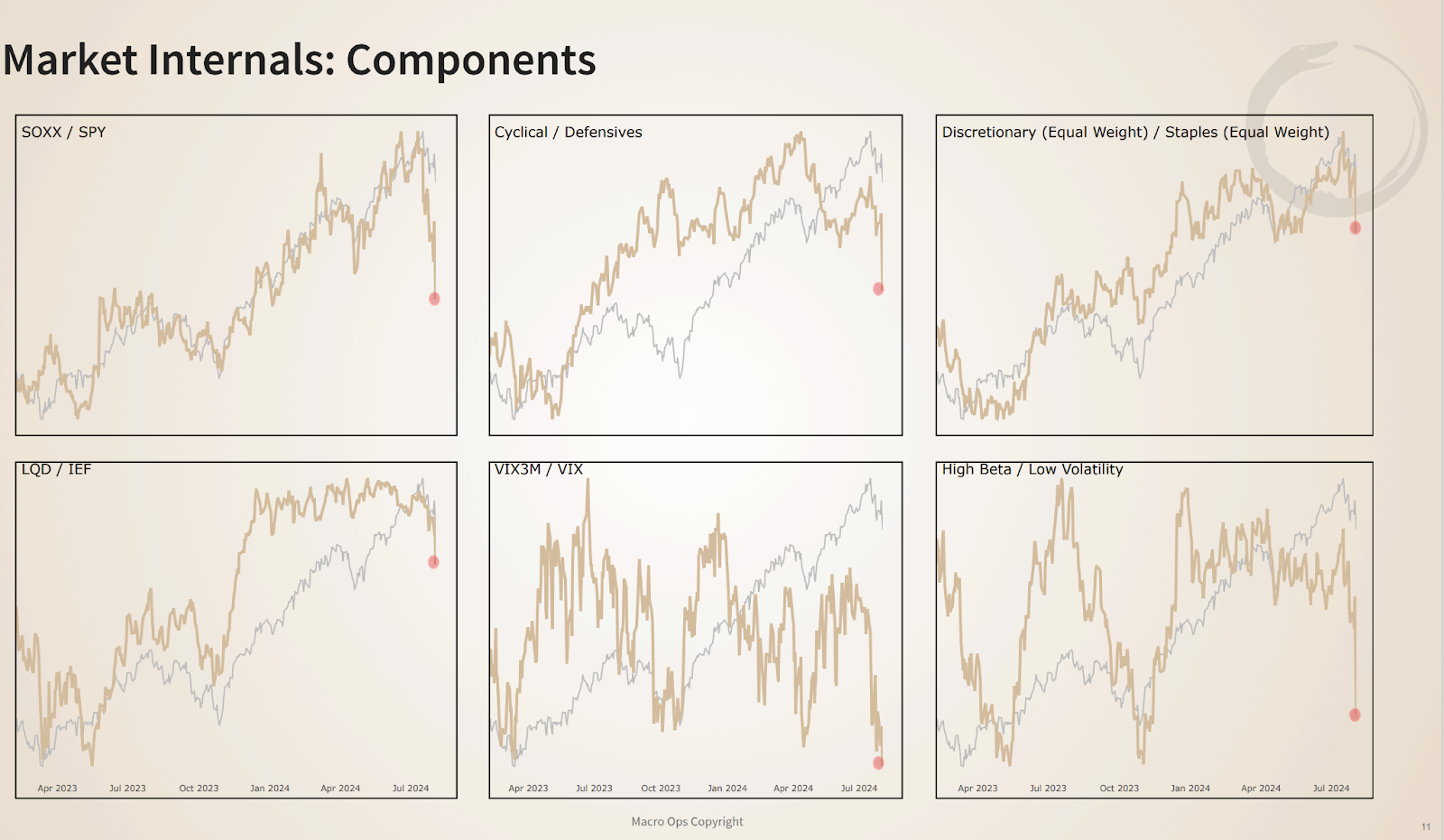

6. For the past month we’ve been pointing to the deteriorating market internals as an increasing reason to be cautious over the short-term. These negative divergences continue and we’re not interested in playing aggressively to the long side until we start to see positive confirmation from these.

