The following is a sample of our weekly Friday Macro Musings — a list of what our team is reading/studying/trading this week.

Our Recent Articles/Interviews —

Financial Sense Podcast – I did a short chat with Chris Sheridan on the Financial Sense podcast last week.

Archimedes Dollar Smile – I dig into the greenback and take a look at where it might be headed.

The Gold Bugs Were Wrong – Tyler talks why buyers of gold have been wrong since the inception of QE. And asks, were they wrong or early?

China Won’t Roll Over Until Liquidity Tightens – Tyler looks at the liquidity situation in China.

The Label Stupidity Loop – I write about the labels we adopt and their impact on how we interpret reality.

Articles I’m reading —

Sam Zell, the man known as the “Grave Dancer” since he’s made a fortune in the distressed debt market was interviewed by the CFA institute. Zell is as sharp as they come and has been in the game for a few decades now, so it’s always informative to hear his thoughts on the market and economy (link here).

He discusses commercial real estate (he thinks it’s oversupplied and near bubble territory), how he views the world through the basic lens of supply and demand, and where he thinks the next crisis will come from. Here’s’ an excerpt.

Zell has never seen a period in his lifetime with more headwinds or more questions without answers than today. He believes conventional wisdom is mistaken by looking at geopolitical risks one at a time. He tries to view each as part of a whole. “We have a different world today and there are lots of players with different values. There is enormous unsettledness,” he said, noting that this manifests itself in a lower global growth rate.

He also recently wrote a book titled Am I Being Too Subtle?. I haven’t read it myself but if any of you have, let me know if it’s worth picking up.

This week I revisited an old white paper put out by Michael Mauboussin titled Expectations Investing: Reading Stock Prices for Better Returns. Here’s the abstract and link.

Investing relies on expectations, and revisions in expectations trigger changes in stock prices. Accurately measuring expectations, therefore, is the key to improving stock selection. Expectations investing requires (1) the development of a conceptual framework, (2) a clear understanding of valuation, including cash flow, the cost of capital, and the forecast horizon, and (3) accurate estimations of price-implied expectations and expectations gaps.

It’s a good short read (only 10 pages) and talks about a very important investing concept. Not truly understanding the pricing mechanism and the embedded expectations within these prices is one of the more common errors that I see traders and investors make.

I don’t necessarily think one needs to get as granular or technical in teasing out these expectations as Michael does. But I do know that trying to suss out the embedded expectations in the market you’re analyzing is essential to winning in this game.

He also wrote a pretty good book on the topic for those of you who want to dive into it more. It’s got the same title as the article.

Video I’m watching —

Ray Dalio has been on a media blitz promoting his new book Principles.

He recently sat down with Bloomberg for a 45 minute interview where they discuss everything from his book, to the building of Bridgewater, to his economic framework and so on. Here’s the link if ya feel like watching.

I put Ray Dalio’s white paper titled How The Economic Machine Works up there with Reminiscences of a Stock Operator and Alchemy of Finance as far as works that have had an impact on my trading and understanding of the macro world.

And apparently, he’s publishing a follow up book that will be an extension of The Economic Machine sometime over the next year. I’m excited for it…

Book I’m reading —

And on that note… this week I’ve been reading Dalio’s book Principles.

I had read the old white paper on their site of the same title a number of times and figured this would be just a book version of that. But I’m happy to find that there’s been quite a bit added to the material.

The book is about, as the title suggests, Dalio’s principles. Over the last 30 years he has codified the rules that he’s used to find success on a personal level, as well as those he has used to build and run the most successful hedge fund in history.

I’m a big fan of the philosophy and highly suggest picking up the book if you’re at all interested in this type of stuff.

Here’s the intro that gives you a bit of the flavor of the book.

Before I begin telling you what I think, I want to establish that I’m a “dumb shit” who doesn’t know much relative to what I need to know. Whatever success I’ve had in life has had more to do with my knowing how to deal with my not knowing than anything I know. The most important thing I learned is an approach to life based on principles that helps me find out what’s true and what to do about it.

You see this type of radical humility amongst many of the great traders. Soros often attributed his money making powers to the fact that he fully embraced his own fallibility. He often said:

My approach works not by making valid predictions but by allowing me to correct false one.

This way of thinking is no easy habit which is why most traders get caught up playing the game of “being right” versus the one of “making money”. The first game you’re serving your ego, in the second you’re serving your capital.