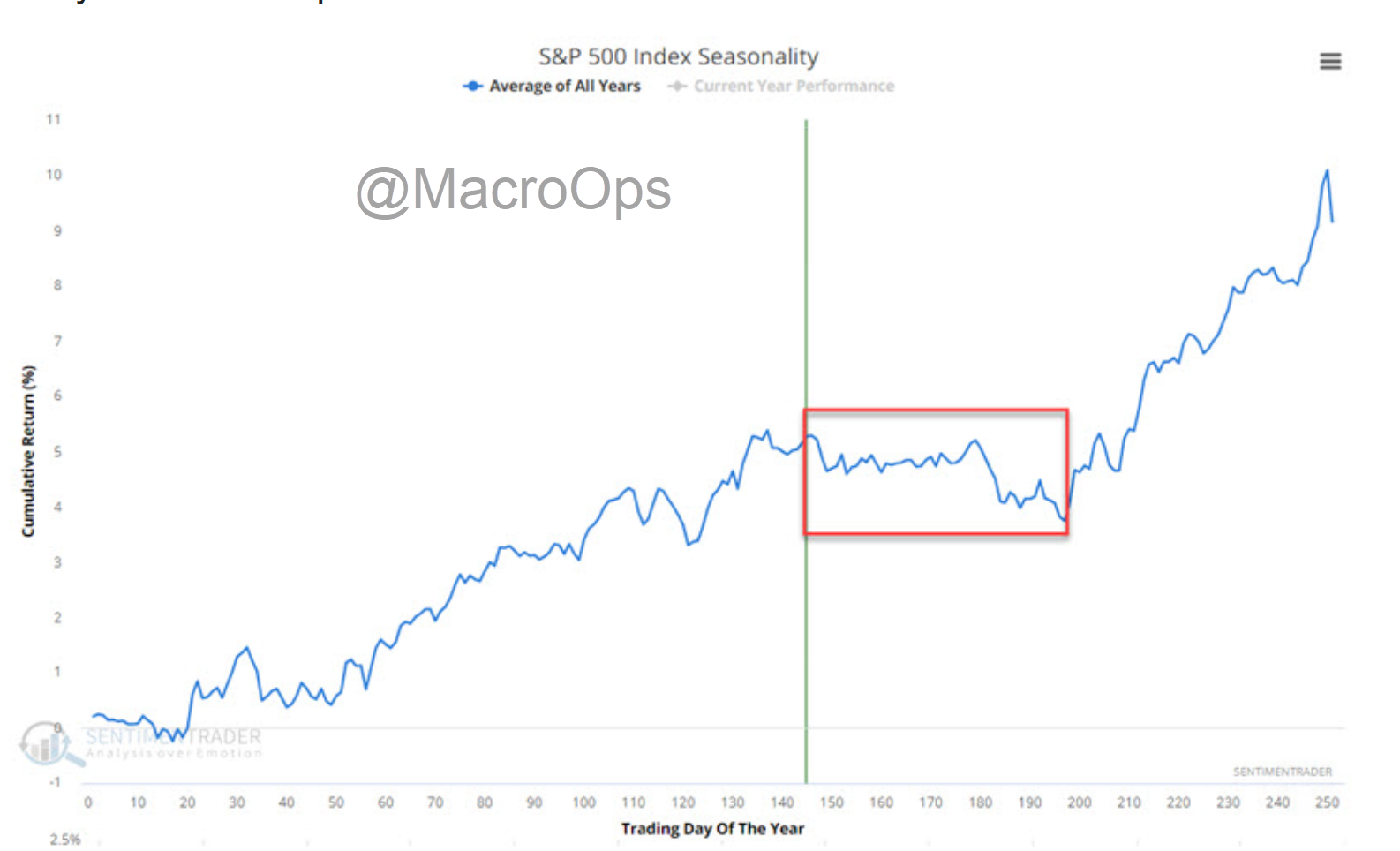

7. Additionally, we’re entering one of the weakest periods of seasonality for US equities over the next two months.

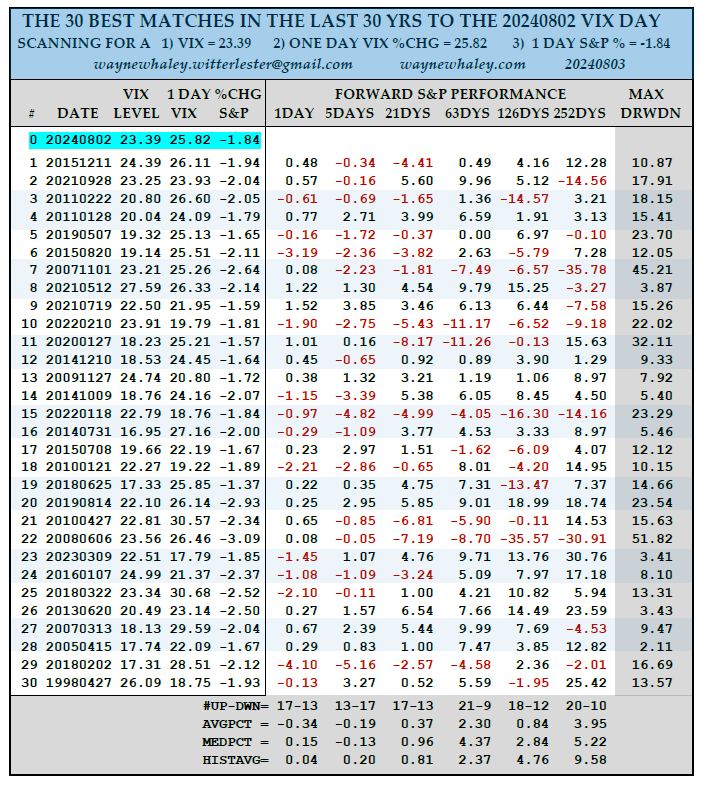

8. Some interesting stats on the VIX and what it may mean for the market from Wayne Whaley. He writes:

“On Friday, I have the Volatility Index (Vix) closing at 23.39 which is its first +20 reading since October of 2023, an accomplishment which I felt merited a review. The 23.39 was a 25.82% increase from the prior day’s 18.59 closing Vix price and, as is usually the case, occurred on a day when the S&P was down 1.84%. Searching the last 30 yrs for the 30 best matches to those three variables, namely: 1) A 23.39 Vix, 2).

“A one day Vix advance of 25.82% and 3) A 1.84% S&P one day decline resulting in the below data set listed in order of best match to those 3 parameters. The forward results are noticeably below historic norms but what grabs my attention is the fact that 20 of the 30 cases had additional double-digit losses (Max DD) from that day at some point in the next year including ten of the top 11 matches and secondly, none of those cases was the S&P bottom as they all incurred an additional loss of at least 2%.

“Collectively considering such factors would support the thesis that there has likely been enough psychological damage to the market that we are now owed at least a 3-5 week bottom building process before a meaningful advance may ensue but feel free to interpret at you choose. One of 19 studies on 14 markets shared with commentary subscribers this am.”