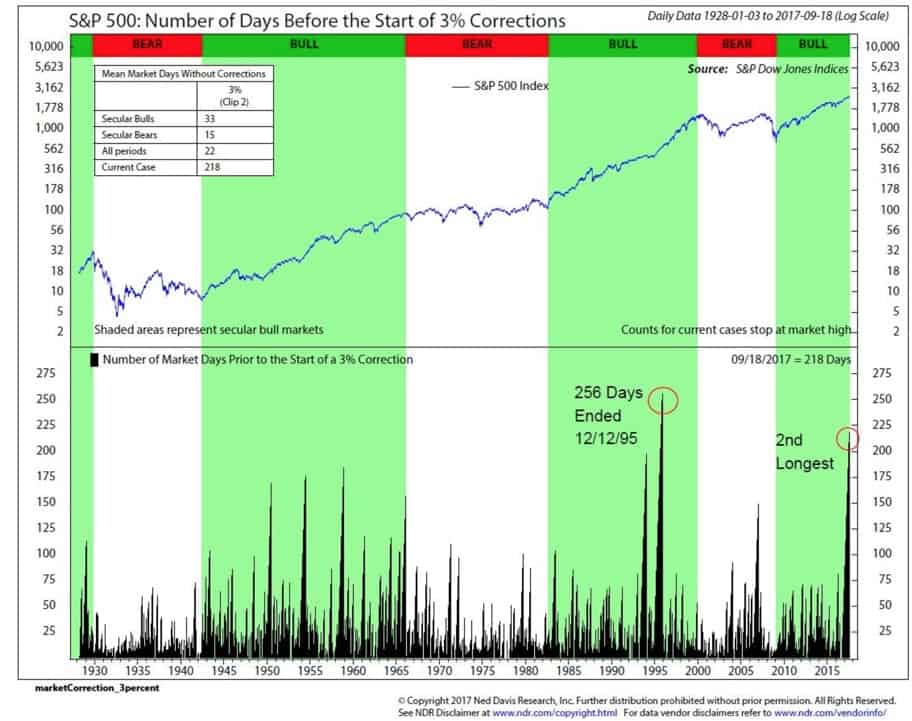

Chart I’m looking at —

We have now gone 222 days without a 3% or more correction in the S&P, making it the second longest such market streak since 95’ (chart via NDR).

That’s pretty impressive stuff. There’s a good chance that we take out the record, too. We’re only 34 days away and with liquidity flush and the credit market humming along there’s no discernible catalyst for a move lower. Though it’s not like there needs to be for a tiny 3% move.

However, we do need to keep an eye on the Nasdaq which recently broke out to the downside of an ascending wedge and is at risk of forming a major topping pattern.

Trade I’m looking at —

JD.com (JD) is China’s version of AMZN. And unlike BABA, which is mostly a platform for outside merchants to sell their wares, kind of like an EBAY, JD owns and operates its entire supply chain.

To give you a sense of the scale, the company operates over 210 warehouses in over 50 cities with an aggregate floor space of approximately four million square meters. It employs more than 120,000 employees and manages over 5,370 delivery stations and pickup stations in approximately 2,350 counties and districts across China. It’s big.

The company did over $47B in revenue over the last year which makes it the third-largest internet company, in terms of sales, right behind AMZN and GOOG.

The chart below shows the stock price (orange), annual revenues (green), TTM EPS (grey), and JD’s price to cash flow per share (blue).

The company has averaged annual revenue growth of 65% over the last 5 years but only trades at 1.3 times sales and 15x cash flow per share.

When digging into potential long-term plays, investments that I call “coffee can” trades because there’s enough of a flywheel there that you could potentially hold for 5+years, I spend a lot of time looking into who the CEO is and what kind of competitor he/she is.

They’re the ones who make the big capital allocation decisions which either widen or narrow their competitive moats. Most companies have average to sub-par leaders. CEO’s who are just there to cash out stock options and parade around their title.

But every once in awhile you come across a maniacally competitive visionary type. Think Henry Ford, Jobs, Bezos etc…

I think JD has one of these types of leaders in its Founder/CEO Liu Qiangdong.

Take a few minutes and read this recent FT interview with him (link here). He and the company have an awesome origins story. Here’s an excerpt where Liu is describing the early days of JD when it was just him operating an online retail message board and electronics stall.

“I bought an old traditional alarm clock and I put it on a wooden floor so it was like an earthquake waking me every two hours — I’d get up and answer questions online and then sleep for another two hours and then get up again,” he says. “In the first four years it was just me doing customer service and it was very good for me because I learned every detail of what our customers wanted.” He has literally lived in his offices for a decade — even as they have become increasingly luxurious.

We have no position in the company and still have plenty of digging to do. Technically the stock looks vulnerable to a selloff at the moment. This would be great as we could then buy at a much better price. We’re looking into some long-term deep OTM calls on the stock which are priced attractively.

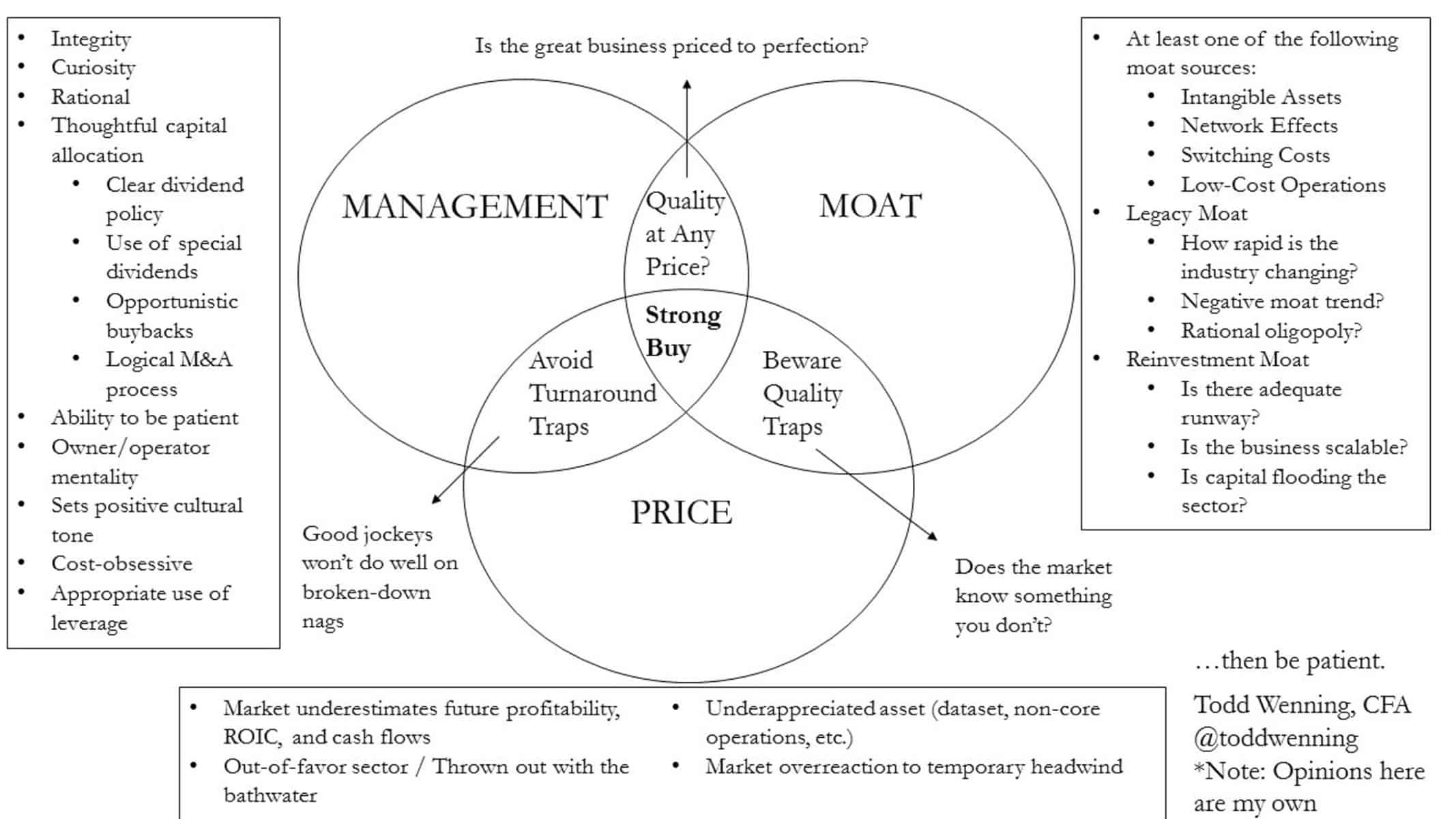

On a somewhat related note here’s a great business/stock analysis diagram shared on twitter by @toddwenning.

Quote I’m pondering —

The world is a very complex place, and if taken as anything more than guideposts, ideologies — be them free-market, socialist, or theological — are simply an impediment to understanding, a convenient excuse for the refusal to think rationally about complex questions. ~ Eric Kraus

An area of trouble for market players is when they apply a faulty precept of how they think the world should be to how it really is. They torture reality to fit their biases and ideologies and this leads to pain, not to mention loss of capital.

We all suffer from this exercise in faulty thinking on some level. God knows I have and do.

For example, I used to apply a moral judgement to central bankers and that affected my analysis of their actions and the market’s response. I see other traders, especially on fintwit, making this same mistake.

Think about how ridiculous that is. It’s illogical, right?

As traders why should we care about applying moral judgements to our “Game Masters”or market valuations sans context? We just want to defend our capital and make money. It all goes back to playing the game of being right versus making money. We should always be striving to focus on the latter and attempt to view the world and play the game of markets as ruthlessly unattached and objectively cold and calculating as possible.

So think… what are some ideas that you have about how the world is, that maybe you haven’t stress-tested against reality and perhaps aren’t serving you well?

Lastly, do yourself a favor and scroll through this excellent slidedeck that serves as a good case study on how to analyze “management” (link here).

If you’re not already, be sure to follow us on Twitter: @MacroOps and on Stocktwits: @MacroOps. I posts my mindless drivel there daily.

And if you’d like to discuss macro with the rest of the Operator community, check out our Global Macro Facebook group by clicking here.