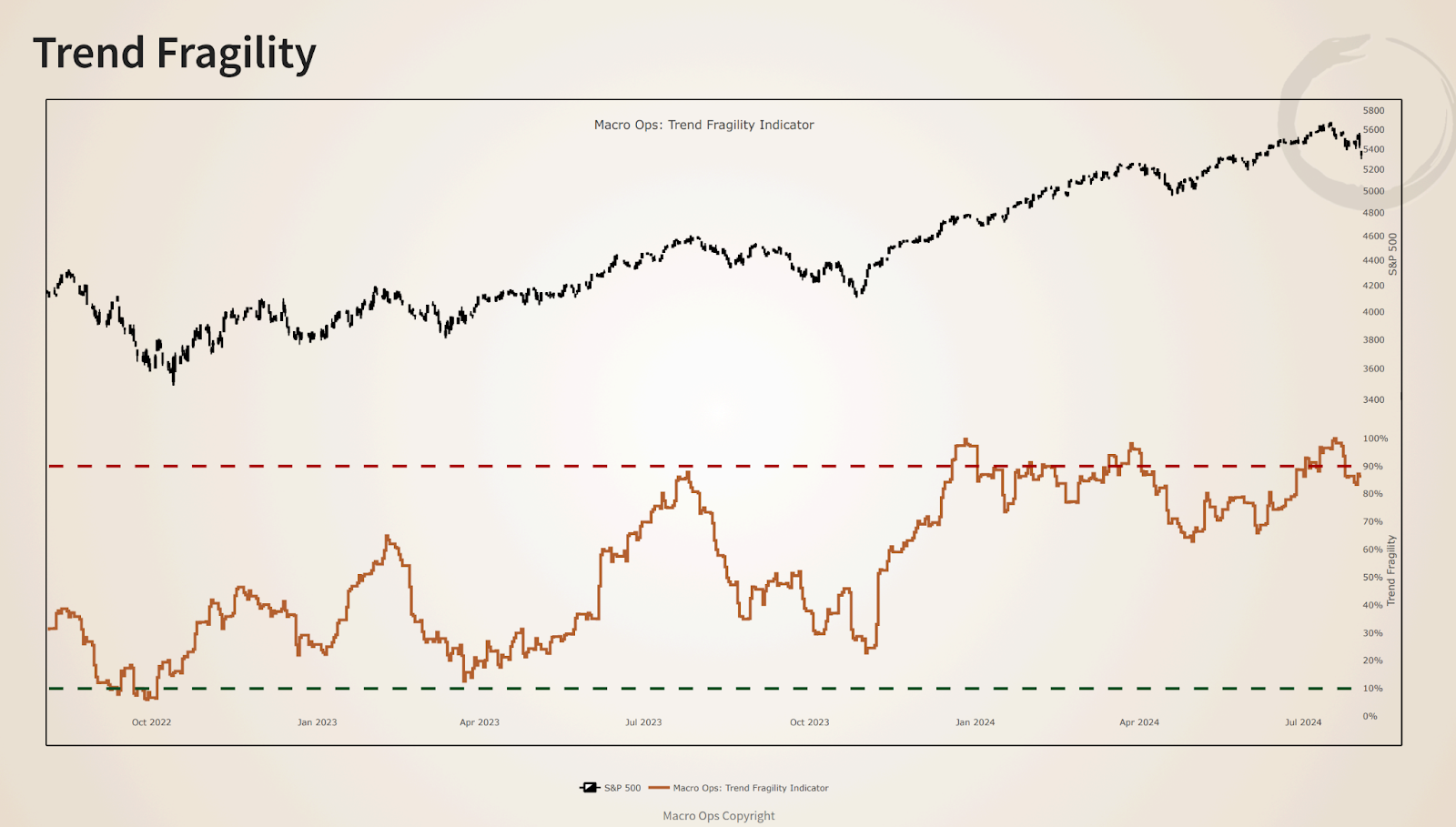

9. Our Trend Fragility indicator gave a 100% reading directly at the top of this move (indicating max fragility). And it’s still elevated at 87%. We want to see this come down to sub 70% before we turn constructive again.

10. Bonds (TLT) traded above the midline of their monthly Bollinger Band for the first time since Dec 21’ this past week.

11. They’re also breaking out to the upside from a volatility compression regime on a weekly basis.

12. My trade pitch for the week is to derisk, step away from the desk, and get out into nature. Leave the aggressive summer trading of choppy markets to the degens living in their parent’s basements… I’m in Iceland for the week visiting a few friends. Here’s the view from our hike yesterday.

Thanks for reading.